AI’s Power Demand in 2026: How Grid Constraints from Top AI Projects Reshape Energy Strategy

The exponential growth in electricity demand from Artificial Intelligence is creating a system-level constraint that forces a strategic bifurcation in the energy sector. This dynamic is compelling companies to choose one of two paths: become pragmatic AI users focused on optimizing internal operations, like Valero, or become large-scale AI enablers, like Chevron, by building new power infrastructure to supply the burgeoning digital economy.

AI Adoption Shifts from Operational Pilots to Commercial Power Infrastructure Projects

Adoption of AI in the energy sector has sharply bifurcated from internally-focused operational efficiency pilots between 2021-2024 to massive, externally-focused infrastructure projects since 2025 designed to meet the surging electricity demand of AI itself.

- The period from 2021-2024 was defined by companies like Valero implementing digital tools for internal optimization, such as using the HTK Horizon platform for customer loyalty and partnering with Mako Networks for secure payment processing, reflecting a focus on established business processes.

- Since early 2025, the focus has pivoted to addressing AI’s energy consumption, with Valero launching 17 Generative AI pilots with C 3.ai for operational efficiency while industry majors like Microsoft and Open AI initiated the reported $500 billion Stargate project, which includes dedicated power generation.

- This shift is confirmed by traditional energy producers entering the AI power market, exemplified by Chevron’s 2025 collaboration with GE Vernova to deliver up to four gigawatts (GW) of natural gas-powered generation specifically to meet data center demand.

- The breadth of applications now ranges from direct emissions control, using AI to reduce methane slip from engines, to securing critical infrastructure with sovereign AI platforms like Indra Mind, indicating AI is moving from a back-office tool to a core component of energy security and supply.

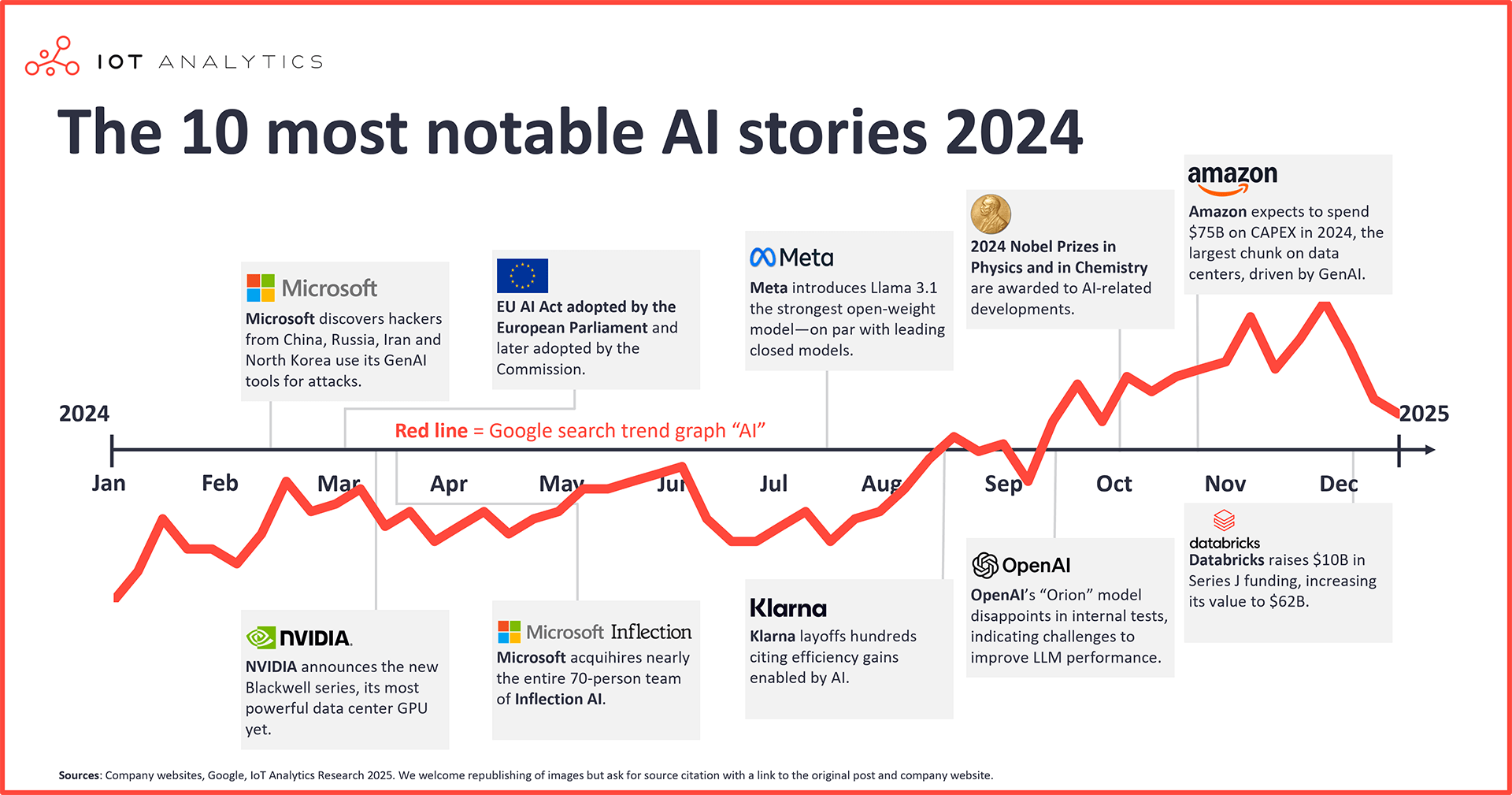

Timeline Highlights Massive AI Infrastructure Spending

This timeline shows major 2024 capital commitments for data centers and GPUs. It visually supports the article’s point about a shift from operational pilots toward large-scale infrastructure projects.

(Source: IoT Analytics)

Capital Flows Pivot to AI Power Generation, Dwarfing Operational Tech Spending

Investment patterns show a clear pivot, with massive capital commitments for new power generation and data center infrastructure beginning in 2025 now eclipsing the more incremental sustaining capital and operational technology investments that characterized prior years.

Venture Capital Investment Pivots Sharply to AI

This chart perfectly illustrates the ‘capital flows pivot’ by showing AI’s share of VC funding soaring to 71% by 2025. It provides direct evidence for the massive new investment patterns described in the section.

(Source: Deb Liu | Substack)

- Valero’s capital plans for 2025 ($1.9 billion) and 2026 ($1.7 billion) are dominated by sustaining capital, underscoring a strategy focused on optimizing existing assets rather than large-scale new energy builds.

- In contrast, the scale of investment to power AI is orders of magnitude larger, highlighted by the reported $500 billion scope of the Stargate initiative by Microsoft and Open AI, a project aimed at building out the requisite data centers and electricity supply.

- Even targeted low-carbon projects are substantial, such as the $315 million investment by Valero and Darling Ingredients in 2023 to produce Sustainable Aviation Fuel (SAF), a venture that creates a new, data-rich environment for AI optimization.

- Venture capital trends validate this shift, with AI-related investments capturing 71% of U.S. VC funding in Q 1 2025, a dramatic increase from 16% in 2021, with the bulk flowing to foundational models and their underlying infrastructure needs.

Table: Key Investments in AI and Related Energy Infrastructure (2023-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Valero 2026 Capital Plan | Jan 2026 | Allocated $1.7 billion, with $1.4 billion for sustaining business and $300 million for growth. Reinforces a focus on optimizing existing refining assets. | Seeking Alpha |

| Microsoft / Open AI (Stargate) | 2025 Onwards | Reported $500 billion initiative to build AI supercomputers and the power generation required to run them. Signals a shift toward vertically integrated energy and tech infrastructure. | Pw C |

| Valero 2025 Capital Plan | Oct 2025 | Outlined a $1.9 billion plan with $1.6 billion for sustaining capital, prioritizing throughput and reliability of its core business. | Seeking Alpha |

| Valero / Darling Ingredients (DGD) | Feb 2023 | Approved a $315 million project to produce 235 million gallons/year of Sustainable Aviation Fuel (SAF), creating a new high-tech facility where AI can optimize production. | ESG News |

Strategic Alliances Form to Bridge the AI Energy Gap

Strategic alliances have evolved from technology service agreements to fundamental energy supply partnerships, as tech firms and energy producers collaborate to solve the critical constraint of powering AI at scale.

- Between 2021 and 2024, partnerships focused on digitizing existing operations, such as Valero’s selection of Mako Networks for its distributor payment network and HTK for its loyalty program.

- Beginning in 2025, partnerships shifted to address systemic challenges, evidenced by Chevron’s alliance with GE Vernova to directly build power capacity for data centers, marking a new class of energy-tech collaboration.

- Valero’s engagement with C 3.ai across 17 pilot programs in 2025 represents a “fast-follower” strategy, leveraging a specialized AI partner to test applications without building foundational models.

- In parallel, collaborations are forming to secure the energy value chain, with Total Energies and Honeywell piloting an AI-assisted control room in November 2025 to enhance industrial autonomy and protect physical assets.

Table: Evolution of Strategic Partnerships for AI and Energy

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Total Energies / Honeywell | Nov 2025 | Piloted an AI-assisted control room to accelerate the shift to industrial autonomy, improving operator decision support and asset security. | Europétrole |

| Chevron / GE Vernova | Announced 2025 | Collaboration to deliver up to 4 GW of natural gas-powered generation, partly to meet surging electricity demand from AI data centers. | Hanwha Data Centers |

| Valero / C 3.ai | Q 1 2025 | Valero participated in 17 Generative AI pilots to explore high-impact use cases for operational efficiency and predictive maintenance across its business units. | Enki.com |

| Valero / Summit Carbon Solutions | Mar 2024 | Valero became an anchor shipper on a proposed carbon capture pipeline, agreeing to capture 3.1 million metric tons of CO 2 annually from eight ethanol plants. | Reuters |

AI’s Energy Demand Concentrates New Infrastructure Development in North America

While AI adoption for operational efficiency is global, the physical infrastructure build-out to power AI is heavily concentrated in North America, particularly the U.S., driven by the location of major tech firms and favorable conditions for energy development.

- Prior to 2025, digital transformation activities were geographically dispersed, exemplified by Valero’s loyalty program modernization in the UK (Texaco Star Rewards) and an AI-driven energy management initiative at the Globe Valero Telepark in the Philippines.

- Since 2025, major capital-intensive projects are centered in the U.S., including Chevron and GE Vernova’s plan for four GW of new gas-fired power generation and the Stargate supercomputer initiative.

- The U.S. Midwest has become a critical hub for related decarbonization infrastructure, with Valero joining both the Navigator and Summit Carbon Solutions pipeline projects to capture CO 2 from its ethanol plants across five states.

- European activity, such as the Indra Mind sovereign AI launch in Spain and the Total Energies/Honeywell pilot, demonstrates a focus on industrial autonomy and security, but at a smaller scale than the U.S. power generation build-out.

AI for Operations Reaches Commercial Scale While AI Power Infrastructure Enters High-Growth Pilot Phase

AI applications for operational efficiency and predictive maintenance have matured into commercially scalable solutions, whereas the technology and infrastructure required to power large-scale AI are in a new, high-growth, and systemically critical deployment phase.

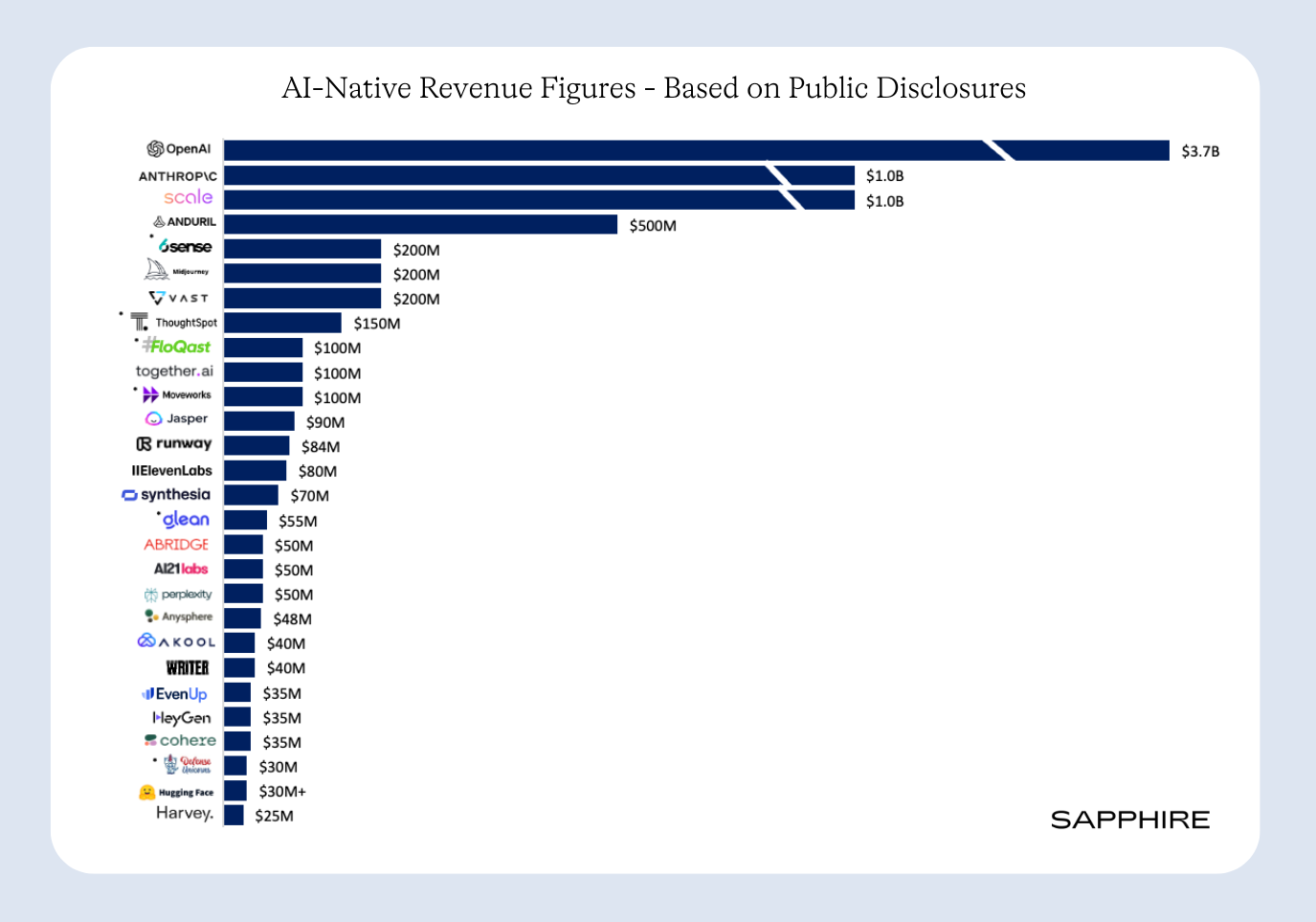

Leading AI Firms Generate Billions in Revenue

This chart demonstrates that AI applications have reached ‘commercial scale’ by showing top firms generating billions in annual revenue. This directly supports the section’s argument about the maturity of AI for operations.

(Source: Sapphire Ventures)

- Between 2021-2024, technologies like predictive maintenance and supply chain analytics moved from pilot to standard practice, with platforms like Kraken Technologies’ AI operating system serving over 70 million accounts, proving scalability in demand-side management.

- The Globe Valero Telepark initiative, which achieved up to 20% in annual energy savings, demonstrated that AI for energy management in commercial buildings was already delivering tangible ROI before 2025.

- The period from 2025 onwards is defined by the challenge of powering AI itself. Projects like Stargate and the Chevron/GE Vernova collaboration are essentially large-scale pilots for a new energy-for-AI infrastructure model, moving beyond concept to physical construction.

- A critical “Gen AI divide” has emerged, where investment in foundational models far outpaces the production of task-specific tools, signaling that while the core AI technology is advanced, its practical application and the infrastructure to support it are still maturing and face significant hurdles.

SWOT Analysis: Navigating AI’s Dual Role as Operational Tool and Energy Demand Driver

The energy sector’s engagement with AI presents a dual opportunity for internal efficiency and external market growth, but this is counterbalanced by the strategic risk of focusing on incremental gains while underestimating the systemic threat and opportunity of AI’s massive power demand.

Forecast Shows Massive AI Business Value Growth

This forecast quantifies the immense business value AI is expected to generate, especially in decision support. It highlights the scale of the ‘Opportunity’ identified in the SWOT analysis.

(Source: ImmuniWeb)

- Strengths are centered on proven efficiency gains from commercially mature AI applications, while weaknesses stem from an incremental, risk-averse approach that may fail to capture larger market shifts.

- Opportunities lie in the vast new market for powering data centers, but this is threatened by grid limitations, regulatory hurdles, and the sheer scale of investment required to meet demand.

Table: SWOT Analysis for AI in the Energy Sector

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | AI demonstrates clear ROI in niche applications like customer loyalty (HTK) and payment security (Mako Networks). | AI delivers measurable operational gains at scale, such as up to 20% energy savings (Globe Valero Telepark) and enhanced decision support (Total Energies/Honeywell pilot). | The business case for using AI for operational efficiency and cost reduction has been validated and is now considered standard practice for maintaining competitiveness. |

| Weaknesses | Adoption is fragmented, with companies focusing on isolated operational problems rather than a systemic AI strategy. | An “incrementalism” risk emerges, where companies like Valero focus on internal efficiency pilots (C 3.ai) and may miss the larger strategic play of powering the AI economy itself. | The “Gen AI divide” highlights a gap between hype and scalable business applications, showing that integrating AI remains a technical hurdle for many. |

| Opportunities | AI is seen as a tool to optimize existing assets, such as improving renewable diesel production and managing carbon capture pipelines (Navigator, Summit). | A massive new, inelastic market for electricity emerges, driven by AI data centers. Demand is projected to double to over 1, 000 TWh by 2030. | The primary opportunity shifted from using AI to being the energy source for AI. The Chevron/GE Vernova deal validates this as a new, high-growth market for energy producers. |

| Threats | Risks are primarily at the firm level, such as data security and the cost of implementing new digital systems. | The threat becomes systemic: grid instability from massive data center demand. Failure to build power infrastructure fast enough could constrain AI growth and the broader economy. | The central threat is no longer internal implementation failure but external infrastructure failure. The scale of projects like Stargate confirms the problem is real and requires trillions in investment. |

2026 Outlook: Expect Energy-Tech Mergers as AI Power Demand Outstrips Grid Capacity

The most critical trajectory for 2026 is the collision between exponential AI-driven electricity demand and finite grid capacity, which will force strategic alignment between technology firms and energy producers.

AI Infrastructure Firms Forecast Explosive Growth

The high projected revenue growth for hardware companies like Nvidia directly implies a surge in the deployment of power-hungry chips. This illustrates the demand trajectory that underpins the article’s 2026 outlook on energy constraints.

(Source: Compounding Your Wealth – Substack)

AI Model Performance Rapidly Nears Perfection

By showing AI models approaching near-perfect scores on key benchmarks, this chart provides technical evidence for the ‘Strengths’ outlined in the SWOT table. The proven capability of the underlying technology validates AI’s business case.

(Source: Sapphire Ventures)

- If data center power demand continues on the trajectory projected by Goldman Sachs and the IEA, doubling by 2030, then watch for tech giants like Microsoft, Amazon, and Google to acquire or form long-term, exclusive offtake agreements with independent power producers or even traditional energy companies.

- The primary signal confirming this trend is the Chevron and GE Vernova partnership, a blueprint for bypassing the public grid to secure dedicated, reliable power. The $500 billion reported scope of the Stargate project suggests this is becoming the default strategy for large-scale AI.

- This could be happening already, as the intense concentration of venture capital into a few AI leaders like Open AI and Scale AI provides them with the war chest needed for such infrastructure-level investments, moving them from software companies to vertically integrated technology and energy players.

- For energy executives at companies like Valero, the key decision is whether to remain an efficient user of AI for operational gains or to pivot business strategy to become a direct supplier to the power-hungry AI industry.

Frequently Asked Questions

What are the two main strategies energy companies are adopting in response to AI’s growth?

Energy companies are choosing one of two paths: becoming pragmatic AI ‘users’ or large-scale AI ‘enablers’. ‘Users’, like Valero, focus on applying AI for internal operational efficiencies, such as their 17 generative AI pilots with C3.ai. ‘Enablers’, like Chevron, are pivoting to build new power infrastructure, such as their collaboration with GE Vernova to supply up to four gigawatts of power specifically for data centers.

How has the focus of AI adoption in the energy sector shifted since 2025?

Before 2025, the focus was on using AI for internal optimization, like improving customer loyalty programs or payment processing. Since 2025, the focus has pivoted to addressing AI’s massive energy consumption. This is seen in massive, externally-focused infrastructure projects like Microsoft and OpenAI’s reported $500 billion Stargate initiative, which includes its own dedicated power generation.

Why is there a huge difference in investment scale between companies like Valero and projects like Microsoft’s Stargate?

The difference reflects their strategic choice. Valero’s investments ($1.7-$1.9 billion annually) are primarily sustaining capital to optimize existing assets. In contrast, projects like the reported $500 billion Stargate initiative are focused on building entirely new infrastructure—supercomputers and the power plants to run them—to enable the future of AI. The capital required to power the AI economy is orders of magnitude larger than what is needed for internal software optimization.

What is the main threat related to AI’s energy demand identified in the SWOT analysis?

The primary threat has shifted from internal implementation risks (like data security) to a systemic, external threat: grid instability. The massive, concentrated power demand from data centers could outstrip the grid’s capacity, potentially constraining the growth of AI and the broader economy. This makes building new power infrastructure a critical challenge.

What major trend does the article predict for 2026 in the energy and tech sectors?

The article predicts that the collision between exponential AI-driven electricity demand and finite grid capacity will force strategic alignments. It anticipates that tech giants like Microsoft, Amazon, and Google will acquire or form long-term, exclusive partnerships with power producers to secure dedicated energy, bypassing the public grid. The Chevron/GE Vernova partnership is cited as a blueprint for this emerging trend.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.