DAC Biorefinery Model, $139/Tonne Capture Cost, Puro.earth Methodology, and 2 Corporate Offtakes (2021 to 2026)

Microalgae Biorefinery Model Shifts Projects from Pure DAC to Co-Product Revenue

The commercial strategy for microalgae-based carbon capture is pivoting from theoretical, large-scale direct air capture (DAC) to integrated biorefineries that depend on high-value co-products to achieve economic viability. The immense capital and operational costs associated with cultivating microalgae at a scale sufficient for gigatonne-level carbon removal cannot be supported by revenue from carbon credits alone. Instead, a successful business model requires stacking revenue from biofuels, bioplastics, and nutraceuticals, with carbon credits acting as a supplemental income stream rather than the primary driver.

- Between 2021 and 2024, the narrative centered on the high biological efficiency of microalgae, which can fix approximately 1.8 kg of CO 2 for every kilogram of biomass produced. However, the high costs of production and the logistical challenges of a 100, 000 km² deployment remained significant barriers, confining most activity to research and small pilots.

- From 2025 to 2026, the market underwent a “reckoning, ” shifting focus toward commercially viable applications. This pivot is validated by the projected growth of the algae biofuel market to $18.64 billion by 2032. The approval of a new carbon credit methodology by Puro.earth in October 2025 for microalgae-based sequestration was a critical step, enabling projects to monetize their carbon removal component within a broader, more resilient biorefinery economic model.

- The fundamental challenge remains the cost of capture. While projections suggest costs could fall below $50 per ton by 2030, current reported costs are as low as $139 per tonne, which is still often above the price of credits in voluntary markets ($10-$30 per ton). This pricing gap necessitates revenue from co-products to make projects bankable.

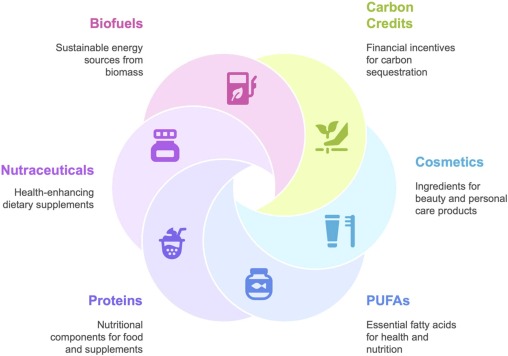

Diagram Shows Microalgae Co-Product Strategy

The diagram is a direct visual representation of the biorefinery model described in the section, illustrating how shifting from pure DAC to a co-product strategy can generate additional revenue streams.

(Source: ScienceDirect.com)

$13 M in Series A Funding, Algama Foods Demonstrates Investor Focus on Protein Co-Products

Recent investment flows into the microalgae sector are not targeting pure carbon capture but are instead directed at companies with a clear path to commercializing high-value bioproducts like proteins, validating the biorefinery economic model. This trend indicates that investors prioritize tangible, established markets over the more speculative and volatile carbon credit market. Capital is following the revenue, and the most bankable revenue is currently in food, feed, and materials, not just carbon.

- In April 2024, Paris-based microalgae producer Algama Foods secured a €13 million Series A funding round to scale up its food product development. This investment highlights the strong market interest in algae as a source of alternative proteins, a market projected to reach $877.12 million by 2030.

- Similarly, Israeli startup Brevel is advancing its commercial model by securing long-term off-take agreements and joint ventures for its non-GMO, microalgae-based protein. This strategy de-risks its expansion by locking in future revenue from established food and nutrition markets.

- While North American startups attracted $410 million in venture capital in 2025, the funding has largely targeted biotechnology applications. There remains a significant lack of major direct investment for gigatonne-scale, carbon-only microalgae projects, reinforcing that carbon capture must be a co-benefit of a profitable biorefinery.

Model Shows Microalgae DAC for CO2-Neutral Cities

This conceptual model illustrates a visionary application of microalgae technology. Such large-scale potential is used to attract investor interest, providing context for the investment focus detailed in the section on Algama Foods’ funding.

(Source: ScienceDirect.com)

Table: Strategic Investments in Microalgae Co-Product Commercialization

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Algama Foods | April 2024 | Received a €13 million Series A funding round led by the venture capital fund of Thai Union. The investment is aimed at scaling the production of microalgae for food applications, demonstrating investor confidence in the high-value protein market. | [PDF] GFI.org |

Microsoft Offtake Agreements Signal Demand for Verifiable Carbon Removal Credits (2025 to 2026)

Corporate offtake agreements, led by buyers like Microsoft, are becoming a critical financing mechanism for the carbon removal industry, but their stringent requirements for durability and verification present a high bar for biological methods. The surge in long-term contracts for verified carbon dioxide removal (CDR) tonnes provides a potential revenue lifeline for microalgae projects, but only if they can prove their sequestration is permanent and auditable. This market pressure is driving the need for robust MRV (monitoring, reporting, and verification) and certified methodologies.

- A market shift occurred in 2025, with a surge in long-term carbon credit offtake agreements totaling $12 billion. This trend provides a clear demand signal and a path to bankability for new carbon removal projects that can meet buyer criteria.

- In early 2026, Microsoft continued its leadership in the space, signing a flurry of large-scale deals, including one for 626, 000 tonnes of durable carbon removal over 15 years and another for 2.85 million soil carbon credits. These agreements underscore the corporate focus on high-quality, verifiable credits.

- This demand for quality directly incentivizes the development of rigorous standards. The approval of the Microalgae Carbon Fixation and Sinking (MCFS) methodology by Puro.earth in October 2025 was a direct response to this need, creating a pathway for microalgae projects to sell credits into the high-quality voluntary market.

Global Carbon Credit Issuance Declines Since 2021

This chart provides crucial market context for the Microsoft agreements. The decline in overall credit issuance suggests a ‘flight to quality,’ underscoring the significance of major corporations seeking out high-integrity, verifiable carbon removal credits.

(Source: ScienceDirect.com)

Table: Key Market-Enabling Partnerships and Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Microsoft Offtake Deal | April 2026 | Signed a 626, 000-tonne carbon removal agreement with a Canadian carbon capture project, demonstrating strong corporate demand for high-volume, long-duration carbon removal credits, which provides a key revenue target for emerging technologies. | ESG News |

| Puro.earth Methodology Approval | October 2025 | The advisory board approved a new methodology for Microalgae Carbon Fixation and Sinking (MCFS). This creates a certified framework for microalgae projects to issue carbon credits, enabling them to access revenue from corporate buyers and the voluntary carbon market. | Carbon Herald |

| Brevel Offtake Agreements | November 2024 | The Israeli startup is securing long-term off-take agreements and joint ventures for its non-GMO microalgae protein. This de-risks commercial scaling by locking in revenue from the established food ingredients market, independent of volatile carbon credit prices. | Israel Agri |

North America Leads Microalgae Innovation with 48% of Genetic Engineering Patents

North America has established itself as the primary hub for microalgae biotechnology innovation and investment, driven by a combination of strong venture capital interest and supportive government policy. While the theoretical application for large-scale DAC is global, the commercial and technical development is currently concentrated in the United States, which provides a favorable environment for scaling up high-value bioproduct applications.

- From 2025 to 2026, North America’s leadership position solidified. The region holds 48% of patents in microalgae genetic engineering and attracted $410 million in venture capital for related startups in 2025 alone.

- U.S. policy provides a significant advantage. The enhanced Section 45 Q tax credit offers $85 per ton for CO 2 that is captured and geologically sequestered, creating a powerful financial incentive for projects that can integrate algae cultivation with permanent storage.

- Other regions are also fostering development. Australia’s Cooperative Research Centres Projects (CRC-P) grants support collaborative research that can include algae-based technologies, but the scale of investment and patent activity remains centered in North America.

Chlorella Strain Shows Superior Biomass Productivity

This chart offers a concrete example of the innovation discussed in the section. The superior productivity of a specific strain is a direct result of the genetic engineering and R&D efforts in which North America holds a leading patent position.

(Source: Frontiers)

Microalgae Cultivation is Mature (TRL 7/8) but Integrated CCUS Remains at Pilot Stage

While the core technology for cultivating specific microalgae species is commercially mature, with some processes reaching Technology Readiness Level (TRL) 7/8, the integrated systems required for cost-effective carbon capture, utilization, and storage (CCUS) at scale remain at a lower TRL. The primary challenge has shifted from simply growing algae to engineering and optimizing a complete system that includes CO 2 uptake, nutrient supply, harvesting, processing, and monetization of all outputs in a financially and energetically positive manner.

- Between 2021 and 2024, research confirmed the high TRL for specific cultivation methods, such as a diatom cultivation process rated at TRL 7/8 (system prototype demonstration in an operational environment). This established the biological feasibility of growing algae at scale.

- From 2025 onwards, the focus has turned to system integration, which remains a key bottleneck. The U.S. Department of Energy reports that integrated CCUS systems leveraging algae are generally at a lower TRL and require further development to move from pilot to commercial scale.

- The market’s increasing demand for verifiable carbon removal adds another layer of technical complexity. Proving the permanence of sequestered carbon in biological systems requires mature monitoring, reporting, and verification (MRV) technology, which is still under development for many microalgae applications.

Chart Shows High Cost is a Barrier to Scaling Carbon Capture

This chart explains the core argument of the section. The high cost of carbon capture is a primary reason why integrated CCUS technology, despite mature cultivation methods, remains at a pre-commercial pilot stage (TRL 7/8).

(Source: Belfer Center)

SWOT Analysis: Microalgae DAC Economics and Commercial Viability

Microalgae’s primary strength is its biological efficiency and its potential for co-product revenue, but this is counteracted by the profound weakness of high capital costs and an economic model that is dependent on nascent carbon markets. The pivot toward an integrated biorefinery model is a direct response to these weaknesses, leveraging market opportunities in biofuels and nutrition while navigating threats from cheaper abatement solutions.

DAC Cumulative Costs to Exceed $2.5T by 2060

The chart’s projection of massive cumulative costs serves as a quantitative basis for the ‘Weakness’ or ‘Threat’ component of the SWOT analysis, highlighting the significant economic challenges to commercial viability.

(Source: Belfer Center)

Table: SWOT Analysis for Microalgae Carbon Capture Farms: Biological DAC Across 100, 000 Square Kilometers

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High CO 2 fixation efficiency (up to 2.0 kg CO 2 per kg biomass). Versatile biomass for various co-products. | Demonstrated ability to produce high-value proteins (Brevel, Algama Foods). Biofuel market projected to grow at 8.8% CAGR. | The value of the biorefinery model was validated as the primary path to commercialization, moving from theory to practice with funded companies. |

| Weaknesses | Extremely high capital expenditure (CAPEX) for photobioreactors and high biomass production costs (up to $2, 040/tonne). High energy and nutrient inputs. | Continued reliance on nascent carbon markets with low credit prices ($10-$30/ton) insufficient to cover costs. Lack of integrated, commercial-scale CCUS systems. | The economic weakness of a carbon-only model was confirmed by a “market reckoning” in the voluntary carbon market, forcing a pivot to co-products. |

| Opportunities | Growing global CCUS market and corporate net-zero pledges. Potential for government support like the 45 Q tax credit. | Surge in corporate offtake agreements (Microsoft deals). Approval of new carbon credit methodologies (Puro.earth) opens access to revenue. 45 Q credit provides $85/tonne for sequestered CO 2. | The pathway to monetizing carbon capture as part of a stacked revenue model became clearer through new methodologies and strong corporate demand for verified credits. |

| Threats | Competition from lower-cost carbon abatement technologies. Logistical and environmental constraints (land, water use) of massive-scale deployment. | Increased scrutiny on the permanence and verification of biological carbon removal. Volatility in carbon credit markets continues to be a major financing risk. | The market threat shifted from just cost competition to “quality competition, ” as buyers now demand rigorous proof of permanent carbon removal, a high bar for biological systems. |

Microalgae 2027 Outlook: Success Hinges on Securing High-Value Offtake Agreements

The trajectory for microalgae carbon capture projects in the next one to two years will be determined not by their carbon capture potential alone, but by their ability to secure bankable, long-term offtake agreements for high-value bioproducts like proteins and biofuels. These agreements are essential for de-risking the high capital investment required for new facilities and provide a stable revenue foundation that volatile carbon markets cannot currently offer.

- If this happens: More companies like Brevel successfully sign long-term joint ventures and offtake agreements for their protein or bioplastic outputs, particularly with major consumer-packaged goods or chemical companies.

- Watch this: Track the price and trading volume of microalgae-derived carbon credits issued under new, high-quality methodologies like Puro.earth‘s. A steady increase in both would signal growing market confidence in the permanence and verifiability of biological carbon removal, making the carbon credit portion of the revenue stack more bankable.

- These could be happening: Startups will increasingly brand themselves as “sustainable materials” or “alternative protein” companies that also capture carbon, rather than as pure-play carbon capture companies. This strategic positioning aligns their business model with stronger, more established markets while retaining the climate benefits as a key value proposition.

DACCS Costs Projected to Remain High Through 2060

This long-term cost projection provides the economic rationale for the section’s outlook. It shows that because DACCS is expected to remain expensive, securing high-value offtake agreements is a critical and necessary strategy for near-term success.

(Source: Belfer Center)

The questions your competitors are already asking

This report covers one angle of the commercial pivot from pure microalgae DAC to integrated biorefineries. The questions that matter most depend on your work.

- What is actually happening with microalgae biorefinery projects since the Puro.earth methodology was approved in October 2025?

- What is the cost breakdown of a commercial-scale microalgae biorefinery, and what is the path from $139/tonne to sub-$50/tonne capture costs?

- What are the opportunities for co-products like biofuels and bioplastics in the emerging microalgae biorefinery market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.