Top 10 LNG Projects Facing Headwinds: BP Sells Stake in Browse, $18.4 B Rio Grande Stalls (2024-2026)

The global Liquefied Natural Gas (LNG) market is undergoing a seismic shift from supply scarcity to a potential structural oversupply, creating significant challenges for projects yet to reach a Final Investment Decision (FID). A massive wave of new liquefaction capacity, primarily from the United States and Qatar, is set to flood the market starting in 2025-2026, threatening a “year of the glut.” This impending oversupply, coupled with the U.S. administration’s temporary pause on new export approvals in 2024, has created a perfect storm of market and regulatory headwinds. Projects like Next Decade‘s $18.4 billion Rio Grande LNG are now navigating not just financial hurdles but also intense community and environmental opposition. The dominant theme for 2025 and beyond is the rapid transition to a buyer’s market, where only the most competitive and de-risked projects will survive, placing unsanctioned developments at high risk of delay or cancellation.

1. Rio Grande LNG

Company: Next Decade

Installation Capacity: 27 MTPA

Applications: LNG Export

Source: Fact sheet: $18.4 bn Rio Grande LNG project and headwinds

2. Alaska LNG

Company: Alaska Gasline Development Corporation (AGDC)

Installation Capacity: 20 MTPA

Applications: LNG Export

Source: US gas industry – LNG Export – Seala AI

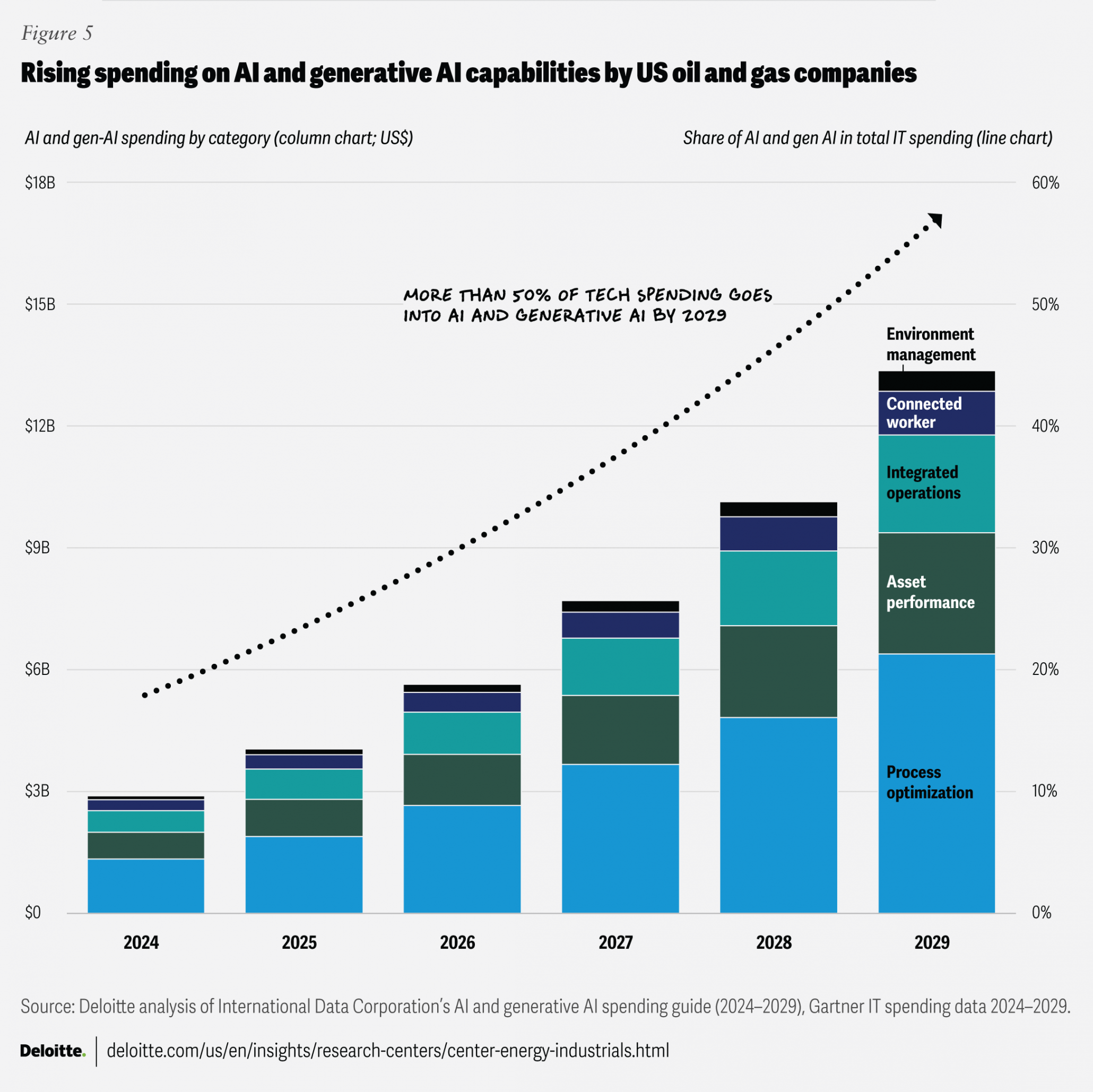

US Oil & Gas AI Spending to Surge Past $14B

The chart suggests a potential pathway to improve the economics of the high-cost, technologically complex Alaska LNG project, indicating how investment in AI and new technologies could enhance its long-stalled viability.

(Source: Deloitte)

3. Papua LNG

Company: Total Energies, Exxon Mobil, Santos

Installation Capacity: Approximately 4 MTPA

Applications: LNG Export

Source: JGC-Hyundai JV awarded EPC contract for major low-carbon LNG …

4. Ksi Lisims LNG

Company: Nisga’a Nation, Rockies LNG, Western LNG

Installation Capacity: Not specified in sources

Applications: LNG Export

Source: [PDF] The Ksi Lisims LNG Project and Broader Canadian Sector Face …

North American LNG Export Capacity to Surge

This chart provides the regional context for the Canadian Ksi Lisims project, illustrating that it is part of a broader surge in North American export capacity which affects all regional projects’ competitiveness.

(Source: The Coal Trader)

5. Browse LNG

Company: Woodside Energy, Shell, BP, Mitsubishi, Mitsui

Installation Capacity: Not specified in sources

Applications: LNG Export

Source: BP to sell 5 pc stake in Australia’s Browse LNG project – Argus Media

Mitsui Forecasts Profit Drop Amid LNG Headwinds

As Mitsui is a key partner in the Browse LNG project through its MIMI joint venture, a chart on its financial outlook provides a direct, stakeholder-specific perspective on the project’s commercial headwinds.

(Source: Investing.com)

6. Arctic LNG 2

Company: Novatek

Installation Capacity: ~19.8 MTPA

Applications: LNG Export

Source: Russia’s Gas Export Strategy: Adapting to the New Reality

China’s LNG Imports Show Significant Volatility

This chart highlights a major commercial risk for the Arctic LNG 2 project, as its viability is closely tied to demand from key Asian markets, particularly the large but historically volatile Chinese market.

7. Delfin Midstream FLNG

Company: Delfin Midstream

Installation Capacity: Not specified in sources

Applications: Floating LNG (FLNG) Export

Source: Delfin Midstream Gives Green Light to $5 Billion LNG Export Project

8. Argent LNG (Port Fourchon)

Company: Argent LNG

Installation Capacity: Not specified in sources

Applications: LNG Export

Source: Argent LNG advances Port Fourchon export project with FERC filings

US LNG Export Capacity Set for Major Expansion

This chart sets the national context for the Argent LNG project, positioning it as a key contributor to the major expansion of U.S. export capacity.

(Source: Deloitte)

9. Argentina LNG Project

Company: Eni, YPF, XRG

Installation Capacity: Not specified in sources

Applications: LNG Export

Source: [PDF] Eni – Annual Report 2025

LNG Market Forecasted to Reach $282B by 2035

The chart provides the primary market justification for a new national-scale project like Argentina’s, showing a large and growing global market value that the country aims to capture with its own export facility.

(Source: Market Research Future)

10. Various Unnamed U.S. Projects

Company: Multiple

Installation Capacity: Not specified in sources

Applications: LNG Export

Source: What Could a Possible Pause to U.S. LNG Export Approvals Mean …

Table: LNG Projects Facing Headwinds (2024-2026)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Next Decade | 27 MTPA | LNG Export | Fact sheet: $18.4 bn Rio Grande LNG project and headwinds |

| Alaska Gasline Development Corporation (AGDC) | 20 MTPA | LNG Export | US gas industry – LNG Export – Seala AI |

| Total Energies, Exxon Mobil, Santos | Approximately 4 MTPA | LNG Export | JGC-Hyundai JV awarded EPC contract for major low-carbon LNG … |

| Nisga’a Nation, Rockies LNG, Western LNG | Not specified in sources | LNG Export | [PDF] The Ksi Lisims LNG Project and Broader Canadian Sector Face … |

| Woodside Energy, Shell, BP, Mitsubishi, Mitsui | Not specified in sources | LNG Export | BP to sell 5 pc stake in Australia’s Browse LNG project – Argus Media |

| Novatek | ~19.8 MTPA | LNG Export | Russia’s Gas Export Strategy: Adapting to the New Reality |

| Delfin Midstream | Not specified in sources | Floating LNG (FLNG) Export | Delfin Midstream Gives Green Light to $5 Billion LNG Export Project |

| Argent LNG | Not specified in sources | LNG Export | Argent LNG advances Port Fourchon export project with FERC filings |

| Eni, YPF, XRG | Not specified in sources | LNG Export | [PDF] Eni – Annual Report 2025 |

| Multiple | Not specified in sources | LNG Export | What Could a Possible Pause to U.S. LNG Export Approvals Mean … |

U.S. LNG Export Capacity to Double by 2031

The chart perfectly illustrates the cumulative impact of the ‘various’ U.S. projects discussed in this section, showing their collective contribution to the doubling of national export capacity by 2031.

(Source: Seeking Alpha)

LNG Market Glut, Pre-FID Projects Face 50% Supply Jump

The sheer diversity of headwinds—from regulatory and financial to geopolitical and community opposition—signals a new, more complex phase for the LNG industry. The expected 50% jump in global capacity between 2025 and 2030 is forcing a strategic re-evaluation for any project not yet under construction. It is no longer enough to simply have access to gas reserves; projects must now navigate a gauntlet of risks. The persistent delays plaguing Total Energies‘ Papua LNG highlight the difficulty of reaching FID in the current environment. Similarly, the strong community and environmental justice opposition confronting Rio Grande LNG demonstrates that social license is now a material financial variable that can delay or derail multibillion-dollar investments. This environment suggests wider industry adoption is consolidating around established players with sanctioned projects, while new entrants face a much higher barrier to entry.

LNG Profit Margins Challenged by Tightening Spreads

The chart directly illustrates the financial consequences of the ‘market glut’ and ‘supply jump’ described in the section, showing how increased competition tightens spreads and challenges profitability for pre-FID projects.

(Source: Seeking Alpha)

USA vs. World, Regulatory Pause Creates U.S. LNG Backlog

Geographically, the LNG supply landscape is being reshaped by two dominant forces: the United States and Qatar. However, the U.S. faces unique self-imposed challenges. The administration’s pause on new export approvals in 2024, while later lifted, created a significant permitting backlog and heightened regulatory uncertainty, directly impacting early-stage developments like Argent LNG. In Canada, projects like Ksi Lisims LNG are grappling with weakening economics and long construction timelines. In Australia, policy uncertainty and partner exits, such as BP’s decision to sell its stake in the Browse LNG project in June 2026, are chilling investment. Meanwhile, Russia’s Arctic LNG 2 project serves as a stark reminder of how geopolitical events can cripple even technologically advanced projects through sanctions. This regional divergence indicates that market leadership is consolidating around players in low-cost jurisdictions with streamlined regulatory and political support.

US to Dominate Global LNG Exports by 2026

The chart visually supports the section’s theme by quantifying the U.S.’s growing dominance in the global LNG market, making the discussion of a regulatory pause and its international implications more impactful.

(Source: The Merchant’s News – Substack)

$18.4 B Rio Grande LNG, The Risk of Stranded Assets

While the underlying liquefaction technology is mature, the current market dynamics are stress-testing the maturity of *project development models*. The primary risk has shifted from technological execution to financial viability in an oversupplied market. Pre-FID projects like the large-scale Argentina LNG venture and Canada’s Ksi Lisims LNG are the most exposed to cost inflation and a narrowing market window. Even projects that have achieved partial FID, such as Next Decade‘s Rio Grande LNG, or those moving forward “despite” headwinds like Delfin Midstream FLNG, are not immune. They are launching directly into a period of intense price competition. The growing concern over stranded assets is a core issue, as investors question the long-term profitability of massive, capital-intensive fossil fuel projects in a world transitioning towards lower-carbon energy.

Natural Gas Demand Projected to Peak Around 2035

The chart provides the core evidence for the ‘risk of stranded assets’ discussed in the section, as a projected peak in natural gas demand threatens the long-term viability of capital-intensive infrastructure like the Rio Grande LNG plant.

(Source: Reuters)

Next Decade’s 27 MTPA Rio Grande LNG Project Viability (2025-2026)

For pre-FID LNG projects, securing binding, long-term offtake agreements before the 2026 supply glut fully materializes is the single most critical factor for survival. If global gas demand growth fails to keep pace with the massive wave of new capacity, watch for a sharp increase in project cancellations and a consolidation wave led by state-backed giants and established portfolio players. These developments could be happening now:

- Losing Steam: The strategic exit of major partners, exemplified by BP‘s decision to divest from the Browse LNG venture in June 2026, signals waning confidence among supermajors in the long-term economics of high-cost, complex greenfield projects.

- Gaining Traction: Sustained and organized community opposition is proving to be a material financial risk, as seen in the persistent legal and regulatory battles faced by Next Decade‘s Rio Grande LNG. This is becoming a key due diligence item for investors.

- Losing Steam: Projects with a history of repeated FID delays, such as Total Energies‘ Papua LNG, are rapidly losing their first-mover advantage and now face a much more competitive landscape than when they were initially conceived.

- Gaining Traction: The willingness of developers like Delfin Midstream to push forward with FID despite acknowledging market and regulatory headwinds indicates a strategic bet by some players on a demand recovery post-2028, accepting significant near-term risk.