Chevron DAC Infrastructure Strategy, Bayou Bend Hub with Talos Energy, 3 Key Partnerships, and a $180/ton 45 Q Credit Focus (2021-2025)

CCUS Industry Adoption, Chevron’s Infrastructure-First Model

Chevron’s 2025 strategy for carbon capture is a deliberate shift away from pioneering novel Direct Air Capture (DAC) technology and toward building large-scale, shared CO 2 transportation and storage infrastructure. This infrastructure-first model positions the company as a foundational service provider for the emerging carbon management economy, prioritizing asset ownership and project execution over high-risk technology development. This approach became concrete in 2025 with the advancement of major hub projects, a change from the more exploratory partnerships seen between 2021 and 2024.

- From 2021 to 2024, energy majors explored various CCUS pathways, with many investments focused on pilot projects or corporate venture capital stakes in technology startups. The market lacked large-scale, committed infrastructure projects.

- In 2025, Chevron’s strategy solidified around its joint venture for the Bayou Bend CCS hub on the Texas Gulf Coast, a project designed to serve multiple industrial emitters. This signals a transition from technology evaluation to building the physical backbone for regional decarbonization.

- This model contrasts with competitors like Occidental, which is pursuing vertical integration by constructing its own proprietary Stratos DAC plant. Chevron aims to build the “pipelines and reservoirs” for the entire industry, including for future competitors in the DAC technology space.

- The adoption of this strategy is enabled by the maturity of point-source capture technologies and the high Technology Readiness Level (TRL) of key DAC components, allowing Chevron to focus on its core competencies: geology, reservoir management, and large-scale project execution. The broader market shows a clear need for these capabilities, as seen in the latest Carbon Capture & DAC Leaders: 2026 Market Analysis.

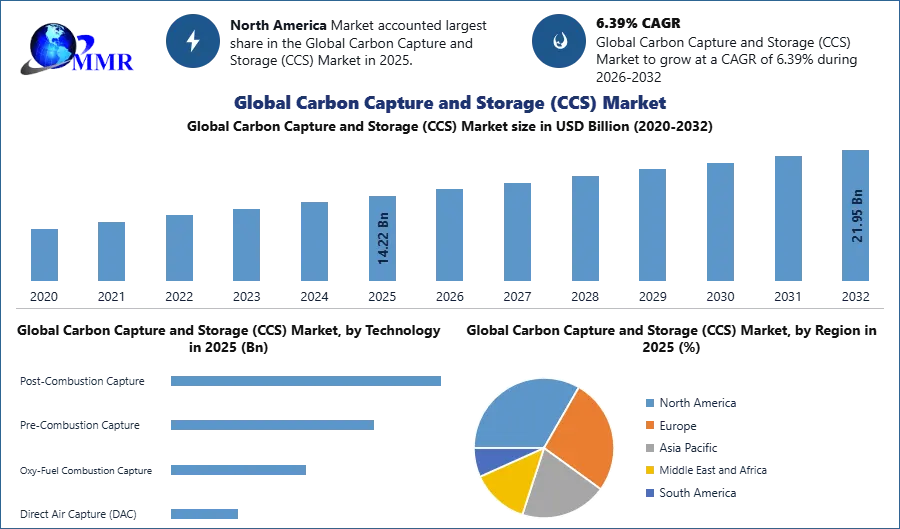

Global CCS Market Forecast to Reach $21.95B

This chart’s forecast of a significant global market for Carbon Capture and Storage (CCS) provides the high-level context for the section’s discussion on broad industry adoption and validates Chevron’s ‘infrastructure-first’ model as a strategy to capture a share of this growing market.

(Source: maximize market research)

$180/ton in Credits, Chevron’s 45 Q-Dependent Investment Model

Chevron’s capital allocation for carbon management in 2025 is fundamentally shaped by the U.S. Section 45 Q tax credit, which makes capital-intensive infrastructure projects economically viable. The incentive structure directly supports the company’s focus on sequestration hubs, as the credits provide a predictable revenue stream that de-risks multi-billion dollar, long-lifecycle investments. This federal support was the primary catalyst for moving projects like Bayou Bend from concept to active development.

- The enhanced 45 Q credit, offering $180 per ton for DAC with dedicated geologic storage and $85 per ton for point-source capture, provides the financial foundation for Chevron’s CCUS projects. This incentive makes the difference between a viable and non-viable project, given current DAC costs of $500 to $1, 000 per ton.

- In February 2025, Chevron reaffirmed its shareholder return plans while announcing a 6-8% global output growth target, indicating that lower-carbon investments are being balanced with its core business. This financial discipline underscores the need for projects to be supported by strong policy incentives like 45 Q.

- The company’s investment in the Bayou Bend CCS hub is a long-term play on the assumption that these credits will remain stable. It positions Chevron to capture value as technology costs fall and carbon removal demand rises, with the market projected to grow significantly.

Direct Air Capture Market to See Explosive Growth

The section discusses an investment model dependent on the $180/ton 45Q tax credit, a powerful incentive for Direct Air Capture (DAC). This chart’s prediction of ‘explosive growth’ in the DAC market is a direct consequence of this financial incentive, illustrating the opportunity Chevron is targeting.

(Source: Market.us)

Table: Chevron Major Carbon Capture Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bayou Bend CCS Hub | 2025 | Continued investment with partners to develop a major CO 2 sequestration hub on the U.S. Gulf Coast, targeting industrial emitters. The project is a cornerstone of Chevron’s infrastructure-first strategy. | decarbonfuse.com |

| Lower Carbon Technologies | 2025 | Sustained corporate investment in a portfolio of lower-carbon solutions, including hydrogen and carbon capture, to reduce carbon intensity while meeting energy demand. | Chevron |

Carbon Dioxide Removal Market to Exceed $3B

A table listing major investments requires justification. This chart provides it by quantifying the substantial market opportunity in Carbon Dioxide Removal (CDR), giving financial context and strategic rationale for the specific Chevron investments detailed in the section.

(Source: Precedence Research)

Chevron 3 Key 2025 Alliances for CCUS Project De-Risking (2025)

In 2025, Chevron aggressively used partnerships to distribute financial risk, access specialized technologies, and accelerate its entry into the carbon management market. These collaborations are the primary execution vehicle for its infrastructure-led strategy, allowing the company to build a diversified portfolio of lower-carbon assets without bearing the full financial and technological burden of any single project. This represents a more formalized and large-scale approach compared to the earlier-stage partnerships seen from 2021 to 2024.

- The advancement of the Bayou Bend CCS hub in August 2025 is a joint venture with Talos Energy and Carbonvert. This structure shares the immense capital cost of developing a sequestration site capable of serving a broad industrial region.

- In January 2025, a strategic partnership with Engie and GE Vernova was announced to develop a natural gas plant with integrated carbon capture. This collaboration combines Chevron’s energy market expertise with proven power generation and capture technology.

- A December 2025 agreement through its Bunge Chevron Ag Renewables (BCAR) joint venture with Cover Cress Inc. demonstrates the integration of carbon management into its renewables business, securing a low-carbon feedstock for fuel production.

Emissions Reduction, Partnerships are Key Industry Investments

This chart directly supports the section’s premise. The headline, ‘Partnerships are Key Industry Investments,’ perfectly aligns with the topic of Chevron forming key alliances to de-risk and execute its CCUS projects, reinforcing the strategic importance of collaboration.

(Source: Turbomachinery Magazine)

Table: Chevron’s 2025 Carbon Capture Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bunge, Cover Cress Inc. | Dec 2025 | Commercial offtake agreement through the BCAR joint venture to integrate a low-carbon feedstock into renewable fuel production, applying carbon management to its renewables portfolio. | World Economic Forum |

| Talos Energy, Carbonvert | Aug 2025 | Advancement of the Bayou Bend CCS joint venture, a major CO 2 transport and storage hub on the Texas Gulf Coast designed to serve as critical infrastructure for regional decarbonization. | decarbonfuse.com |

| Engie, GE Vernova | Jan 2025 | Strategic partnership to develop a U.S. natural gas plant integrated with carbon capture technology, aiming to decarbonize fossil-fuel-based power generation. | GMI Insights |

Cement Production Dips as Import Reliance Plateaus

The section details Chevron’s partnerships. This chart highlights the cement industry, a hard-to-abate sector and a prime target for CCUS technology. It provides context for the type of industrial partners Chevron would seek to help decarbonize, making the partnerships listed in the table more tangible.

(Source: ClearPath)

US Gulf Coast Focus, Chevron’s Bayou Bend Project Dominance

Chevron’s carbon management activities in 2025 are heavily concentrated on the U.S. Gulf Coast, specifically Texas and Louisiana. This geographic focus is a strategic decision based on the convergence of favorable geology for CO 2 sequestration, a high density of industrial emitters, existing pipeline infrastructure, and a supportive policy environment. The progression of the Bayou Bend project in this region represents the physical manifestation of its entire CCUS strategy.

- Between 2021 and 2024, CCUS interest was geographically dispersed, with projects and studies occurring globally. However, the passage of the Inflation Reduction Act in the U.S. created a powerful gravitational pull for investment.

- In 2025, Chevron’s primary focus is the Bayou Bend CCS project in Southeast Texas. This location offers access to one of the nation’s largest concentrations of industrial emissions, providing a ready market for CO 2 sequestration services.

- The U.S. Department of Energy’s selection of sites in Texas and Louisiana for its Regional DAC Hubs program, including Project Cypress, further validates the Gulf Coast as the epicenter of U.S. carbon removal efforts and reinforces the strategic value of Chevron’s assets in the area.

- This regional concentration allows Chevron to leverage its decades of operational experience in the Gulf Coast’s oil and gas sector, applying existing knowledge of subsurface geology and project management to the new carbon storage industry.

US Hydrogen Market to Reach $33B by 2030

The section’s focus is on the US Gulf Coast and the Bayou Bend project. This chart is highly relevant as Bayou Bend is strategically positioned to enable low-carbon (blue) hydrogen production. The projected growth of the US hydrogen market underscores the economic driver behind the project’s dominance.

(Source: MarketsandMarkets)

Technology Maturity, Chevron’s Use of Proven CCUS Components

Chevron’s 2025 approach prioritizes the integration of commercially ready technologies over the development of novel capture methods. By focusing on infrastructure, the company leverages mature components of the CCUS value chain, specifically point-source capture systems and established geologic sequestration practices, while positioning itself to service more nascent DAC technologies as they scale. This pragmatic choice minimizes technology risk and allows for more predictable project execution timelines.

- The partnership with GE Vernova and Engie to build a natural gas plant with carbon capture relies on post-combustion capture technology, which has a Technology Readiness Level (TRL) of 9 and is considered commercially proven.

- The Bayou Bend project focuses on CO 2 transport and storage, which utilizes expertise and technologies directly analogous to those used in the oil and gas industry for decades, such as pipeline transport and injection well management.

- While Direct Air Capture technologies are still maturing on the cost curve, with costs in 2025 between $500-$1, 000 per ton, their TRL is considered high enough (TRL 6-7) for initial commercial scale-up. Chevron’s strategy is to provide the storage service for these DAC plants rather than building them itself, avoiding direct exposure to the challenges facing specific ventures like those in the SCW Systems DAC deployment.

- This approach validates that the primary barrier to CCUS deployment in 2025 is not the absence of technology, but the high cost and the lack of integrated, large-scale infrastructure, which is exactly the problem Chevron aims to solve.

Oil and Gas Pipe Market to Hit $81B by 2035

This section discusses Chevron’s use of mature, proven technology. The chart, showing a robust market for pipes, illustrates the health and availability of a critical component for CO2 transportation infrastructure. This supports the claim that the components for CCUS are mature and ready for deployment.

(Source: Oil & Gas Advancement)

Chevron SWOT Analysis of its 2025 CCUS Infrastructure Strategy

An analysis of Chevron’s 2025 strategy reveals a company leveraging its core strengths to build a defensible position in a new market, while simultaneously exposing itself to significant policy-related risks. The strategy is pragmatic and capitalizes on existing competencies but relies heavily on external factors for its long-term success.

- Strengths: Chevron leverages world-class expertise in subsurface geology, reservoir management, and large-project execution, creating a strong competitive advantage in the CO 2 storage sector.

- Weaknesses: The lack of proprietary, low-cost capture technology makes Chevron dependent on partners and positions it as a service provider rather than a technology leader.

- Opportunities: The infrastructure-first model allows Chevron to become an essential, utility-like service provider for the entire carbon economy, generating stable returns from a wide range of customers.

- Threats: The strategy’s economic viability is almost entirely dependent on the stability of the 45 Q tax credit; any negative changes to this policy represent a critical threat to project profitability and timelines.

Exxon Leads in Announced Clean Hydrogen Capacity

This chart provides a key ‘Threat’ for the section’s SWOT analysis. It shows a major competitor, Exxon, leading in clean hydrogen capacity, which is often linked with CCUS. This competitive pressure directly impacts Chevron’s infrastructure strategy and highlights a major challenge it faces.

(Source: Enverus)

Table: SWOT Analysis for Chevron’s 2025 DAC and CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 and Forward | What Changed / Validated |

|---|---|---|---|

| Strengths | Core competencies in subsurface geology and large project management were recognized as transferable to CCUS. | These competencies are actively deployed in the Bayou Bend project, shifting from theoretical advantage to practical application. | The 2025 advancement of Bayou Bend validated that Chevron’s oil and gas skills are a primary competitive moat in the CCUS infrastructure segment. |

| Weaknesses | Limited in-house development of novel DAC sorbent technologies compared to some competitors. | Strategy formalizes a reliance on partners (Engie, GE Vernova) for capture technology, accepting a role as integrator and operator. | The 2025 partnerships confirmed Chevron is choosing to buy/partner for capture technology rather than build its own, focusing capital on infrastructure. |

| Opportunities | The potential for a large carbon management market was identified, contingent on policy and cost reductions. | The strategy to build service hubs positions Chevron to capitalize on a projected $217.8 billion carbon market by 2033 by serving all emitters. | The focus on hubs in 2025 shows a clear intent to capture a tolling/service fee from the broader decarbonization trend, not just its own emissions. |

| Threats | High cost of DAC and uncertainty around long-term policy support for CCUS created investment hesitation. | Heavy reliance on the $180/ton 45 Q tax credit makes the entire strategy vulnerable to future U.S. policy shifts. | The large-scale commitment in 2025 locked Chevron into a strategy highly sensitive to political risk, making policy stability the single most critical external factor. |

Direct Air Capture (DAC) Purchase Volume Trends

For a SWOT analysis on DAC strategy, this chart illustrates a clear ‘Opportunity’. The rising trend in DAC purchase volumes signals growing demand and a receptive market, validating the strategic push into DAC technology discussed in the section.

(Source: CDR.fyi)

1 Key Metric to Watch, Chevron’s Bayou Bend FID Timing

The single most important signal to monitor for Chevron’s carbon management strategy is the Final Investment Decision (FID) for the Bayou Bend CCS Hub. This milestone will move the project from the development phase to full construction, locking in major capital commitments and providing a definitive timeline for when the first large-scale, third-party CO 2 sequestration service will be available on the U.S. Gulf Coast. An on-schedule FID would validate the economic model and regulatory pathway, while any delay would signal potential headwinds.

- If an FID is announced in late 2025 or early 2026, watch for immediate announcements of major offtake agreements from industrial emitters in the Houston Ship Channel and Beaumont-Port Arthur area. These contracts would confirm market demand for the hub.

- This could mean that Chevron’s infrastructure-first strategy is gaining significant commercial traction, proving that industrial players are willing to pay for third-party sequestration services to meet their decarbonization goals.

- On the other hand, if the FID is delayed, watch for statements from Chevron or its partners citing regulatory hurdles, permitting delays, or uncertainty regarding the long-term stability of the 45 Q tax credit.

- This could mean that the perceived policy and execution risks are higher than anticipated, potentially slowing the pace of infrastructure development across the entire U.S. CCUS industry and impacting the Carbon Capture DAC market growth trends.

Hydrogen Generation Market Sees Strong Growth

The section identifies the Bayou Bend Final Investment Decision (FID) as a key metric. This chart explains why: the hydrogen market is seeing strong growth. This growth creates urgency, making the timing of the FID critical for Chevron to capitalize on the opportunity and not fall behind.

(Source: Market.us)

The questions your competitors are already asking

This report covers one angle of Chevron’s infrastructure-first strategy for carbon capture. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the CCUS infrastructure market: Chevron’s hub model vs. Occidental’s vertical integration?

- Chevron’s investments and funding. Is the Bayou Bend project on track to be commercially viable with the $180/ton 45Q credit?

- What are the opportunities for DAC technology companies in the emerging Gulf Coast carbon management market, given Chevron’s hub strategy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.