Black Rock DAC Strategy, $550 M Occidental Investment, $38 B AES Talks, and 2 Major CCUS Partnerships (2025)

DAC Commercialization, Black Rock Backs Industrial Giants and Infrastructure

In 2025, Black Rock pivoted from a passive observer to a primary financial architect in the carbon management sector, shifting the industry’s focus from early-stage technology pilots to bankrolling commercial-scale infrastructure. The firm’s strategy bypasses direct technology development in favor of large-scale capital allocation to established energy and infrastructure companies, de-risking the capital-intensive path to gigaton-scale carbon removal.

- Prior to 2025, the Direct Air Capture (DAC) market was characterized by venture funding for technology startups and smaller-scale pilot projects. The focus was on validating novel capture methods and securing preliminary offtake agreements.

- The turning point in 2025 was Black Rock‘s $550 million investment in Occidental Petroleum‘s STRATOS project. This signaled a strategic preference for funding the execution capabilities of industrial incumbents over the technological risk of startups.

- This approach was further solidified by the firm’s use of its subsidiary, Global Infrastructure Partners (GIP), to pursue a $38 billion takeover of utility AES and partner with Italian energy major Eni. This demonstrates a dual strategy of funding carbon capture projects while simultaneously acquiring the underlying energy assets needed to power them.

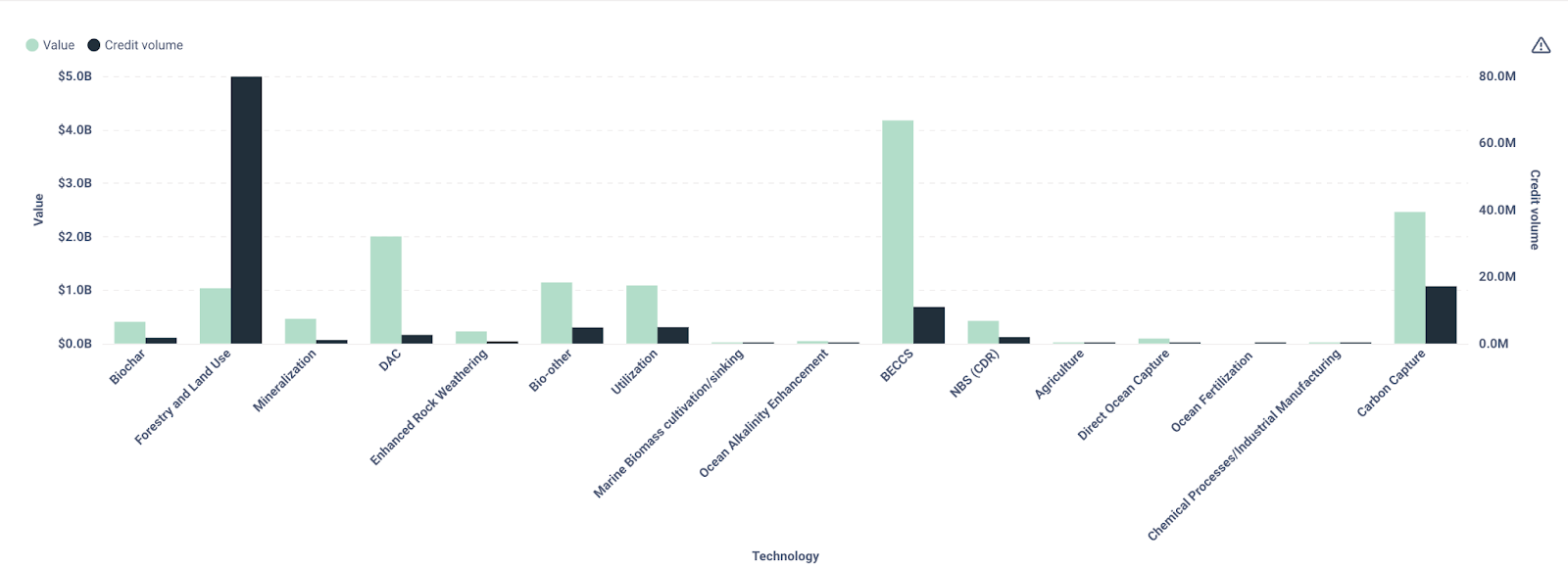

2025 Carbon Removal Market Landscape Detailed

This section outlines Black Rock’s strategy to back industrial giants for DAC commercialization. The chart detailing the 2025 carbon removal market landscape provides the necessary context, showing the key players and overall structure of the market where Black Rock is deploying its strategy.

(Source: AlliedOffsets)

$38 B AES Bid, Black Rock’s Capital Allocation for Carbon Management

Black Rock’s 2025 investment activity reveals a clear strategy to deploy massive capital into tangible, hard assets across the carbon management value chain. The firm is making multi-billion-dollar moves to secure both the technology platforms and the critical energy infrastructure required for them to operate at scale, establishing a powerful financial flywheel.

- The most significant potential transaction is the advanced discussion by Black Rock-owned GIP to acquire utility AES for $38 billion. This move would provide control over vast power generation assets, creating a vertically integrated path to supply low-carbon electricity to energy-intensive DAC facilities.

- Black Rock committed a direct $550 million investment into Occidental‘s 1 Point Five subsidiary to fund the construction of the STRATOS DAC plant in Texas. This provides the necessary project financing to build the world’s largest such facility.

- In Europe, the firm made a strategic investment in Eni‘s CCUS business, with a deal valuing the unit at $1.2 billion. This provides Black Rock with a significant stake in a portfolio of European carbon capture projects and validates the commercial case for the technology.

Q1 2025 Carbon Removal Market Transactions

This section focuses on a significant capital allocation event, Black Rock’s bid for AES. The chart showing Q1 2025 market transactions provides a timely, relevant backdrop, illustrating the active deal-making environment in which this major bid takes place.

(Source: AlliedOffsets)

Table: Black Rock Strategic Investments in Carbon Management

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| AES | Oct 2025 | Advanced talks for a $38 billion acquisition by Black Rock‘s GIP. Aims to control a major utility to power and support large-scale decarbonization projects. | Energy Central |

| Eni | Jul 2025 | Black Rock invested in Eni‘s CCUS business, which was valued at $1.2 billion. This move secures a foothold in the European carbon capture market with an established energy player. | Carbon Herald |

| Occidental (STRATOS) | Feb 2025 | Black Rock made a $550 million investment in 1 Point Five to directly finance the construction of the STRATOS DAC plant, the world’s largest. | [PDF] The CCC UK |

Black Rock Forges 3 Alliances with Eni, Occidental, and AES (2025)

In 2025, Black Rock leveraged partnerships as its primary mechanism to enter and shape the carbon management industry, pairing its immense financial resources with the operational and technical expertise of established energy leaders. These collaborations are structured to mobilize capital for infrastructure rather than engage in direct technology co-development.

- A pivotal partnership was formed through an exclusivity agreement between Black Rock‘s GIP and Eni in May 2025. The agreement concerns a potential co-control stake in Eni‘s CCUS holding, combining GIP’s infrastructure investment expertise with Eni‘s technical capabilities to scale projects like the Ravenna CCS Hub.

- The firm’s $550 million investment in Occidental‘s 1 Point Five subsidiary functions as a deep financial partnership. It enables Occidental to construct the $1.3 billion STRATOS project while giving Black Rock significant financial exposure to the world’s flagship DAC facility.

- A broader, synergistic partnership was launched in September 2025 with GIP, Microsoft, and MGX to raise up to $100 billion for AI infrastructure. This creates a blueprint for financing energy-intensive technology sectors and establishes a future customer base for the decarbonization solutions Black Rock is funding.

M&A and Partnerships a Top-Tier Board Priority

The section highlights Black Rock’s specific alliances in 2025. The chart provides the broader strategic context, showing that M&A and partnerships are a top-tier board priority, thus rationalizing Black Rock’s focus on forging such alliances as a core part of its strategy.

(Source: The Harvard Law School Forum on Corporate Governance)

Table: Black Rock Carbon Management Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| AES | Oct 2025 | Advanced takeover talks via GIP aim to create a partnership for deploying decarbonization technologies across a major US utility’s asset portfolio. | Energy Central |

| Eni | May 2025 | GIP signed an exclusivity agreement for a co-control stake in Eni‘s CCUS holding, creating a formal structure to jointly develop and scale European carbon capture assets. | Carbon Capture Magazine |

| Occidental Petroleum | Feb 2025 | A $550 million investment created a financial partnership to build the STRATOS DAC facility, with Black Rock providing capital and Occidental providing project execution. | [PDF] The CCC UK |

Texas vs Europe, Black Rock’s Dual-Pronged Geographic DAC Strategy

Black Rock‘s 2025 capital deployment shows a clear, dual-pronged geographic strategy focused on the two most mature markets for carbon management: the United States and Europe. The firm is targeting regions with strong policy support and established industrial partners capable of executing large-scale projects.

- In the United States, Black Rock‘s strategy is anchored in Texas, capitalizing on favorable geology for CO₂ sequestration and strong policy incentives like the 45 Q tax credit. Its investment in Occidental’s STRATOS project in the Permian Basin places it at the epicenter of the nascent US DAC industry.

- In Europe, the firm is focused on industrial CCUS through its partnership with Eni. The investment and collaboration target projects like the Ravenna CCS Hub in Italy, leveraging Eni‘s existing infrastructure and expertise to capture emissions from hard-to-abate industries.

- This geographic focus differs from the pre-2025 landscape, which saw more distributed, smaller-scale DAC pilots across various locations, including Switzerland (Climeworks) and Canada (Carbon Engineering). Black Rock‘s entry has concentrated major capital flows into hubs with clear commercialization pathways.

US Dominates Announced DAC Project Pipeline

The section discusses Black Rock’s geographic strategy for DAC, comparing the US (Texas) and Europe. The chart visually supports this by highlighting the dominance of the US in the announced DAC project pipeline, providing a macro context for Black Rock’s focus on Texas.

(Source: Internationale Politik Quarterly)

CCUS and DAC Maturity, Black Rock Bets on Scalable Execution

The year 2025 marks the point where Black Rock validated large-scale DAC and CCUS as a viable asset class for institutional investment, shifting the measure of maturity from technology readiness levels to commercial deployability. The firm’s strategy is to finance the scaling of proven technologies rather than funding early-stage R&D.

- Before 2025, the maturity of DAC was debated, with costs ranging from $200 to $700 per ton and no commercial-scale plants in operation. The sector was largely in the pilot and demonstration phase.

- Black Rock’s $550 million backing of Occidental’s STRATOS plant, which uses Carbon Engineering’s liquid-solvent technology, represents a bet on execution and scale. The project, designed to capture 500, 000 metric tons per year, moves the technology from demonstration to its first commercial iteration.

- Similarly, the investment in Eni’s CCUS business signals confidence in the maturity of point-source capture for industrial decarbonization. It treats carbon capture not as a novel climate tech but as essential industrial infrastructure, a view reinforced by the acquisition of GIP. The Carbon Capture DAC Market Report 2026: Key Growth Trends will likely reflect this shift towards infrastructure-led growth.

Direct Air Capture Market to See Explosive Growth

The section details Black Rock’s bet on the scalable execution of DAC, which is underpinned by the technology’s growing maturity. The chart’s forecast of explosive growth for the DAC market directly illustrates the opportunity Black Rock is aiming to capture through scalable solutions.

(Source: Market.us)

SWOT Analysis, Black Rock’s Carbon Infrastructure Financial Strategy

Black Rock‘s 2025 strategy positions it as a dominant financial force in carbon management by leveraging its core strengths in asset management and infrastructure investment. However, this approach also creates dependencies on policy and the execution capabilities of its partners.

- The firm’s primary strength is its ability to deploy massive, patient capital into infrastructure-scale projects, de-risking the sector for the broader market.

- A key weakness is its indirect model, which relies on the operational success of partners like Occidental and Eni to deliver returns and technological progress.

- The main opportunity lies in architecting the financial ecosystem for a multi-trillion-dollar carbon removal industry and capturing value across the entire chain, from power generation to sequestration.

- The most significant threat is policy risk, as the profitability of these investments, particularly in the U.S., is heavily dependent on the stability and longevity of incentives like the 45 Q tax credit.

Charts Compare DAC Cost-Benefit to Renewables

This section covers the SWOT analysis of Black Rock’s financial strategy. A core component of such an analysis is understanding the economic viability of the investment. The chart comparing the cost-benefit of DAC to renewables provides crucial data for assessing the Opportunities (e.g., potential for high returns) and Threats (e.g., competition from cheaper alternatives) in the SWOT framework.

(Source: Nature)

Table: SWOT Analysis for Black Rock’s Carbon Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Passive equity holdings in energy companies; large AUM. | Active infrastructure investment via GIP; direct project financing ($550 M in STRATOS); ability to orchestrate multi-billion-dollar deals ($38 B AES talks). | The acquisition of GIP transformed Black Rock from a passive shareholder into an active infrastructure developer with deep operational expertise. |

| Weaknesses | Limited direct involvement in technology or project development; exposed to broad market risk of energy sector. | Reliance on partners (Occidental, Eni) for project execution and technology performance; investments are highly capital-intensive and illiquid. | The firm’s financial commitment is now directly tied to the success of specific, first-of-a-kind commercial projects, increasing concentrated risk. |

| Opportunities | Growing corporate demand for carbon credits; emerging policy support for carbon removal. | Architecting the financial market for carbon management; creating synergies with other infrastructure plays (AI data centers); first-mover advantage among asset managers. | Black Rock validated carbon infrastructure as a major asset class, opening the door for large-scale institutional investment beyond venture capital. |

| Threats | Technological uncertainty of DAC; high cost of capture; reputational risk from ESG criticism. | Policy instability (changes to 45 Q tax credit); potential underperformance of large-scale projects (STRATOS); competition from other financial giants entering the space. | The reliance on policy became an explicit financial risk, as the bankability of projects like STRATOS depends directly on the $180/ton tax credit. |

$100 B AI Fund, Black Rock’s Blueprint for Future DAC Hubs

Looking ahead, the primary indicator of Black Rock’s strategy will be its ability to replicate its 2025 capital formation model for other large-scale, energy-intensive technology sectors. The partnership with Microsoft and MGX to raise up to $100 billion for AI infrastructure serves as a direct blueprint for financing future DAC hubs.

- If this happens: The $38 billion acquisition of AES by GIP is finalized. Watch this: How GIP directs AES‘s capital expenditure toward developing low-carbon power generation specifically to support DAC and other clean tech ventures. This would signal a move toward creating closed-loop energy and decarbonization systems.

- And these could be happening: The initial operational data from STRATOS in late 2025 or early 2026 validates its capture efficiency and energy consumption metrics. This would trigger further direct investments by Black Rock into a portfolio of DAC projects, potentially with other Carbon Capture & DAC Leaders: 2026 Market Analysis.

- And these could be happening: Black Rock announces a dedicated carbon management infrastructure fund, using the AI partnership model to attract sovereign wealth and pension fund capital. This would cement its role as the market-maker for the entire carbon removal industry.

The questions your competitors are already asking

This report covers one angle of BlackRock’s capital-led strategy for commercializing Direct Air Capture. The questions that matter most depend on your work.

- Which industrial incumbents are gaining ground in the DAC market due to BlackRock’s capital-first strategy?

- BlackRock’s $550M investment in Occidental’s STRATOS project. Is the initiative progressing from announcement to commercial-scale deployment?

- What are the opportunities for energy and infrastructure companies in the DAC market, following BlackRock’s partnerships with Occidental and Eni?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

DAC Purchase Volume Peaks in 2023

This section focuses on competitive intelligence. A chart showing a peak in purchase volume in the previous year would spark urgent questions among competitors about market demand saturation or volatility, making it a key topic for analysis.

(Source: CDR.fyi)