SMR Deployment for Texas Data Centers, Last Energy 600 MW Plan, Fermi America 17 GW Project, and 4 Nuclear Pacts (2025 to 2026)

Data Center Power Demand, ERCOT’s 136 GW Interconnection Queue Spurs BTM Solutions

The Electric Reliability Council of Texas (ERCOT) faces an unprecedented power demand surge, driven by AI data centers, that has rendered traditional grid interconnection untenable and forced developers toward behind-the-meter (BTM) generation. This shift is not a future possibility but a current commercial reality, as the scale and velocity of demand growth outpace the grid’s ability to respond. The market has moved from discussing grid constraints in 2024 to actively deploying BTM solutions in 2026 to bypass multi-year delays.

- Before 2025, the primary concern was a projected doubling of demand to around 150 GW by 2030, a significant but seemingly manageable long-term planning challenge. By April 2026, revised forecasts showed demand could quadruple, with high-end projections reaching 228 GW by 2032, fundamentally altering the risk calculus for grid dependency.

- The most direct evidence of this crisis is the ERCOT large load interconnection queue, which exploded from 41 GW in early 2024 to 136 GW by June 2025. With data centers accounting for over 75% of this requested load and interconnection wait times stretching 3-4 years, grid-only power strategies have become a critical business risk.

- In response, commercial activity has pivoted decisively to BTM generation. In October 2025, Oracle contracted with Volta Grid for 2.3 GW of modular natural gas power. In January 2026, Matrix Data Centers broke ground on a campus powered by a Bloom Energy fuel cell microgrid. These deals, along with plans by Last Energy for 600 MW of microreactors, signal a definitive move to secure power independent of the main grid.

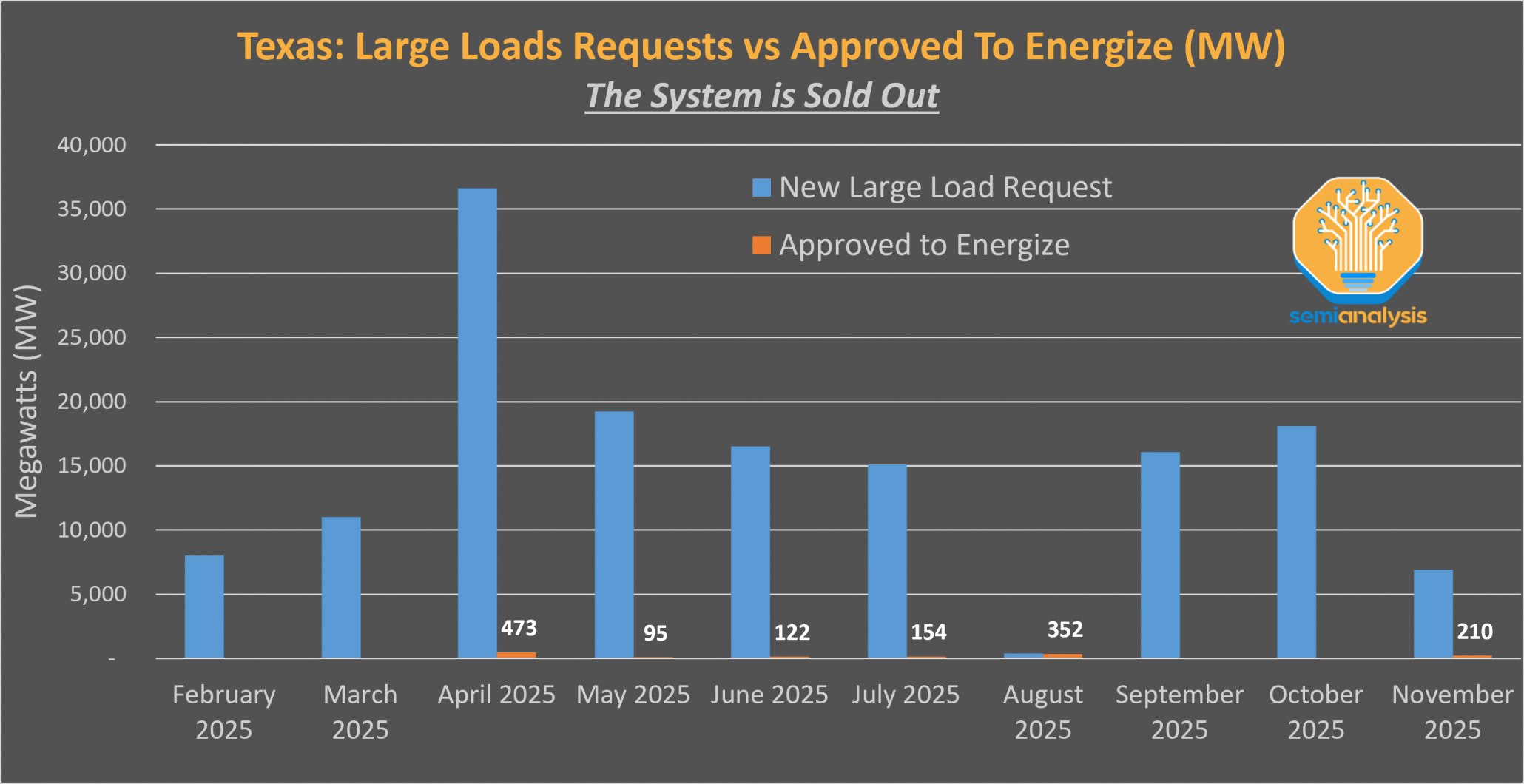

Texas Grid Overwhelmed by Power Demand

This chart perfectly visualizes the section’s core topic: the massive gap between new power demand and grid capacity in Texas. It substantiates the claim that the interconnection queue is untenable, forcing a pivot to behind-the-meter solutions.

(Source: SemiAnalysis)

$7.65 B in Fuel Cell Deals, Bloom Energy’s Market Capture for Data Centers

Capital is flowing decisively toward technologies that offer speed and reliability, with fuel cells emerging as a primary beneficiary of the urgent need for on-site power. Investment patterns in 2025-2026 show a clear preference for deployable, modular solutions that can be brought online within the aggressive timelines of AI infrastructure projects, a stark contrast to the more speculative, long-term investments that characterized the preceding period.

- A $7.65 billion wave of data center deals for fuel cells was recorded in a 90-day period in early 2026, signaling rapid market validation. This investment is predicated on the technology’s ability to be deployed in 12-18 months, directly addressing the multi-year grid interconnection bottleneck.

- This contrasts with the 2021-2024 period, where major announcements like ECL’s planned 1 GW off-grid hydrogen data center, with an estimated $8 billion total installed cost, represented ambitious long-term goals rather than immediate, scalable deployments.

- While renewable Power Purchase Agreements (PPAs) continue, such as Meta‘s agreement for a 600 MW solar plant from Enbridge, the market now recognizes that intermittent sources alone are insufficient. The new investments in firm power technologies like fuel cells are designed to complement these renewable sources and ensure the “five nines” (99.999%) reliability that data centers require.

Table: Key Investments in Texas Data Center Power Solutions

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Market | Early 2026 | Secured an estimated $7.65 billion in data center deals over a 90-day period, driven by the need for rapid deployment to bypass grid queues. This indicates a major capital shift toward modular, behind-the-meter solutions. | Introl Blog |

| Oracle / Volta Grid | Oct 2025 | Oracle contracted for 2.3 GW of modular natural gas generation from Volta Grid to power its Texas AI data centers, representing a significant investment in a mature, fast-to-deploy BTM technology. | POWER Magazine |

| Meta / Enbridge | Jul 2025 | Enbridge announced a $900 million investment in a 600 MW solar project, with Meta as the offtaker to power its Texas data centers. This shows continued commitment to large-scale renewable PPAs. | Utility Dive |

| ECL Data Center | Sep 2024 | Announced plans for a 1 GW off-grid AI data center powered by hydrogen fuel cells near Houston, with a total estimated cost of $8 billion. This project signals long-term ambition for fully grid-independent, zero-carbon power. | pv magazine USA |

Texas vs. National Trend, ERCOT Data Center Power Deals Accelerate

The ERCOT demand crisis has concentrated and accelerated the formation of large-scale power partnerships in Texas, moving beyond the pilot-scale or nationally dispersed agreements seen before 2025. This has created a unique ecosystem where hyperscalers, utilities, and technology providers are forging alliances across a diverse portfolio of generation technologies, from natural gas to advanced nuclear, to solve a region-specific capacity shortfall.

- Before 2025, foundational partnerships were forming, such as AEP‘s agreement for up to 1 GW of Bloom Energy‘s fuel cells and Caterpillar‘s successful demonstration with Microsoft on hydrogen backup power. These validated the technology but were not yet a direct response to a grid-wide capacity crisis.

- The period from 2025 to 2026 is defined by large-scale, Texas-centric partnerships directly aimed at new generation. Key examples include Crusoe and Blue Energy partnering for a nuclear-powered AI data center, and Amazon exploring a campus adjacent to an existing nuclear plant in Somervell County.

- While hyperscalers continue to sign large renewable PPAs, such as Google‘s 1 GW solar agreement with Total Energies, the newest partnerships explicitly target firm, 24/7 power. The agreement between Sage Geosystems and San Miguel Electric Cooperative to build the first pressure geothermal system is another example of a Texas-based partnership designed to deliver dispatchable power to the ERCOT grid.

Table: Key Strategic Partnerships for Texas Data Center Power

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Energy / SDC | Jan 2026 | Partnership to deploy up to 450 MW of fuel cells for the AI data center market. This alliance targets the growing demand for modular and rapidly deployable on-site power solutions. | Data Center Dynamics |

| Crusoe / Blue Energy | Oct 2025 | Partnership to develop a nuclear-powered AI data center in the Port of Victoria, Texas. This represents a strategic move to secure long-term, carbon-free baseload power for high-density computing. | Crusoe |

| Sage Geosystems / San Miguel Electric Co-op | Sep 2025 | Successfully built the world’s first pressure geothermal system in South Texas. The partnership aims to deliver long-duration, dispatchable power, providing a new source of firm renewable energy for the ERCOT grid. | POWER Magazine |

| AEP / Bloom Energy | Nov 2024 | AEP established an agreement to secure up to 1 GW of Bloom Energy‘s solid oxide fuel cells to provide rapid power solutions for data centers and other large customers, bypassing grid backlogs. | AEP |

SWOT Analysis: Texas Firm Power for Data Centers

The urgent demand for data center power in Texas creates a massive market opportunity (Strength) but is constrained by grid limitations (Weakness), while the viability of new technologies like SMRs and geothermal (Opportunity) faces threats from long permitting times and fuel price volatility (Threat).

Modular Nuclear Offers Scalable Power Options

This infographic directly illustrates the ‘SMRs’ (Small Modular Reactors) opportunity mentioned in the SWOT analysis. It clarifies the scale of this technology, which is presented as a key opportunity to meet future demand.

(Source: TSCS – Substack)

Table: SWOT Analysis for Texas Data Center Power Solutions

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Pro-business regulatory environment; abundant natural gas and renewable resources. | Unprecedented demand growth (136 GW queue) creates a definitive, bankable market for new generation. State-level political support for nuclear and firm power emerges. | The abstract strength of a good business climate was validated by a concrete, multi-gigawatt wave of commercial projects from companies like Oracle, Last Energy, and Amazon. |

| Weaknesses | Grid instability concerns following Winter Storm Uri; growing reliance on intermittent wind and solar. | Grid interconnection queue wait times of 3-4 years become a primary business constraint. Forecasts show potential for a 79% wholesale price hike by 2027. | The theoretical risk of grid strain became a quantifiable bottleneck, forcing the market to internalize power generation costs and creating the business case for BTM solutions. |

| Opportunities | Early pilot projects for advanced geothermal (Sage Geosystems) and hydrogen fuel cells (Caterpillar/Microsoft). | Fuel cells secure $7.65 B in deals. SMRs move to site-specific plans (Last Energy, Fermi America). Geothermal shown to be 31-45% cheaper than grid power if co-located. | Emerging technologies shifted from R&D concepts to tangible solutions being pursued to solve a specific, urgent commercial need, accelerating their path to market. |

| Threats | High CAPEX and long permitting timelines for nuclear. Fuel cost volatility for natural gas. | The Nuclear Regulatory Commission (NRC) process remains a major schedule risk for SMRs. Reliance on natural gas (for turbines and fuel cells) creates exposure to price volatility and emissions concerns. | The primary threats—long lead times for nuclear and fuel costs for gas—became more acute as the urgency of demand intensified, creating a clear trade-off between deployment speed and long-term operating cost. |

2027-2030 Scenario, Fuel Cells Bridge Gap to Nuclear and Geothermal

In the immediate future, data center developers will overwhelmingly adopt natural gas and fuel cell solutions to meet urgent power needs, creating a “bridge” period while longer-lead time technologies like nuclear and geothermal secure financing and regulatory approval for commercial operation post-2030.

On-Site Gas Generation Requires Significant Redundancy

The section identifies natural gas as a key ‘bridge’ technology. This chart visualizes a critical trade-off for that solution, showing how redundancy requirements scale with generator size to ensure reliability for data centers.

(Source: SemiAnalysis)

- If This Happens: ERCOT’s high-growth demand materializes as projected, and grid interconnection queues remain a primary bottleneck for developers needing to bring new capacity online within 24 months.

- Watch This: The ratio of final investment decisions (FIDs) for BTM fuel cell and modular gas projects versus the rate at which SMR applications from companies like Last Energy advance through the NRC’s licensing process. A faster NRC timeline could accelerate nuclear adoption, while delays will cement the dominance of gas and fuel cells in the medium term.

- These Could Be Happening: By 2028, a significant fleet of fuel cell-powered data centers will be operational in Texas, validating the BTM model at scale. The first commercial data center contract for an advanced geothermal system, likely building on the success of the Fervo Energy or Sage Geosystems pilots, will be announced. By 2030, the first microreactors will be under construction, having secured long-term PPAs with data center consortiums seeking to de-risk their operations from natural gas price volatility and meet decarbonization goals.

The questions your competitors are already asking

This report covers one angle of the commercial pivot to behind-the-meter nuclear, fuel cell, and geothermal power for data centers facing Texas grid constraints. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the Texas BTM power market for data centers?

- What is the outlook for SMR deployment for Texas data centers by 2030, given ERCOT’s interconnection queue?

- How do SMRs compare to fuel cells and geothermal for powering a 1 GW AI data center campus behind-the-meter?

- Which hyperscalers and data center operators are actively pursuing behind-the-meter nuclear or fuel cell solutions to bypass ERCOT’s multi-year wait times?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.