NVIDIA 800 V DC Data Center Power, 31 Partner Ecosystem with Vertiv, 1 MW Racks, and 39 GW Capacity Forecast (2025 to 2026)

Grid Availability: The Primary Constraint for 800 V DC Data Center Deployments

The rapid adoption of 800 V DC power architecture within data centers is solving internal power density and efficiency challenges, but it is exposing a more significant external bottleneck: the availability of grid-scale power and transmission equipment. While the internal power architecture advanced significantly from 2025 to today, driven by a mature electric vehicle component supply chain, the success of these new AI factories is now constrained not by internal technology but by the five-year backlogs for high-voltage transformers and the inability of regional grids to supply multi-gigawatt power.

- Between 2021 and 2024, the discussion around data center power was largely academic, focusing on the potential of higher voltages and the limitations of 48 V DC systems. The primary challenges were seen as component development and creating new internal power designs.

- Starting in 2025, the conversation shifted to deployment. NVIDIA released its 800 V DC architecture and announced collaborations with a 31-company ecosystem, including major players like Vertiv and Delta Electronics. This validated the technical viability and commercial readiness of the internal power systems needed for racks exceeding 100 k W.

- However, by 2026, the central challenge became external. Reports confirmed that up to half of planned U.S. data center builds were delayed or canceled, not due to rack-level technology, but because of severe grid constraints and multi-year lead times for critical electrical components.

- The 800 V DC architecture successfully reduces internal copper use by up to 45% and improves efficiency by 4% to 5%, but these gains are nullified if the data center cannot secure a grid connection to power its operations in the first place.

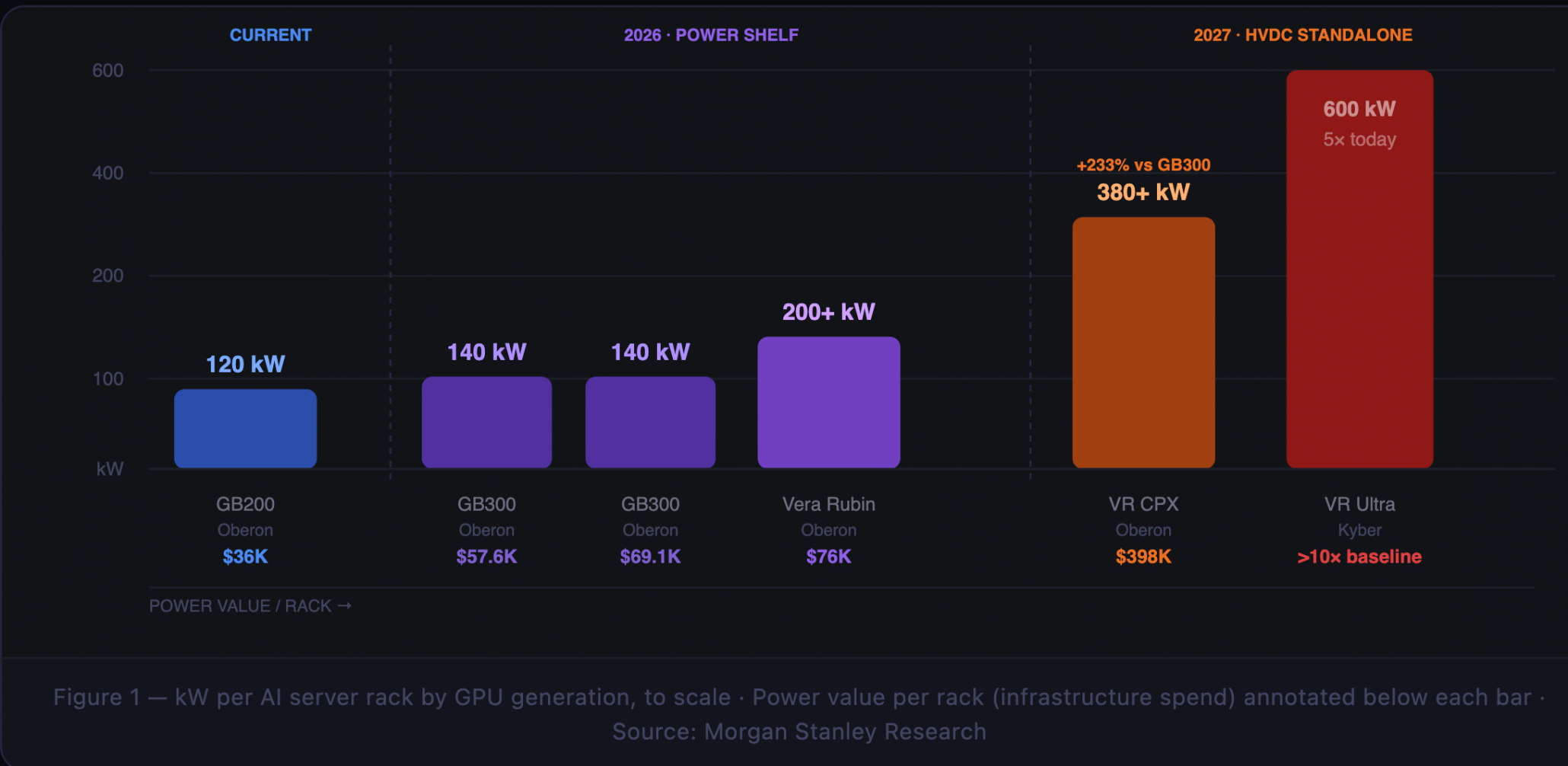

AI Rack Power Needs to Jump 5x by 2027

This chart visually establishes the core reason for grid constraints by showing the exponential growth in power demand from AI racks. This provides essential context for the section’s argument that grid availability is the primary bottleneck.

(Source: Data Gravity)

Market Forecasts for Data Center Power Systems Show Significant Growth

Financial projections for the data center power market confirm a rapid expansion, with the niche but critical segment for AI-specific high-voltage DC systems expected to grow significantly. The wide variation in forecasts for the overall market reflects differing assumptions about the pace of AI adoption and the resolution of grid-level constraints. However, all analyses point toward a multi-billion dollar opportunity driven by the urgent need to power next-generation compute.

- Market projections made between 2025 and 2026 show the global data center power system market growing from a baseline of approximately $21 billion to $35 billion in 2025 to a forecasted $50 billion to $70 billion by 2034.

- The specific market for AI Data Center HVDC Power Supply Systems is projected to triple, growing from $1.53 billion in 2025 to $4.59 billion by 2035, indicating that this high-voltage architecture is expected to capture a growing share of new builds.

- A contract from 2024 by server company 2 CRSi with a U.S. data center operator, valued at $610 million, highlighted the commercial demand for solutions promising significant energy and cost savings, a trend that the 800 V DC architecture directly addresses.

Data Center Power Device Market Shows Strong Growth

The chart and its corresponding section are a direct match. The chart visually confirms the ‘significant growth’ mentioned in the section’s heading, providing the key data forecast that the text is built around.

(Source: Yole Group)

Table: Data Center Power Market Size Forecasts

| Forecast Provider | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Marketsand Markets | 2025–2030 | Forecasts the global data center power market to grow from $35.14 billion in 2025 to $50.51 billion by 2030, at a CAGR of 7.5%. This reflects steady growth in power infrastructure spending. | Marketsand Markets |

| Intel Market Research | 2025–2034 | Projects the market will expand from $21.52 billion in 2025 to $56.50 billion by 2034, at a higher CAGR of 16.2%, suggesting an acceleration driven by AI demands. | Intel Market Research |

| Precedence Research | 2025–2034 | Offers a bullish forecast, predicting the market will hit $70.21 billion by 2034 from a 2025 baseline of $22.93 billion. This points to sustained, high-growth investment. | Precedence Research |

| Precedence Research (AI HVDC segment) | 2025–2035 | Estimates the specific AI Data Center HVDC Power Supply System market will grow from $1.53 billion in 2025 to $4.59 billion by 2035. This shows the targeted growth within the high-voltage DC niche. | Precedence Research |

Power Electronics Market to Exceed $65B by 2036

This chart provides a macro-level market forecast that aligns with the purpose of a section dedicated to market size forecasts. It offers a broader, long-term perspective on the power electronics industry, which is the parent market for the data center power systems being discussed.

(Source: LinkedIn)

NVIDIA’s 31-Partner Ecosystem Accelerates 800 V DC Adoption

The transition to 800 V DC architecture is being organized and accelerated by a collaborative ecosystem led by NVIDIA, which is standardizing designs to ensure interoperability and speed market entry. Before 2025, high-voltage DC was a fragmented concept with bespoke solutions. Today, a clear, multi-vendor ecosystem has emerged, mirroring the standardization efforts that enabled the EV charging market to scale.

- In May 2025, NVIDIA formalized the 800 V DC movement by publishing its architectural white paper and announcing its collaboration with key power electronics companies, effectively creating a blueprint for the industry.

- Legacy power management firms like Delta Electronics and Vertiv quickly aligned, announcing their development of complete 800 V DC ecosystems in October 2025 and showcasing hardware like 660 k W power racks at industry events in March 2026.

- Semiconductor giants also joined the initiative. In March 2026, Texas Instruments announced a partnership with NVIDIA to develop a complete 800 V power solution, while Renesas and Navitas highlighted their Ga N and Si C components optimized for this architecture.

- This coordinated effort, spanning from system architects to component suppliers, reduces the adoption risk for data center operators and ensures a supply of standardized, interchangeable parts.

Diagram Outlines Next-Gen AI Power Architecture

The diagram provides a crucial visual aid for a section discussing the partner ecosystem. It illustrates the very 800 V DC architecture that these partners are adopting, giving readers a concrete understanding of the technology being implemented.

(Source: Yole Group)

Table: Key 800 V DC Data Center Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| NVIDIA and Ecosystem Partners | May 2025 | NVIDIA announced collaborations with over 30 partners to build out the 800 V DC ecosystem for its AI platforms. This serves to standardize the architecture and de-risk adoption for customers. | NVIDIA Technical Blog |

| Ideal Power and Industry Partner | May 2026 | Signed a letter of intent to develop a B-TRAN-enabled prototype for NVIDIA’s Rubin Ultra platform, with evaluation planned by a U.S. hyperscaler. This indicates specialized technology players are entering the ecosystem. | Proactive Investors |

| Texas Instruments and NVIDIA | March 2026 | TI unveiled its partnership with NVIDIA to develop a complete 800 V DC power architecture, providing reference designs and components to accelerate development for other hardware manufacturers. | Yahoo Finance |

| Vertiv and NVIDIA | October 2025 | Announced a close collaboration to advance 800 V DC platform designs, from converters to lifecycle services. This signals that full end-to-end infrastructure support is becoming available from established vendors. | Vertiv |

US Grid Constraints Impede Data Center Growth, Despite 800 V DC Efficiency

While the 800 V DC architecture optimizes power usage within the data center, its large-scale deployment is heavily concentrated in the United States, a region now facing critical grid infrastructure shortages. The power efficiency gains at the rack level do not solve the macro problem of securing sufficient electricity and the physical equipment needed to deliver it, making geography a primary factor in project viability.

- Between 2021 and 2024, data center location strategy was primarily driven by factors like land cost, fiber connectivity, and local tax incentives. Grid power was often assumed to be available.

- From 2025 onward, the primary site selection criterion has become the availability of multi-hundred-megawatt power connections. Projections show U.S. data centers could consume 9% of national electricity by 2030, up from 4% in 2023.

- Reports in 2026 revealed that approximately half of all planned data center construction in the U.S. has been delayed or halted specifically due to the inability to secure power from utilities and the extreme lead times for essential grid components like high-voltage transformers.

- Europe faces similar challenges, with reports highlighting a potential “1 GW power crisis” for data centers. The problem is global, but the highest concentration of new AI-driven demand is in the U.S., making it the most visible example of this infrastructure gap.

Tech Capex Rivals Major Historical Infrastructure Projects

The chart effectively contextualizes the scale of the issue discussed in the section. By showing that tech capex is on par with major historical infrastructure projects, it underscores the massive economic impact of the grid constraints that are impeding data center growth.

(Source: Not Boring by Packy McCormick)

SWOT Analysis of the 800 V DC Data Center Architecture

The strategic analysis of 800 V DC adoption reveals a technology with mature, compelling strengths derived from the EV industry, but one that is directly exposed to external, systemic threats from an unprepared electrical grid. The shift from theoretical benefits before 2024 to real-world deployment challenges after 2025 has clarified the true opportunities and risks.

AI Server Rack Component Costs Reach $15k

This chart fits well within a SWOT analysis. The high cost of components is a significant factor, representing a potential ‘Weakness’ in the business case or a ‘Threat’ to rapid adoption, making it a relevant data point for the analysis.

(Source: Tech Investments)

Table: SWOT Analysis for 800 V DC Power Distribution in Data Centers

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical benefits of higher voltage (reduced I²R losses, less copper) were well understood from physics and EV applications. Wide-bandgap semiconductors like Si C and Ga N were seen as enabling but still nascent for this market. | Quantified benefits are now proven in partner reference designs, with 4% efficiency gains, 30-40% copper reduction, and total cost savings of 30%. The EV supply chain for Si C/Ga N components is mature and cost-effective. | The theoretical efficiency and cost benefits have been validated through commercial product announcements and ecosystem partnerships. The strength of leveraging the EV supply chain was confirmed. |

| Weaknesses | Concerns centered on the lack of standards, potential safety risks of high-voltage DC in a data center environment, and a workforce unfamiliar with the technology. Industry inertia favored sticking with known AC and 48 V DC architectures. | While standards are emerging via NVIDIA’s ecosystem, the core weakness remains industry inertia and the need for workforce re-skilling. The adoption timeline is debated, with some analysts predicting only 10% of new AI nodes will require 800 V by 2030. | The weakness shifted from a technology gap to an adoption and skills gap. NVIDIA’s de facto standardization is mitigating one weakness, but workforce training remains a persistent challenge. |

| Opportunities | The opportunity was seen as enabling the next generation of high-power computing and improving Power Usage Effectiveness (PUE) for sustainability goals. The market was seen as a future possibility. | The opportunity is now immediate and concrete: enabling single-rack power densities exceeding 100 k W, with a path to 1 MW. This is a requirement for next-gen AI platforms like NVIDIA’s Rubin Ultra. The market for AI HVDC power is projected to grow to $4.59 billion. | The opportunity was validated from a future “nice-to-have” for efficiency to a “must-have” enabler for competitive AI infrastructure. The direct link between 800 V DC and future GPU roadmaps is now explicit. |

| Threats | Threats were perceived as competitive power architectures or a slower-than-expected rise in rack power densities that would make the transition unnecessary. | The primary threat has become external and severe: grid connection unavailability, 5-year lead times for high-voltage transformers, and project cancellations due to power shortages. The success of the technology is now hostage to macro-level infrastructure capacity. | The threat shifted from internal technology competition to an external, physical supply chain bottleneck in the electrical grid itself. This threat was validated by numerous reports of stalled data center projects in 2026. |

If Grid Constraints Persist, Watch for On-Site Power Generation

The most critical variable for the deployment of 800 V DC data centers in the year ahead is the availability of grid power. If utilities cannot accelerate connection times and if transformer manufacturing does not scale, data center operators will be forced to pursue on-site power generation, fundamentally altering the economic and logistical model of new builds.

- If this happens: Watch for a surge in announcements from data center operators about partnerships with natural gas providers, small modular reactor (SMR) developers, and large-scale solar and battery storage integrators.

- Watch this: The number of data center projects that include a dedicated microgrid or on-site power plant in their initial planning application, rather than as a backup system. This will be a leading indicator of a permanent shift away from total reliance on the grid.

- These could be happening: Hyperscalers may begin acquiring or directly investing in power generation assets to secure their energy supply. We may also see data center developments cluster in regions not for fiber connectivity, but for proximity to large-scale power sources, such as nuclear plants or major renewable energy hubs.

The questions your competitors are already asking

This report covers one angle of the shift in bottlenecks for 800V DC data centers, from internal rack architecture to external grid availability. The questions that matter most depend on your work.

- What is the outlook for the 39 GW AI data center capacity forecast given the multi-year lead times for high-voltage transformers?

- Which data center operators are successfully deploying 800V DC at scale, and which plans are being delayed or canceled due to grid constraints?

- What is actually happening with NVIDIA’s 31-company ecosystem since the 2025 announcement? Is it still progressing despite the grid bottleneck?

- Which companies are gaining ground in the 800V DC power market—component suppliers like Vertiv and Delta, or the grid-level equipment manufacturers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.