BESS Capacity Shift: LONGi’s 62% Potis Edge Deal, $4.7 B in Solar Losses, and 5 GWh Vikram Solar Target (2025-2026)

Solar Industry Crisis, Chinese Manufacturers Face $4.7 B in Projected Losses

A severe profitability crisis in the solar photovoltaic (PV) sector is forcing China’s largest manufacturers to execute a strategic pivot into battery energy storage systems (BESS). An unsustainable price war, driven by massive domestic overcapacity, has collapsed profit margins, making the core business of selling solar panels unable to support growth. This is not a voluntary diversification but a necessary corporate survival strategy to escape financial distress and find a new growth engine.

- Between 2021 and 2024, Chinese solar manufacturers focused on aggressive capacity expansion, dominating the global supply chain with approximately 85% of production. This led to a boom in output but also laid the groundwork for intense price competition.

- Starting in 2025, the market entered a state of crisis. In January 2026, five of the largest PV manufacturers, including LONGi Green Energy and JA Solar, projected a combined deficit of up to $4.7 billion for the 2025 fiscal year.

- The price war became so severe that by 2025, seven major module companies reported their first collective financial losses in eight years. This forced a strategic retreat from a purely solar-focused model toward the more profitable and rapidly growing BESS market.

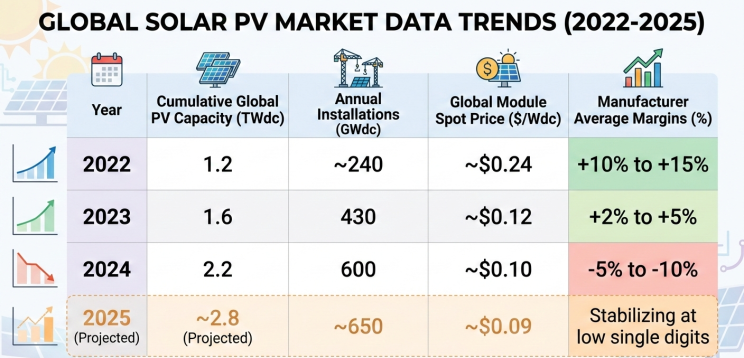

Solar Manufacturer Margins Collapse Amid Price War

This chart directly visualizes the financial crisis described in the section, showing collapsing margins which are the direct cause of the projected $4.7B in losses.

(Source: LinkedIn)

$2.8 B in US Cancellations, Chinese Firms Redirect Investment Focus

Financial decisions are being shaped by a combination of domestic market pressures and international trade barriers, leading to a significant redirection of capital. While geopolitical tensions have forced the cancellation of planned investments in the United States, Chinese firms are channeling funds into building out domestic BESS manufacturing capacity to serve the booming global energy storage market.

- In 2025, Chinese clean technology firms cancelled approximately $2.8 billion in planned manufacturing investments in the U.S. These decisions were a direct response to new policies and geopolitical friction that stalled factory expansions for Chinese-linked companies.

- This withdrawal from the U.S. manufacturing landscape contrasts sharply with investment activity in the BESS sector. In late 2025, LONGi acquired a 62% stake in battery manufacturer Potis Edge, a clear signal of its strategic intent to make BESS a primary growth engine.

- Other manufacturers are following suit. India’s Vikram Solar, facing similar market pressures, announced plans in August 2025 to diversify into BESS, targeting an installed capacity of 5.0 GWh by fiscal year 2027. This demonstrates a broader industry trend of reallocating capital from solar to storage.

Table: Strategic Capital and Investment Shifts (2025-2026)

| Company / Group | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LONGi Green Energy | Nov 2025 | Acquired a 62% stake in Potis Edge to pivot into battery manufacturing as a primary growth engine amid collapsing solar margins. | Nikkei Asia |

| Chinese Clean-Tech Firms | 2025 | Cancelled $2.8 billion in planned U.S. manufacturing investments due to regulatory and geopolitical shifts, forcing a retreat from U.S. expansion. | Investment Monitor |

| Vikram Solar | Aug 2025 | Announced diversification into BESS with a target to establish 5.0 GWh of installed capacity by FY 27 to create new revenue streams. | Chittorgarh |

Chinese Energy Storage Overseas Orders Surge

This chart illustrates the market pull behind the ‘Strategic Capital and Investment Shifts,’ showing that surging overseas demand for energy storage is the key driver for manufacturers redirecting their capital.

(Source: Volt Insight – Substack)

LONGi’s Neo Volta Partnership, A Strategic BESS Market Entry (2026)

Solar manufacturers are using strategic partnerships and acquisitions to rapidly enter the BESS value chain and secure market access. These alliances allow them to leverage their manufacturing scale while partnering with companies that have established channels and specific market expertise, accelerating their entry into grid-scale and residential storage projects.

- The strategic pivot is exemplified by LONGi’s acquisition of Potis Edge in late 2025, which immediately gave it significant battery manufacturing capabilities.

- This move was quickly followed by a downstream partnership. In January 2026, U.S.-based Neo Volta announced a collaboration with Potis Edge to manufacture electric grid batteries, directly leveraging the new capacity controlled by LONGi.

- This chain of events shows a clear strategy: acquire manufacturing assets and then partner with established market players to deploy products. This allows former solar giants to bypass the slower process of building a new brand and sales channel from scratch.

Sungrow Stock Surges Amid BESS Pivot

This chart provides market validation for LONGi’s strategic BESS entry by showing how investors rewarded a competitor for a similar pivot, affirming the strategy’s potential.

(Source: Volt Insight – Substack)

Table: Key Partnerships in the Solar-to-Storage Pivot

| Lead Partner / Acquirer | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Neo Volta / Potis Edge (LONGi) | Jan 2026 | Neo Volta partnered with LONGi-backed Potis Edge to manufacture electric grid batteries, providing LONGi with a U.S. market channel for its new BESS products. | Nikkei Asia |

China vs US, Geopolitics Guide LONGi’s BESS Strategy

The geographic focus of this manufacturing pivot is split between a massive domestic build-out in China and a cautious, partnership-driven approach to international markets. While China’s internal market provides a large demand base for BESS, geopolitical tensions and trade barriers, particularly from the U.S., are forcing companies to adopt indirect strategies for overseas growth.

- Activity from 2021 to 2024 was characterized by Chinese solar firms expanding their physical manufacturing footprint globally, including in the U.S.

- This shifted in 2025. China’s government began to curb “disorderly” expansion and cancelled a 13% VAT rebate for solar and storage exports, pressuring firms to be more strategic about international sales.

- Simultaneously, the U.S. administration’s crackdown on China-linked firms led to the cancellation of planned factories, effectively closing the door on direct manufacturing investment. This has pushed companies like LONGi to use partnerships with firms like Neo Volta as a primary vector for accessing the American market, a stark contrast to the previous strategy of building local plants.

- The pivot is also creating opportunities in other regions, such as India, where the government’s push for $32 billion in energy storage by 2032 creates a new demand center for Chinese technology and manufacturing capacity.

SWOT Analysis, The Risks in the Pivot from Solar to BESS

The strategic shift from solar panels to battery storage is an essential survival maneuver, but it is not without significant risks. While leveraging immense manufacturing strengths, these companies are entering a market that is already showing signs of the same competitive dynamics that crippled the solar industry.

- The primary strength is the vast, low-cost manufacturing expertise that allowed Chinese firms to dominate the solar industry. This can be directly applied to BESS production to achieve scale rapidly.

- A major opportunity lies in the explosive growth of the BESS market, which is projected to grow at a CAGR of over 15% through 2030, offering the revenue and margin potential that has disappeared from the solar panel sector.

- However, a critical weakness is the reliance on a different and equally concentrated supply chain for critical minerals like lithium and cobalt, which CATL and others are working to secure. This trades one set of supply chain risks for another.

- The most significant threat is the high probability of repeating the cycle of overcapacity. The massive influx of capital from former solar giants, combined with entries from automakers like Ford and GM, threatens to create a BESS supply glut and trigger a new price war within three to five years.

Jinko’s BESS Roadmap Details Rapid Tech Advancement

This chart illustrates a significant ‘Threat’ for the SWOT analysis: intense competitive pressure. A competitor’s rapid technological advancement represents a major risk for any company pivoting into the same market.

(Source: LinkedIn)

Table: SWOT Analysis for the Solar-to-BESS Manufacturing Pivot

| SWOT Category | Strengths | Weaknesses | Opportunities | Threats |

|---|---|---|---|---|

| Analysis | Vast, established, low-cost manufacturing capabilities and global supply chain expertise from the solar industry. Existing relationships with global utility and energy customers can be cross-leveraged. | Lack of differentiation, as most companies are pursuing a similar scale-based strategy. High reliance on critical mineral supply chains (lithium, cobalt) controlled by a few nations. | Explosive growth in the global BESS market, projected to exceed $100 billion by 2030. Ability to offer integrated solar-plus-storage solutions, capturing more value. | Replication of overcapacity and a new price war as numerous large players enter the BESS market simultaneously. Increased competition from automakers like Ford and GM repurposing EV battery factories for energy storage. |

China’s Solar Installations Surge to Record Highs

This chart represents a key ‘Strength’ in the SWOT analysis. It demonstrates Chinese manufacturers’ proven experience in massive-scale deployment and manufacturing, a core competency that can be leveraged from solar to BESS.

(Source: Carbon Brief)

BESS Price War Scenario, LONGi’s Post-2026 Margin Risks

The most critical scenario to monitor is the potential for a rapid compression of BESS margins by 2027, mirroring the solar industry’s collapse. The sheer volume of planned battery manufacturing capacity in China suggests a price war is a matter of when, not if. Companies that fail to differentiate beyond cost and scale will face the same profitability crisis they are currently fleeing.

- If this happens: The massive influx of new BESS manufacturing capacity from both former solar giants and automakers will outpace near-term demand growth, triggering an aggressive price war for market share.

- Watch this: Monitor the pricing of lithium iron phosphate (LFP) battery packs, a key indicator of market competition. A sustained fall in prices despite strong demand would signal the onset of a supply glut. Also, track the capacity utilization rates of major battery manufacturers.

- These could be happening: Winners will be those that secure upstream supply of critical minerals, achieve technological differentiation with next-generation chemistries (e.g., sodium-ion), and integrate hardware with energy management software to offer complete solutions rather than commoditized battery packs.

Chinese Solar Subsidies Created Global Panel Surplus

This chart serves as a cautionary tale, explaining the dynamic that could lead to the ‘BESS Price War Scenario.’ It shows how subsidies led to a surplus in solar, warning that the same pattern could trigger the post-2026 margin risks in the BESS market.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of the Chinese solar manufacturers’ strategic pivot to battery storage. The questions that matter most depend on your work.

- Which Chinese solar manufacturers are gaining or losing ground in the pivot to the BESS market?

- Is LONGi a good investment at this stage of the solar panel-to-BESS market transition?

- What is the outlook for Chinese-made BESS deployment in Europe and the US by 2030, following the PV overcapacity crisis?

- Which utility-scale project developers are adopting BESS from traditionally PV-focused manufacturers like LONGi and JA Solar?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.