Top 10 BESS Projects, Adani’s 3.5 GWh Deal, Jupiter’s 700 MW Plant, and Saudi Arabia’s 7.8 GWh System (2024-2026)

An analysis of major Battery Energy Storage System (BESS) projects from 2024 to 2026 reveals a definitive market shift towards gigawatt-hour scale deployments. The primary finding is that BESS has evolved from providing short-duration ancillary services to becoming a core grid asset capable of supplying firm capacity and replacing conventional peaker plants. This trend is demonstrated by landmark projects like the 7.8 GWh system connected in Saudi Arabia and Adani Group’s announced 3.5 GWh facility in India. The dominant theme for 2025 is this strategic pivot to multi-gigawatt-hour systems, which are essential for integrating massive renewable energy portfolios and ensuring grid reliability. The United States, particularly California and Texas, continues to lead in deployment, with projects like the 821 MW / 3, 287 MWh Edwards & Sanborn facility setting new benchmarks for hybrid solar-plus-storage.

1. Jupiter Power Everett Facility

Company: Jupiter Power

Installation Capacity: 700 MW

Applications: Grid reliability and flexibility

Source: Jupiter Power gets approval for 700 MW battery storage in Everett

2. Thurrock Storage Project

Company: Statera Energy

Installation Capacity: 300 MW

Applications: Grid balancing services and flexibility for the National Grid

Source: National Grid connects UK’s largest battery storage facility at Tilbury …

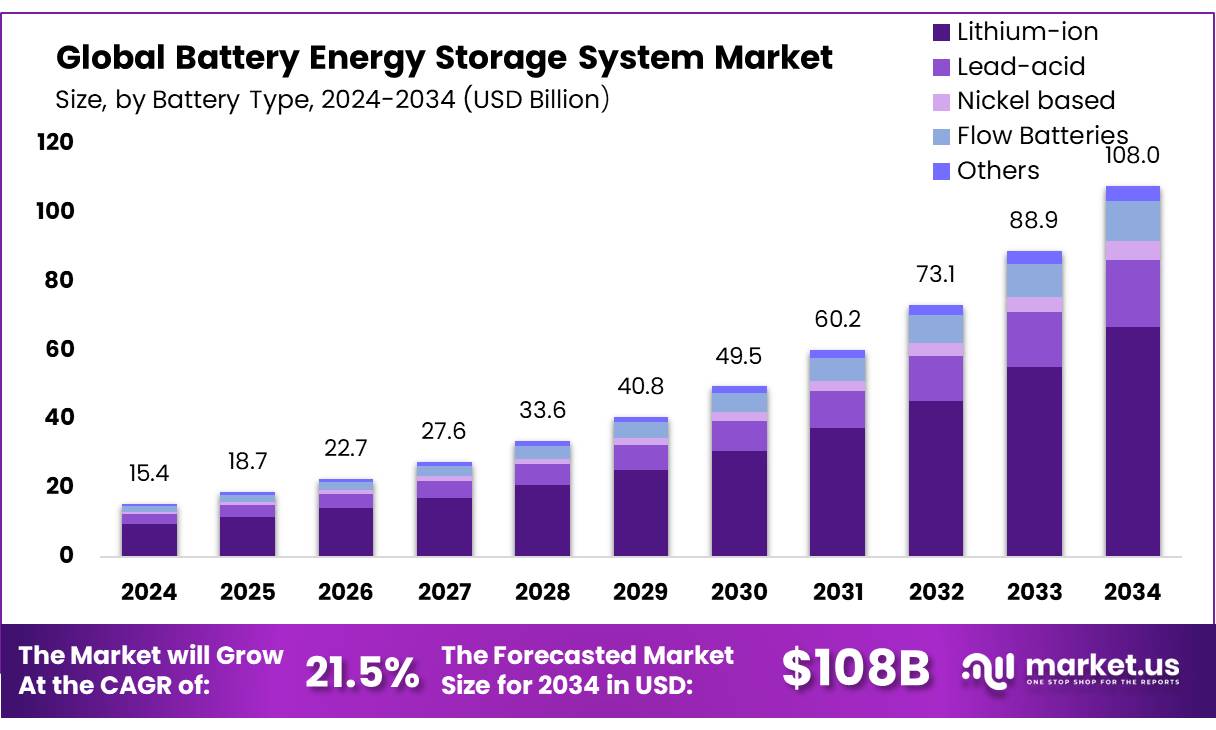

BESS Market to Reach $108B by 2034

The chart’s forecast of a $108B market provides the financial and investment rationale for large-scale international projects like the Thurrock Storage Project in the UK.

(Source: Market.us)

3. DTE Trenton Channel BESS

Company: DTE Energy

Installation Capacity: 220 MW

Applications: Clean energy transition, replacing a retired coal power plant

Source: DTE Energy seeking developers for new energy storage projects

Global Energy Storage Capacity Growing 12% Annually

This chart illustrates the consistent and strong annual growth in the energy storage market, providing the backdrop of momentum that justifies investments such as the DTE Trenton Channel BESS.

(Source: Wood Mackenzie)

4. Adani Group BESS Project

Company: Adani Group

Installation Capacity: 1, 126 MW / 3, 530 MWh

Applications: Utility-scale energy storage, grid stabilization

Source: Adani Group Announces Strategic Entry into Battery Energy Storage …

Global Battery Storage Deployments Grew 4x

The chart’s depiction of a fourfold increase in deployments explains the market environment that prompted a major industrial conglomerate like the Adani Group to make a significant entry into the BESS sector.

(Source: IDTechEx)

5. Saudi Arabia BESS Project

Company: Not specified

Installation Capacity: 7, 800 MWh (7.8 GWh)

Applications: Grid-scale energy storage to support national energy transition

Source: Saudi Arabia connects 7.8 GWh battery storage project to the grid

6. Indi Grid & IFC BESS Project

Company: Indi Grid and International Finance Corporation (IFC)

Installation Capacity: 180 MW / 360 MWh

Applications: Grid stability and renewable energy integration

Source: IFC and Indi Grid Partner to Build India’s Largest Utility-Scale Energy …

7. Energy Vault BESS Project

Company: Energy Vault

Installation Capacity: 150 MW / 300 MWh

Applications: Providing critical grid services in the ERCOT market

Source: Energy Vault Announces Acquisition of 150 MW Battery Energy …

China and US Dominate Battery Storage Capacity

As Energy Vault is a US-headquartered company, this chart places its projects within the context of one of the world’s two leading markets, highlighting the competitive landscape and scale of the US BESS industry.

(Source: LinkedIn)

8. Edwards & Sanborn Solar + Storage

Company: Terra-Gen

Installation Capacity: 821 MW / 3, 287 MWh

Applications: Hybrid solar-plus-storage for firm, dispatchable renewable power

Source: Biggest projects in the energy storage industry in 2024

Solar & Storage Projects to Surge in 2025

The chart directly reflects the theme of the section, providing the macro trend of a surge in solar and storage projects that the Edwards & Sanborn facility is a prime example of.

(Source: Crux)

9. Gemini Solar + Storage

Company: Quinbrook Infrastructure Partners / Primergy Solar

Installation Capacity: 380 MW / 1, 416 MWh

Applications: Storing and dispatching solar energy to meet peak evening demand

Source: When to install battery energy storage systems bess? – Polinovel Tech

10. Moss Landing Power Plant Expansion

Company: Vistra Energy

Installation Capacity: 350 MW / 1, 400 MWh (expansion phase)

Applications: Enhancing grid reliability and capacity in California

Source: Top 10: Energy Storage Projects

Table: Top 10 BESS Projects (2024-2026)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Jupiter Power | 700 MW | Grid reliability and flexibility | Source |

| Statera Energy | 300 MW | Grid balancing services | Source |

| DTE Energy | 220 MW | Clean energy transition, coal plant replacement | Source |

| Adani Group | 1, 126 MW / 3, 530 MWh | Utility-scale energy storage | Source |

| Not specified | 7, 800 MWh | National energy transition support | Source |

| Indi Grid / IFC | 180 MW / 360 MWh | Grid stability, renewable integration | Source |

| Energy Vault | 150 MW / 300 MWh | ERCOT grid services | Source |

| Terra-Gen | 821 MW / 3, 287 MWh | Hybrid solar-plus-storage | Source |

| Quinbrook / Primergy | 380 MW / 1, 416 MWh | Solar energy time-shifting | Source |

| Vistra Energy | 350 MW / 1, 400 MWh | Grid reliability and capacity | Source |

North America BESS Market to Reach $50B by 2031

This chart quantifies the significant market opportunity in North America, providing regional context for the continent’s largest operational BESS, the Moss Landing Power Plant.

(Source: Mordor Intelligence)

Grid Firming Applications, Adani’s 3.5 GWh Project Signals Mainstream BESS Adoption

The range of applications for these top-tier projects confirms that BESS is no longer a niche asset for frequency regulation. Instead, it is being deployed for core grid functions. The most significant pattern is the use of BESS for firm capacity and peaker plant replacement. For example, DTE Energy’s planned 220 MW project is sited at a retired coal plant, explicitly serving as a clean energy substitute. Similarly, the enormous scale of the Saudi Arabian 7.8 GWh system and Adani’s 3.5 GWh project in India is designed to provide long-duration storage that firms up intermittent renewables and provides reliable power for hours at a time. This is a strategic departure from the shorter-duration batteries of the past, indicating that utilities and grid operators now see BESS as a direct competitor to natural gas peaker plants.

Battery Trading Revenue Models Compared for 2026

The section focuses on ‘Grid Firming Applications,’ and this chart directly illustrates the various revenue models associated with those applications, connecting the project’s function to its financial viability.

(Source: ESS News)

US & India Lead BESS Deployments, Vistra Energy and Adani Group Projects Set Pace

Geographically, the United States remains the most active market for large-scale BESS deployment, driven by strong policy support and urgent grid needs. California continues to be a global hub, with massive hybrid projects like Edwards & Sanborn (821 MW BESS) and standalone systems like Vistra Energy’s Moss Landing expansion solidifying its leadership. Texas is another key market, with projects like Energy Vault’s 150 MW facility targeting the volatile ERCOT grid. However, the most significant trend is the emergence of new gigawatt-scale markets. India’s energy transition is fueling massive investments, exemplified by Adani Group’s strategic entry and the Indi Grid/IFC partnership. Likewise, Saudi Arabia’s 7.8 GWh installation demonstrates how oil-rich nations are leveraging BESS to modernize their grids and facilitate a shift towards renewables, establishing a new frontier for giga-scale projects.

Battery Storage to be 28% of New US Capacity

This chart provides concrete data to support the section’s headline that the US is leading BESS deployments, showing that battery storage constitutes a significant portion of all new power capacity.

(Source: ESS News)

Vistra Energy’s 1.4 GWh Moss Landing Expansion Demonstrates BESS Scalability (2024)

The successful operation and expansion of these projects reveal the commercial maturity and scalability of BESS technology. The completion of Vistra Energy’s 350 MW / 1, 400 MWh expansion at Moss Landing in 2024 underscores that multi-hundred-megawatt systems are not just viable but can be expanded modularly. Furthermore, the commissioning of the world’s largest solar-plus-storage projects, Edwards & Sanborn (821 MW BESS) and Gemini (380 MW BESS), proves that the co-location model is a mature and effective strategy for delivering dispatchable renewable energy. While standalone storage projects like the 700 MW Jupiter Power facility in Massachusetts show maturity in grid-support applications, the seamless integration of GWh-scale batteries with nearly a gigawatt of solar PV represents the market’s leading edge. These installations confirm that BESS technology is ready for prime time as a foundational element of the modern grid.

Global BESS Projects Reach Gigawatt Scale

The section discusses the scalability of Vistra’s Moss Landing expansion, and the chart perfectly illustrates the global trend of projects reaching the gigawatt scale that Moss Landing exemplifies.

(Source: Blackridge Research & Consulting)

7.8 GWh, Saudi Arabia’s BESS Signals Shift to Long-Duration Storage

Looking ahead, the single most critical expectation is that the market will increasingly prioritize and value BESS projects with longer storage durations—typically four hours or more. This shift is essential for moving beyond ancillary services and enabling BESS to function as a true capacity resource that can replace fossil fuel generation. Recent data provides clear signals of this trend gaining traction.

- The connection of the Saudi Arabian 7.8 GWh project in December 2025 establishes a new global standard focused on massive energy capacity (MWh) rather than just power (MW).

- Adani Group’s planned 1, 126 MW / 3, 530 MWh project in India, announced in November 2025, features an approximate 3.1-hour duration, clearly targeting energy time-shifting and capacity support.

- Leading US projects like the Moss Landing expansion (1, 400 MWh for 350 MW) and Edwards & Sanborn (3, 287 MWh for 821 MW) both have a 4-hour duration, cementing this as the benchmark for utility-scale applications in mature markets.

- Policy drivers, such as the state mandates in Massachusetts that spurred the 700 MW Jupiter Power facility, are increasingly structured to procure reliable capacity, inherently favoring longer-duration storage systems.

Global Energy Storage Additions Forecasted to Grow

The chart’s forecast of growing global additions provides a forward-looking context for the massive 7.8 GWh Saudi Arabian project, which is a key contributor to this future growth.

(Source: ESS News)

The questions your competitors are already asking

This report covers one angle of the strategic pivot to gigawatt-hour BESS deployments. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the utility-scale BESS market?

- What is the outlook for multi-gigawatt-hour BESS deployment in key markets like the US, India, and Saudi Arabia by 2030?

- Adani’s 3.5 GWh facility and Jupiter Power’s 700 MW plant. Are these landmark projects progressing from announcement to deployment on schedule?

- Which grid operators in the US and Europe are adopting BESS to replace conventional peaker plants?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.