SLB CCUS Enablement, Sequestri Launch, John Cockerill & Shell Deals, and $22 B Project Cancellations (2025)

Hydrogen Enablement, SLB Sequestri Launch and 2 Major Partnerships

In 2025, SLB pivoted to become a critical technology enabler for the hydrogen market, strategically avoiding direct production risks amid widespread project cancellations and focusing instead on high-value services like carbon capture and digital solutions. As the clean energy sector faced significant headwinds, including over $22 billion in canceled projects during the first half of the year, SLB leveraged its core competencies to de-risk hydrogen development for other operators rather than compete with them.

- In a market grappling with high green hydrogen production costs of $4 to $12 per kilogram, SLB‘s primary move was the June 16, 2025, launch of its Sequestri Carbon Capture and Storage (CCS) platform. This end-to-end solution directly addresses a major bottleneck for blue hydrogen projects, providing a scalable and reliable pathway for CO 2 sequestration and leveraging SLB‘s extensive subsurface expertise.

- The company reinforced its technology-first approach through key collaborations. A partnership with John Cockerill Hydrogen announced on March 4, 2025, aims to develop advanced low-carbon hydrogen production technologies, positioning SLB as a supplier of critical systems.

- Further strengthening its digital enablement strategy, SLB signed a strategic agreement with Shell on December 11, 2025, to co-develop AI-driven solutions. This collaboration is designed to enhance operational efficiency for complex new energy systems, including integrated hydrogen and CCS facilities.

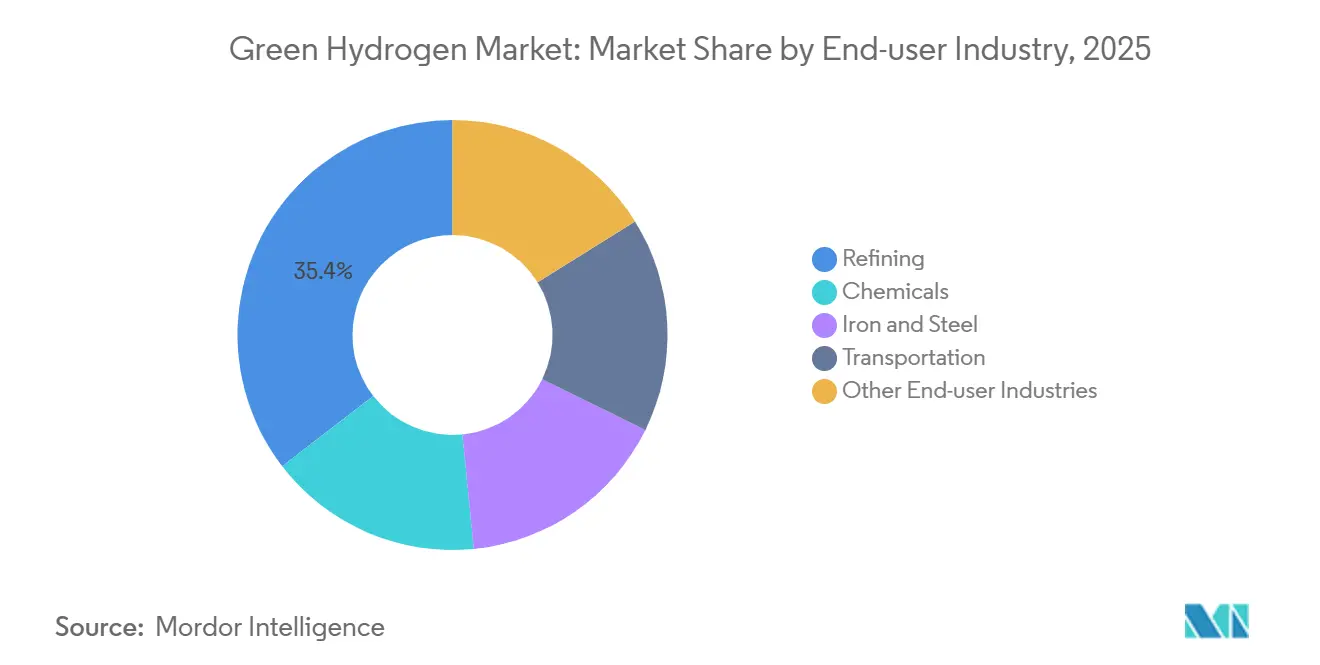

Refining Dominates 2025 Green Hydrogen Market

This chart’s focus on the refining sector as the dominant end-market for green hydrogen in 2025 directly informs the partnership strategy mentioned in the section heading. It provides a clear rationale for SLB to target and collaborate with refineries to advance its ‘Hydrogen Enablement’ goals.

(Source: Mordor Intelligence)

SLB New Energy Investments and Champion X Acquisition (2025)

SLB‘s 2025 investment strategy prioritized acquiring foundational technologies and building its service portfolio over taking direct equity in production projects. This approach was highlighted by a major acquisition designed to bolster its technical capabilities for the broader energy sector, including processes critical to blue hydrogen production.

- The definitive agreement to acquire Champion X, announced on February 25, 2025, represented a significant capital allocation. While not a pure-play hydrogen investment, the acquisition enhances SLB’s portfolio of production chemistry and artificial lift technologies, which are directly relevant for optimizing the efficiency of natural gas feedstock production for blue hydrogen.

- The company’s March 4, 2025, announcement on its commitment to driving the New Energy business forward signaled a strategic focus of internal R&D and capital resources. The emphasis was on developing technology systems for low-carbon hydrogen and other new energy verticals, underscoring a disciplined investment approach centered on technology ownership rather than asset ownership.

PEM and Alkaline Electrolyzers Lead 2025 Market

A chart detailing the leading electrolyzer technologies for 2025 provides critical context for a section about SLB’s new energy investments and acquisitions. This data helps justify strategic moves, including the Champion X acquisition and investments in electrolyzer technology ventures like Genvia.

(Source: Precedence Research)

Table: SLB Strategic Investments & Acquisitions

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Champion X | Feb 2025 | SLB reached a definitive agreement to acquire Champion X, a move designed to strengthen its production and recovery technology portfolio. This enhances capabilities in production chemistry, which can improve efficiencies in feedstock production for blue hydrogen. | SLB |

2 Key Deals, SLB Hydrogen and CCS Technology Partnerships

In 2025, SLB solidified its technology-led strategy through targeted collaborations with industry leaders Shell and John Cockerill Hydrogen to accelerate development in digital solutions and hydrogen production technology, respectively.

- The December 11, 2025, strategic collaboration with Shell focuses on developing and deploying AI-driven digital solutions. The partnership aims to improve efficiency and performance across the energy value chain, with a specific application toward optimizing complex and integrated new energy systems like hydrogen and CCS.

- SLB’s collaboration with John Cockerill Hydrogen, highlighted in a March 4, 2025, update, is centered on developing solutions for low-carbon hydrogen production. This partnership allows SLB to contribute its expertise in scaling industrial technologies without taking on the direct risks of hydrogen production and sales.

Table: SLB New Energy Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Shell plc | Dec 2025 | To jointly develop AI-driven digital solutions for the energy industry, aimed at improving efficiency and performance across the value chain, including new energy systems. | Yahoo Finance |

| John Cockerill Hydrogen | Mar 2025 | Collaboration to develop and accelerate the adoption of solutions for low-carbon hydrogen production, leveraging technology to build out the enabling ecosystem. | SLB |

Global Rollout, SLB New Energy Technology System Strategy

SLB‘s 2025 hydrogen strategy is geographically agnostic by design, focusing on creating globally applicable technology platforms like Sequestri rather than investing in region-specific production assets.

- The launch of the Sequestri CCS platform in June 2025 is a global initiative, designed to leverage SLB‘s worldwide subsurface expertise to support blue hydrogen and industrial decarbonization projects in any region with suitable geological storage formations.

- Unlike the pre-2025 period where regional hydrogen hubs were the primary focus for many project developers, SLB‘s 2025 partnerships with global players like Shell and John Cockerill Hydrogen aim to create technology standards and solutions that can be deployed internationally.

- Market data from 2025 indicates that Asia Pacific is set to capture a dominant share (47.40%) of the green hydrogen market. This suggests that while SLB‘s technology offerings are global, the initial commercial traction for its enabling solutions will likely follow these high-growth regions.

Asia Pacific Leads 2025 Green Hydrogen Market

For a section on ‘Global Rollout’ and strategy, a chart identifying the leading geographic market is essential. Highlighting Asia Pacific’s leadership in 2025 helps to explain and justify the regional focus of SLB’s new energy technology system strategy.

(Source: Precedence Research)

CCS Commercialization, SLB Sequestri Platform Launch

In 2025, SLB advanced its technology from development to commercial deployment with the launch of its Sequestri CCS business, signaling that carbon storage has matured enough for a standardized and scalable business model.

- The transition is marked by the June 16, 2025, introduction of Sequestri, which moves Carbon Capture and Storage from bespoke engineering projects to a full-value-chain, productized solution. This shift contrasts with the more fragmented, pilot-focused approach that characterized the market before 2025.

- While CCS technology reached commercial readiness, SLB‘s work with John Cockerill Hydrogen on production technology and its historical involvement with Genvia on solid oxide electrolyzers remain in the technology development and acceleration phase. This work directly addresses the high cost of green hydrogen, which remains a primary barrier to its broad commercial adoption.

- The collaboration with Shell on AI solutions validates that digital technology is now a mature and critical component for optimizing the performance and de-risking the development of complex new energy systems.

Captive Hydrogen Market to Reach $189.9B by 2030

This chart is highly relevant as the ‘Captive Hydrogen Market’ consists of large industrial facilities that are the primary customers for CCS. The growth in this market directly correlates with the opportunity for CCS commercialization, justifying the launch of SLB’s Sequestri platform.

(Source: MarketsandMarkets)

SWOT Analysis, SLB Green Hydrogen Strategy and Market Position

SLB‘s 2025 SWOT profile reflects a strategic pivot, leveraging its core subsurface and project management strengths to exploit the growing decarbonization market while mitigating the financial risks associated with nascent green hydrogen production.

- Strengths are rooted in decades of subsurface expertise and global project execution capabilities, now repurposed for CCS through the Sequestri platform and de-risking hydrogen projects for clients.

- Weaknesses include a continued reliance on partners like John Cockerill Hydrogen for core hydrogen production technology and the fact that its blue hydrogen enablement strategy remains exposed to natural gas price volatility and policy uncertainty around CCS.

- Opportunities lie in establishing Sequestri as the industry standard for CCS, making SLB an indispensable partner for nearly all large-scale industrial decarbonization and blue hydrogen projects globally.

- Threats include the possibility that persistently high green hydrogen costs and financing difficulties could stall the entire market, reducing demand for enabling technologies. Additionally, other major industrial and service companies are competing to offer similar integrated CCS solutions.

Green Hydrogen Market to Exceed $230B by 2035

This large-scale market forecast directly supports the ‘SWOT Analysis’ by defining the ‘Opportunity’ available to SLB. It quantifies the potential market size, which is fundamental to evaluating SLB’s green hydrogen strategy and its overall market position.

(Source: Precedence Research)

Table: SWOT Analysis for SLB Hydrogen Enablement Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Deep subsurface and oilfield service expertise; global operational footprint. | Leveraged core expertise to launch Sequestri CCS platform; established digital partnerships (Shell). | The strategy to repurpose legacy strengths for the energy transition was validated with a concrete, commercial offering for CCS. |

| Weaknesses | Limited track record in new energy ventures; perceived as an oil & gas company. | Reliance on partners (John Cockerill Hydrogen) for hydrogen production technology; New Energy is still a small part of overall revenue. | The “buy and partner” strategy for technology gaps was confirmed, acknowledging it does not own all required expertise in-house. |

| Opportunities | Emerging markets for decarbonization, hydrogen, and CCS. | Capitalized on market need for CCS by launching Sequestri; positioned as a technology enabler amid market volatility. | The market’s struggle with project execution and financing validated SLB‘s decision to provide de-risking services instead of becoming a producer. |

| Threats | Policy uncertainty; high cost of new energy technologies; competition. | Market instability with $22 B in clean energy project cancellations; high cost of green hydrogen ($4-$12/kg) threatening demand. | The threat of market collapse due to high costs became a tangible reality in 2025, validating SLB‘s lower-risk, service-oriented approach. |

SLB 2026 Outlook, Sequestri Adoption and Genvia Milestones

The primary indicator for the success of SLB‘s hydrogen strategy in 2026 will be the commercial adoption of its Sequestri platform, with the first major contracts serving as tangible validation of its blue hydrogen enablement model.

- If SLB announces one or more large-scale, multi-year contracts for the Sequestri platform, watch for an acceleration of Final Investment Decisions (FIDs) on blue hydrogen projects that were previously stalled by CCS uncertainty and complexity.

- This could be happening if SLB‘s quarterly earnings reports in late 2025 and early 2026 show significant revenue growth in the New Energy division, with specific attribution to the new CCS business line.

- If tangible technology milestones or pilot project results emerge from the partnerships with Shell or John Cockerill Hydrogen, watch for SLB to begin marketing integrated service packages that combine digital optimization with hydrogen production hardware.

- This could be happening if SLB makes further bolt-on acquisitions of smaller technology companies that complement its digital, chemical, or electrolyzer development tracks, signaling a move to consolidate and own a larger portion of its technology stack.

Green Hydrogen Cost Competitiveness Forecast to 2049

A long-term cost competitiveness forecast provides the strategic vision for the ‘2026 Outlook’. It shows the end-goal that ‘Genvia Milestones’ are designed to achieve, linking near-term technological progress to the long-term viability and profitability of green hydrogen.

(Source: ScienceDirect.com)

The questions your competitors are already asking

This report covers one angle of SLB’s pivot to a technology-enabling role in the hydrogen market. The questions that matter most depend on your work.

- How is SLB’s technology-enabler strategy performing amid widespread hydrogen project cancellations?

- Which hydrogen project operators are adopting SLB’s Sequestri CCS platform to de-risk blue hydrogen development?

- SLB’s activities in new energy. Are the partnerships with John Cockerill and Shell progressing from announcements to commercial offerings?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.