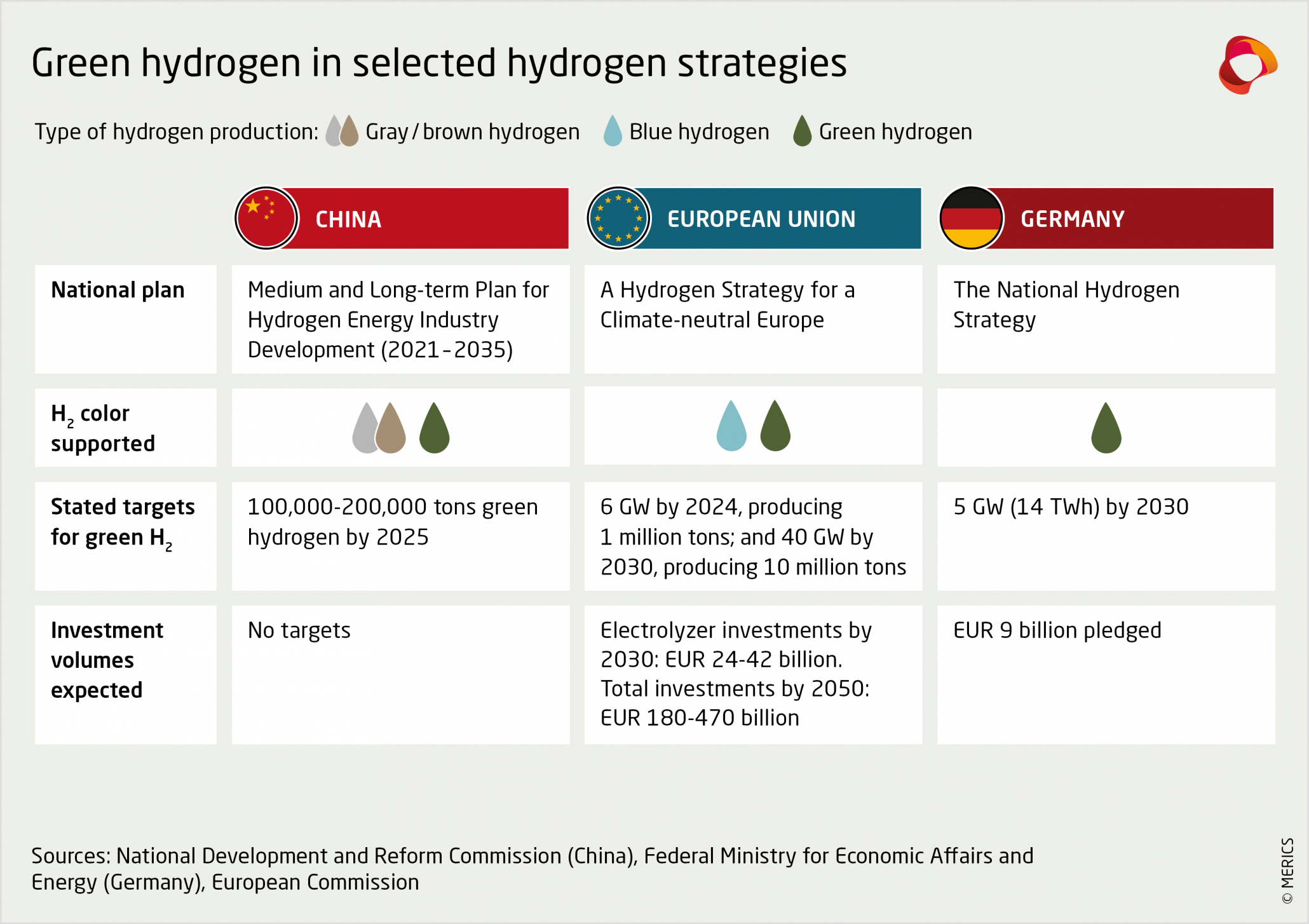

Green Hydrogen in China, Petro China’s 8, 100 Ton Capacity, 221 B Yuan National Investment, and 500+ Projects (2021-2025)

Petro China Green Hydrogen Projects vs. China’s 200, 000 Ton National Scale

In 2025, Petro China adopted a cautious “fast follower” strategy in green hydrogen, focusing on internal use and leveraging existing assets, which contrasts sharply with the explosive, policy-driven national ramp-up that saw China’s total green hydrogen capacity surpass its official 2025 targets.

- Between 2021 and 2024, state-owned energy firms began laying the groundwork for hydrogen, but 2025 marked a significant acceleration, with over 500 new hydrogen projects launched nationally, representing a total investment of 221 billion yuan.

- By December 2025, China’s national green hydrogen production capacity exceeded 200, 000 tonnes per year, surpassing the high-end of its 2025 target and demonstrating the market’s rapid maturation.

- Petro China’s primary contribution in 2025 was an increase in its high-purity hydrogen production capacity to 8, 100 tons, a notable internal increase but a small fraction of the national total, indicating a strategy to de-risk its entry rather than lead the market.

- Competitors like SINOPEC took a more aggressive public stance, promoting flagship demonstration projects to integrate green hydrogen directly into the petrochemical industry, signaling a more urgent push for large-scale deployment.

China’s National Green Hydrogen Targets for 2025

The section discusses Petro China’s projects in the context of China’s ‘200,000 Ton National Scale.’ This chart directly visualizes the national target, providing the necessary benchmark to understand the scale and ambition of the projects mentioned in the section.

$221 B National Investment, Petro China’s Balanced Capital Allocation in 2025

While China’s hydrogen sector saw over 221 billion yuan in new project investments in 2025, Petro China maintained a balanced capital allocation strategy, simultaneously funding its initial green hydrogen capacity while committing billions to traditional petrochemical complexes.

- The surge in national investment was driven by China’s “dual-carbon” goals and anticipation of strong policy support in the upcoming 15 th Five-Year Plan (2026-2030).

- Petro China’s parent, CNPC, reported a tangible outcome from its sustainable energy redirection, increasing its high-purity hydrogen output by 136.3% year-over-year from a capacity of 8, 100 tons.

- This green investment competes for capital with legacy operations, evidenced by Petro China’s concurrent investment of a combined $8.9 billion in two new olefin-based chemical complexes in Jilin and Guangxi during 2025.

- To prepare for commercialization, Petro China International established dedicated global carbon and power trading teams, a strategic investment in the capabilities needed to monetize future low-carbon products.

China’s Renewable Hydrogen Capacity Forecast to Surge

The section focuses on the ‘$221 B National Investment’ and its impact. This forecast chart, showing a surge in renewable hydrogen capacity, is the direct visual consequence of such a massive investment, illustrating the expected outcome of the capital allocation.

(Source: Rystad Energy)

Table: Petro China Green vs. Traditional Investments (2025)

| Entity / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| China National Hydrogen Sector | 2025 | Over 500 new projects launched with a total investment of 221 billion yuan, driven by national decarbonization policies. | Energy Connects |

| Petro China (CNPC) High-Purity Hydrogen | 2025 | Achieved an annual production capacity of 8, 100 tons, with output increasing 136.3% Yo Y. Serves internal decarbonization needs and builds operational experience. | CNPC CSR Report |

| Petro China Jilin & Guangxi Olefin Complexes | 2025 | Invested $4.7 billion and $4.2 billion respectively in two major petrochemical projects, highlighting continued capital allocation to fossil-fuel-based infrastructure. | C&EN |

Refining Market Shows Shift to Green Hydrogen

This section’s heading indicates a table comparing ‘Green vs. Traditional Investments.’ The chart perfectly complements this by illustrating the market dynamic driving this investment shift—the move away from traditional refining towards green hydrogen as a decarbonization solution.

(Source: Global Market Insights)

Petro China’s Commercial Projects Amidst SINOPEC’s Flagship Deployments

Petro China’s main commercial activity in 2025 was the operational expansion of its own hydrogen production for internal use, a strategy that differs from competitor SINOPEC, which focused on flagship projects aimed at broader industrial decarbonization.

- Petro China’s 8, 100-ton capacity primarily serves its own operations, a model that mitigates offtake risk but limits its immediate impact on the wider merchant hydrogen market.

- In comparison, SINOPEC has been actively developing large-scale green hydrogen projects to supply its refineries and establish a more visible market leadership position.

- The national context is defined by provincial-level efforts, with regions like Inner Mongolia and Shandong already producing over 4 million tons of hydrogen annually, although this is predominantly grey hydrogen from fossil fuels.

- Petro China’s strategy appears to be building foundational experience before committing to large, external-facing commercial projects, allowing the market and infrastructure to mature first.

Table: China Hydrogen Project Comparison (2025)

| Company / Region | Project / Metric | Capacity / Scale | Strategic Purpose | Source |

|---|---|---|---|---|

| China (National) | Total Installed Green H 2 Capacity | >200, 000 tons/year | Exceeded national 2025 target, driven by policy and state-owned enterprise investment. | Hydrogen Insight |

| Petro China (CNPC) | High-Purity Hydrogen Production | 8, 100 tons/year | Internal use for decarbonization; a cautious, de-risked market entry. | CNPC CSR Report |

| SINOPEC | Flagship Demonstration Projects | Not specified | Actively integrating green hydrogen into the petrochemical industry to establish market leadership. | Sci Open |

China’s Green Hydrogen Players and Projects Mapped

The section heading is ‘Table: China Hydrogen Project Comparison.’ A map showing the key players and project locations across the country is an excellent visual tool to introduce and summarize the data that would be detailed in such a comparison table.

China’s West-to-East Divide, Petro China’s Production and Transport Challenge

China’s green hydrogen economy in 2025 is defined by a significant geographic mismatch, with large-scale production potential concentrated in the renewable-rich western and northern regions, while major industrial demand centers are located on the eastern coast, creating a critical midstream infrastructure bottleneck.

- From 2021-2024, project planning was localized, but by 2025, the national strategy clearly emerged to leverage abundant solar and wind resources in regions like Inner Mongolia, Xinjiang, and Gansu for electrolysis-based production.

- Petro China’s own focus aligns with this, with projects like the Yumen Oilfield renewable power-to-gas initiative situated in the resource-rich west.

- The primary constraint that became evident in 2025 is the lack of long-distance, high-capacity hydrogen pipelines to transport the produced gas to coastal industrial provinces, a challenge that requires massive state-level investment.

- This transportation gap limits the commercial viability of large-scale western projects and forces them to rely on local consumption or more expensive truck-based transport, hindering national decarbonization efforts.

Operational LNG Terminals to Reach 9 by 2027

This section discusses China’s ‘West-to-East Divide’ and the associated ‘Production and Transport Challenge.’ This chart on LNG terminal expansion directly addresses the theme of energy transport infrastructure, which is crucial for bridging geographical production and consumption gaps.

(Source: Panda Perspectives – Substack)

SWOT Analysis: Petro China’s Green Hydrogen Position in 2025

Petro China’s 2025 position in green hydrogen is characterized by the strength of its existing infrastructure and state backing, offset by the weakness of its cautious strategy compared to the market’s rapid pace, presenting both a massive policy-driven opportunity and a threat from more agile competitors.

PetroChina Navigates Five Key Risk Categories

A SWOT Analysis involves evaluating Strengths, Weaknesses, Opportunities, and Threats. This chart, which details ‘Five Key Risk Categories,’ directly corresponds to the ‘Weaknesses’ and ‘Threats’ components of a SWOT, making it a perfect visual aid for the analysis.

(Source: Stone Research)

Table: SWOT Analysis for Petro China’s Green Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Vast natural gas pipeline network and infrastructure. Strong balance sheet and status as a National Oil Company. | Leveraging existing assets and expertise for a low-risk entry. Established new carbon and power trading teams. | The 2025 strategy confirmed Petro China is using its incumbent advantages to manage its transition, rather than pursuing a high-risk, first-mover approach. |

| Weaknesses | Heavy reliance on fossil fuel revenue. Organizational inertia against rapid change. | Production capacity (8, 100 tons) is minor compared to national scale (200, 000+ tons). Adopting a “fast follower, ” not a leadership, role. | The scale of national growth in 2025 validated that Petro China is lagging behind the market’s pace and more aggressive competitors like SINOPEC. |

| Opportunities | China’s national “dual-carbon” goals create a massive, mandated market for green energy. | Anticipation of the 15 th Five-Year Plan is driving huge investment. A potential pullback in US subsidies could give China a lead. | The explosive 221 billion yuan investment in 2025 validated the immense market opportunity, making Petro China’s participation a strategic necessity. |

| Threats | Technical and cost challenges of green hydrogen. Emergence of new, specialized energy players. | Critical domestic technology bottlenecks in electrolyzer efficiency and high-pressure storage. A major midstream infrastructure gap. | The rapid buildout in 2025 confirmed that infrastructure and supply chain maturity are now the primary threats to scaling, not just initial production cost. |

PetroChina Gas Storage Capacity Expands Steadily

This section is a table detailing a SWOT analysis. A key ‘Strength’ for an oil and gas major like PetroChina in the hydrogen economy is its existing infrastructure. This chart, showing expanding gas storage capacity (which can be repurposed for hydrogen), perfectly illustrates a core strength that would be listed in the SWOT table.

(Source: Panda Perspectives – Substack)

Petro China’s Next Move: The 15 th Five-Year Plan Will Force Scale-Up

The most critical catalyst for Petro China’s green hydrogen strategy is the forthcoming 15 th Five-Year Plan (2026-2030), which is expected to mandate industrial-scale hydrogen deployment, forcing the company to shift from cautious exploration to aggressive, large-scale project execution.

- If the plan sets ambitious industrial decarbonization targets using hydrogen, watch for Petro China to announce significantly larger green hydrogen projects with capacities far exceeding its current 8, 100-ton scale.

- This could be happening now: Petro China is likely using the 2025 period to finalize site selection and feasibility studies for large-scale projects in anticipation of the new policy directives.

- Watch for major investment announcements related to midstream infrastructure, particularly Petro China’s potential participation in building the national hydrogen pipeline backbone to connect western production with eastern demand.

- A key signal of this shift will be increased R&D spending or technology partnerships aimed at resolving domestic supply chain bottlenecks in electrolyzers and storage, moving beyond reliance on existing mature technology.

Timeline Shows China’s Hydrogen Policy Foundation

The section looks forward to the ’15th Five-Year Plan’ and the need to scale up. This timeline chart provides the essential historical context of China’s hydrogen policy, setting the stage for a discussion about future policy and the next strategic steps.

The questions your competitors are already asking

This report covers one angle of PetroChina’s cautious green hydrogen strategy within China’s wider market boom. The questions that matter most depend on your work.

- Which state-owned enterprises, like PetroChina and SINOPEC, are gaining or losing ground in China’s green hydrogen market?

- PetroChina’s green hydrogen investments. Is its 8,100-ton capacity scale-up on track for its internal demand targets?

- What is the outlook for green hydrogen deployment in China’s petrochemical sector beyond 2025?

- Which Chinese petrochemical operators are adopting green hydrogen for refining, and at what scale?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.