Green Hydrogen Shipping, 18% Port Readiness, $12 B Market, and 5 US Projects Launching (2025)

Green Hydrogen Adoption in Maritime Projects Hindered by Cost and Infrastructure Gaps

The maritime industry’s adoption of green hydrogen is constrained by unfavorable economics and a critical lack of bunkering infrastructure, forcing carriers to adopt a cautious stance despite mounting regulatory pressure. In 2025, the significant price premium of green hydrogen and the scarcity of refueling facilities at major ports create a high-risk environment, slowing direct investment in hydrogen-powered vessels and pushing focus towards more mature transitional fuels.

- In the 2025 period, the production cost of green hydrogen ranges from $3 to $12 per kilogram, a prohibitive price compared to the $1 to $3 per kilogram for grey hydrogen derived from fossil fuels.

- The cost disparity extends to green hydrogen derivatives, with green ammonia priced at approximately $800 per tonne in 2025, substantially higher than the $455.73 per tonne for High Sulphur Fuel Oil (HSFO).

- A fundamental “chicken-and-egg” problem persists, where a lack of hydrogen-powered vessels discourages port infrastructure investment, while the absence of bunkering facilities deters shipping lines from ordering such ships.

- As of 2025, analysis shows only 18% of global ports have any form of green fuel bunkering capabilities, representing a major physical bottleneck for the adoption of fuels like green hydrogen.

- In response, many carriers are prioritizing investments in dual-fuel vessels that can operate on green methanol, which is viewed as a more commercially ready transitional fuel due to easier handling and more developed, albeit still limited, infrastructure.

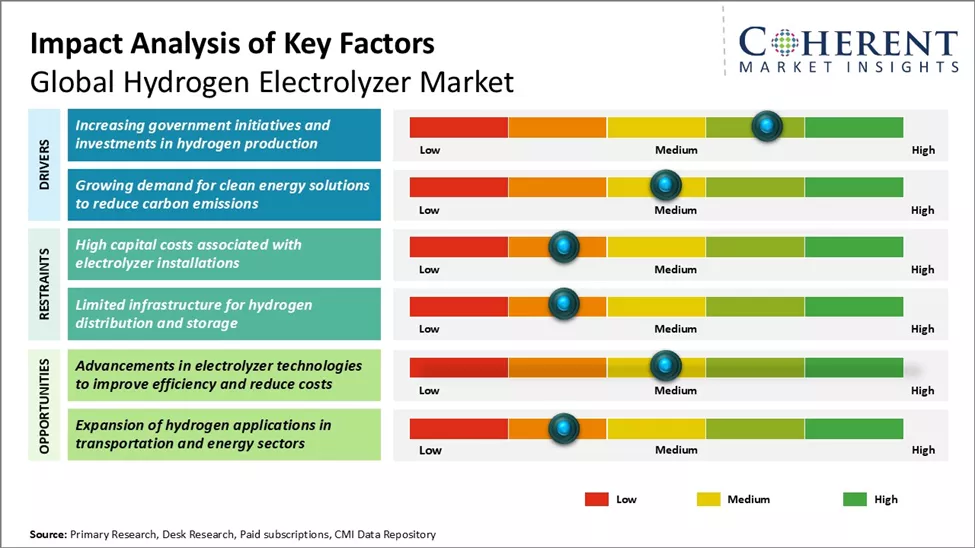

Electrolyzer Market Restraints Mirror Maritime Hydrogen Hurdles

The section discusses adoption being ‘Hindered by Cost and Infrastructure Gaps.’ The chart’s headline, mentioning ‘Restraints’ and ‘Hurdles,’ directly mirrors the section’s theme of challenges and barriers in the hydrogen market.

(Source: Coherent Market Insights)

$20 B Sustainable Fuel Market, Pacific International Lines Navigates Investment Cycles

The sustainable marine fuel market is valued at approximately $20 billion in 2025, with forecasts indicating explosive growth driven by decarbonization mandates; however, this top-line figure obscures the divergent investment trajectories for different fuel types. While the overall market is expanding, direct investment into green hydrogen production and maritime assets faces delays due to project cancellations and economic uncertainty, contrasting with the more immediate, smaller-scale investments flowing into biofuels and green methanol.

- The sustainable marine fuel market is estimated between $19.9 billion and $21.69 billion in 2025, with projections to exceed $600 billion by the early 2030 s, signaling a massive capital reallocation within the energy and shipping sectors.

- Despite long-term growth projections, the near-term investment climate for green hydrogen is challenging. A September 2025 report from the IEA noted a wave of project cancellations and delays, creating supply-side uncertainty.

- Conversely, the green methanol ships market reached $4.29 billion in 2025 and is projected to grow at a CAGR of over 25%, reflecting investor confidence in it as a viable near-term decarbonization pathway.

- Global investment in the broader hydrogen economy is expected to surpass $320 billion by 2030, but securing Final Investment Decision (FID) for large-scale green hydrogen projects remains a significant hurdle in 2025.

Green Hydrogen Market To See Explosive Growth

The section heading focuses on navigating investment cycles within a large sustainable fuel market. A chart illustrating ‘Explosive Growth’ provides the context for why this market requires active investment cycle navigation and highlights the opportunity.

(Source: Mordor Intelligence)

Partnership Strategy for Pacific International Lines: Green Shipping Corridors

The dominant partnership strategy in the maritime sector in 2025 is the formation of Green Shipping Corridors, a collaborative model designed to de-risk investment by concentrating infrastructure and vessel deployment on specific high-traffic routes. With no specific green hydrogen partnerships announced by Pacific International Lines, the industry-wide focus on these corridors indicates a strategic shift towards multi-stakeholder collaboration to overcome the high costs and logistical challenges of the energy transition.

- Green Shipping Corridors, such as the one being developed between ports in the Pacific Northwest and Singapore, are the primary mechanism for pooling demand and justifying investment in new bunkering infrastructure.

- Companies are forming joint ventures specifically to address infrastructure gaps, with a focus on developing bunkering technology and services for hydrogen derivatives like ammonia.

- Port authorities are acting as key facilitators. Klaipėda Port in Lithuania, for instance, announced plans to commence green hydrogen production in 2026 with an initial 2 MW electrolysis capacity.

- In Asia, the Port of Hong Kong is developing a Code of Practice for green methanol bunkering in 2025 and will begin feasibility studies for hydrogen and ammonia, signaling regional commitment to building out the necessary supply chains.

Green Hydrogen Prices Vary Across Key Markets

This section is about creating a ‘Partnership Strategy’ for ‘Green Shipping Corridors.’ A chart showing that ‘Prices Vary Across Key Markets’ is crucial data for identifying optimal partners and routes for cost-effective green hydrogen sourcing.

(Source: IMARC Group)

Global Green Hydrogen Hotspots, Pacific International Lines Market Exposure

The development of green hydrogen production and infrastructure is geographically uneven, with North America, Europe, and key Asian hubs emerging as leaders due to strong policy support and strategic industrial planning. For a global carrier like Pacific International Lines, navigating this fragmented geographic landscape is critical for future fuel procurement and operational compliance.

- In the period before 2025, green hydrogen initiatives were largely in planning stages globally. From 2025 onwards, these plans are materializing into physical projects and specific regulatory actions in key regions.

- The European Union is a primary driver, with its Fuel EU Maritime regulation taking effect in 2025, mandating a 2% reduction in GHG intensity for fuels used by ships.

- The United States is incentivizing domestic production through policy measures like the Hydrogen Tax Credit (45 V), with five major green hydrogen production projects scheduled to begin operations in 2025.

- Asia shows significant activity, with Singapore positioning itself as a central hub for hydrogen trade and bunkering, while the Asia Pacific green hydrogen market is projected to grow from $5.84 billion in 2025 to $112.79 billion by 2035.

Asia-Pacific Leads Global Green Hydrogen Market

The section discusses ‘Global Green Hydrogen Hotspots’ and Pacific International Lines’ (PIL) market exposure. As PIL is a Singapore-based company, a chart identifying the ‘Asia-Pacific’ as the leading market directly addresses both the ‘hotspot’ and ‘market exposure’ aspects.

(Source: SkyQuest Technology Consulting)

Technology Readiness: Green Hydrogen in Maritime Is Pre-Commercial Scale

While the core technologies for producing green hydrogen, such as alkaline electrolysis, are mature, their application at the scale required for the maritime industry remains in a pre-commercial phase in 2025. The sector is reliant on the advancement of ancillary technologies, including high-density storage, safe bunkering systems, and efficient onboard propulsion like solid-oxide fuel cells, which are still navigating certification and scaling challenges.

- Between 2021-2024, the focus was on pilot projects and engine development for hydrogen and its derivatives. In 2025, the conversation has shifted to the immense challenge of scaling up production and building the global distribution infrastructure.

- Alkaline electrolyzers dominate the production market in 2025, holding over 75% of market share due to their proven reliability and cost-effectiveness for large-scale deployment.

- Onboard technology is advancing, with hydrogen fuel cell systems progressing through the certification process in 2025, but widespread commercial availability on large vessels is not yet a reality.

- The industry’s pragmatic approach is demonstrated by the surge in orders for dual-fuel methanol vessels, indicating that while hydrogen is the long-term goal, its technological and logistical ecosystem is not yet mature enough for widespread adoption. The use of other decarbonization technologies like Direct Air Capture will also be part of the long term strategy.

Global Green Hydrogen Demand Outpaces Supply

The section states that green hydrogen in maritime is at a ‘Pre-Commercial Scale.’ A chart showing that ‘Demand Outpaces Supply’ perfectly illustrates a key characteristic of a nascent, pre-commercial market where technology and production are not yet mature.

(Source: IMARC Group)

SWOT Analysis for Pacific International Lines Green Hydrogen Initiatives

The strategic landscape for green hydrogen in maritime shipping is defined by a tension between strong regulatory drivers and significant real-world constraints related to cost, infrastructure, and technology readiness. For carriers like Pacific International Lines, navigating this environment requires balancing long-term decarbonization goals with near-term commercial viability.

Green Hydrogen Market Forecasts 60% CAGR

This section is a ‘SWOT Analysis.’ A chart forecasting a ‘60% CAGR’ provides a powerful quantitative data point for the ‘Opportunities’ component of the SWOT, justifying strategic initiatives in the green hydrogen space.

(Source: MarketsandMarkets)

Table: SWOT Analysis of the Maritime Green Hydrogen Market (2025)

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Zero-emission potential recognized as a key long-term decarbonization solution for shipping. Theoretical support from policymakers. | IMO Net-Zero Framework discussions solidify targets, giving a clear long-term signal. EU Fuel EU Maritime regulation provides a concrete mandate. | Regulatory ambition solidified into initial, legally binding mandates (EU), moving from theoretical to practical drivers for adoption. |

| Weaknesses | High projected production cost and lack of bunkering infrastructure identified as major barriers. Concerns over onboard storage density. | Production cost remains 3-4 x higher than grey hydrogen. Only 18% of ports have green bunkering. A wave of project delays is reported. | The scale of the cost and infrastructure gap is validated by market data in 2025, confirming that these are not short-term but systemic challenges. |

| Opportunities | Concept of Green Shipping Corridors proposed to de-risk investment. National hydrogen strategies announced in several countries. | Corridors (e.g., Pacific Northwest-Singapore) move into active development. The U.S. 45 V tax credit implementation drives project planning. | The “corridor” concept is validated as the primary strategic tool for industry collaboration, moving from white papers to active planning. |

| Threats | Competition from other alternative fuels like LNG, biofuels, and ammonia. Risk of uncoordinated regional regulations creating a complex compliance environment. | Green methanol emerges as a strong transitional competitor, with a $4.29 B market for methanol ships. Policy uncertainty persists around the final IMO framework. | Green methanol’s role as a primary transitional fuel is validated by vessel order books and market growth, posing a near-term competitive threat to hydrogen’s momentum. |

Scenario Modeling for Pacific International Lines in 2026

The critical factor for 2026 will be whether the maritime industry sees tangible progress in closing the gap between regulatory ambition and on-the-ground reality for green hydrogen. For a carrier like Pacific International Lines, the key is to monitor signals that reduce investment risk and validate a path to scalability.

- If the final IMO Net-Zero Framework is adopted with strong, globally consistent mandates in late 2025, then watch for a significant increase in long-term offtake agreements for green hydrogen and ammonia in 2026, as carriers move to secure future supply.

- If a critical mass of green hydrogen projects announced in the U.S. and Europe successfully reach Final Investment Decision (FID) in 2026, then watch for a corresponding uptick in orders for ammonia-ready and hydrogen-fuel-cell-capable vessels, as confidence in future fuel availability grows.

- If progress on bunkering infrastructure at major hubs like Singapore, Rotterdam, and in the Pacific Northwest stalls or faces delays, then these could be happening: carriers will double down on transitional fuels like green methanol and biofuels, further delaying hydrogen’s widespread adoption by several years.

Wind Power Leads Green Hydrogen Production in 2025

The section is about ‘Scenario Modeling for… 2026.’ This chart provides a specific, near-term forecast (2025) about the production mix (‘Wind Power Leads’), which serves as a critical input assumption for building a plausible 2026 scenario model.

(Source: Yahoo Finance)

The questions your competitors are already asking

This report covers one angle of Pacific International Lines’ green hydrogen strategy for 2025. The questions that matter most depend on your work.

- Pacific International Lines’ activities in green hydrogen. Are its key projects progressing from pilot to deployment for 2025?

- What is the outlook for green hydrogen bunkering infrastructure deployment, given the current 18% port readiness?

- How does green hydrogen compare to green methanol as a viable fuel for shipping lines like PIL in 2025?

- Which shipping carriers are adopting dual-fuel vessels capable of running on green hydrogen or its derivatives?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.