SOFC Marinized Fuel Cells, $8.4 B NEOM Deal with Air Products, 1 SABA Offtake Agreement, and Over 20% of EU Projects Stalled (2021 to 2026)

Industry Adoption Risks: The Viability-Bankability Gap in Hydrogen Shipping

The critical path to deploying marinized fuel cells for hydrogen transport is stalled by a “viability-bankability” gap, where technologically mature systems cannot secure financing due to prohibitive fuel costs and a lack of guaranteed long-term demand. The market has shifted from a period of technology-led optimism between 2021 and 2024, characterized by pilot projects, to a sobering economic reality check from 2025 onward, where project success hinges on securing bankable commercial frameworks before final investment decisions are made.

- Between 2021 and 2024, industry focus was on validating the technical feasibility of maritime fuel cell applications. This period saw a rise in demonstration projects and partnerships aimed at proving the operational capabilities of Proton Exchange Membrane (PEM) and Solid Oxide Fuel Cells (SOFC) in marine environments.

- Starting in 2025, the narrative shifted to economic execution, exposing a gap between what is technologically possible and what is commercially bankable. The levelized cost of green hydrogen remains at a prohibitive $3.50-$6.00/kg, which is 2 to 3.5 times more expensive than grey hydrogen, creating a classic chicken-and-egg dilemma between shipowners and fuel producers.

- This economic friction is now manifesting in project failures. In July 2025, India’s Solar Energy Corporation (SECI) cancelled a major tender for green hydrogen hubs, and a late 2024 analysis by Westwood Energy found that over a fifth of all European hydrogen projects had been stalled or cancelled, citing immature offtake markets.

- In response, the market is pivoting to models that de-risk investment through binding offtake agreements. Infinium’s Project Atlas, selected by the Sustainable Aviation Buyers Alliance (SABA) in April 2026, exemplifies this strategy, requiring corporate buyers to enter long-term purchase agreements to secure project financing.

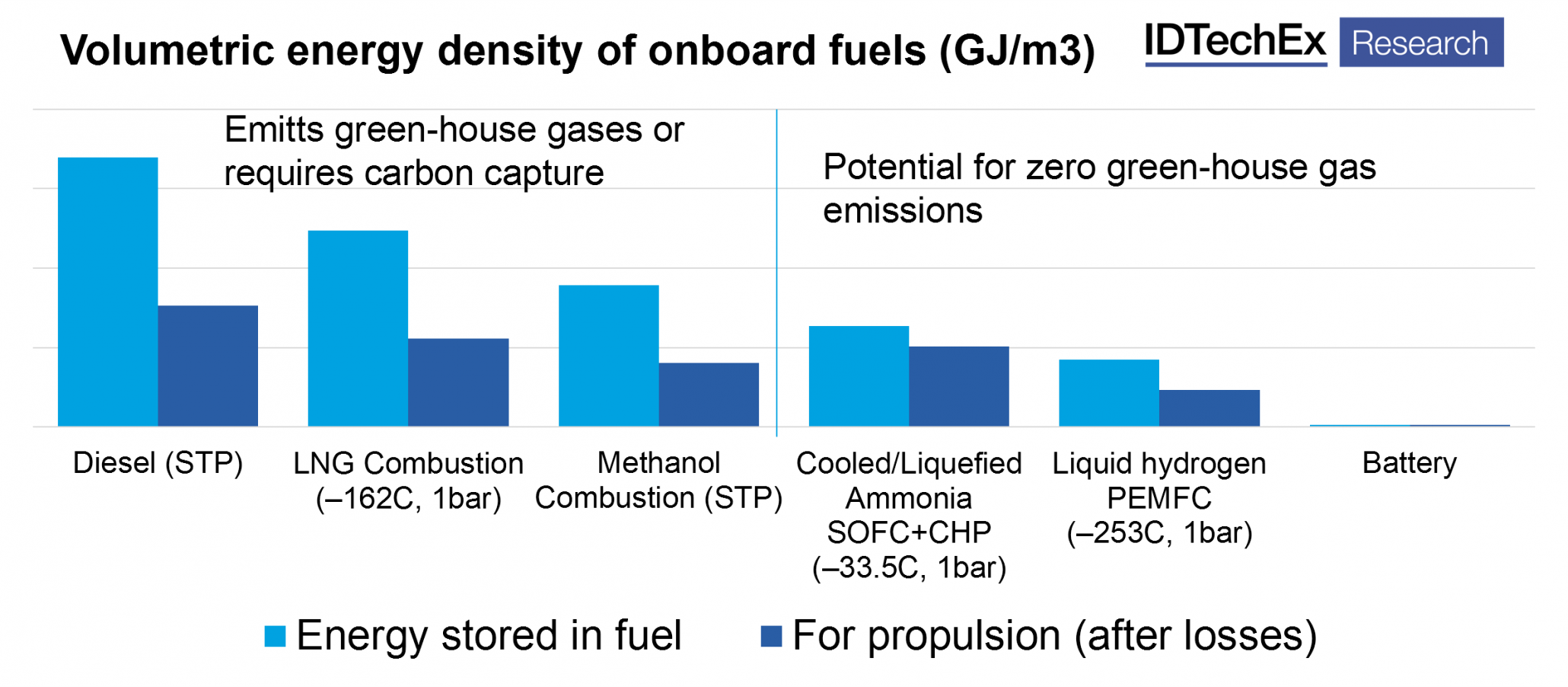

Hydrogen Lags in Onboard Fuel Energy Density

The section covers industry adoption risks for hydrogen shipping. The chart illustrates a fundamental technical risk by showing hydrogen’s low onboard energy density compared to other fuels, which directly impacts the viability and bankability of shipping applications by limiting range and cargo space.

(Source: IDTechEx)

Investment and Cancellations: Policy Support Fails to Guarantee Final Investment Decisions

Despite significant government incentives designed to spur the hydrogen economy, a wave of project cancellations and postponements from 2025 reveals that policy support alone is insufficient to close the financing gap for capital-intensive infrastructure. The market is now demonstrating that binding, long-term offtake agreements are the primary prerequisite for projects to reach a Final Investment Decision (FID), as they provide the revenue certainty required by investors.

- The U.S. Inflation Reduction Act (IRA), with its $3.00/kg production tax credit, was a major catalyst for project announcements through 2024. However, the period from 2025 to 2026 has shown that translating these announcements into FIDs is challenging without guaranteed buyers.

- Project cancellations are a direct signal of this commercial friction. The most prominent example is the cancellation of the Solar Energy Corporation of India (SECI) tender for green hydrogen hubs in July 2025, which followed a pattern of similar postponements in Europe due to economic headwinds and uncertain demand.

- Conversely, successful projects are explicitly tied to secured offtake. In August 2025, Copenhagen Infrastructure Partners (CIP) acquired a 70% stake in H 2 APEX’s German hydrogen project, a move that provides the capital needed to build out infrastructure to serve future offtakers.

- This dynamic underscores the “missing middle” financing challenge identified by the Council on Foreign Relations, where projects are technologically viable but cannot secure capital without firm revenue streams, a problem that subsidies alone have not solved.

Green Hydrogen Market to Exceed $230B by 2035

The section explains that policy support has not guaranteed final investment decisions, leading to cancellations. The chart provides crucial context by showing the massive projected market size, explaining why companies are pursuing these large, risky investments despite the uncertainty.

(Source: Precedence Research)

Table: Recent Hydrogen Project Investments and Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Copenhagen Infrastructure Partners (CIP) / H 2 APEX | Aug 2025 | CIP acquired a 70% majority stake in the first phase of H 2 APEX’s hydrogen project in Lubmin, Germany, providing critical capital for a large-scale production facility. | Offshore Energy |

| Solar Energy Corporation of India (SECI) | Jul 2025 | Cancelled a major tender for setting up green hydrogen production hubs, signaling commercial and economic headwinds despite government support. | Guidance Note on GFI Mechanism |

Partnership Data: Alliances Shift From Technology Validation to Bankable Offtake Deals

Partnerships in the hydrogen sector are evolving from technology-focused collaborations, prevalent from 2021 to 2024, to commercially-driven alliances centered on securing binding, long-term offtake agreements. This strategic shift from 2025 onward reflects the market’s recognition that converting project pipelines into operational assets depends entirely on establishing financeable revenue streams to de-risk massive upfront capital investments.

- The period between 2021 and 2024 was defined by technology development partnerships. For example, the collaboration between Air Products and Baker Hughes in November 2022 aimed to develop next-generation hydrogen compression technology, focusing on technical advancement rather than immediate commercial offtake.

- From 2025, the focus has pivoted to securing revenue. The $8.4 billion NEOM Green Hydrogen Project reached financial close in May 2023 only after its joint venture partners, including Air Products and ACWA Power, secured a 30-year binding offtake agreement with Air Products for the entire output of green ammonia.

- This trend is confirmed by the April 2026 selection of Infinium’s Project Atlas by the Sustainable Aviation Buyers Alliance (SABA). The entire premise of the deal is for SABA members to create bankable offtake contracts to support the project’s financing.

- Similarly, Texas LNG Brownsville secured a 20-year binding offtake agreement with RWE in February 2026, fully subscribing the project and enabling it to move toward FID. These deals demonstrate that firm, long-duration purchase commitments are now the most critical factor for project success.

Hydrogen Demand Dominated by Incumbent Industrial Uses

The section discusses the shift in alliances toward securing bankable offtake deals for new applications. The chart provides the context for this by showing that current demand is saturated by industrial uses, highlighting the critical need for such deals to create new, bankable demand in emerging sectors.

(Source: Nature)

Table: Key Commercial Agreements in the Hydrogen Sector

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Infinium / Project Atlas | Apr 2026 | Selected by SABA for members to negotiate long-term, binding offtake agreements for e Fuels, a model designed to secure project financing through guaranteed demand. | Decarbonisation Technology |

| Texas LNG Brownsville LLC | Feb 2026 | Signed a 20-year binding offtake agreement with RWE for LNG, which can serve as a feedstock for blue hydrogen, fully subscribing the project’s capacity. | Sunya AI |

| NEOM Green Hydrogen Project | May 2023 | The $8.4 billion project, a JV between ACWA Power, Air Products, and NEOM, reached financial close after securing a 30-year exclusive offtake agreement with Air Products. | Ammonia Energy |

Geographic Focus: Policy Creates Concentrated Hubs, But Infrastructure Lags

Government policies are successfully creating geographically concentrated hydrogen production and demand centers, but the physical infrastructure needed to connect these zones via maritime transport remains a primary bottleneck. While the U.S. has emerged as a production leader due to the IRA, and the EU is a designated demand center, regulatory delays and a lack of port-side infrastructure are fragmenting the development of a global hydrogen market.

- The United States, supercharged by the IRA’s $3.00/kg tax credit, has become the epicenter for green hydrogen project announcements. Final guidance released in early 2025 provided the certainty needed for developers to advance projects, such as Infinium’s large-scale e Fuels facility in Texas announced in May 2025.

- The European Union is positioned as a major demand hub, driven by the Renewable Energy Directive (RED III). However, as of January 2026, implementation is severely lagging, with only 4 of 27 member states having transposed the directive into national law, delaying the creation of a guaranteed market for imported hydrogen.

- Major production projects are concentrated in regions with low-cost renewables and strong government backing, most notably the NEOM project in Saudi Arabia. This creates a clear geographic separation between low-cost supply and high-value demand, making maritime transport essential.

- The core challenge is the absence of hydrogen-ready infrastructure at ports, including storage, bunkering facilities, and specialized carriers. This infrastructure gap prevents the physical connection of emerging U.S. and Middle Eastern production hubs with demand centers in Europe and Asia.

Hydrogen Hubs Market to See 19.2% CAGR

The section discusses the formation of concentrated geographic hubs due to policy. The chart directly supports this by providing a specific market forecast (19.2% CAGR) for these hubs, quantifying their expected growth and economic importance.

(Source: Polaris Market Research)

Technology Maturity: Fuel Cells Are Ready, But The Hydrogen Supply Chain Is Not

The core technology for marinized fuel cells is commercially mature and ready for deployment, but its large-scale adoption is constrained by the immaturity and high cost of the broader hydrogen supply chain. While both PEM fuel cells and SOFCs from companies like Doosan and Bloom Energy are at a high Technology Readiness Level (TRL 8-9), the pathways for producing and transporting clean hydrogen at a competitive cost are not yet established.

- Marinized fuel cells offer significant efficiency advantages, with SOFCs capable of reaching over 60% electrical efficiency, compared to 30-45% for traditional marine internal combustion engines. This technological validation was the focus of the 2021-2024 period.

- However, the fuel to power these systems remains the primary obstacle. Green hydrogen produced via electrolysis costs between $3.50 and $6.00 per kilogram, far from the sub-$2/kg target needed for widespread adoption.

- Key enabling technologies for hydrogen transport, such as green ammonia synthesis, are at a much lower maturity (TRL 5-7). This creates a critical weakness in the value chain, as ammonia is considered a leading carrier for long-distance maritime trade.

- The “viability-bankability gap” is therefore not a fuel cell problem but a fuel supply problem. The technological readiness of the propulsion system is overshadowed by the prohibitive cost of green hydrogen production and the lack of scalable infrastructure for its transport as a carrier liquid.

Hydrogen Fuel Supply Chain Efficiency Remains Low

The section argues that the hydrogen supply chain is not ready, contrasting it with mature fuel cell technology. This chart provides direct evidence for this claim by illustrating the low overall ‘well-to-wake’ efficiency of the hydrogen supply chain, a key barrier to adoption.

(Source: Frontiers)

SWOT Analysis: Marinized Fuel Cells for Hydrogen Transport

The strategic outlook for marinized fuel cells is defined by a conflict between high technological maturity and severe economic and infrastructural headwinds. While policy support and efficiency gains create significant opportunities, the high cost of green hydrogen and the difficulty in securing bankable offtake agreements present immediate threats to large-scale deployment.

Fuel Cell Market to Exceed $18B by 2030

The section provides a SWOT analysis for marinized fuel cells. The chart quantifies a major market ‘Opportunity,’ a key component of a SWOT analysis, by showing the fuel cell market is projected to grow to over $18 billion.

(Source: MarketsandMarkets)

Table: SWOT Analysis for Marinized Fuel Cells in Hydrogen Transport

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High theoretical efficiency (SOFC >60%), potential for zero-emission propulsion, growing number of pilot projects (e.g., by MOL). | Technology readiness for PEM and SOFC confirmed at TRL 8-9. Fuel flexibility of SOFCs for ammonia/methanol recognized as a key advantage for long-haul shipping. | The technology’s readiness is no longer in question; the focus has shifted to its superior efficiency and fuel flexibility as key value propositions over internal combustion engines. |

| Weaknesses | High CAPEX of fuel cell systems, durability concerns, and the challenge of on-board hydrogen storage. | The primary weakness is now the prohibitive cost of green hydrogen ($3.50-$6.00/kg) and the absence of port bunkering and storage infrastructure. | The bottleneck has moved from the ship-level technology to the external fuel supply chain and its underlying economics. The cost of fuel, not the engine, is the main barrier. |

| Opportunities | Strong policy signals (e.g., IMO 2050 goals, EU Green Deal), projected growth in the hydrogen economy, and potential for cost reduction through scale. | The US IRA offers a powerful $3.00/kg production tax credit. The marine fuel cell market is projected to reach $7.58 billion by 2035. | Policy has become a tangible financial incentive (IRA) rather than a distant target (IMO goals), creating a direct, though still insufficient, economic pull for green hydrogen projects. |

| Threats | Uncertainty over future regulations and the pace of cost reduction for green hydrogen production. | Policy instability (IRA amendments, slow RED III adoption in EU), and a wave of project cancellations due to the failure to secure bankable offtake agreements. | The threat has shifted from regulatory uncertainty to commercial execution risk. The market is now actively punishing projects that cannot secure long-term buyers, regardless of policy support. |

Scenario Modelling: Bankable Offtake Agreements Will Dictate 2026-2027 Deployment

The primary indicator for scaling maritime hydrogen transport in the next 12-18 months is not further technological maturation but the conversion rate of announced projects into Final Investment Decisions (FIDs). This hinges almost exclusively on the ability of project developers to secure binding, long-term offtake agreements that make multi-billion-dollar infrastructure investments bankable.

- If a critical mass of offtake agreements is signed: Watch for a wave of FIDs for large-scale green hydrogen production hubs and associated port infrastructure. This would signal that the “viability-bankability” gap is beginning to close. Key signals include announcements from major industrial consumers or shipping lines like Hapag-Lloyd committing to green ammonia or methanol contracts.

- If offtake agreements remain scarce: Expect continued project delays and cancellations, particularly in regions with less aggressive subsidies than the U.S. The hydrogen economy would remain fragmented in pilot projects, failing to connect production and demand at scale. A key signal would be major energy companies shelving previously announced hydrogen projects.

- What could be happening: A two-tiered market is developing. Projects with strong sovereign backing (e.g., NEOM) or those integrated with credit-worthy corporate offtakers (e.g., Infinium/SABA) will advance, while speculative projects will fail. The success of marinized fuel cells will depend on their integration into these successful, vertically-aligned value chains.

Hydrogen Vehicle Market Forecasts Strong Growth

The section focuses on scenario modelling to predict future deployment. The chart is a direct example of this, presenting a market forecast—a form of scenario modelling—for the deployment of hydrogen technology in the key vehicle sector.

(Source: Mordor Intelligence)

The questions your competitors are already asking

This report covers one angle of the viability-bankability gap in the hydrogen shipping market. The questions that matter most depend on your work.

- What is the status of the $8.4B NEOM-Air Products green hydrogen deal? Is it progressing from announcement to a bankable offtake framework for shipping?

- What is the commercial outlook for marinized fuel cell deployment in hydrogen shipping by 2030, given over 20% of EU projects are stalled?

- How do marinized SOFCs compare to PEM fuel cells for hydrogen transport, considering the prohibitive $3.50-$6.00/kg cost of green hydrogen?

- Which shipping lines or cargo owners are successfully securing bankable offtake agreements for green hydrogen transport, bridging the viability-bankability gap?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.