Global LNG Supply Chain Risk 2026: How Qatar’s Disruption Exposes Systemic Vulnerabilities

Industry Risk: From Anticipated Glut to Structural Deficit

The Qatar Energy force majeure has fundamentally inverted the global LNG market outlook, transforming the dominant narrative from an impending supply glut to a multi-year structural deficit defined by acute geopolitical risk. Prior to March 2026, market consensus centered on massive expansion projects in Qatar and the U.S. creating an oversupplied market; the attacks on Qatari infrastructure instantly nullified that forecast, exposing the extreme vulnerability of concentrating global energy supply in a single geographic chokepoint.

- Between 2021 and 2024, Qatar Energy focused on de-risking its North Field expansion by signing numerous 27-year supply contracts with partners like Sinopec and Total Energies, preparing the market for a wave of low-cost supply. The strategic priority was securing long-term demand for its massive production increase.

- The military attacks in early March 2026 acted as a black swan event, forcing an immediate shutdown of facilities in Ras Laffan and taking 12.8 million tonnes per annum (MTPA) of LNG offline. This single event shifted the primary market risk from future oversupply to immediate, prolonged undersupply.

- The immediate commercial fallout included a greater than 30% surge in European gas futures and secondary force majeure declarations from major traders like Shell and Total Energies, demonstrating how disruption at a single production hub cascades through the entire global value chain.

- The incident revealed that while the market was pricing for a supply surplus, it had underpriced the geopolitical risk to the physical infrastructure underpinning that supply. The estimated five-year recovery timeline validates this as a long-term structural problem, not a temporary disruption.

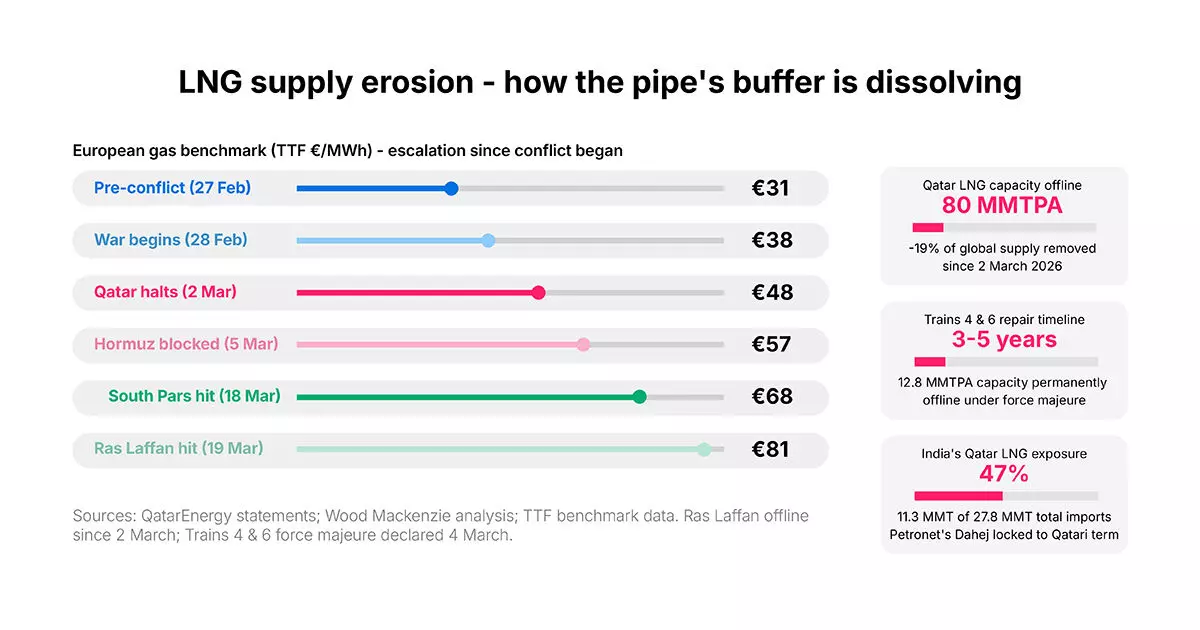

Qatar Outage Triggers European Gas Price Spike

This chart directly visualizes the core argument of the section: the March 2026 Qatar disruption inverted the market from glut to deficit, causing a dramatic price increase.

(Source: The Core)

Partnerships: Qatar’s Strategy to Underpin Global LNG Dominance

Qatar Energy’s expansion strategy hinges on embedding a select group of energy supermajors and sovereign buyers into its North Field projects through long-term joint ventures and offtake agreements. This approach secures the multi-billion-dollar financing required for its massive capacity build-out while guaranteeing market access and insulating it from spot price volatility. These partnerships, established between 2022 and 2024, are now critical for managing the crisis and planning the recovery.

- The North Field East (NFE) and North Field South (NFS) projects attracted partners like Total Energies, Shell, Exxon Mobil, Conoco Phillips, and Eni, who brought capital and technical expertise in exchange for equity stakes in the new liquefaction trains.

- China was secured as a foundational customer through state-owned Sinopec, which not only signed a historic 27-year deal for 4 MTPA but also took a direct 5% equity stake in an NFE train, aligning its interests directly with Qatar’s production.

- European energy security was a key target, with Qatar signing 27-year deals to supply France (3.5 MTPA via Total Energies) and a 15-year deal to supply Germany (2 MTPA via Conoco Phillips), positioning itself as a long-term alternative to Russian pipeline gas.

Table: Key Strategic Partnerships for Qatar’s LNG Expansion (Pre-Incident)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Sinopec (China) | April 2023 | Took a 5% stake in an 8 MTPA NFE train. Followed a 27-year deal for 4 MTPA, the longest in industry history, locking in China as a foundational buyer. | Oil Price.com |

| Total Energies (France) | October 2023 | Signed a 27-year agreement to supply France with up to 3.5 MTPA. The company was the first partner selected for the NFE expansion, investing $1.5 billion. | Oil Price.com |

| Conoco Phillips (Germany/US) | November 2022 | Secured an agreement to supply Germany with 2 MTPA for at least 15 years starting in 2026, marking a significant entry for Qatari LNG into Europe’s largest economy. | Conoco Phillips |

| Shell | October 2022 | Selected as a partner for the 16 MTPA North Field South (NFS) expansion project, building on its long-standing presence in Qatar’s energy sector. | Egypt Oil & Gas |

Geography: A Market Bifurcates Between Exposed Importers and Opportunistic Exporters

The force majeure has created a clear geographic divide in the global LNG market, severely heightening energy security risks for import-dependent nations in Europe and Asia while creating a significant commercial opportunity for U.S. LNG exporters. Before the incident, the focus was on how European and Asian buyers would absorb the coming supply wave; now, their primary challenge is replacing large, long-term contracted volumes that have vanished from the market. This dynamic highlights the core tension in the US LNG vs Qatar LNG competition.

- Nations with direct offtake agreements are most exposed, including Italy, Belgium, South Korea, and China. These countries must now enter the highly competitive and expensive spot market to secure replacement cargoes, a direct threat to their industrial competitiveness and Asia’s energy security. India, in particular, faces a supply crisis due to its high reliance on Qatari volumes.

- The United States is the primary beneficiary of the crisis. With significant operational export capacity and destination-flexible contracts, U.S. producers like Cheniere Energy and Venture Global LNG can redirect cargoes to meet the urgent demand from Europe and Asia, capturing premium pricing. The US LNG Expansion 2026 is now positioned as a critical backstop for global energy security.

- For Europe, the disruption is a second major energy shock following the cutoff of Russian pipeline gas. It reinforces the vulnerability of relying on a concentrated source of imported energy and will likely trigger a renewed push for alternative supplies and accelerated renewable energy deployment to mitigate the risk of a new European energy crisis.

Technology Maturity: Infrastructure Vulnerability Eclipses Technical Risk

The Qatar crisis is not a failure of LNG technology, which is mature and proven at scale, but a stark demonstration that even the most advanced technical systems are only as resilient as the physical infrastructure housing them. Between 2021 and 2024, the industry’s focus was on deploying established liquefaction technology for massive capacity expansions like the North Field project. The events of 2026 prove that geopolitical and security risks to centralized infrastructure are now the dominant factors governing supply reliability, superseding purely technical or operational concerns.

Attacks on LNG Facilities Highlight Infrastructure Risk

This chart quantifies the damage from attacks on Qatari infrastructure, directly supporting the section’s thesis that physical vulnerability, not technology maturity, is the dominant risk.

(Source: Gulf Times)

- The technology used in Qatar’s existing and planned LNG trains represents decades of refinement in cryogenics and natural gas processing. The construction of the North Field East and South projects, awarded to engineering giants like Technip Energies and Chiyoda, was based on proven, commercially available liquefaction processes.

- The disruption was caused by military strikes on operating facilities, not by a malfunction or technical limitation of the LNG production process itself. The damage to specific trains (S 4 and S 6) requires extensive physical reconstruction, highlighting a vulnerability that cannot be solved with process optimization or software.

- The secondary impact on helium supply, which led U.S. distributor Airgas to declare force majeure, further illustrates this dependency. Helium is extracted during the LNG cooling process, meaning its supply is directly tied to the operational status of the physical liquefaction plant.

SWOT Analysis: Qatar’s LNG Disruption

The force majeure event has recast the strategic strengths, weaknesses, opportunities, and threats facing the global LNG market. The primary change is the validation of a long-standing threat, shifting the market’s focus from economic competition to physical supply security.

- Strengths: Qatar’s unparalleled low production cost and vast reserves remain its core long-term advantage, positioning it to reclaim market share once capacity is restored.

- Weaknesses: The high concentration of critical energy infrastructure in a single, geopolitically volatile location has been validated as a systemic weakness.

- Opportunities: U.S. exporters are presented with a multi-year opportunity to secure market share and long-term contracts at premium prices.

- Threats: The primary threat has evolved from price competition to direct military action and the risk of long-term demand destruction as buyers accelerate their transition to other energy sources.

Table: SWOT Analysis of the Global LNG Market Post-Disruption

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Qatar’s low production cost ($0.3/mm Btu) and massive North Field reserves positioned it to dominate the future market. | Low production cost remains a strategic asset for post-recovery competition. U.S. market flexibility and scale become a key strength. | The crisis validated that low cost is irrelevant without supply security. The U.S. emerges as the key swing supplier due to its operational scale and political stability. |

| Weaknesses | Theoretical risk of supply chain disruption due to geopolitical tensions in the Persian Gulf. High dependence of European and Asian economies on LNG imports. | The concentration of 77 MTPA of capacity at Ras Laffan is confirmed as a critical single point of failure for the global market. | A theoretical risk became a realized, multi-year disruption, proving that geographic concentration is the market’s primary structural weakness. |

| Opportunities | U.S. LNG projects raced to sign contracts ahead of the anticipated Qatari supply glut. European buyers sought to diversify from Russian gas. | U.S. exporters (Cheniere, Venture Global) see stock gains and can command premium prices for spot cargoes to replace lost Qatari volumes. | The opportunity for U.S. LNG shifted from competing with future Qatari supply to immediately backfilling a 12.8 MTPA structural deficit. |

| Threats | A potential price war triggered by a post-2026 oversupply from Qatar and U.S. expansions. Slowing demand growth in mature markets. | Direct military attacks on critical energy infrastructure. Long-term demand destruction as buyers accelerate investments in renewables for energy security. | The primary threat shifted from economic (price war) to existential (physical destruction of supply). The idea that the LNG transition fuel is over in terms of reliability has gained traction. |

Scenario Modelling and Summary

If geopolitical instability in the Middle East persists, watch for a strategic acceleration of final investment decisions (FIDs) for LNG export projects in politically stable jurisdictions, particularly the United States. The Qatar crisis serves as a powerful, price-insensitive catalyst for buyers to prioritize supply chain security over pure cost optimization, fundamentally re-weighting the calculus for long-term energy procurement.

US LNG Capacity Rises Amid Market Shift

This chart supports a key finding in the SWOT table, illustrating the rise of U.S. suppliers like Venture Global, which emerges as a key strength and swing supplier post-disruption.

(Source: Crack The Market – Substack)

- Signal to Watch: A surge in new long-term contracts signed by European and Asian buyers with U.S. LNG developers, even at prices higher than those historically offered by Qatar. This would confirm a structural shift toward valuing geopolitical stability.

- Signal to Watch: Increased investment in LNG import terminal capacity in Europe and Asia, designed to accommodate more diverse supply sources beyond the Middle East.

- Potential Development: A renewed policy push within major importing nations (e.g., Germany, Japan, South Korea) to accelerate domestic energy production and renewable energy targets as a direct response to the unreliability of fossil fuel imports.

Frequently Asked Questions

What caused the global LNG supply disruption described in the report?

The disruption was caused by military attacks in early March 2026 on Qatar’s LNG facilities in Ras Laffan. This black swan event was not a technical failure but a physical attack on infrastructure, which forced an immediate shutdown and took 12.8 million tonnes per annum (MTPA) of LNG offline.

How did this event change the outlook for the global LNG market?

It fundamentally inverted the market outlook, transforming the dominant forecast of an impending supply glut into a multi-year structural deficit. Before the incident, the market expected an oversupply from new projects in Qatar and the U.S. Afterward, the primary risk shifted from future oversupply and price competition to an immediate, prolonged undersupply and physical supply security.

Which countries or companies are most negatively affected by the Qatar disruption?

The most exposed are import-dependent nations with direct offtake agreements, particularly in Europe and Asia. The report specifically names Italy, Belgium, South Korea, China, and India as facing heightened energy security risks. Major energy traders like Shell and TotalEnergies, who were partners in Qatar’s expansion, also had to declare secondary force majeure declarations.

Why is the United States considered the primary beneficiary of this crisis?

The U.S. is the primary beneficiary because its LNG producers, such as Cheniere Energy and Venture Global, have significant operational export capacity and destination-flexible contracts. This allows them to redirect cargoes to fill the supply gap in Europe and Asia, capturing premium prices and positioning U.S. LNG as a critical backstop for global energy security.

What was Qatar’s strategy for its LNG expansion before the incident?

Prior to the disruption, Qatar’s strategy was focused on securing long-term demand and financing for its massive North Field expansion. It did this by signing numerous long-duration (up to 27-year) supply contracts and forming partnerships with energy supermajors (like TotalEnergies, Shell, ExxonMobil) and key state-owned buyers (like China’s Sinopec), thereby locking in foundational customers and de-risking its multi-billion-dollar investment.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.