Equinor CCUS Strategy, $5 B Renewables Cut, bp Teesside Partnership, and 10-12 GW Target Revision (2021 to 2025)

Equinor 2025 Strategy, A Pivot from Renewables Expansion to Integrated Value Creation

In 2025, Equinor executed a significant strategic pivot, moving away from rapid renewable capacity expansion to prioritize an integrated power model that combines renewables with flexible gas and energy storage. This shift is a direct response to lower-than-expected returns from pure-play renewables and the rising demand for reliable, dispatchable power from sectors like data centers.

- Prior to 2025, Equinor was on a trajectory to become a broad energy company, with a stated ambition to allocate 50% of its gross capital expenditures to renewables and low-carbon solutions by 2030.

- In February 2025, the company reversed course, scrapping the 50% green CAPEX target and cutting planned investment in renewables by 50% to $5 billion for the 2025-2027 period.

- The company simultaneously lowered its 2030 renewable capacity target from a range of 12-16 GW to 10-12 GW, signaling a clear de-emphasis on volume in favor of value.

- In April 2025, Equinor formed a new “Power” business area, merging its renewables portfolio with dispatchable gas-to-power plants and battery storage to mitigate intermittency and create more stable returns from volatile power markets.

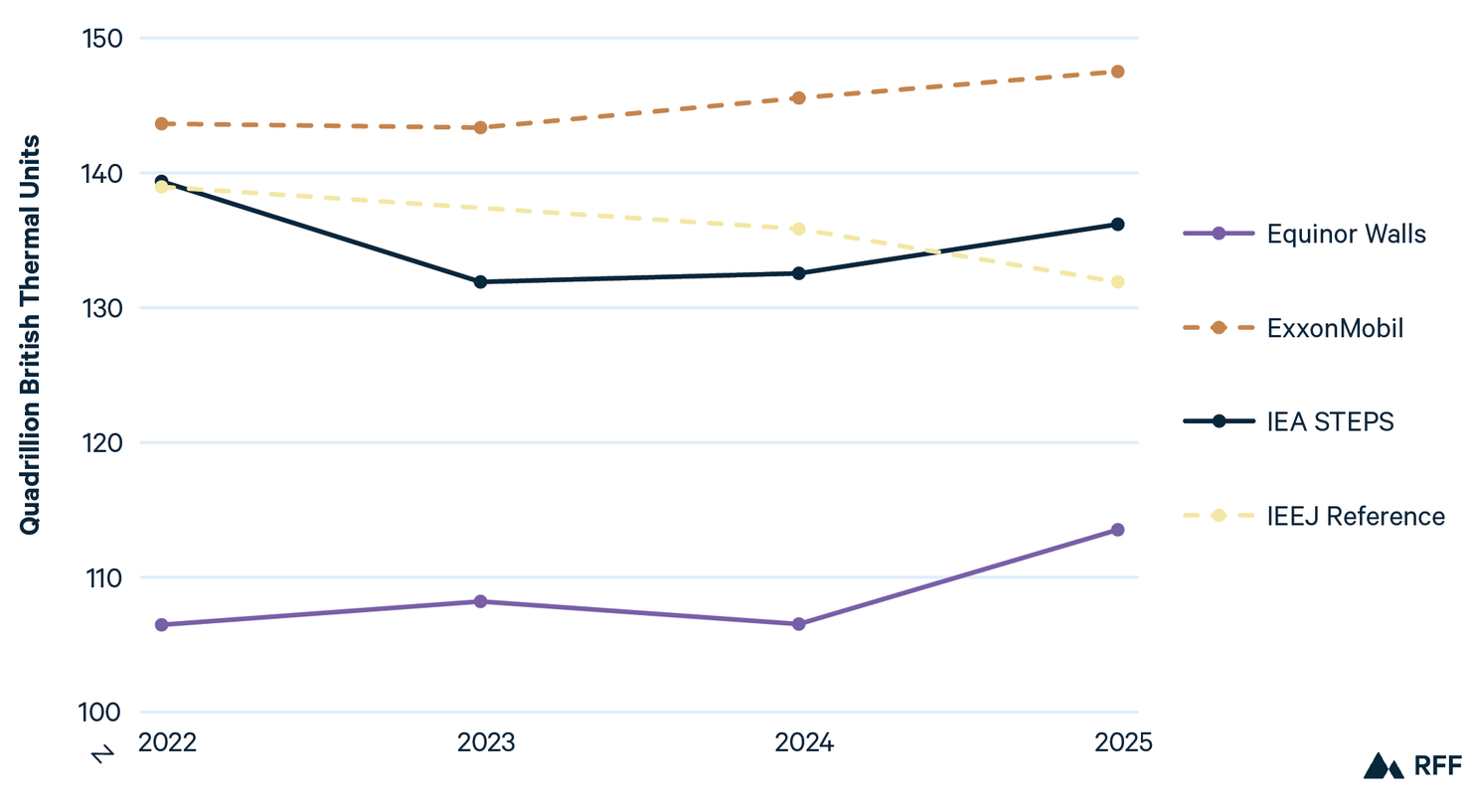

Energy Projections Show Equinor’s Divergence in 2025

The section discusses Equinor’s strategic pivot, and the chart explicitly visualizes ‘Equinor’s Divergence’ from previous energy projections, directly supporting the section’s theme.

(Source: RFF.org)

$5 B Investment Cut, Equinor Reallocates Capital from Renewables to Core Business

Equinor’s strategic realignment in 2025 was defined by a tangible reallocation of capital away from its renewables division and back toward its highly profitable core oil and gas operations and synergistic low-carbon projects. This financial maneuver is designed to de-risk its energy transition plan, improve shareholder returns, and use the cash flow from legacy assets to fund a more selective and integrated long-term strategy.

- The most significant move was the decision to slash investment in renewables and low-carbon solutions from a planned $10 billion to $5 billion over the next two years.

- This move was reinforced in July 2025 with the announcement of a $1.6 billion investment to boost natural gas production in Pennsylvania, a direct channeling of capital back to fossil fuels.

- The company also recommended discontinuing certain capital-intensive electrification projects on the Norwegian Continental Shelf in October 2025, further demonstrating its new focus on financial discipline and project viability.

- This recalibration contrasts sharply with the pre-2025 period, which saw aggressive investment in growing its renewables pipeline, including offshore wind projects that faced increasing costs and supply chain pressures.

Renewable Project Pipeline Strong Through 2029+

The section details Equinor’s capital reallocation away from renewables. The chart, showing a strong renewable project pipeline in the broader industry, provides essential context that highlights the counter-cyclical and strategic nature of Equinor’s decision.

(Source: Deloitte)

Table: Equinor Strategic Investment and Cancellation Analysis (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| NCS Electrification Projects | Oct 15, 2025 | Equinor recommended discontinuing certain offshore platform electrification projects, signaling a strategic reassessment of capital-intensive initiatives to prioritize higher-return ventures. | Equinor |

| Natural Gas Production Boost | Jul 15, 2025 | Announced a $1.6 billion investment to increase natural gas production in Pennsylvania, demonstrating a clear reallocation of capital back to profitable fossil fuel operations. | U.S. Senate |

| Strategic Investment Reduction | Feb 5, 2025 | Cut investment in renewables and low-carbon solutions by 50% to $5 billion for 2025-2027. This freed up capital and marked a pivot away from pure-play renewables growth. | Financial Times |

Equinor Partnerships with bp and Shell Signal a Focus on Industrial-Scale CCS

In line with its strategic shift, Equinor’s partnership activity in 2025 centered on large-scale infrastructure projects that support its integrated energy model, particularly in Carbon Capture and Storage (CCS). These collaborations leverage its core competencies in subsurface management and large project execution, creating low-carbon value chains rather than standalone renewable assets.

- The Net Zero Teesside Power project, a joint venture with bp, is a cornerstone of this strategy. It aims to build the UK’s first gas-fired power plant with integrated CCUS, providing dispatchable low-carbon electricity.

- The Northern Lights project, a joint venture with Shell and Total Energies, is foundational to Equinor’s ambitions. It is developing the world’s first open-source CO₂ transport and storage infrastructure, creating a service model for industrial decarbonization across Europe.

- These industrial-scale partnerships represent a shift from the pre-2025 focus on forming joint ventures for specific offshore wind farm developments. The new model focuses on creating enabling infrastructure for an entire low-carbon industrial cluster.

Hydrogen Generation Market to Exceed $285B by 2035

The section focuses on partnerships for industrial-scale CCS. The chart on the growing hydrogen market is relevant, as large-scale CCS is a key enabler for producing ‘blue’ hydrogen, a major area for partnerships between energy companies like Equinor, bp, and Shell.

(Source: Precedence Research)

Table: Equinor Key Strategic Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| bp / Net Zero Teesside Power | Oct 7, 2025 | A joint venture to develop the UK’s first gas-fired power plant with carbon capture. The project exemplifies Equinor’s integrated strategy of providing flexible, low-carbon power to support industrial clusters. | Legal 500 |

| Total Energies, Shell / Northern Lights | Jul 1, 2025 | An equal joint venture developing the world’s first open-access CO₂ transport and storage infrastructure. This project is critical for enabling Equinor’s blue hydrogen plans and a broader CCS service market. | Total Energies |

UK and Norway, Equinor Concentrates Low-Carbon Efforts in Core Geographic Markets

Equinor’s geographic strategy for distributed and low-carbon energy initiatives has become more focused, concentrating on regions where it can leverage existing infrastructure, subsurface expertise, and supportive regulatory frameworks. This represents a move away from a more scattered global renewables expansion seen before 2024 toward creating deep, integrated value chains in core markets.

- The UK has become a primary focus, with the Net Zero Teesside Power project and its role in the East Coast Cluster demonstrating a commitment to building a full low-carbon ecosystem, including power, hydrogen, and CCUS.

- Norway remains central, particularly for large-scale CCS infrastructure like the Northern Lights project and efforts to reduce emissions on the Norwegian Continental Shelf, though some electrification projects were deprioritized in 2025 based on cost-benefit analysis.

- While it maintains an international portfolio, including the Firefly floating wind project in South Korea, the strategic weight has shifted to developing integrated energy hubs in the North Sea region, where it has a dominant existing presence.

Oil & Gas Electrification Market Poised for Growth

The section describes Equinor’s focus on low-carbon efforts in its core markets of the UK and Norway. The chart on the growth of the oil & gas electrification market directly relates to a key decarbonization strategy being deployed in these specific geographic areas (e.g., electrifying North Sea platforms).

(Source: maximize market research)

Technology Maturity, Equinor Integrates Mature Gas with Deployable CCS Technology

The company’s 2025 strategy shows a clear preference for combining high-TRL technologies in novel ways rather than betting on early-stage, unproven concepts for its core business. By pairing its mature and highly efficient gas-to-power operations (TRL 9) with commercially deployable carbon capture technologies like amine scrubbing (TRL 8-9), Equinor is creating a new class of low-carbon, dispatchable assets.

- Before 2025, much of the transition narrative centered on scaling renewable technologies like offshore wind. While still part of the portfolio, the economic and integration challenges of these technologies prompted a strategic re-evaluation.

- The formation of the “Power” unit in 2025 is a structural acknowledgment that the value is not in any single technology but in the integration of systems: pairing intermittent renewables with flexible gas and battery storage.

- The significant focus on projects like Net Zero Teesside confirms that Equinor sees mature gas turbine technology combined with proven post-combustion capture as the most viable near-term path to providing large-scale, low-carbon, reliable power.

- This approach leverages Equinor’s deep expertise in gas markets and large-scale engineering, differentiating it from pure-play renewable developers and positioning it as a provider of system stability.

Equinor’s 2050 Scenarios Show Role of Gas

The section discusses Equinor’s strategy of integrating mature gas with CCS. The chart, which shows Equinor’s own scenarios for the continuing role of gas, provides a direct rationale for this technology integration strategy.

(Source: RFF.org)

SWOT Analysis, Equinor’s Strategic Repositioning and Market Exposure

Equinor’s pivot in 2025 is a calculated de-risking of its energy transition, but it introduces a new set of strategic trade-offs. The move strengthens its financial position in the short term and leverages core competencies, yet it also increases its exposure to commodity cycles and potential criticism from ESG-focused stakeholders.

- The key strength validated in 2025 is its ability to generate significant cash flow from its oil and gas portfolio ($6.53 billion adjusted operating income in Q 2 2025) to fund a more deliberate transition.

- A primary weakness is the potential for reputational damage and investor backlash from being perceived as slowing its green ambitions, which could affect its cost of capital over the long term.

- The main opportunity is capturing the high-value market for reliable, low-carbon power demanded by data centers and heavy industry, a market that pure-play renewables struggle to serve alone.

- A significant threat remains policy and regulatory risk. A rapid tightening of emissions policies or a failure of CCS technology to deliver on cost and scale could undermine its integrated gas-with-CCS strategy.

Energy Giants Model Divergent Transition Paths

The section provides a SWOT analysis of Equinor’s strategic repositioning. The chart comparing the divergent transition paths of major energy giants provides the perfect competitive context for such an analysis, illustrating Equinor’s position relative to its peers.

(Source: RFF.org)

Table: SWOT Analysis for Equinor 2025 Strategic Pivot

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Perceived as a leader in energy transition among oil majors; strong renewables project pipeline. | Profitable oil & gas core to fund transition; expertise in large, complex offshore projects and gas markets. | The company validated that its core O&G business is the financial engine, pivoting to leverage this strength more explicitly for a value-focused transition. |

| Weaknesses | Exposure to high CAPEX and low returns in competitive offshore wind auctions. | Reputational risk from cutting green targets; increased reliance on volatile fossil fuel prices. | The 2025 pivot exposed the financial weakness of a pure renewables push and accepted reputational risk in exchange for financial stability. |

| Opportunities | Lead the rapid build-out of global renewable capacity. | Provide high-value, reliable, low-carbon power for data centers; lead the emerging CCS service market. | The market opportunity shifted from simply adding green megawatts to providing complex, reliable energy solutions, which Equinor is now structured to target. |

| Threats | Supply chain bottlenecks and cost inflation for renewable projects. | Policy or regulatory changes undermining CCS viability; long-term competition from advancing battery storage or nuclear. | The primary threat shifted from execution risk in renewables to systemic risk in its new integrated model, particularly its dependence on the success of CCS. |

Equinor’s Future, Performance of the New “Power” Unit Is the Key Signal to Watch

The success of Equinor’s 2025 strategic pivot hinges entirely on the execution and profitability of its newly created “Power” business area. The single most critical expectation for the years ahead is that this integrated unit must demonstrate it can deliver higher, more stable returns than a pure-play renewables strategy could, justifying the controversial decision to scale back green ambitions.

- If this strategy is successful, watch for Final Investment Decisions (FIDs) on key enabling projects like Net Zero Teesside Power and the signing of long-term, high-value power purchase agreements with industrial users and data centers.

- A key signal of traction would be future capital market updates showing the “Power” unit delivering superior margins and attracting project financing on favorable terms, validating the integrated model.

- Conversely, a signal of trouble would be delays or cancellations of these large-scale CCS projects, a failure to secure offtake agreements, or financial reports showing the unit is failing to outperform renewables-focused peers, which could force another strategic re-evaluation.

Virtual Power Plant Market to Exceed $45B

The section identifies the new ‘Power’ unit’s performance as a key future indicator. The chart on the high-growth virtual power plant (VPP) market illustrates a key, high-value opportunity that such a ‘Power’ unit would target, making it a relevant measure of future success.

(Source: Precedence Research)

The questions your competitors are already asking

This report covers one angle of Equinor’s evolving energy transition strategy. The questions that matter most depend on your work.

- Which integrated energy companies are gaining ground as pure-play renewables face headwinds?

- Is Equinor a good investment after its pivot away from the 50% green CAPEX target?

- Equinor investments and funding. Is the revised 10-12 GW renewable capacity target on track after the $5B CAPEX cut?

- What is actually happening with Equinor’s ‘Power’ business area since the April 2025 reorganization?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.