Bloom Energy SOFC Data Center Agreements, $5 B Brookfield Deal, 1 GW AEP Partnership, and Major Deployments (2021 to 2026)

SOFC Hybridization, Bloom Energy Solves Data Center Load Volatility

The definitive solution to Solid Oxide Fuel Cell (SOFC) degradation under volatile data center loads is not a materials science breakthrough, but system-level hybridization. The market has validated the pairing of SOFCs with Battery Energy Storage Systems (BESS) as the commercially viable architecture to shield the fuel cell from damaging power fluctuations. This approach leverages the SOFC for high-efficiency baseload power while the BESS absorbs the rapid, high-ramp-rate load swings characteristic of AI workloads, effectively engineering the degradation risk out of the system.

- Between 2021 and 2024, the primary focus was on mitigating degradation through material science and advanced controls, with companies like Microsoft testing SOFCs for backup power and academic research focused on redox cycling and thermal stress. The problem was framed as an inherent weakness of the SOFC core technology.

- From 2025 onwards, the strategy shifted decisively to system integration. Bloom Energy’s landmark agreements with American Electric Power (AEP) and Brookfield are predicated on this hybrid model, where the SOFC is insulated from volatility. This pivot treats the fuel cell as a component within a larger, more resilient power system, accelerating commercial adoption without waiting for a perfect, cycle-proof cell.

- The extreme power profile of AI workloads, with swings from 20% to 150% in milliseconds, made standalone SOFCs commercially non-viable for primary power. The SOFC+BESS model is now the standard for providing the required reliability and power quality, moving the technology from a niche backup application to a primary power source for hyperscalers.

Schematic Shows Hybrid SOFC System Architecture

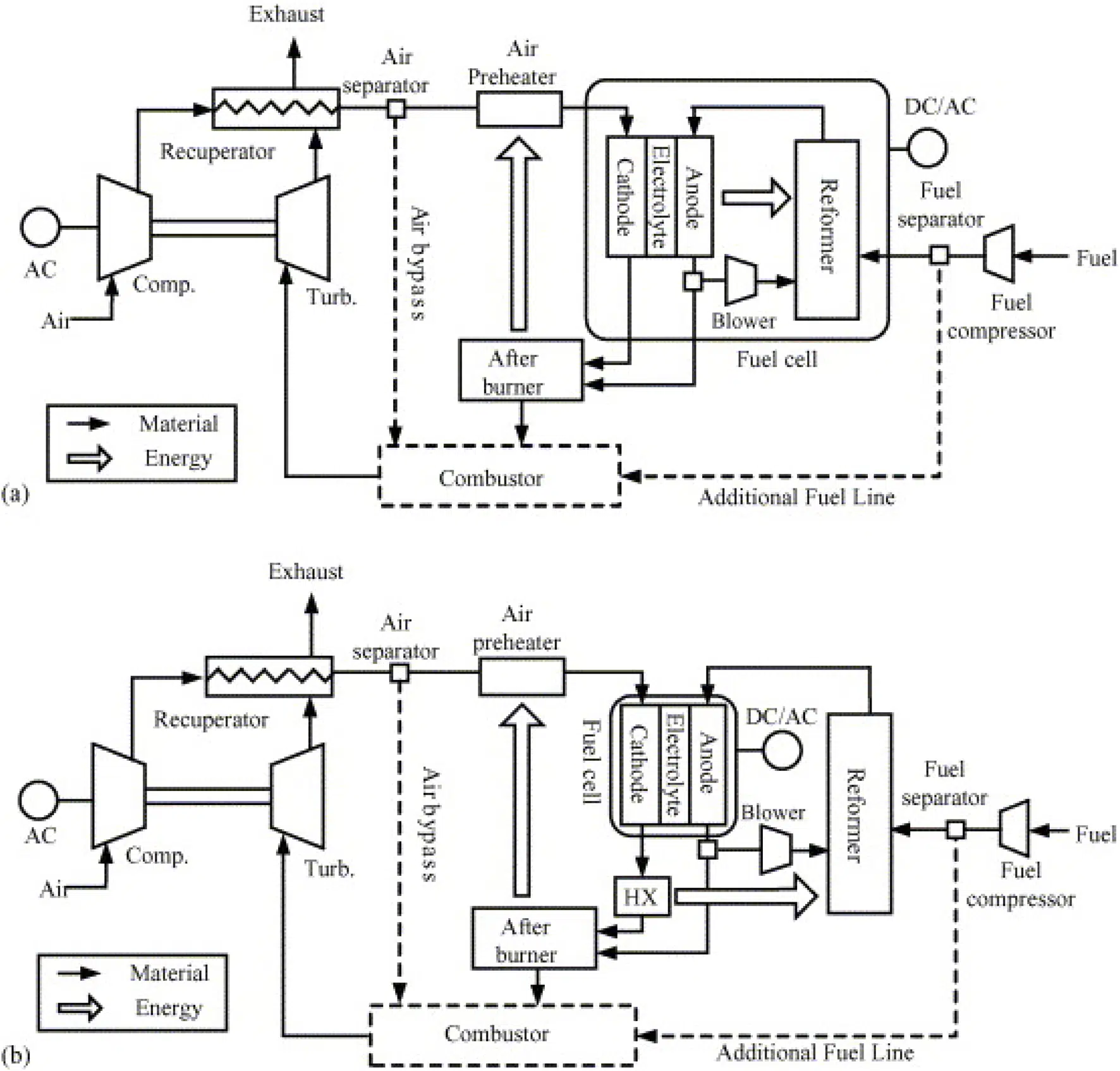

This chart’s schematic of a hybrid SOFC system directly illustrates the ‘system-level hybridization’ concept that is central to the section’s discussion on solving load volatility.

(Source: Frontiers)

$7.65 B in Deals, Bloom Energy Cements Data Center Market Position

Investment in the Solid Oxide Fuel Cells market for data centers has matured from technology-focused R&D funding to massive, multi-billion-dollar infrastructure financing deals designed for large-scale deployment. This financial shift validates the technology’s bankability and signals market acceptance of SOFCs as a critical component of data center infrastructure, driven by the urgent need for grid-independent power for AI. These agreements focus on deploying power capacity, not just developing technology.

- The $5 billion infrastructure partnership between Bloom Energy and Brookfield in 2026 marks a turning point, creating a dedicated financial vehicle to deploy SOFC technology at AI data centers globally. This moves financing from corporate balance sheets to project-based infrastructure funding.

- Bloom Energy‘s $2.65 billion, 20-year offtake agreement with AEP for up to 1 GW of SOFCs further solidifies this trend. A major utility is now underwriting the deployment of SOFCs as a core solution for its data center customers.

- Similarly, Fuel Cell Energy’s partnership with SDCL to develop, finance, and deploy 450 MW of fuel cell projects targets the same market, confirming that the industry-wide financing model is shifting towards large-scale, third-party-financed energy-as-a-service contracts.

Table: Major SOFC Financial Commitments and Investments for Data Centers

| Company / Partnership | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bloom Energy / AEP | 2026 | $2.65 billion, 20-year offtake agreement to supply up to 1 GW of SOFCs for data center sites within AEP‘s service territory. Secures long-term revenue and validates utility-scale adoption. | Climate Drift |

| Bloom Energy / Brookfield | 2026 | $5 billion infrastructure partnership to finance and deploy Bloom‘s SOFC technology at AI data centers globally. Creates a dedicated capital pool for rapid deployment. | Data Center Dynamics |

| Fuel Cell Energy / SDCL | 2026 | Partnership to develop and finance 450 MW of fuel cell power projects, with a strong focus on the data center market. Aims to provide clean power-as-a-service. | Data Center Knowledge |

Bloom Energy’s AEP and Brookfield Deals, 1 GW+ for AI Data Centers

Strategic partnerships have evolved from small-scale technology pilots to multi-gigawatt, multi-billion-dollar deployment agreements with utilities, infrastructure funds, and data center operators. This shift demonstrates that key stakeholders now view SOFCs as a mature, scalable, and essential solution for the AI-driven power crisis, rather than a technology requiring further validation. The focus is on execution and deployment at an unprecedented scale.

- The 2021-2024 period was characterized by evaluation partnerships, such as Equinix‘s project with Vertiv to test the integration of natural gas SOFCs with UPS systems. These were proof-of-concept initiatives aimed at validating technical feasibility.

- By 2025-2026, partnerships became commercially definitive. The Bloom Energy–AEP agreement for 1 GW of power and the Bloom Energy–Brookfield $5 billion financing deal represent a transition to industrial-scale deployment, treating SOFCs as a standard asset class for data center power.

- Partnerships are also forming around key sub-components and market entry. The collaboration between Ceres Power, Doosan, and Delta Electronics to develop megawatt-scale systems for AI data centers illustrates a strategy to penetrate the market through licensing and co-development, targeting production by late 2026.

Table: Key SOFC Data Center Partnerships and Alliances

| Lead Company / Partner(s) | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bloom Energy / AEP | 2026 | Utility partnership to supply up to 1 GW of SOFCs for data centers, providing a grid-independent power solution to AEP‘s large industrial customers. | AEP |

| Ceres Power / Delta Electronics | 2025 | Delta is developing megawatt-scale SOFC systems using Ceres‘ technology for AI data centers, aiming for production by the end of 2026. This expands Ceres‘ reach via a licensing model. | Investing.com |

| SK ecoplant / GDS Holdings | 2023 | Collaboration to trial and promote SOFC power solutions for data centers in Southeast Asia, starting in Singapore, to address the region’s growing power needs. | GDS |

| Equinix / Vertiv | 2021 | Development project to validate the integration of SOFCs with UPS systems and lithium-ion batteries, proving the hybrid power concept for data center resiliency. | Data Center Knowledge |

US vs. Asia, Bloom Energy and SK ecoplant Target Data Center Growth

The United States is the undisputed leader in large-scale SOFC deployment for data centers, driven by the immediate and immense power demands of its domestic AI industry and established players like Bloom Energy. However, strategic partnerships and initial deployments in Asia, particularly in power-constrained markets like Singapore, signal that this region is the next major frontier for growth, with companies like SK ecoplant and Ceres Power establishing an early foothold.

- North America dominates current commercial activity, highlighted by Bloom Energy’s multi-gigawatt agreements and deployments for customers like Intel in Silicon Valley. This is a direct response to grid congestion and delayed interconnection queues in major US data center hubs.

- In Asia, the approach is currently more focused on establishing market presence through strategic trials and partnerships. SK ecoplant‘s collaboration with GDS in Singapore and Day One‘s launch of a hydrogen-powered SOFC data center are foundational projects aimed at proving the technology’s viability in the region.

- The technology licensing model is a key vector for Asian market entry. Ceres Power‘s partnerships with Korean firm Doosan and Taiwanese firm Delta Electronics allow it to leverage the manufacturing scale of established industrial giants to serve the Asian data center market.

SOFC+BESS Commercial Scale, Bloom Energy Bypasses Degradation Risk

The technology for powering data centers with SOFCs has matured from a component-level challenge to a commercially scalable, system-level solution. The integration of SOFCs with BESS is no longer a pilot concept but a validated, bankable architecture being deployed at the gigawatt scale. This hybrid approach effectively circumvents the intrinsic material limitations of SOFCs under dynamic loads, allowing the market to move forward without waiting for fundamental breakthroughs in ceramic engineering.

Schematic Details SOFC Hybrid System Operation

This schematic details a hybrid SOFC system, visually explaining the ‘validated, bankable architecture’ discussed in the section for bypassing degradation risk at commercial scale.

(Source: Frontiers)

- The period from 2021-2024 was defined by proving technical viability. Research focused on material durability, such as metal-supported SOFCs from Weichai Power, and system-level proofs of concept, like Microsoft‘s 3 MW backup power test.

- In 2025-2026, the technology achieved commercial validation at scale. The Bloom Energy–AEP 1 GW agreement is not for a future technology; it is for an existing, commercially available system. This signals the technology has crossed the chasm from development to industrial deployment.

- The market’s acceptance of the hybrid model as the de-facto standard has shifted the key challenge from technology risk to execution risk. The primary constraints are now manufacturing capacity and the speed of deployment, not the performance or reliability of the SOFC+BESS system itself. Other innovations, like reversible SOFCs from Elcogen, add flexibility but the core power solution is now established.

SWOT Analysis of Bloom Energy’s SOFC Data Center Strategy

The strategic position of SOFC technology for data centers is defined by a clear strength in efficiency and reliability, countered by a significant weakness in upfront capital cost. The unprecedented power demand from AI creates a massive market opportunity, but the primary threat is the ability of manufacturers to scale production and supply chains to meet this demand.

Table: SWOT Analysis for SOFCs in the Data Center Market

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | High electrical efficiency (50-60%) and low emissions compared to diesel generators, primarily for baseload applications. | Proven reliability in a hybrid SOFC+BESS configuration, enabling primary power for volatile AI loads. High efficiency provides a strong TCO advantage. | The technology’s core efficiency advantage was successfully combined with a system-level solution (BESS) to overcome its primary operational weakness (load following). |

| Weakness | High CAPEX and susceptibility to degradation from thermal and redox cycling under the variable loads of data centers. | High capital cost (approx. $4, 000/k W) remains a barrier, though the focus is shifting to Total Cost of Ownership (TCO) and speed of deployment. | The degradation weakness was commercially mitigated by hybridization. High CAPEX remains the primary challenge, though it is becoming less of a deterrent due to the urgency of AI power needs. |

| Opportunity | Growing data center market and corporate ESG goals create demand for cleaner on-site power, mainly for backup or stable baseload. | Explosive, grid-breaking power demand from AI makes grid-independent, rapidly deployable power a necessity. At least 25% of new demand may be met by behind-the-meter solutions. | The opportunity grew exponentially with AI. SOFCs shifted from being a “green” alternative to an “enabling” technology for AI infrastructure that the grid cannot support. |

| Threat | Competition from other technologies like PEM fuel cells and the established position of diesel generators for backup power. | Manufacturing scalability and supply chain constraints to meet multi-gigawatt orders. Ability to deliver on massive deals with AEP and Brookfield is the key execution risk. | The primary threat shifted from technological competition to industrial execution. The challenge is no longer about proving the technology but about building it fast enough. |

Scenario Modeling for Bloom Energy and the SOFC Market in 2026

The single most critical factor for the SOFC market in the year ahead is the manufacturing and supply chain execution of industry leaders, particularly Bloom Energy. The technology’s viability and market fit for AI data centers are no longer in question; the defining variable is the ability to scale production to meet the multi-gigawatt demand pipeline that has been secured through recent landmark agreements. Failure to deliver on these contracts would create a significant opening for competing technologies.

- If this happens: Bloom Energy and its key suppliers announce new manufacturing plant expansions or long-term raw material agreements in the next 6-12 months. Watch this: These announcements would signal that the supply chain is scaling to meet the demand from the AEP and Brookfield deals, de-risking execution and solidifying Bloom‘s market leadership. These could be happening: Confidence in the SOFC sector would increase, likely leading to more utilities and infrastructure funds structuring similar large-scale deployment partnerships.

- If this happens: Reports of project delays emerge, citing equipment lead times or component shortages. Watch this: Any slippage in deployment timelines for major projects would be a critical negative signal, indicating that manufacturing capacity is a significant bottleneck. These could be happening: Data center developers may be forced to turn to less efficient but more readily available technologies like natural gas engines, or face costly delays in bringing new AI capacity online. This could temper the market’s growth projections.

The questions your competitors are already asking

This report covers one angle of SOFC commercialization for data center power. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the SOFC for data centers market?

- What is the status of Bloom Energy’s 1 GW AEP partnership and $5 B Brookfield deal since the announcements?

- What is the outlook for SOFC+BESS hybrid deployment in AI data centers by 2030?

- Which hyperscalers and colocation providers are adopting the SOFC+BESS model for primary power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.