Thermal Battery Industrial Heat, 5 GWh Antora Project with POET, and $10/k Wh CAPEX Target (2021 to 2026)

Industrial Heat Projects, Antora 5 GWh Plant Validates Commercial Scale

The application of thermal batteries has decisively moved from theoretical cost models and pilot-scale tests to the first commercial, GWh-scale deployments for industrial decarbonization. The commissioning of the 5 GWh “Project Big Stone” in May 2026 marks a critical inflection point, validating thermal storage as a direct replacement for fossil-fuel-fired boilers in process manufacturing, a sector that was previously a major challenge for electrification.

- Between 2021 and 2024, the market focused on defining the technical and economic potential of Long-Duration Energy Storage (LDES). Reports from the U.S. Department of Energy established cost reduction targets, aiming to lower LDES CAPEX by 45-55% by 2030 from a baseline of $1, 100–$1, 400 per k W. The conversation was dominated by future pathways and the need for policy support to de-risk first-of-a-kind projects.

- The period from 2025 to today demonstrates a material shift to execution. The Antora Energy and POET project in South Dakota provides the first real-world data point for a GWh-scale thermal battery, targeting a Levelized Cost of Storage (LCOS) between $0.05 and $0.10 per k Wh. This project directly leverages low-cost wind power to provide 24/7 process heat, proving the business case enabled by earlier policy incentives.

- The diversity of applications is also now clear. While earlier discussions centered on grid-scale electricity storage, the Antora project confirms the primary value proposition is displacing natural gas for industrial heat. This specialization distinguishes thermal energy storage from lithium-ion BESS, which remains focused on shorter-duration grid services. The successful operation validates sensible heat storage as a high Technology Readiness Level (TRL 8-9) solution.

Antora Installs GWh-Scale Thermal Battery System

The chart’s headline directly aligns with the section’s focus on Antora’s GWh-scale plant and its validation of commercial-scale operations. This visual evidence supports the narrative that Antora is executing large industrial heat projects.

(Source: LinkedIn)

$500 B in IRA Incentives, Antora Capitalizes on Federal Tax Credits

Federal policy, specifically the Inflation Reduction Act (IRA), has been the primary financial catalyst that unlocked the commercial viability of standalone thermal storage for industrial use. Before the IRA, storage projects typically required co-location with renewable generation to be eligible for tax credits, creating a barrier for industrial facilities wanting to draw low-cost power directly from the grid. The standalone Investment Tax Credit (ITC) created a new, viable business model.

- The IRA, passed in 2022, allocated an estimated $369 billion to $500 billion in clean energy incentives, with the standalone storage ITC being the most critical provision for this market. This allowed project developers to claim a 30% tax credit on storage systems, regardless of their power source, making it economical to capture zero- or negative-priced grid electricity.

- The Advanced Energy Project Credit (48 C) provided a further layer of support, offering $4 billion in credits specifically for projects that establish or re-equip industrial facilities to reduce greenhouse gas emissions. This directly applies to retrofitting a biofuel plant like POET’s with a thermal battery to replace fossil-fuel boilers.

- These incentives created the necessary financial de-risking for capital providers and industrial partners to back large-scale projects. Securing long-term offtake agreements, where an industrial user guarantees the purchase of heat for 15-20 years, became feasible once the project economics were improved by the ITC. The Antora-POET project serves as the model for this structure.

Table: Key Financial and Policy Catalysts for Thermal Storage

| Policy / Incentive | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Project Big Stone Commissioning | May 2026 | Antora and POET commissioned a 5 GWh thermal battery. The project validates the bankability of large-scale thermal storage, leveraging low-cost renewables to displace fossil fuels in industrial bio-processing. | Associated Press |

| Advanced Energy Project Credit (48 C) | 2023 | Provided $4 billion in tax credits (up to 30%) for industrial decarbonization projects. This directly incentivized retrofits of existing manufacturing facilities, such as replacing boilers with thermal batteries. | U.S. Department of the Treasury |

| Inflation Reduction Act (IRA) | 2022 | Introduced the standalone energy storage Investment Tax Credit (ITC), allowing projects to receive up to a 30% credit without being tied to a generation asset. This unlocked the business case for using grid electricity to power industrial heat storage. | Mc Kinsey |

US Industrial Heartland, Antora and POET Center on South Dakota

The geographic focus for large-scale thermal battery deployment is concentrating in regions with a combination of high industrial heat demand and access to low-cost, intermittent renewable energy. The selection of Big Stone City, South Dakota for the Antora-POET project is a strategic decision, placing the facility in a location with abundant wind resources and a significant industrial offtaker, which provides a replicable model for other industrial zones.

- From 2021 to 2024, discussions around LDES geography were broad, often focusing on grid-constrained areas like California or regions with ambitious renewable targets. The actual deployment of LDES technologies like Compressed Air Energy Storage (CAES) was limited by geological constraints, while flow batteries like those developed by VRB Energy were still in earlier commercial stages.

- The commissioning of Project Big Stone in 2026 anchors the U.S. Midwest as a prime territory for industrial heat decarbonization. South Dakota’s significant wind generation creates periods of very low-cost electricity that the thermal battery can capture and store, creating a strong economic case that is less dependent on grid service revenue streams common in other markets.

- While the Antora project is a U.S. milestone, it is compared to other large storage projects globally, such as the 1 GWh Oneida Energy Storage project in Canada, a lithium-ion system commissioned in 2025. This comparison highlights the diverging applications: electrochemical batteries for grid electricity services versus thermal batteries for dedicated industrial heat, defining separate geographic and market opportunities.

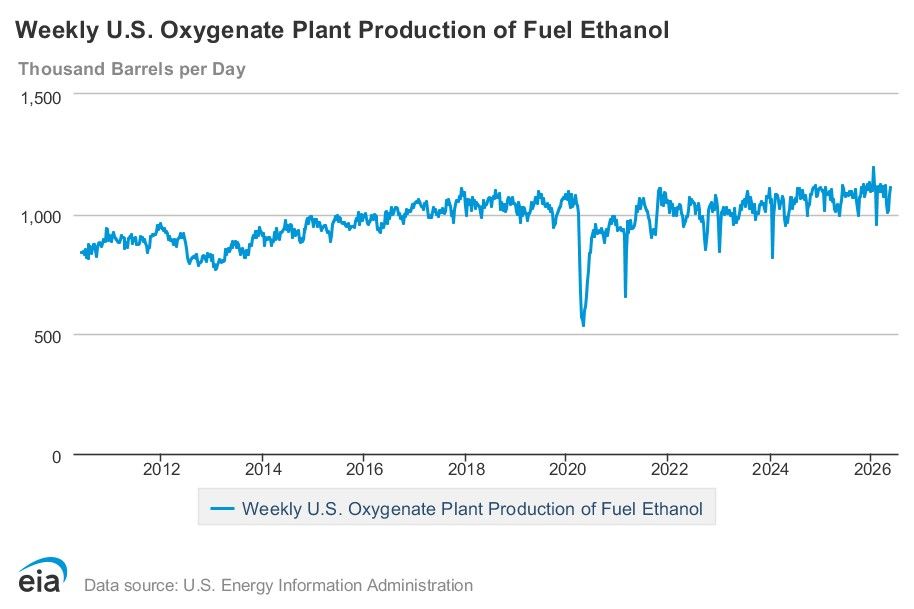

US Ethanol Production Stabilizes Above 1M Barrels/Day

This chart provides essential market context for the section discussing Antora’s partnership with POET, a major ethanol producer. The data on stable, high-volume ethanol production highlights the significant and consistent energy demand in this sector, underscoring the opportunity for decarbonization in the US Industrial Heartland.

(Source: Ethanol Producer Magazine)

Commercial Scale Achieved, Antora Moves Beyond Pilot Stage

Thermal energy storage using sensible heat is now a commercially mature technology, demonstrated by the successful deployment and commissioning of a multi-GWh system. The period from 2021 to 2024 was characterized by technology validation at the pilot level and academic analysis, while the period since 2025 is defined by the first commercial-scale operations that prove both technical reliability and economic viability.

- In the 2021-2024 timeframe, the technology’s readiness was considered high (TRL 8-9) in principle, but it lacked a flagship commercial project to prove bankability. Analysis focused on techno-economic targets, such as achieving an installed cost below $10/k Wh and improving round-trip efficiencies, which were theoretically high for direct heat applications but unproven at scale.

- The 2026 commissioning of Project Big Stone by Antora serves as the definitive validation point. Comprised of more than 200 modular thermal battery units, the 5 GWh facility demonstrates scalability. It confirms that the technology can provide multi-day storage (around 100 hours), a significant advantage over the 2-4 hour duration of typical lithium-ion batteries for industrial use cases that require continuous heat.

- This milestone firmly separates thermal storage for heat from other LDES technologies still in earlier development or targeting different applications. While lithium-ion BESS remains the dominant technology for short-duration grid services, Antora’s project proves that thermal batteries are a more direct and efficient solution for decarbonizing process heat by avoiding electricity-to-heat conversion losses.

SWOT Analysis of Thermal Storage for Industrial Heat

The strategic position of thermal batteries has been significantly validated, shifting from a technology with theoretical advantages to a commercially proven solution for industrial decarbonization. The successful commissioning of GWh-scale projects has confirmed its strengths and capitalized on market opportunities, though threats from established technologies remain.

Table: SWOT Analysis for Thermal Battery Industrial Decarbonization

| SWOT Category | 2021 – 2024 Status | 2025 – 2026 Status | What Changed / Validated |

|---|---|---|---|

| Strengths | Based on low-cost, abundant materials like carbon. Theoretical advantage in Levelized Cost of Storage (LCOS) for long durations. High direct heat-to-heat efficiency. | Demonstrated CAPEX potential of <$10/k Wh and LCOS of $0.05-$0.10/k Wh at GWh scale. Proven multi-day (100+ hour) storage capability. | The theoretical cost and performance advantages were validated by the Antora-POET project, confirming the technology’s economic competitiveness against fossil fuels for industrial heat. |

| Weaknesses | Low Technology Readiness Level for GWh-scale systems. Lack of bankable projects and operational data made it a high-risk investment. Lower round-trip efficiency for electricity-out applications compared to Li-ion. | Round-trip efficiency (70-90%) is lower than Li-ion (>90%) for electricity-to-electricity services, confining its primary application to industrial heat. | Project bankability was achieved, resolving the largest commercial weakness. The efficiency gap with Li-ion for grid services remains, solidifying its niche in the heat market. |

| Opportunities | The Inflation Reduction Act (IRA) and its standalone storage ITC created a massive policy tailwind. Growing industrial demand for decarbonization solutions. | Volatile fossil fuel prices and increased frequency of zero- or negative-priced electricity make storing low-cost renewables highly profitable. Expansion into other sectors like cement and steel. | The policy opportunity from the IRA was converted into a concrete, economically driven market opportunity, as demonstrated by the ability to arbitrage low-cost wind power. |

| Threats | Competition from other LDES technologies and green hydrogen for industrial heat. Incumbent natural gas remained a low-cost competitor. | Rapidly falling costs of lithium-ion BESS. Development of alternative heat solutions like those from Ameresco or other providers could challenge market share in specific applications. | While thermal storage has secured the industrial heat niche, the broader energy storage market remains highly competitive. The primary threat is now less about technological feasibility and more about market penetration speed. |

Antora Project Replication, Scenario Modeling for Industrial Heat

The most critical factor for the thermal battery market in the year ahead is the successful replication of the Antora-POET offtake and project model in other hard-to-abate sectors. If developers can sign similar long-term heat purchase agreements with cement, steel, or chemical manufacturers, the technology will solidify its role as a primary tool for industrial decarbonization, creating a distinct and valuable market segment separate from the grid-focused BESS industry.

- If this happens: Expect a wave of announcements for new GWh-scale thermal storage projects attached to industrial facilities, particularly in regions with high renewable penetration and established manufacturing bases.

- Watch this: The financing terms of the next 2-3 major thermal battery projects. Securing debt financing from major institutions without significant risk premiums will signal that the technology is considered fully bankable by capital markets.

- These could be happening: Antora and its competitors are likely in advanced negotiations with companies in other sectors. The success at the POET facility provides the operational proof needed to close these deals, potentially leading to a rapid scaling of the project pipeline beyond biofuels.

The questions your competitors are already asking

This report covers one angle of thermal battery commercialization for industrial heat. The questions that matter most depend on your work.

- What is the outlook for thermal battery deployment in the industrial heat sector by 2030?

- Antora investments and funding. Is the company on track for its $10/kWh CAPEX target?

- How does Antora’s thermal battery compare to green hydrogen for high-temperature industrial process heat?

- Which food & beverage or bio-processing operators are adopting thermal batteries for process heat?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

]]>Flow Battery Supply Chain, Rongke Power 1 GWh Project, $520 M Investment, and 111 GWh Demand (2021 to 2026)

VRFB Cost & Supply Chain Risk, $120/k Wh Vanadium Volatility

Vanadium price volatility and a concentrated supply chain remain the primary constraints on widespread Vanadium Redox Flow Battery (VRFB) adoption, creating a significant risk premium that overshadows the technology’s technical advantages in long-duration storage.

- The 2021-2024 period saw growing awareness of vanadium’s cost impact, but the 2025-2026 period has crystallized the financial risk. Price fluctuations between $10.25 and $28.75 per pound directly added $45 to $120 per k Wh to system costs, creating significant uncertainty for project developers and financiers.

- While China’s dominance of the vanadium supply chain (over 70%) was a known factor before 2025, the commissioning of domestic GWh-scale projects like the $520 million Jimusaer plant in January 2026 signals a strategic move to consume this supply internally, potentially tightening availability and increasing prices for international projects.

- The market’s reaction to this risk is bifurcated. The December 2025 recall of Prolux Solutions’ residential VRFB systems and the company’s subsequent pivot to LFP chemistry underscores investor and commercial skepticism about the technology’s viability in cost-sensitive segments where reliability is paramount.

- This cost-risk profile has opened the door for competing long-duration technologies. The momentum behind iron flow batteries, promoted by companies like Form Energy, is a direct response to the market’s search for energy storage solutions that rely on more abundant and price-stable materials, a threat that intensified post-2024.

$55 M VRB Energy Deal, UK Grant, and Prolux Recall Signal Market Split

Investment patterns from 2024 to 2026 reveal a market bifurcation, with significant capital flowing into established, utility-focused VRFB players while the residential segment experiences major setbacks and cancellations.

- Investment in 2024-2025 centered on scaling proven grid-scale technology. VRB Energy secured the largest early-stage deal in the sector in 2024 with a $55 million funding round, specifically aimed at expanding manufacturing capacity for large systems in the US and China.

- Government support remains a critical driver for de-risking commercial projects. In May 2025, Invinity Energy Systems secured a grant from the UK’s Department for Energy Security and Net Zero (DESNZ) for a 20.7 MWh VRFB project, confirming policy’s role in validating commercial deployments.

- In a significant blow to the residential market, Germany’s Prolux Solutions issued a full recall of its Storac VRFB home storage systems in December 2025 and announced it was canceling its VRFB product line in favor of Lithium Iron Phosphate (LFP) technology, citing reliability and cost issues.

- This contrasts with the pre-2024 period, where investment was more exploratory. The post-2024 focus is clearly on bankable, utility-scale applications, with venture capital and government funds targeting companies with a demonstrated path to delivering large, reliable systems.

Table: VRFB Investments and Cancellations

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| VRB Energy | June 2025 | Received the largest early-stage deal in the sector in 2024, valued at USD 55 million. The funding is targeted at scaling up manufacturing capacity to meet growing demand for utility-scale systems. | [PDF] World Energy Investment 2025 |

| Invinity Energy Systems | May 2025 | Awarded a grant by the UK’s Department for Energy Security and Net Zero (DESNZ) for an up to 20.7 MWh VRFB project. This demonstrates government support for validating the technology at a commercial scale. | [PDF] 2024 Annual Report |

| Prolux Solutions | December 2025 | Issued a product recall for all Storac residential VRFB systems and announced the cancellation of the product line. The company will pivot to LFP technology, marking a significant setback for VRFBs in the residential market. | Prolux Solutions Recalls VRFBs |

Invinity Energy Systems 2 Key Deals with MHI & Siemens Gamesa (2021 to 2026)

Strategic partnerships formed between 2024 and 2026 show a clear industry strategy to de-risk market entry and supply chains by aligning with major industrial incumbents and raw material suppliers.

- In September 2025, Invinity Energy Systems announced a strategic partnership with Mitsubishi Heavy Industries (MHI) to co-develop and deploy large-scale VRFB systems, leveraging MHI’s global reach and project execution expertise to access new markets.

- To secure the upstream supply chain, Richmond Vanadium Technology (RVT) signed a key agreement with RKP Global in June 2026 to establish Australia’s first fully integrated mine-to-battery supply chain, a direct response to market concerns over Chinese supply dominance.

- Prior to 2024, partnerships were often focused on pilot projects and technology validation. The new agreements post-2025, including a commercial agreement between Invinity and Siemens Gamesa, are commercially oriented, focusing on scaling manufacturing, securing supply, and global deployment, signaling a shift from R&D collaboration to commercial execution.

Table: VRFB Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Richmond Vanadium Technology (RVT) & RKP Global | June 2026 | Agreement to establish Australia’s first mine-to-battery vanadium supply chain. This strategic move aims to de-risk the supply of critical raw materials and counter the market’s dependence on China. | RVT & RKP Global Agreement |

| Invinity Energy Systems & Mitsubishi Heavy Industries (MHI) | September 2025 | Strategic partnership for the co-development and deployment of large-scale VRFB systems. This alliance validates the technology and provides a channel to market through a major industrial player. | All Vanadium Redox Flow Battery Market |

| VRB Energy | October 2024 | Announced plans for three new factories with a combined annual capacity of 550 MW in the US and China. This move is a direct supply-side response to anticipated demand for GWh-scale projects. | VRB Energy Plans 550 MW Capacity |

China vs. West, VRFB Geographic Focus on Grid-Scale Projects

The global VRFB market’s geography has consolidated around two distinct models: China’s state-driven, vertically integrated GWh-scale deployment, and a more fragmented Western model reliant on government subsidies and strategic partnerships to compete.

- From 2025 to 2026, China cemented its leadership by commissioning the world’s first GWh-scale VRFB projects, including the 1 GWh facility in Jimusaer, Xinjiang. This activity is driven by national policy and the integration of battery manufacturing with domestic vanadium production.

- In contrast, Western activity is driven by specific policy incentives. The US market is supported by federal tax credits like the Section 48 E Clean Electricity Investment Credit, while Australia’s government is backing projects with initiatives like an AUD 50 million grant program for LDES feasibility studies.

- Prior to 2025, VRFB deployments were more scattered, with pilot projects in multiple regions including Europe, North America, and Japan. The recent period shows a concentration of large-scale execution in China and strategic, policy-driven projects in the US and Australia.

- Europe faced a setback with the December 2025 recall and cancellation of Prolux Solutions’ residential VRFB line in Germany, damaging confidence in the European residential segment and reinforcing the global focus on utility-scale applications.

VRFB Tech Maturity, TRL 8-9 Validation vs. Residential Setbacks

VRFB technology has definitively proven its maturity for grid-scale applications (TRL 8-9) with the successful commissioning of GWh projects, but significant challenges in cost, reliability, and form factor have stalled its adoption in the residential market.

- The most significant validation of VRFB maturity occurred in January 2026 with the commissioning of the 200 MW / 1 GWh project in China, demonstrating the technology is ready for commercial deployment at the scale required for grid stabilization. This follows years of successful MW-scale deployments before 2024.

- Established players like Sumitomo Electric continue to refine the technology, launching an advanced VRFB system in February 2025 that builds on decades of operational experience and addresses known performance parameters for utility customers.

- However, the technology’s maturity does not extend uniformly across all applications. The December 2025 recall of Prolux Solutions’ residential VRFB systems highlights a technology readiness gap for smaller, cost-sensitive applications, where issues with reliability or balance-of-plant complexity proved insurmountable.

- The core technology of the vanadium electrolyte and stack is mature. The industry’s focus post-2024 is now on standardizing components, improving the balance of plant, and reducing manufacturing costs, which are now the primary barriers, not fundamental technical readiness for its target grid market.

SWOT Analysis, VRFB Market Strengths & Supply Chain Risks

The VRFB market’s fundamental strength in long-duration technical performance is counterbalanced by a critical weakness in its cost structure and supply chain, creating an opportunity for policy-driven growth but also a threat from lower-cost alternative technologies.

- The market’s primary strength lies in the technology’s long cycle life (20, 000+ cycles) and non-flammability, making it technically superior for grid-scale, long-duration applications.

- Its greatest weakness is the high upfront capital cost and dependence on a volatile vanadium supply chain, which is heavily concentrated in China.

- The main opportunity comes from strong policy tailwinds for long-duration energy storage, such as US tax credits, which improve project economics.

- The most significant threat is competition from emerging, lower-cost LDES technologies like iron flow batteries, which do not carry the same commodity price risk.

Table: SWOT Analysis for VRFB Market (2021-2025)

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Long cycle life, scalability, and safety were well-understood theoretical advantages. Multiple MW-scale pilots demonstrated technical feasibility. | Technical superiority validated with 1 GWh project in China (2026) and advanced systems from Sumitomo Electric (2025). Long-term reliability proven. | The technology’s transition from pilot-scale promise to GWh-scale reality was validated, confirming its suitability for the intended grid market. |

| Weaknesses | High upfront CAPEX and theoretical risk of vanadium price volatility were primary concerns for investors. | High CAPEX ($350-$500/k Wh) remains a barrier. Vanadium price volatility became a tangible risk, adding up to $120/k Wh to system costs. | The theoretical weakness of cost and price volatility was confirmed as a real-world, quantifiable financial risk, hindering bankability without subsidies. |

| Opportunities | General government support for renewables and emerging energy storage mandates provided a potential market. | Specific, robust LDES policies like the uncapped US Residential Clean Energy Credit and Section 48 E credits created direct financial incentives and a clear business case. | Vague policy support evolved into concrete, bankable financial incentives, turning a potential opportunity into a primary market driver. |

| Threats | Lithium-ion was the main competitor. Alternative flow battery chemistries were largely in R&D. | Competition from low-cost iron flow batteries (e.g., ESS Inc.) intensified. The Prolux recall (2025) showed LFP as a direct threat in smaller segments. | The competitive threat diversified beyond Li-ion to include other LDES chemistries specifically targeting VRFB’s primary weakness: raw material cost. |

VRFB 2026 Scenario, Vanadium Price Stability as the Key Catalyst

The VRFB market’s trajectory in the next 18-24 months hinges almost entirely on its ability to mitigate vanadium cost and supply risks; if prices remain volatile, expect a shift in investment toward alternative LDES chemistries like iron flow.

- If this happens: Major VRFB manufacturers demonstrate an all-in system CAPEX below $300/k Wh on a new project announced in 2026.

- Watch this: Monitor announcements from companies like VRB Energy and Invinity Energy Systems for project cost breakdowns and look for signs of new, non-Chinese vanadium mining projects reaching final investment decisions, such as the Australian Vanadium Project.

- These could be happening: A successful cost demonstration would accelerate VRFB adoption in the 6-10 hour storage market, likely triggering a new wave of utility-scale project announcements in North America and Australia and firming up the 17.6% CAGR forecast.

- If this happens: Vanadium prices spike again in 2026, and another VRFB company faces commercial difficulties similar to Prolux Solutions.

- Watch this: Track the project pipelines of public VRFB companies versus those of emerging competitors like ESS Inc. Increased announcements for iron flow pilot projects with major utilities would be a strong negative signal for VRFB sentiment.

- These could be happening: Investor capital would pivot away from VRFBs toward chemistries with more stable and abundant raw materials, forcing VRFB companies to rely more heavily on electrolyte leasing models and putting the long-term growth forecast at risk.

The questions your competitors are already asking

This report covers one angle of the commercial viability of Vanadium Redox Flow Batteries. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the long-duration storage market as a result of vanadium supply chain risks?

- What is the outlook for VRFB deployment given the $45 to $120 per kWh cost volatility from vanadium price fluctuations?

- How does the VRFB cost structure compare to emerging alternatives like iron flow batteries for utility-scale storage?

- What is the impact of China’s GWh-scale projects, like the $520M Jimusaer plant, on global vanadium availability for international developers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

]]>