US Battery Storage in 2026: Can Manufacturing Scale to Meet 500 GWh Demand?

Industry Risks: US Battery Storage Deployment Outpaces Domestic Supply Chain

The U.S. energy storage market’s explosive growth, targeting 18.9 GW of new capacity in 2025, is creating a significant structural tension between soaring demand and a nascent domestic manufacturing base. While the 2021-2024 period was characterized by scaling deployments of imported lithium-ion systems, the 2025-2026 era is defined by a high-stakes race to onshore the entire supply chain, a direct response to мощные стимулы a Inflation Reduction Act (IRA). This transition introduces substantial execution risk, as the market must now build factories, process materials, and train a workforce at a pace that matches gigawatt-scale demand from both traditional grid projects and new, energy-intensive sectors like artificial intelligence.

- Prior to 2025, market growth was contingent on the availability and cost of imported battery systems. The post-IRA environment has shifted the critical path to the speed of domestic factory construction and the ability of developers to meet stringent domestic content requirements that take full effect in 2026, creating a potential policy-induced bottleneck.

- A major strategic shift occurred in 2025 with the emergence of AI data centers as a primary demand driver, exemplified by Form Energy’s landmark 12 GWh supply agreement for its iron-air batteries. This multi-billion-dollar use case, which requires massive, reliable power, was not a significant factor in the 2021-2024 period and now adds immense pressure on the supply chain.

- The entrance of industrial heavyweights like Ford, which announced in December 2025 its plan to repurpose EV manufacturing capacity for stationary storage, signals a new phase of market maturation. This strategic pivot to produce LFP-based BESS for data centers by 2027 underscores a convergence between the automotive and energy sectors not seen in previous years.

- The U.S. energy storage industry’s collective commitment in April 2025 to invest $100 billion by 2030 formalizes this supply chain build-out. However, this capital must be deployed effectively to prevent a supply-demand gap as import reliance is discouraged and domestic alternatives are still scaling.

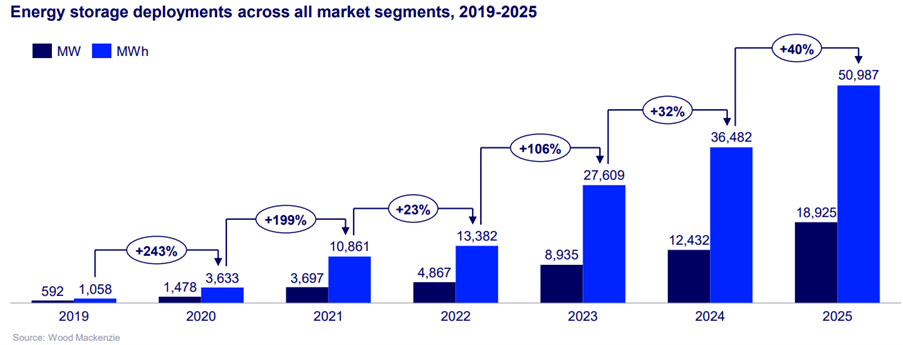

US Storage Deployments Surge to 18.9 GW

This chart directly visualizes the explosive deployment growth mentioned in the text, specifically confirming the 18.9 GW of new capacity targeted for 2025.

(Source: Mercom India)

Investment Analysis: IRA Unlocks $100 Billion for US Battery Manufacturing

The Inflation Reduction Act has directly catalyzed a wave of strategic investments aimed at building a secure, domestic battery supply chain capable of supporting the projected 500 GWh of deployment through 2031. Before 2024, investments were primarily focused on project development and software. From 2025 onward, capital allocation has decisively shifted upstream to multi-billion-dollar manufacturing and materials processing facilities, a clear indicator that investors are underwriting the long-term vision of American energy independence.

- The market’s bullish outlook was solidified by the U.S. energy storage sector’s April 2025 pledge to invest $100 billion by 2030. This commitment is not just for project deployment but explicitly targets the procurement of American-made grid batteries, creating a powerful demand signal for domestic manufacturers.

- Major foreign battery producers are committing billions to U.S. production. In July 2025, Panasonic Energy began mass production at its new Kansas factory, aiming for 32 GWh of annual capacity, a scale-up directly incentivized by the IRA’s manufacturing credits.

- Downstream project financing also reflects this confidence. In March 2025, Clearway closed $605 million in financing for its battery storage portfolio in Utah, demonstrating that large-scale utility projects remain highly bankable, providing a stable offtake for the new manufacturing plants.

Table: Key Investments in US Battery Storage (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Form Energy | Mar 2026 | Secured a 12 GWh supply agreement to provide its multi-day iron-air batteries for new U.S. AI data centers, validating a new technology and a new, massive end-market. | Energy Storage News |

| Ford | Dec 2025 | Announced the launch of a battery storage business, repurposing part of its Kentucky EV battery plant to produce BESS units for data centers, with shipments planned for 2027. | ESS News |

| Panasonic Energy | Jul 2025 | Began mass production at its new automotive lithium-ion battery factory in Kansas, targeting an annual capacity of 32 GWh to accelerate U.S. local production for EVs and stationary storage. | Panasonic |

| US Energy Storage Industry | Apr 2025 | A collective commitment to invest $100 billion by 2030 to build and purchase American-made grid batteries, aiming to create 350, 000 jobs. | American Clean Power |

| Clearway | Mar 2025 | Closed $605 million in financing for a portfolio of grid-enhancing battery storage projects in Utah, signaling strong investor appetite for large-scale deployment. | Clearway Energy Group |

Geography: IRA Reshapes US Battery Investment Beyond Texas and California

While project deployment remains concentrated in states with high renewable penetration, IRA incentives are fundamentally reshaping the geographic landscape of battery manufacturing investment. Before 2025, market activity was overwhelmingly centered in Texas and California due to favorable grid policies and solar-plus-storage economics. Now, manufacturing investment is flowing into new industrial corridors in the Midwest and Southeast, drawn by “energy community” tax bonuses, skilled labor, and logistical advantages.

- Deployment leadership remains with states like Texas (6, 998 MW planned for 2025), California (4, 209 MW), and Arizona (3, 662 MW), which together account for over 80% of planned additions. These regions represent the largest end-markets for the domestic battery output.

- Manufacturing investment, however, is decentralizing. Ford’s decision to repurpose its plant in Kentucky, Panasonic’s new factory in Kansas, and Gotion’s $2 billion investment in Illinois show a clear trend of building industrial capacity outside the traditional solar and wind belts.

- This geographic diversification is a direct outcome of the IRA, which provides a 10% tax credit bonus for projects sited in “energy communities, ” often areas with a history of fossil fuel production. This incentivizes companies to redevelop industrial sites and tap into existing skilled workforces.

Technology Maturity: Long-Duration Storage Moves from Pilot to Commercial Scale

The U.S. battery market’s expansion relies on mature, commercially proven (TRL 9) 4-hour lithium-ion technology, but the period from 2025-2026 marked a critical validation point for next-generation long-duration energy storage (LDES). While the 2021-2024 timeframe focused on cost reduction and scaling of Li-ion, the current era is seeing alternative chemistries secure their first large-scale commercial offtake agreements, proving their readiness to address grid needs beyond daily peak shifting.

- The most significant milestone is Form Energy’s 12 GWh supply agreement in March 2026 for its iron-air battery system. This moves the technology from pilot stages (TRL 6-7) directly to commercial-scale deployment (TRL 8) and validates its business case for powering AI data centers.

- The market is also seeing a strategic shift in lithium-ion chemistry. Ford’s plan to use lithium iron phosphate (LFP) for its stationary storage products highlights a move toward cheaper, more durable, and safer chemistries over higher-energy-density alternatives used in some EVs.

- While Li-ion remains dominant, the improving cost-competitiveness of BESS is accelerating the bankability of these alternative technologies. The successful deployment of Form Energy’s project will be a crucial de-risking event for other LDES technologies, such as thermal and geothermal storage, which are still in earlier pilot phases (TRL 6-7).

SWOT Analysis: US Battery Storage Market

The U.S. battery storage market’s strength is its unparalleled policy support, but its primary weakness is the immense execution risk tied to scaling a domestic supply chain fast enough to meet both surging demand and stringent 2026 local content rules.

Table: SWOT Analysis for US Battery Storage Manufacturing and Supply Chain

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | Maturing Li-ion technology and falling costs. State-level mandates (e.g., CA, NY) provided primary policy support. | The Inflation Reduction Act (IRA) provides powerful, long-term federal tax credits for both deployment and manufacturing, creating immense financial tailwinds. | The market shifted from being driven by state policy to being supercharged by federal industrial policy, unlocking over $100 billion in investment. |

| Weakness | Heavy reliance on imported battery cells and components, primarily from China, creating supply chain vulnerability. | A domestic manufacturing gap. New factories from LG Energy Solution, Samsung SDI, and SK On are still ramping up, creating a near-term risk of not meeting demand or IRA content rules in 2026. | The weakness shifted from a geopolitical risk to a concrete execution risk. The key question is no longer “where to buy?” but “can we build it fast enough?” |

| Opportunity | Grid modernization and pairing storage with utility-scale solar and wind projects to provide ancillary services. | The emergence of new, massive demand centers, particularly AI data centers, which require 24/7 reliable power that the grid cannot provide alone (e.g., Form Energy’s 12 GWh deal). | The addressable market expanded beyond traditional grid services to include a high-growth, multi-billion-dollar industrial segment, providing a new layer of demand. |

| Threat | Persistent grid interconnection queues and project permitting delays, which slowed down deployment velocity. | A potential policy cliff in 2026, when stringent domestic sourcing requirements for IRA tax credits take effect. Failure to secure a compliant supply chain could increase costs or delay projects. | The primary threat evolved from administrative bottlenecks to a hard-deadline policy challenge that directly impacts project economics and supply chain strategy. |

Scenario Modelling: Navigating the 2026 Domestic Content Policy Cliff

The U.S. battery market’s trajectory toward 500 GWh by 2031 hinges almost entirely on its ability to navigate the 2026 domestic content policy transition without significant disruption. Investors and strategists should monitor domestic manufacturing output and project pricing in the first half of 2026 as the primary signal of success or slowdown.

US Storage Growth Scenarios to 2031

This chart directly illustrates the section’s ‘Scenario Modelling’ theme by presenting three distinct growth trajectories (High, Base, Low) through 2031.

(Source: Mercom India)

- Bull Case: If U.S. factories ramp up faster than expected and developers secure compliant supply chains, the market could maintain its 52% year-over-year growth rate. Watch quarterly installation reports from Wood Mackenzie and the EIA in Q 1 and Q 2 2026 for the first hard evidence of this continued acceleration.

- Bear Case: If supply chain dislocations and price volatility emerge due to a scramble for IRA-compliant components, a temporary slowdown or flattening of the growth curve in 2026 is highly probable. Watch for announcements of project delays or public statements from developers citing sourcing challenges.

- Key Signal: The market entry of Ford will be a critical validation point. Tracking its initial sales volumes and customer feedback upon first shipments in 2027 will indicate the potential for other large-scale industrial manufacturers to successfully enter and further drive down costs in the BESS space.

Frequently Asked Questions

What is the biggest challenge for the US battery market in 2026?

The primary challenge is a potential “policy-induced bottleneck.” The market faces immense execution risk in trying to scale a domestic manufacturing supply chain fast enough to meet both explosive demand (driven by grids and AI) and the stringent domestic content requirements of the Inflation Reduction Act (IRA), which take full effect in 2026.

How has the Inflation Reduction Act (IRA) changed the battery industry?

The IRA has fundamentally shifted the market’s focus from importing battery systems to building a domestic supply chain. It provides powerful federal tax credits for both manufacturing and deployment, directly catalyzing over $100 billion in planned investments and incentivizing companies like Panasonic and Ford to build or repurpose factories in the U.S.

What new industry is driving a surge in demand for battery storage?

Artificial Intelligence (AI) data centers have emerged as a primary new demand driver. These energy-intensive facilities require massive, reliable 24/7 power, creating a new multi-billion-dollar market for large-scale energy storage. A key example is Form Energy’s 12 GWh supply agreement specifically for new U.S. AI data centers.

Are battery technologies beyond standard lithium-ion becoming commercially viable?

Yes. The 2025-2026 period is a critical validation point for next-generation technologies. Form Energy’s 12 GWh deal for its multi-day iron-air batteries marks a major step from pilot stage to commercial-scale deployment. Additionally, there is a strategic shift toward Lithium Iron Phosphate (LFP) chemistry for stationary storage, as seen in Ford’s plans, due to its durability, safety, and lower cost.

What is the total projected demand and investment for the US battery market?

The U.S. is projected to require 500 GWh of battery storage deployment through 2031. To support this growth, the U.S. energy storage industry has collectively committed to investing $100 billion by 2030 to build out the domestic supply chain and purchase American-made grid batteries.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.