Blue Hydrogen Strategy, Saudi Aramco Slashes 77% of Target, Inks BHIG Deal, and Secures 51 US Agreements (2025)

Blue Hydrogen Pivot Signals Market-Wide Reality Check on Green Hydrogen Viability

In 2025, Saudi Aramco executed a significant strategic pivot, prioritizing commercially ready blue hydrogen over higher-cost green hydrogen, a move that reflects a broader market reality check on the economic viability of large-scale green projects. This shift from the ambitious green hydrogen rhetoric of the 2021-2024 period is defined by tangible investments in blue ammonia infrastructure, a pragmatic response to persistent high costs and uncertain international demand for green hydrogen.

- In a major course correction in March 2025, Saudi Aramco slashed its 2030 blue ammonia production target by over 77%, from 11 million tonnes per annum (mtpa) down to a more realistic 2.5 mtpa, directly citing a lack of buyer interest at current high prices.

- This contrasts with the pre-2025 period, which was dominated by announcements for giga-scale green hydrogen projects. The flagship NEOM Green Hydrogen Project, despite being 80% complete in 2025, faces significant demand risk and struggles to secure offtake agreements beyond its primary partner, Air Products.

- Saudi Aramco solidified its blue hydrogen focus by finalizing the acquisition of a 50% stake in the Blue Hydrogen Industrial Gases (BHIG) facility in Jubail, creating a clear pathway to leverage its existing natural gas feedstock and planned Carbon Capture and Storage (CCS) infrastructure.

- The economic challenge is stark, with green hydrogen production costs in 2025 ranging from $3.74 to $12.00 per kg, far from the price points needed to stimulate widespread industrial adoption and making blue hydrogen a more pragmatic near-term option.

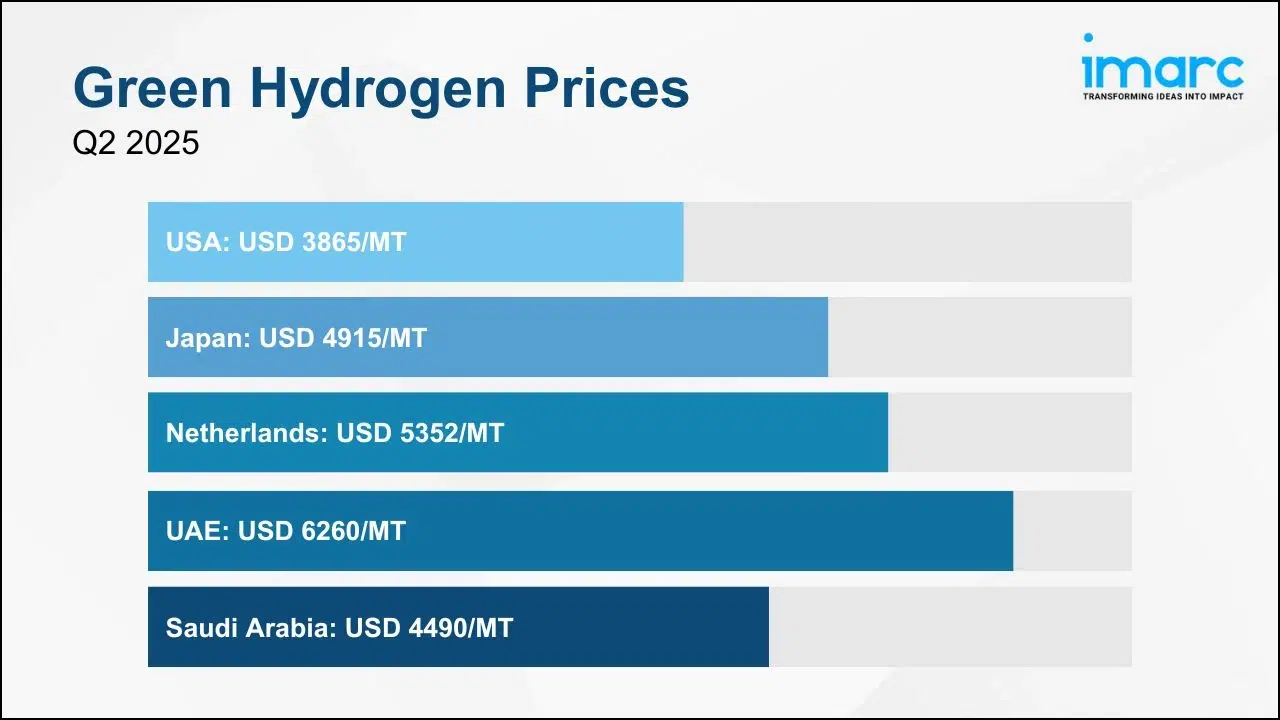

Green Hydrogen Prices Remain High in Q2 2025

The section discusses a ‘reality check’ on the viability of green hydrogen. The chart, showing that green hydrogen prices remain high, provides a direct and quantitative reason for this reality check, as cost is a primary barrier to market-wide viability.

(Source: IMARC Group)

$10 B National Program, Saudi Aramco Prioritizes Blue Hydrogen CAPEX Over Green

Saudi Aramco’s 2025 investment strategy reveals a clear prioritization of capital for scalable blue hydrogen production, while relegating green hydrogen exposure to smaller, strategic venture investments. This dual-track approach allows the company to build a tangible low-carbon business today using its core competencies, without taking on the immense financial risk of pre-commercial green hydrogen mega-projects.

- The cornerstone of Saudi Aramco’s hydrogen investment in 2025 was the acquisition of a 50% stake in the Blue Hydrogen Industrial Gases (BHIG) company, a direct capital commitment to large-scale blue ammonia production in Jubail.

- To maintain a foothold in green hydrogen technology, Aramco Ventures completed a strategic investment in electrolyzer manufacturer Hydo Tech in February 2025, gaining valuable technical insight without committing to building a large-scale green facility itself.

- These direct investments occur within the broader context of the Saudi Green Initiative’s $10 billion green hydrogen program, which primarily supports the national-level NEOM project, a separate entity from Saudi Aramco’s direct operational control.

- Saudi Aramco’s significant financial capacity, evidenced by a $5.0 billion bond issuance in May 2025, provides the flexibility to fund its capital-intensive blue hydrogen and CCS infrastructure projects.

Charts Show Saudi Arabia’s Low Renewable Capacity

The section states that Saudi Aramco is prioritizing blue hydrogen CAPEX over green. The chart, showing Saudi Arabia’s low renewable capacity, provides a fundamental, country-specific rationale for this decision. Low renewable capacity makes large-scale green hydrogen production difficult and expensive, thus favoring the blue hydrogen pathway.

(Source: ScienceDirect.com)

Table: Saudi Aramco Key Hydrogen-Related Investments (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Saudi Arabia (SGI) | Nov 11, 2025 | The national $10 billion green hydrogen program provides the overarching government support for the sector, primarily benefiting projects like NEOM. | drivinghydrogen.com |

| International Bond Issuance | May 11, 2025 | Aramco raised $5.0 billion through an international bond issuance, providing capital for general corporate purposes and enhancing financial flexibility for strategic projects like hydrogen. | aramco.com |

| Blue Hydrogen Industrial Gases (BHIG) | Mar 24, 2025 | Saudi Aramco finalized its acquisition of a 50% equity stake in BHIG to anchor its blue hydrogen and ammonia production ambitions in Jubail Industrial City. | fuelcellsworks.com |

| Hydo Tech | Feb 20, 2025 | Aramco Ventures made a strategic investment in electrolyzer manufacturer Hydo Tech to gain exposure and technical knowledge in the green hydrogen production value chain. | aramcoventures.com |

Ecosystem Strategy, Saudi Aramco Builds Alliances with Linde, Coors Tek and 51 US Firms

While scaling back its own production targets, Saudi Aramco spent 2025 actively building a global hydrogen ecosystem through strategic partnerships aimed at de-risking technology, developing the value chain, and securing future market access. This flurry of agreements shows a focus on creating the enabling conditions for a hydrogen economy rather than simply building supply.

- Saudi Aramco established key technology partnerships to address critical bottlenecks, including an agreement with Linde Engineering to develop ammonia cracking technology and a collaboration with Coors Tek on innovative ceramic membrane hydrogen generators.

- The company signed a massive slate of agreements with US firms, totaling 51 Mo Us across two major announcements in May and November 2025 with a potential value exceeding $120 billion, to deepen industrial and technological ties.

- In parallel, Saudi Aramco is strengthening relationships with key potential export markets in Asia, including South Korea, India, and Japan, by collaborating on regulations and standards to facilitate future trade.

Power Generation Dominates Saudi Green Hydrogen Market

The section discusses building an ‘Ecosystem Strategy’ through alliances. This chart, by identifying ‘Power Generation’ as the dominant end-market, shows where this ecosystem and its associated partnerships would be focused to capture the largest share of demand.

(Source: IMARC Group)

Table: Saudi Aramco 2025 Hydrogen Partnership and Alliance Data

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Various US Companies | Nov 19, 2025 | Announced 17 Mo Us and agreements with US firms with a potential value over $30 billion, building on earlier deals to enhance cross-sector collaboration. | aramco.com |

| Linde Engineering | Oct 13, 2025 | A technology agreement to jointly develop a new ammonia cracking technology, essential for converting ammonia back to hydrogen at the point of use. | oilandgasmiddleeast.com |

| Coors Tek | Oct 13, 2025 | A technology partnership to develop a scalable hydrogen generator using advanced ceramic membranes for more efficient hydrogen production. | oilandgasmiddleeast.com |

| Various US Companies | May 14, 2025 | Signed 34 Mo Us and agreements with major US companies, with a potential total value of approximately $90 billion, to foster broad industrial partnership. | aramco.com |

| Asian Partners (South Korea, India, Japan) | Jan 15, 2025 | Enhancing government and regulatory collaboration to develop standards and frameworks for future hydrogen trade, securing future offtake markets. | sciencedirect.com |

Saudi Arabia Focus, Aramco Centers Production in Jubail for Asian Export

Saudi Aramco’s geographical focus in 2025 is distinctly centered on developing domestic production hubs in Saudi Arabia with the explicit goal of servicing future demand in energy-importing Asian nations. The strategic locations of its projects are designed to leverage existing industrial infrastructure and coastal access for efficient export logistics.

- During the 2021-2024 period, discussions around Saudi hydrogen were dominated by the futuristic NEOM project on the Red Sea coast. In 2025, however, Saudi Aramco’s direct operational focus has solidified around Jubail Industrial City on the Arabian Gulf coast for its blue ammonia project.

- The choice of Jubail is strategic, as it is an established industrial hub with extensive port facilities and proximity to Saudi Aramco’s massive natural gas fields and planned CCS infrastructure.

- The company’s market development efforts in 2025 were heavily oriented towards Asia, with active engagement in South Korea, Japan, and India to establish the regulatory and commercial groundwork for future ammonia shipments.

- This geographical strategy positions Saudi Aramco to supply the first wave of low-carbon hydrogen demand, which is expected to emerge from the decarbonization efforts of heavy industries and power sectors in these key Asian economies.

Saudi Green Hydrogen Market Forecasted to Boom

The section focuses specifically on Saudi Arabia. The chart, which forecasts a boom in the Saudi green hydrogen market, provides the direct market context and potential for the geographic area discussed in the heading.

(Source: IMARC Group)

Commercial Scale Blue Hydrogen vs. Pre-Commercial Green Hydrogen

The technological maturity of blue versus green hydrogen production is the central factor driving Saudi Aramco’s strategic choices in 2025. The company is committing capital to blue hydrogen technology, which is commercially mature and scalable today, while treating green hydrogen as a longer-term prospect that still carries significant technological and economic risk.

- From 2021-2024, green hydrogen was promoted as a near-future solution. However, 2025 data confirms it remains pre-commercial at scale, evidenced by the NEOM project’s struggle to find buyers willing to pay the high cost of production, estimated between $3.74 and $12.00 per kg.

- In contrast, blue hydrogen production, which combines conventional steam methane reforming (SMR) with CCS, leverages decades of proven industrial processes. Saudi Aramco’s 2025 acquisition of a stake in the BHIG facility validates this technology’s readiness for immediate, large-scale deployment.

- Saudi Aramco’s investment in Hydo Tech and partnerships with Linde on ammonia cracking are not for immediate deployment but are strategic moves to understand and influence the development of next-generation technologies that could eventually make green hydrogen viable.

Chart: High Costs Are Key Green Hydrogen Restraint

The section contrasts commercial-scale blue hydrogen with ‘pre-commercial’ green hydrogen. The chart, stating that high costs are a key restraint, directly explains why green hydrogen is still considered pre-commercial.

(Source: Coherent Market Insights)

SWOT Analysis of Saudi Aramco Hydrogen Strategy (2025)

Saudi Aramco’s 2025 hydrogen strategy is a calculated balance of leveraging its incumbent strengths in hydrocarbon production while navigating the threats of a slow-to-materialize global hydrogen market. The pivot to blue hydrogen mitigates near-term risk but exposes the company to the long-term threat of being outpaced by falling green hydrogen costs.

- The primary strength is Saudi Aramco’s access to cheap natural gas and its world-class expertise in executing large-scale industrial projects.

- A key weakness is the continued high cost and lack of firm offtake agreements for its blue ammonia, as demonstrated by the drastic reduction of its 2030 production target.

- The main opportunity is to establish a dominant position in the blue ammonia export market before competitors, particularly by securing long-term contracts with Asian buyers.

- A significant threat is that continued rapid innovation in renewables and electrolyzers could make green hydrogen cost-competitive sooner than expected, potentially stranding Saudi Aramco’s blue hydrogen assets.

Green Hydrogen Market Forecast Shows Explosive Growth

This section is a SWOT Analysis. The chart, showing explosive market growth, would be used to illustrate the ‘Opportunity’ aspect of the SWOT. It demonstrates the significant market potential that Saudi Aramco’s hydrogen strategy aims to capture.

(Source: Fortune Business Insights)

Table: SWOT Analysis for Saudi Aramco Hydrogen Initiatives (2025)

| SWOT Category | 2021 – 2024 | 2025 to Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Announcements highlighted access to cheap solar and wind for green hydrogen. | Focus shifted to leveraging cheap natural gas feedstock, existing industrial infrastructure (Jubail), and financial power ($5 B bond). | Aramco validated that its most bankable strength is its existing hydrocarbon and project management expertise, not just renewable potential. |

| Weaknesses | The high theoretical cost of green hydrogen was a known but distant challenge. | The high cost of blue ammonia became a tangible barrier, forcing a 77% cut in the 2030 production target due to a lack of willing buyers. | The “green premium” is no longer a theoretical weakness but a market-defining commercial hurdle that directly forced a strategic retreat. |

| Opportunities | The opportunity was framed as leading the global green hydrogen export market. | The opportunity has been refined to dominate the more nascent and pragmatic blue ammonia market first by securing anchor customers in Asia (Japan, South Korea). | Aramco has validated a more focused, risk-adjusted market entry strategy, prioritizing a viable blue market over a speculative green one. |

| Threats | The primary threat was seen as other countries developing green hydrogen capacity faster. | The immediate threat is a complete lack of market demand at the required price point for any color of low-carbon hydrogen, risking project unviability. | The threat shifted from competition to a fundamental lack of bankable demand, a much more immediate and existential risk for current projects. |

Offtake Agreements are the Key Signal for Saudi Aramco’s Hydrogen Future

The single most critical development to watch for Saudi Aramco’s hydrogen strategy is the signing of a binding, long-term offtake agreement for its blue ammonia. If Saudi Aramco can secure a major contract for its planned 2.5 mtpa capacity, it will validate its entire blue hydrogen pivot and send a powerful signal that a commercial market for low-carbon hydrogen is finally emerging.

- If this happens, watch for Saudi Aramco to potentially revise its production targets upward again and accelerate development at the Jubail facility. A successful deal would provide a bankable template for future projects.

- The key signal to monitor is any announcement of a firm sales contract with a major utility or industrial player in Japan, South Korea, or Europe. This would be a significant step beyond the non-binding Mo Us signed to date.

- If no major offtake agreements materialize by the time the NEOM green hydrogen project starts operations in 2026, it could indicate a systemic failure in market demand, forcing Saudi Aramco and the Kingdom to re-evaluate their entire hydrogen export strategy.

- The implementation of carbon pricing mechanisms like the EU’s Carbon Border Adjustment Mechanism (CBAM) in 2026 could be the catalyst that finally makes Saudi Aramco’s low-carbon products economically attractive to international buyers.

Green Hydrogen Market to Near $200B by 2035

The section highlights the importance of offtake agreements. This chart quantifies the future market size, showing the significant revenue potential at stake. Offtake agreements are the mechanism to secure a piece of this large future market, making the chart highly relevant context.

(Source: Evolvance Market Research)

The questions your competitors are already asking

This report covers one angle of Saudi Aramco’s hydrogen commercialization strategy. The questions that matter most depend on your work.

- What is actually happening with the NEOM Green Hydrogen Project? Is it securing offtake agreements beyond Air Products?

- Saudi Aramco’s hydrogen investments. Is the revised 2.5 mtpa blue ammonia target for 2030 achievable given market conditions?

- How does blue hydrogen compare to green hydrogen on commercial readiness and cost for large-scale industrial projects in 2025?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.