Top 10 SMR Projects: Meta’s 6.6 GW Ambition & Amazon’s X-energy Partnership Drive Nuclear Deals (2024-2025)

A strategic shift is underway in the energy sector, with technology corporations emerging as the primary catalysts for the Small Modular Reactor (SMR) market. Driven by the voracious energy demands of Artificial Intelligence, hyperscale data centers are underwriting the first wave of commercial SMR projects. Landmark commitments, including Meta’s staggering 6.6 GW nuclear energy ambition, Amazon’s 960 MW project with X-energy, and Google’s 500 MW agreement with Kairos Power, provide the bankable, long-term offtake agreements necessary to de-risk and accelerate SMR deployment. The dominant trend for 2025 is clear: corporate demand for 24/7 carbon-free energy is transforming SMRs from a theoretical solution into a commercially funded infrastructure imperative, bypassing traditional utility procurement models.

1. Meta Nuclear Energy Projects

Company: Meta Platforms, Inc.

Installation Capacity: Up to 6.6 GW

Applications: Data Center Power

Source: Meta Signs Three Nuclear Deals of Up to 6.6 GW to Fuel AI Data …

2. Darlington New Nuclear Project

Company: Ontario Power Generation (OPG), GE Hitachi

Installation Capacity: 1, 200 MW

Applications: Grid Power

Source: Small modular reactors | Darlington SMR – OPG

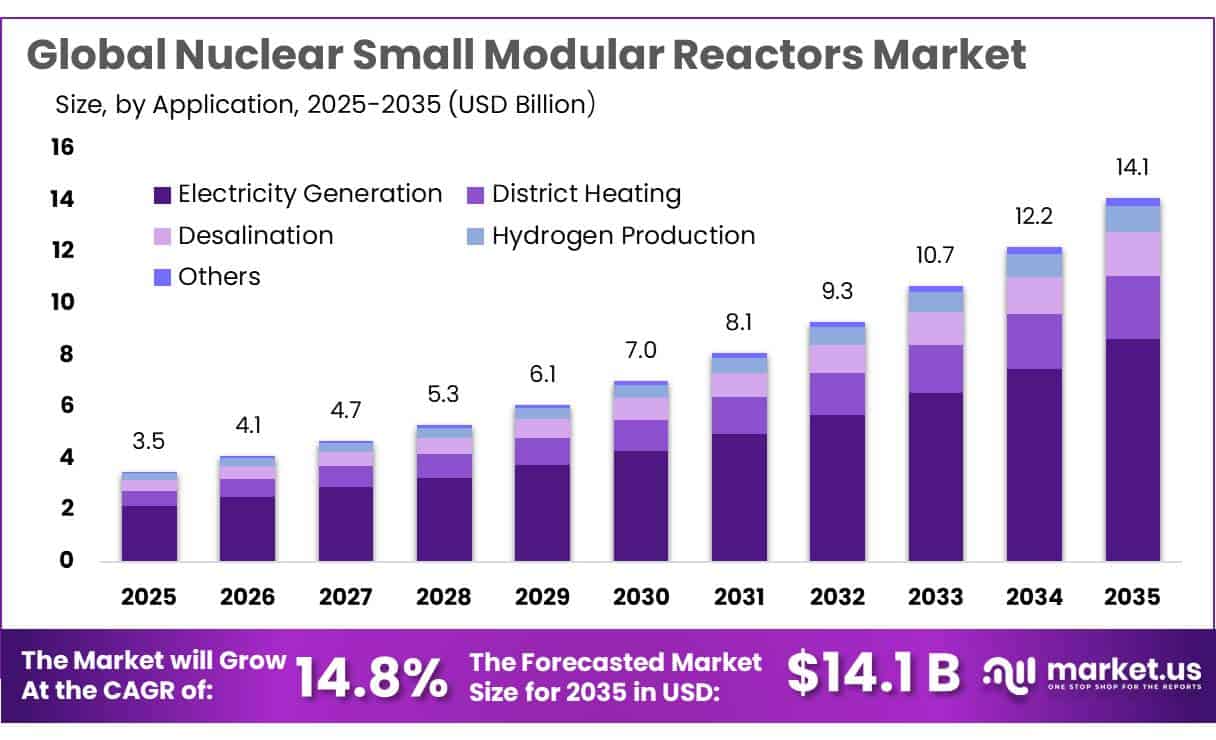

SMR Market to Exceed $14B by 2035

The chart quantifies the significant market opportunity that pioneering projects like the Darlington SMR are tapping into, providing financial context for the investment in this first-of-a-kind G7 deployment.

(Source: Market.us)

3. Amazon-Energy Northwest SMR Project

Company: Amazon, X-energy, Energy Northwest

Installation Capacity: 960 MW

Applications: Data Center Power

Source: Washington nuclear facility will deploy 12 Amazon-funded SMRs

Data Centers Face Up to 7-Year Wait for Grid Power

This chart highlights the critical problem that motivates companies like Amazon to pursue alternative power sources like SMRs. The long wait times for grid connections make on-site, reliable nuclear power an attractive solution for rapid data center expansion.

(Source: Energy Industry Insights from Avanza Energy – Substack)

4. Microsoft-Constellation TMI PPA

Company: Microsoft, Constellation Energy

Installation Capacity: 835 MW

Applications: Data Center Power

Source: Nuclear power for AI: inside the data center energy deals | Introl Blog

Data Center Power Demand Projected to Skyrocket

The chart provides the macro context for Microsoft’s PPA, illustrating the massive projected increase in data center power demand that necessitates securing large-scale, reliable, and carbon-free energy sources.

(Source: POWER Magazine)

5. Holtec SMR Deployment at Palisades

Company: Holtec International, DOE, TVA

Installation Capacity: 600 MW

Applications: Grid Power

Source: Energy Department Selects TVA and Holtec to Advance Deployment …

SMR Project Pipeline Swells in Permitting Stage

This chart directly reflects the current status of many SMR projects like the one at Palisades, which are progressing through the crucial permitting and licensing phase before construction can begin.

(Source: POWER Magazine)

6. Google-Kairos Power Agreement

Company: Google, Kairos Power, TVA

Installation Capacity: 500 MW

Applications: Data Center Power

Source: Google Bets Big on Nuclear: Inks Deal with Kairos Power for 500 …

AI Power Demand Varies by Phase

This chart explains the underlying driver for Google’s interest in advanced nuclear power, linking the specific phases of AI development to energy consumption, a problem the Kairos agreement aims to solve.

(Source: tech plus trends)

7. Nu Scale Power Project in Romania

Company: Nu Scale Power, Ro Power Nuclear

Installation Capacity: 462 MWe

Applications: Grid Power

Source: Nu Scale expects 77-MWe design approval in July, first SMR order …

Global Nuclear Capacity to Grow 100 GW by 2035

The chart contextualizes the Romanian project within a broader international trend of expanding nuclear capacity, demonstrating that this SMR deployment is part of a global movement to increase nuclear power.

(Source: POWER Magazine)

8. Terra Power Natrium Demo Project

Company: Terra Power, GE Hitachi, Pacifi Corp

Installation Capacity: 345 MW

Applications: Grid Power

Source: These nuclear companies lead the race to build small reactors in U.S.

9. Oracle SMR Data Center Project

Company: Oracle

Installation Capacity: 1, 000 MW (Gigawatt-scale)

Applications: Data Center Power

Source: Oracle will use three small nuclear reactors to power new 1-gigawatt …

Data Center Power Market to Exceed $50B

The chart quantifies the size of the data center power market, providing the financial context for why a company like Oracle would make a strategic investment in its own power generation via SMRs.

(Source: MarketsandMarkets)

10. Holtec-EDF-Tritax UK Data Center

Company: Holtec, EDF, Tritax

Installation Capacity: Not specified

Applications: Data Center Power

Source: UK and US firms outline plans for advanced nuclear development …

Table: Top SMR Projects by Planned Capacity and Application

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Meta Platforms, Inc. | Up to 6.6 GW | Data Center Power | Meta Signs Three Nuclear Deals… |

| Ontario Power Generation (OPG), GE Hitachi | 1, 200 MW | Grid Power | Small modular reactors | Darlington SMR – OPG |

| Amazon, X-energy, Energy Northwest | 960 MW | Data Center Power | Washington nuclear facility… |

| Microsoft, Constellation Energy | 835 MW | Data Center Power | Nuclear power for AI… |

| Holtec International, DOE, TVA | 600 MW | Grid Power | Energy Department Selects TVA and Holtec… |

| Google, Kairos Power, TVA | 500 MW | Data Center Power | Google Bets Big on Nuclear… |

| Nu Scale Power, Ro Power Nuclear | 462 MWe | Grid Power | Nu Scale expects 77-MWe design approval… |

| Terra Power, GE Hitachi, Pacifi Corp | 345 MW | Grid Power | These nuclear companies lead the race… |

| Oracle | 1, 000 MW | Data Center Power | Oracle will use three small nuclear reactors… |

| Holtec, EDF, Tritax | Not specified | Data Center Power | UK and US firms outline plans… |

Gas Engine Orders for Data Centers Surge

This chart illustrates a current, carbon-intensive solution to the data center power problem, highlighting the market opportunity for cleaner alternatives like the proposed Holtec SMR project.

(Source: Energy Industry Insights from Avanza Energy – Substack)

SMR Adoption for Data Centers, Tech Giants’ 10 GW+ Demand Signals Market Shift

The data reveals a clear and decisive pivot in the SMR market, driven by direct corporate offtake rather than traditional utility planning. Projects linked to Meta, Amazon, Microsoft, Google, and Oracle account for over 10 GW of stated demand and planned capacity. This trend signifies more than just a new customer segment; it represents a fundamental change in the project development model. For instance, Amazon’s dual role as an investor in X-energy and the anchor customer for its 960 MW plant in Washington creates a vertically-aligned incentive structure that reduces financial risk and accelerates the path to commercialization. This model, where the end-user becomes a key enabler of the technology, is being replicated by Google’s agreement with Kairos Power and is the implicit goal of Meta’s massive RFP. This is a critical departure from the speculative nature of past nuclear projects.

Data Center Power Market Shifts to Services

The chart’s depiction of a market shifting towards services aligns with the section’s headline, as SMR adoption by tech giants represents a move towards integrated, dedicated power solutions.

(Source: MarketsandMarkets)

North America Leads SMR Deployment, OPG’s Darlington Plant Sets G 7 Precedent

Geographically, North America has firmly established itself as the global leader in SMR deployment. The Darlington New Nuclear Project in Ontario, Canada, is a vital pathfinder, being the first commercial SMR project to move into the construction phase in a G 7 nation. Its progress provides an essential real-world benchmark for costs, supply chain logistics, and regulatory execution for GE Hitachi’s BWRX-300 technology. The United States, however, is the epicenter of demand, with nearly all major tech-driven projects located within its borders. This is fueled by the concentration of AI development and data center infrastructure, combined with supportive federal initiatives like the DOE’s loan programs. Europe is an important secondary market, with projects like Nu Scale’s in Romania and the planned Holtec-EDF data center campus in the UK aimed at bolstering energy security and meeting regional decarbonization mandates.

US Leads World in SMR Development Pipeline

The chart visually confirms the section’s claim that North America is at the forefront of the SMR development pipeline, providing context for the significance of the Darlington project as a G7 precedent.

(Source: Enerdata)

345 MW Under Construction, Terra Power’s Natrium Demonstrates Advanced Reactor Viability

These projects reveal a multi-layered maturation of SMR technology. A few key designs are breaking away from the pack and moving from paper to physical construction. GE-Hitachi’s BWRX-300 and Terra Power’s Natrium reactor are the most advanced, having broken ground at sites in Canada and Wyoming, respectively. The Natrium project is particularly significant for its integrated molten salt energy storage system, demonstrating how advanced reactors can provide flexible, dispatchable power to complement renewables. In the next tier, technologies like X-energy’s Xe-100 and Holtec’s SMR-300 have secured major commercial partnerships that are driving them toward deployment. Finally, Google’s deal with Kairos Power validates a more advanced, non-light-water reactor design (KP-FHR), indicating that major customers are willing to back next-generation technology to meet their long-term energy goals.

SMR Project Pipeline Surges, Driven by Data Centers

This chart shows the overall momentum in the SMR pipeline, of which the TerraPower project is a leading example. It illustrates that this project’s move into construction is part of a larger, surging trend.

(Source: Wood Mackenzie)

Meta’s 6.6 GW RFP, Key SMR Contract Award to Watch in 2026

The strategic focus has now shifted from project announcements to execution. The primary action for market participants is to monitor the construction progress of first-movers and the ability of the nascent SMR supply chain to scale without significant bottlenecks or cost overruns.

- Signal to watch: The progress of the Darlington and Terra Power Natrium projects will be scrutinized. Any reported delays or cost overruns could dampen investor confidence, while on-time, on-budget execution would provide a powerful tailwind for the entire industry.

- Signal to watch: The selection of an SMR developer for Meta’s multi-gigawatt RFP will be a defining market event, likely cementing the chosen technology provider as a market leader for years to come.

- Signal to watch: The final investment decision for Nu Scale’s VOYGR-6 plant in Romania, expected in early 2026, will be a critical test for deploying a US-designed SMR in Europe and a bellwether for the region’s nuclear ambitions.

- Signal to watch: The emergence of further “repowering” projects, similar to Holtec’s plan for the Palisades site, which leverage existing grid infrastructure to reduce costs and accelerate timelines.

The questions your competitors are already asking

This report covers one angle of SMR commercialization, driven by corporate demand for data center power. The questions that matter most depend on your work.

- Which SMR developers, like X-energy and Kairos Power, are gaining ground in the data center power market?

- What is the outlook for SMR deployment for data center power by 2030, given the current project pipeline from Meta, Amazon, and Google?

- Which hyperscale data center operators are adopting SMRs, and what partnership models are emerging beyond the Amazon/X-energy deal?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.