Petro China CCUS Strategy: 1 M Ton Xinjiang EOR Project, $5.59 B CNPC Asset Deal, and 4 M Ton National Volume (2021 to 2025)

CCUS-EOR Projects, Petro China 1 M Ton Xinjiang Milestone vs CNOOC Offshore Model

In 2025, Petro China‘s carbon capture adoption solidified around large-scale onshore Enhanced Oil Recovery (EOR) projects, creating a strategic divergence from competitors like CNOOC who are pioneering offshore dedicated sequestration. This EOR-centric model leverages existing assets to turn CO 2 into a productive input for oil extraction, prioritizing economic returns over pure-play carbon disposal.

- Prior to 2025, Petro China‘s CCUS projects were operational but had not yet reached megaton-scale annual injection rates; 2025 marked a significant operational scale-up, with CO 2 injection volumes increasing 55.9% year-over-year as of August.

- The company’s flagship Xinjiang Oilfield CCUS project became China’s first to surpass 1 million tons of CO 2 injection in a single year during 2025, using captured emissions from local coal-chemical plants to boost output from mature oil fields.

- In direct contrast, CNOOC launched China’s first offshore carbon storage facility in May 2025, the Enping 15-1 project, which is designed for dedicated sequestration with an annual capacity of over 100, 000 metric tons, not EOR.

- This strategic split is critical: Petro China‘s model generates revenue from increased oil production, while CNOOC‘s project represents a move toward a service model for permanent CO 2 disposal, essential for decarbonizing industries beyond oil and gas.

- Petro China‘s EOR focus contributes significantly to China’s total onshore CCUS injection volume, which reached 4 million tons annually in 2025 across more than 10 separate EOR projects.

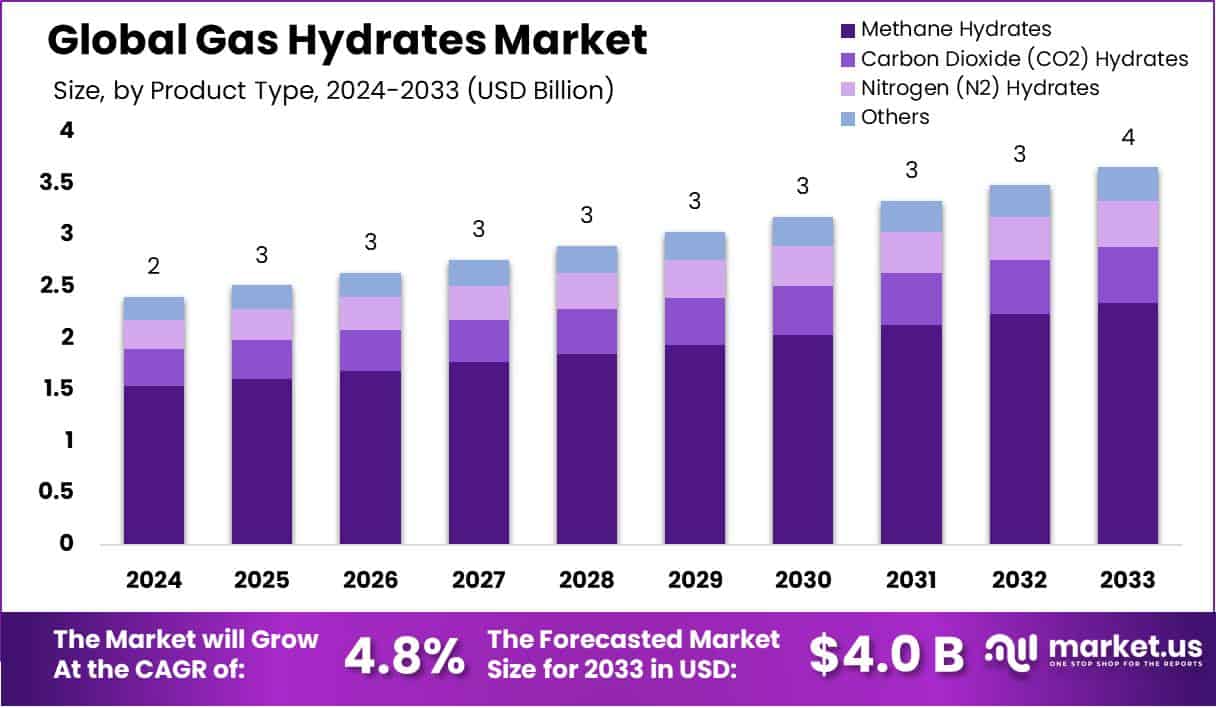

CO2 Hydrates Market Grows Amid Carbon Sequestration Push

The section compares specific CCUS project models (Petro China’s onshore EOR vs. CNOOC’s offshore). A chart on the emerging market for CO2 hydrates, a novel sequestration technology, provides context on the technological landscape and future strategies beyond current project types.

(Source: Market.us)

$9.19 B in Deals, Petro China Gas Infrastructure Investment Strategy

Petro China‘s 2025 investment strategy heavily prioritized natural gas infrastructure through over $9 billion in announced deals, framing it as a critical transition fuel while direct investment in dedicated low-carbon solutions remained a small fraction of its capital expenditure. These investments strengthen the company’s core fossil fuel business and create infrastructure that could be adapted for future CO 2 transport.

- The largest investment was a $5.59 billion proposal in August 2025 to acquire three major gas storage facilities from its parent company, CNPC, consolidating its control over key national energy assets.

- In November 2025, Petro China launched a $3.6 billion joint venture with state-owned Pipe China to establish two major gas storage companies, further expanding China’s national gas handling and storage capacity.

- These substantial investments in fossil fuel infrastructure dwarf the company’s direct spending on renewables and dedicated sequestration, which is estimated at only 1-2% of total capital expenditure.

- This spending pattern reveals a strategy of incremental decarbonization, prioritizing the resilience of its profitable gas business while making measured, not radical, steps into non-EOR carbon management.

Gas Storage Capacity Expands Significantly by 2025

The section details Petro China’s $9.19 billion investment strategy in gas infrastructure. The chart directly visualizes a key outcome of this strategy, showing the planned expansion of gas storage capacity by 2025.

(Source: Panda Perspectives – Substack)

Table: Petro China 2025 Strategic Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Acquisition from CNPC | August 2025 | Proposed a $5.59 billion acquisition of three gas storage facilities (Xinjiang, Xiangguosi, Liaohe) to enhance infrastructure for gas handling, which is directly applicable to future large-scale CO 2 transport and storage. | Reuters |

| Joint Venture with Pipe China | November 2025 | Established two major gas storage joint ventures with a combined investment of $3.6 billion to enhance China’s gas storage capacity, supporting the role of natural gas as a transition fuel. | Oil Price.com |

| Corporate Transformation | July 2025 | Announced a US$9.6 billion investment to transform its business, with a significant portion directed towards low-carbon initiatives, including CCUS and developing a green industrial layout. | Persistence Market Research |

Petro China 2 Major JVs, Pipe China and CNPC Infrastructure Deals (2025)

In 2025, Petro China forged critical partnerships to consolidate its control over China’s gas infrastructure, moves that support its long-term natural gas strategy and create a foundational network for potential future large-scale CO 2 transport. These alliances with other state-owned giants underscore a coordinated national strategy to manage the energy transition.

- The $3.6 billion joint venture with Pipe China in November 2025 creates a powerful alliance to develop and operate crucial gas storage infrastructure, essential for both energy security and a potential future hydrogen or CO 2 economy.

- The proposed $5.59 billion asset acquisition from parent company CNPC is an internal consolidation that streamlines operations and places strategic storage assets directly under Petro China‘s control.

- In September 2025, Petro China International, its trading arm, signed multiple cooperation agreements for Liquefied Natural Gas (LNG) at the Gastech 2025 conference, reinforcing its global position in the gas market.

- These domestic partnerships are complemented by an opening for foreign collaboration, as evidenced by Aramco‘s announcement in December 2025 of its focus on expanding investment in China’s low-carbon energy solutions.

Natural Gas Production Shows Consistent Growth

The section discusses major joint ventures and infrastructure deals with entities like Pipe China. The chart showing consistent growth in natural gas production illustrates the strategic importance and successful outcome of such deals in securing and increasing supply.

(Source: Panda Perspectives – Substack)

China Onshore vs Offshore, Petro China CCUS Geographic Focus

China is the exclusive geographic focus for Petro China‘s major CCUS activities in 2025, with a clear strategic split between its onshore EOR projects in western regions like Xinjiang and the emerging offshore dedicated storage sites being developed by competitors along the coast. This geographic divergence reflects different regional resource availabilities and strategic priorities.

- Petro China‘s flagship CCUS activities are concentrated at its mature onshore oilfields, particularly the Xinjiang Oilfield in Northwest China, where depleted reservoirs are ideal for EOR and storage.

- The infrastructure investments made in 2025, such as the acquisition of gas storage facilities in Xinjiang and Liaohe, further entrench Petro China‘s operational footprint in these established onshore energy hubs.

- This onshore focus contrasts sharply with CNOOC’s pioneering move into offshore CCS with the Enping 15-1 project, located in the Pearl River Mouth Basin of the South China Sea, close to the dense industrial clusters of the Pearl River Delta.

- The geographic split is significant: Petro China‘s model links inland industrial CO 2 sources to inland oilfields, while CNOOC‘s model targets coastal emissions sources for permanent sub-seabed sequestration, representing two distinct and parallel pathways for China’s national decarbonization effort.

PetroChina’s Carbon Offset Strategy Profiled

This section analyzes the geographic focus of Petro China’s CCUS projects, comparing onshore and offshore potential. A chart profiling the company’s broader carbon offset strategy provides the high-level context that informs these specific geographic decisions.

(Source: Nature)

CCUS Commercial Scale, Petro China EOR vs. Sequestration Viability

In 2025, Petro China demonstrated that CCUS for enhanced oil recovery (EOR) is commercially operational at a megaton scale in China, while dedicated CO 2 sequestration, particularly offshore, advanced to a proven commercial phase but at a smaller initial scale. The technology for capture is mature; the primary differentiator is the economic model for utilization or storage.

- Between 2021-2024, Petro China was scaling its CCUS-EOR projects; in 2025, the Xinjiang Oilfield project’s success in injecting over 1 million tons of CO 2 validated the commercial maturity and scalability of the EOR-centric model.

- The successful operation of post-combustion capture technology at the industrial plants supplying CO 2 to the Xinjiang project confirms its readiness for large-scale deployment within China’s industrial sector.

- CNOOC’s Enping 15-1 project, which began operations in May 2025, proved that dedicated offshore sequestration is now technically viable in China, moving it from pilot to commercial status, albeit with an initial capacity of around 0.1-0.3 Mtpa.

- The key barrier to wider adoption of non-EOR CCUS is not the capture technology itself but the absence of a robust business case and the lack of dedicated midstream infrastructure for CO 2 transport and permanent storage, a gap Petro China‘s gas infrastructure investments may eventually help fill.

China’s CCUS Strategy Shifts to Dedicated Storage

The section compares the commercial viability of EOR versus sequestration for CCUS. The chart’s headline, ‘China’s CCUS Strategy Shifts to Dedicated Storage,’ directly supports this theme by indicating a strategic move towards sequestration, which is a central point in the viability debate.

(Source: Petroleum Exploration and Development)

SWOT Analysis, Petro China CCUS Strategy and Market Position

Petro China‘s 2025 CCUS strategy leverages its vast existing infrastructure and EOR expertise as a key strength but faces threats from evolving regulations and competing sequestration models that could render its EOR-centric approach insufficient in the long term. The company is positioned as an operational leader in onshore CCUS but a strategic follower in the broader energy transition.

PetroChina Dominates Market with 40% Share

The section provides a SWOT analysis of Petro China’s CCUS strategy and its market position. The chart, which shows Petro China’s dominant market share, directly quantifies a key ‘Strength’ for this analysis.

(Source: Panda Perspectives – Substack)

Table: SWOT Analysis for Petro China CCUS Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strength | Possessed a large portfolio of mature oilfields and existing infrastructure suitable for CCUS-EOR. | Leveraged over 1, 000 depleted reservoirs and acquired $5.59 B in gas storage assets, repurposing them for CO 2 management and EOR. | The strategy of using existing assets for CCUS was validated at scale, with the Xinjiang project injecting 1 million tons of CO 2 in a year. |

| Weakness | Low stated investment in new energy relative to total capital expenditure. Public commitment to transition was not yet backed by large-scale spending. | Direct investment in low-carbon projects remained low at only 1-2% of total CAPEX. Over $9 billion was committed to natural gas infrastructure. | The 2025 investment strategy confirmed a continued prioritization of fossil fuels (natural gas) over a rapid pivot to renewables or dedicated CCS. |

| Opportunity | China’s national Emissions Trading System (ETS) was established but focused only on the power sector, offering limited incentive for industrial CCUS. | The ETS expanded to include heavy industries like steel and cement. Petro China‘s trading arm handled over 16 million metric tons of CO 2 equivalent. | The expanding ETS created a tangible market mechanism. Petro China validated its ability to operate as a sophisticated player in this market, monetizing carbon reductions. |

| Threat | Competitors were exploring different CCUS models, but none were operational at scale in China. | CNOOC successfully launched China’s first offshore CCS project (Enping 15-1), creating a viable alternative to Petro China‘s EOR-focused model. | A competing, non-EOR business model for carbon management was proven commercially viable in China, threatening to capture the market for pure-play industrial decarbonization. |

Petro China 2026 Outlook, ETS Expansion and CNOOC Competition

If China’s Emissions Trading System (ETS) expands to include the oil and gas sector and the carbon price strengthens, watch for Petro China to announce its first large-scale, non-EOR dedicated sequestration project to compete with CNOOC‘s proven offshore model. The company has the operational capacity and asset base to pivot; the trigger will be policy-driven economics.

- If this happens: The expansion of China’s national ETS to steel and cement in late 2025 is a clear precursor. A rising carbon price, driven by stricter national climate targets, would directly challenge the economics of emitting and create a stronger business case for permanent sequestration over EOR.

- Watch this: Monitor Petro China for Final Investment Decisions (FIDs) on new projects in the 0.5-1.0 Mtpa range. The key indicator will be whether their primary purpose is stated as dedicated geological storage rather than enhanced oil recovery.

- This could be happening: CNOOC‘s successful operation of the Enping 15-1 offshore project in 2025 provides a clear competitive benchmark and a proven service model that industrial emitters may prefer. This external pressure may force Petro China to diversify its CCUS portfolio to avoid being locked into a declining EOR-dependent market.

Carbon Emissions Market to Exceed $6.2T by 2034

This section discusses the 2026 outlook, including the expansion of the Emissions Trading Scheme (ETS). The chart’s forecast for the growth of the carbon emissions market provides direct quantitative support for the significance of the ETS expansion.

(Source: Dimension Market Research)

The questions your competitors are already asking

This report covers one angle of PetroChina’s commercial strategy for large-scale CCUS deployment. The questions that matter most depend on your work.

- Which companies are gaining ground in China’s CCUS market: PetroChina with its onshore EOR model or CNOOC with its offshore sequestration model?

- How does PetroChina’s onshore CCUS-EOR compare to CNOOC’s offshore dedicated sequestration for scalability and economic returns in the Chinese market?

- PetroChina investments and funding. Is the company on track to reach its 4 million ton national CCUS volume target by the end of 2025?

- What is the outlook for CCUS-EOR deployment across China’s other mature onshore oilfields beyond the Xinjiang project?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.