Koloma Geological Hydrogen Funding, $245.7 M Raised, Mitsubishi Partnership, and 16 U.S. DOE Projects (2021 to 2026)

Geological Hydrogen Commercial Projects, Koloma and Gold Hydrogen Lead Drilling Efforts

The geologic hydrogen sector has transitioned from theoretical modeling and small-scale proofs-of-concept to active, venture-backed commercial drilling aimed at proving scalable resource extraction. This shift marks a critical move from assessing whether the resource exists to determining if it can be produced economically. The success or failure of these initial commercial wells will dictate the industry’s near-term growth trajectory and its ability to attract large-scale capital.

- Between 2021 and 2024, the industry’s primary commercial datapoint was the small-scale Hydroma project in Mali, which served as a proof-of-concept by using naturally produced hydrogen to power a local village. During this period, activity was largely confined to academic studies and early-stage exploration by a few private pioneers.

- A significant acceleration occurred from 2025 to today, with well-funded startups launching ambitious drilling campaigns. Koloma is now actively drilling in Idaho, and Australia’s Gold Hydrogen has reported high-purity results from its Ramsay 1 and 2 wells, shifting the market’s focus from discovery to commercial viability.

- The emergence of “stimulated” hydrogen concepts, led by companies like Vema Hydrogen and Geo Kiln, introduces a strategic hedge against pure exploration risk. This approach aims to create hydrogen in-situ by injecting fluids into favorable rock formations, potentially offering a more predictable production method.

- Government support has become a key enabler. The U.S. Department of Energy (DOE) allocated $20 million across 16 research projects to advance exploration and production, while Michigan’s Executive Directive No. 2026-1 signals state-level commitment to building a commercial framework for the industry.

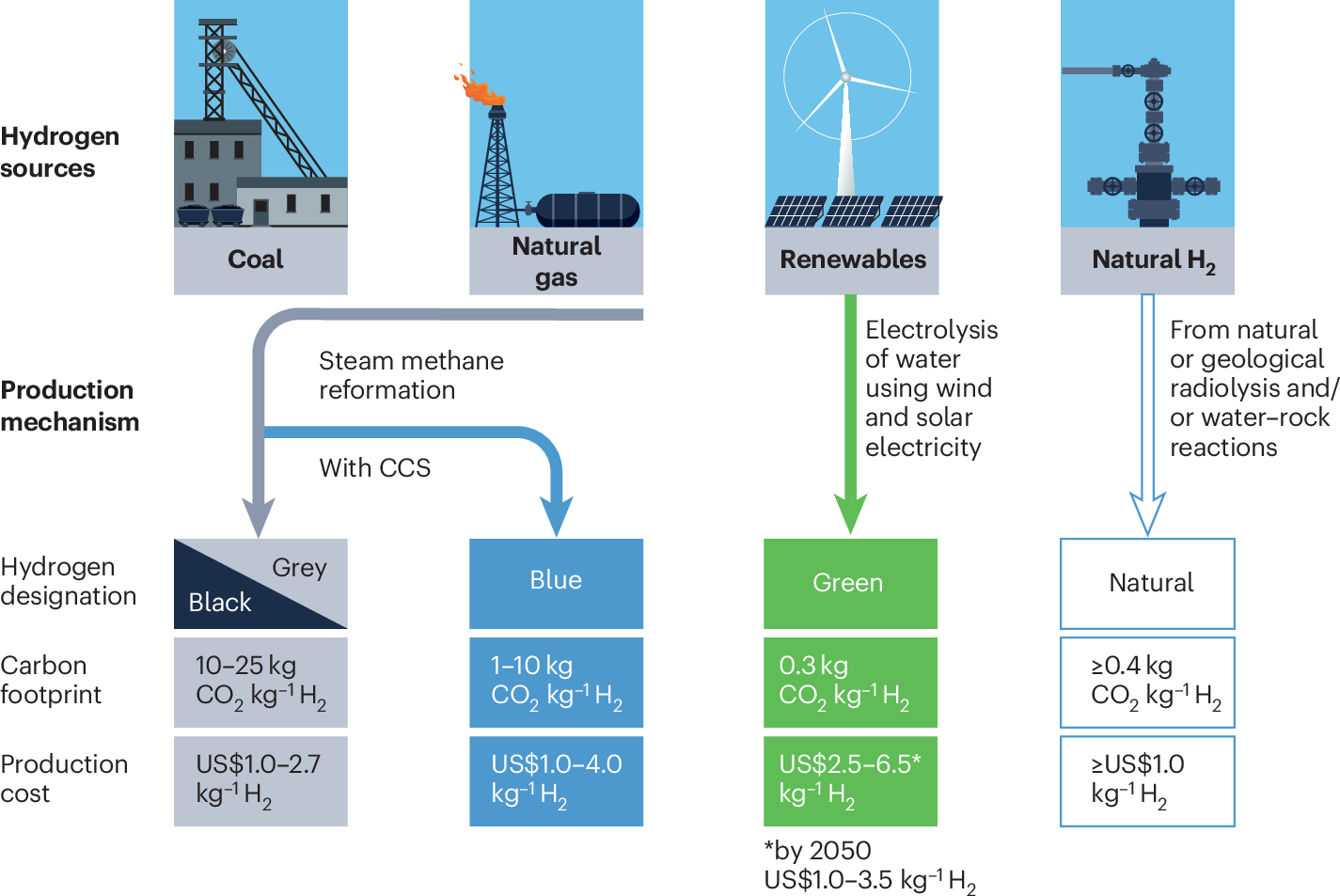

Natural Hydrogen Competes on Cost

This section discusses the shift to proving geologic hydrogen can be produced economically. This chart directly supports that theme by comparing the production cost of natural hydrogen to established methods.

(Source: Nature)

$340 M in Funding, Koloma Dominates Geologic Hydrogen Investment Activity

Venture and strategic corporate investment in geologic hydrogen has surged since 2023, with a significant concentration of capital flowing to a few leading startups. This funding is critical for de-risking the sector through aggressive, capital-intensive exploration and drilling programs. The pattern of investment shows a market consolidating behind perceived front-runners while still supporting novel technological approaches.

- Between 2023 and 2024, Koloma secured its position as the market leader by raising a total of $245.7 million, including a foundational $91 million round led by Breakthrough Energy Ventures.

- From 2025 to today, Koloma’s funding advantage widened, with its total capital raised reaching an estimated $340 million. This represents approximately 85% of the $400 million raised by the sector to date, giving it a substantial operational lead.

- Strategic industrial players entered the market in July 2025 with a A$14.5 million ($9.54 million) investment in Gold Hydrogen by a consortium including Toyota and Mitsubishi Gas Chemical. This signals a clear industrial push to secure future clean hydrogen supply chains.

- Seed-stage funding remains active for new technologies. Vema Hydrogen raised $13 million in a February 2025 seed round to develop pilot wells for its “rocks-to-hydrogen” stimulated production method, indicating investor appetite for alternatives to pure exploration.

Table: Geologic Hydrogen Strategic Investments

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Koloma | 2026-02-26 | Total funding reached $340 M, solidifying its position as the most well-capitalized company in the sector with an estimated 85% of total funds raised. | Wood Mackenzie |

| Gold Hydrogen | 2025-07-11 | Raised A$14.5 M ($9.54 M) from Toyota, Mitsubishi Gas Chemical, and Eneos. The investment gives the Japanese firms a combined 22% share to secure future hydrogen supply. | C&EN |

| Vema Hydrogen | 2025-02-20 | Secured a $13 M seed funding round led by Propeller Ventures and Extantia to develop pilot wells for its stimulated geologic hydrogen technology. | Hydrogen Insight |

| Koloma | 2024-10-15 | Received a $50 M investment from Mitsubishi Heavy Industries and Osaka Gas to advance exploration and accelerate commercialization efforts. | Mitsubishi Heavy Industries |

| Koloma | 2023-07-20 | Raised a $91 M funding round led by Breakthrough Energy Ventures, establishing it as a major player and validating interest from high-profile climate investors. | Carbon Credits |

Koloma 3 Major Partnerships, Hy Terra and Geo Kiln Pioneer New Technology (2025 to 2026)

Strategic partnerships formed since 2025 are critical for accelerating exploration and de-risking technology. These collaborations combine specialized exploration technology, large-scale industrial engineering expertise, and innovative production concepts, creating integrated approaches to commercialization that a single startup could not achieve alone.

- Koloma has assembled a key technology stack through recent partnerships. Its February 2025 collaboration with Fleet Space leverages satellite-based exploration, while a separate agreement with Xcalibur Smart Mapping aims to accelerate resource discovery.

- The company secured a major industrial endorsement via its October 2024 partnership with Mitsubishi Heavy Industries and Osaka Gas, which provides both capital and deep engineering expertise essential for scaling from exploration to production.

- The stimulated hydrogen segment advanced significantly with the November 2025 binding collaboration between Hy Terra and Geo Kiln. This partnership will pioneer thermally engineered geologic hydrogen tests at the Nemaha Project in Kansas, aiming to prove a new commercialization pathway.

Table: Geologic Hydrogen Strategic Partnerships

| Lead Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Hy Terra & Geo Kiln | 2025-11-26 | Signed a binding collaboration to pioneer thermally engineered geologic hydrogen tests. The goal is to accelerate commercialization pathways for stimulated hydrogen production. | Nat H 2 Investing |

| Koloma & Fleet Space | 2025-02-25 | Partnered to enhance data-driven natural hydrogen exploration. Koloma will use Fleet Space’s satellite-based subsurface mapping technology to identify promising drilling locations. | Fleet Space |

| Koloma & Mitsubishi Heavy Industries | 2024-10-15 | Formed a partnership alongside a $50 M investment to advance geologic hydrogen exploration and commercialization, combining Koloma’s exploration work with MHI’s industrial scale. | Koloma |

US and Australia Emerge as Key Hubs, Koloma and Gold Hydrogen Drive Exploration

Geologic hydrogen exploration is geographically concentrated in regions with favorable geology and supportive policy. The United States and Australia have emerged as the primary commercial hotspots, driven by targeted government resource mapping, new state-level policy initiatives, and promising early drilling results that have attracted significant international investment.

- From 2021 to 2024, exploration activity was sparse and globally scattered. Key locations included Mali (Hydroma’s operational well), Australia (Gold Hydrogen’s initial work on the Yorke Peninsula), and early-stage drilling in the U.S. Mid-Continent Rift system by Natural Hydrogen Energy LLC.

- The release of the U.S. Geological Survey’s (USGS) prospectivity map in January 2025 was a major catalyst for the industry. It provided a data-driven framework that focused U.S. exploration efforts on high-potential zones in the Great Lakes, Rocky Mountains, and specific areas on the East Coast.

- Since 2025, the U.S. has experienced a surge in targeted activity. Koloma is actively pioneering drilling in Idaho, Hy Terra is pursuing its project in Kansas, and the state of Michigan issued Executive Directive No. 2026-1 to formally prepare its regulatory environment for a geologic hydrogen industry.

- Australia remains a key global player, with Gold Hydrogen’s Ramsay wells confirming high purity levels. This success was instrumental in attracting a $9.54 million investment from Japanese industrial giants Toyota and Mitsubishi in 2025, validating the region’s commercial potential.

Technology Validation, Koloma and Hy Terra Drilling Moves from Theory to Practice

Geologic hydrogen technology is rapidly advancing from theoretical science and resource mapping to the critical pilot and validation phase. The primary challenge has shifted from proving the science of natural hydrogen formation to engineering reliable extraction methods and demonstrating commercially viable flow rates from drilled wells, a hurdle the industry must clear to scale.

- The 2021-2024 period was defined by establishing the scientific basis, primarily through serpentinization and radiolysis theories, and repurposing exploration tools from the oil and gas sector. The Mali well served as the only, albeit small-scale, real-world production example.

- Since early 2025, the industry has entered a new phase of active drilling and technology validation. The success of exploration now hinges on proving that hydrogen accumulates in large, high-pressure, extractable reservoirs, a critical unknown that current drilling by Koloma seeks to answer.

- Promising discoveries provided crucial validation and spurred investment. In late 2023, Gold Hydrogen reported purity up to 86% from its Australian well, while a deep drill hole in Finland detected concentrations up to 46% in 2024.

- A recent technological shift is the focus on stimulated production. This approach, pursued by Geo Kiln in partnership with Hy Terra, represents a parallel path to commercialization that could bypass the high risks of pure exploration by engineering hydrogen resources on demand.

SWOT Analysis, Koloma Cost Disruption Potential vs. Exploration Uncertainty

The strategic outlook for geological hydrogen is defined by the immense opportunity of its projected sub-$1/kg production cost, which is counterbalanced by significant weaknesses in geological understanding and the external threat of competing clean energy pathways. Recent drilling and investment have validated the potential but have not yet resolved the core exploration risks.

Geologic Hydrogen’s Key Environmental Advantages

This section introduces a SWOT analysis where a key strength is the low environmental impact. This chart visualizes that strength by showing geologic hydrogen’s low carbon intensity and water usage.

(Source: CarbonCredits.com)

Table: SWOT Analysis for Geologic Hydrogen Commercialization

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Theoretical low-cost potential (sub-$1.50/kg) and low carbon footprint based on scientific models. Mali well provided proof of concept for high-purity natural hydrogen. | Projected cost refined to $0.50-$1.00/kg. Low carbon intensity and water usage claims are substantiated by early analyses from companies like Koloma. | The core economic argument has been validated and strengthened by consistent third-party and corporate modeling, attracting major industrial investors like Toyota and Mitsubishi. |

| Weaknesses | Extreme exploration uncertainty. Lack of established geological models for hydrogen systems, comparable to the mature models for oil and gas. Very limited drilling data. | Exploration risk remains the primary weakness, but is now being actively tested by well-funded drilling programs from Koloma (Idaho) and Gold Hydrogen (Australia). | The weakness is being directly addressed. The industry has moved from acknowledging the risk to spending hundreds of millions of dollars to resolve it through the drill bit. |

| Opportunities | Potential to disrupt manufactured hydrogen markets (green and blue) and provide a new primary clean energy source for industry and power generation. | Opportunities have expanded to specific high-growth sectors. The potential for low-cost, continuous power is being targeted for the AI data center boom and mining operations. | The addressable market has become more defined, moving beyond general decarbonization to specific, high-value industrial applications where geologic hydrogen’s profile is advantageous. |

| Threats | Technological stagnation if early exploration wells were unsuccessful. Competition from rapidly scaling green and blue hydrogen production. | The main threat is that initial commercial wells fail to establish commercial flow rates, which could freeze venture capital funding. The IRA Hydrogen Tax Credit makes green hydrogen more competitive in the near term. | The threat has become more immediate. The industry’s credibility now rests on the outcomes of a few key drilling projects over the next 1-3 years. |

Geological Hydrogen Scenario, Flow Rate Data from Koloma is the Key Signal for 2026

The commercial viability of the entire geological hydrogen sector will be determined in the next 3 to 5 years by the drilling results and flow-rate data from a handful of leading companies. Success would trigger a significant reallocation of capital across the clean energy sector, while failure would relegate the resource to a niche curiosity.

Extraction Costs are a Key Hurdle

This section discusses future scenarios where commercial viability depends on overcoming costs. This chart details a potential high-cost reality, illustrating the economic hurdle companies must clear to succeed.

(Source: ScienceDirect.com)

- If companies like Koloma and Gold Hydrogen can demonstrate sustained, commercially viable flow rates from their current pilot wells, watch for a rapid influx of capital from major energy corporations and a potential pivot away from more expensive green and blue hydrogen projects for certain applications like heavy transportation.

- The key signal to monitor is not just the discovery of hydrogen, which is now well-established, but the publication of verifiable data on flow rates, purity, and projected reservoir size. This data is the primary hurdle between exploration and bankability.

- A parallel indicator to watch is the progress of stimulated hydrogen pilots from firms like Hy Terra and Geo Kiln. Success in these engineered projects would provide a crucial fallback, mitigating the risk of pure exploration and offering a more predictable path to production.

- The establishment of clear regulatory frameworks, as initiated by Michigan’s 2026 directive, is a leading indicator of government confidence. The speed at which other jurisdictions follow suit will be essential for scaling the industry beyond initial pilots.

The questions your competitors are already asking

This report covers one angle of geological hydrogen’s transition from research to commercial-scale drilling. The questions that matter most depend on your work.

- Which companies are gaining ground in the race to commercialize geological hydrogen?

- What is the outlook for geological hydrogen to become a cost-disruptive energy source by 2030?

- How does the pure exploration approach of Koloma and Gold Hydrogen compare to ‘stimulated’ hydrogen for achieving commercial scalability?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.