Doosan Fuel Cell SOFC Development, 350 MW EET Hydrogen Project, LG Partnership, and 450, 000 Ene-Farm Units (2021 to 2026)

SOFC Commercial Projects, Three Divergent Regional Models Emerge

The Solid Oxide Fuel Cell (SOFC) market for Combined Heat and Power (CHP) is not advancing uniformly; instead, it is fragmenting into three distinct regional growth models dictated by local policy and economic drivers. Between 2021 and 2024, the market was largely defined by Japan’s subsidy-driven residential success. However, from 2025 onward, a clear divergence is apparent: Japan remains the mature anchor for residential systems, South Korea is aggressively targeting large-scale industrial power, and Europe is cultivating a policy-led market for commercial and industrial decarbonization.

- In Japan, the Ene-Farm program established a stable foundation, deploying over 400, 000 residential fuel cell units by 2024 and growing to over 450, 000 units by 2026. This created a mature, albeit subsidized, consumer market and a sophisticated manufacturing base led by firms like Mitsubishi Heavy Industries.

- South Korea’s strategy, backed by a national hydrogen roadmap, shifted focus towards larger systems for grid stability and industrial use. This includes developing micro-CHP units in partnership with firms like LG Electronics, with a focus on cost reduction through large-scale manufacturing.

- Europe’s market, framed by the EU Green Deal and Energy Efficiency Directive, is driven by commercial and industrial applications. Activity is concentrated in projects for hard-to-abate sectors, exemplified by EET Hydrogen’s planned 350 MW blue hydrogen facility, which uses a CHP plant to anchor offtake and targets a final investment decision in late 2026.

- New applications emerging after 2024 validate the technology’s versatility beyond traditional CHP. These include behind-the-meter power for data centers to bypass grid constraints and pilot projects for maritime decarbonization, where fuel-flexible SOFCs are seen as a viable path to meet stringent emissions targets.

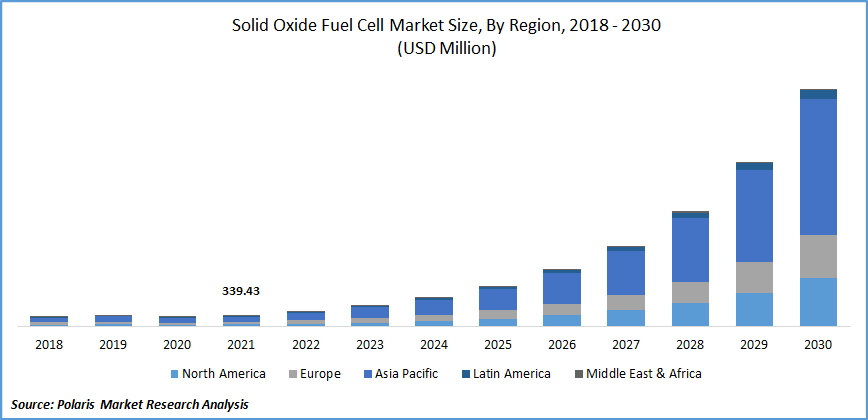

Asia-Pacific to Dominate Future SOFC Growth

This chart visually supports the section’s claim of divergent regional models by showing the Asia-Pacific region, which includes Japan and South Korea, as the primary driver of market growth.

(Source: Polaris Market Research)

Over $3 B Market in 2026, Government Funding Remains a Critical Enabler

Investment in the SOFC market is directly correlated with government policy, with public funding mechanisms and subsidies serving as the primary drivers of growth and de-risking capital for manufacturers and adopters. The global market is projected to reach between $2.9 billion and $3.2 billion in 2026, with growth heavily concentrated in regions offering strong regulatory support. This dependence on policy creates a landscape where investment flows follow government commitment, rather than purely market-based economics.

SOFC Market Projected to Hit $2.89B in 2026

This forecast directly validates the article’s projection of a market between $2.9 and $3.2 billion in 2026, sourcing data from Mordor Intelligence, which is cited in the report.

(Source: Mordor Intelligence)

- The Asia-Pacific region commands the largest market share due to sustained government backing. Japan’s Ene-Farm program has been the most significant global driver, creating the world’s largest residential fuel cell market.

- South Korea accelerated its investment with a national hydrogen roadmap supported by a KRW 500 billion (approximately $360 million) fund dedicated to fostering a domestic supply chain for hydrogen and fuel cell technologies.

- In Europe, investment is channeled through programs like the Clean Hydrogen Joint Undertaking, which funds innovation and deployment to help meet decarbonization goals. The EU’s Energy Efficiency Directive also creates a regulatory incentive for new thermal power installations over 20 MW to consider high-efficiency CHP.

- While not a direct focus of this report, the U.S. Inflation Reduction Act (IRA) acts as a powerful global catalyst, providing significant tax credits that stimulate worldwide manufacturing scale-up and cost-reduction efforts, indirectly benefiting projects in Europe and Asia.

Table: SOFC Market Size and Growth Forecasts

| Forecast Provider | 2026 Market Size ($B) | Forecast Value & Year | CAGR (%) | Source |

|---|---|---|---|---|

| Mordor Intelligence | $2.89 B | $16.53 B by 2031 | 41.73% | Mordor Intelligence |

| Roots Analysis | $3.19 B | $143.66 B by 2040 | 31.25% | Roots Analysis |

| Fortune Business Insights | N/A | $5.97 B by 2034 (Stationary) | 13.94% | Fortune Business Insights |

| Verified Market Research | N/A | $12.5 B by 2032 | 21.1% | Verified Market Research |

Doosan Fuel Cell Key Alliances Target Cost and Scale (2021 to 2026)

Strategic partnerships are the primary mechanism for SOFC developers to address the twin challenges of high upfront cost and manufacturing scale, with recent collaborations aimed at both technology improvement and market creation. These alliances connect technology specialists with industrial giants capable of system integration and mass production. This collaborative approach is critical for moving SOFC technology from subsidized niches into commercially viable, large-scale applications.

Forecast Projects $12.5B Market by 2032

This chart from Verified Market Research directly visualizes a data point listed in the section’s table, matching the forecast value, year, and CAGR.

(Source: Verified Market Research)

- A key technology-focused collaboration involves Doosan Fuel Cell and LG Electronics, who are co-developing residential micro-CHP units. Their goal is to achieve sub-600°C operation, which promises to reduce material costs and improve long-term durability, making the technology more competitive for the mass market.

- In Europe, a notable market-creation partnership is seen in EET Hydrogen’s 350 MW blue hydrogen project. The project’s financial viability is anchored by a new hydrogen-ready CHP plant, demonstrating industrial confidence in using SOFC-based systems at a significant scale.

- The Asia-Pacific SOFC/SOEC Alliance represents a broader, ecosystem-level collaboration. It brings together Japanese firms with deep expertise in durability, Korean system integrators, and Chinese manufacturing hubs to accelerate innovation and drive down unit costs across the region.

- A 2024 pilot project between Eco Ceres and GDS Holdings in China demonstrated the use of Hydrotreated Vegetable Oil (HVO) to power SOFCs for data center backup. This partnership validates a new commercial application and a pathway to decarbonize critical digital infrastructure.

Table: Key Strategic Partnerships in the SOFC Market

| Partners / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| EET Hydrogen Project | 2026 (Target FID) | A new hydrogen-ready CHP plant will anchor offtake for a 350 MW blue hydrogen facility, validating industrial-scale demand for SOFC-CHP. | H 2 View |

| LG Electronics & Doosan Fuel Cell | 2026 | Co-development of residential micro-CHP units targeting sub-600°C operation to reduce material costs and improve durability. | Keytologic |

| Eco Ceres & GDS Holdings | 2024 | Launched a pilot to use HVO-powered SOFCs for data center backup power, demonstrating a low-carbon alternative to diesel generators. | Advanced Biofuels USA |

| Asia-Pacific SOFC/SOEC Alliance | Ongoing | A regional collaboration promoting technology sharing between Japanese durability experts, Korean system integrators, and Chinese manufacturers. | Intel Market Research |

Japan vs. Europe, Diverging SOFC Deployment Strategies

Geographic deployment of SOFC-CHP technology is not uniform, with regional strategies reflecting different national priorities regarding energy security, industrial policy, and decarbonization pathways. Japan has successfully created a high-volume residential market through direct consumer subsidies, establishing it as the global leader in deployed units. In contrast, Europe’s approach is geared towards industrial and commercial applications, using carbon pricing and efficiency mandates as primary market drivers, which results in larger but fewer individual deployments.

Residential Sector Led Europe’s 2021 SOFC Market

This chart provides specific data for Europe’s SOFC market, one of the key regions discussed, showing the residential segment’s dominant share in 2021.

(Source: Fortune Business Insights)

- Japan leads the world in residential deployment, holding 28% of the total fuel cell market share in 2026. The Ene-Farm subsidy program was the critical enabler, successfully commercializing the technology for consumers and creating a mature manufacturing ecosystem.

- South Korea is focused on building a domestic supply chain for large-scale SOFC and SOEC systems. Its strategy is driven by a national hydrogen roadmap aimed at achieving energy independence and decarbonizing its heavy industrial base.

- Europe prioritizes industrial CHP applications, driven by policies like the Energy Efficiency Directive and the Carbon Border Adjustment Mechanism (CBAM). The market is characterized by projects over 250 k W in hard-to-abate sectors where SOFC’s high efficiency offers a clear value proposition for reducing emissions and energy costs.

60% Electrical Efficiency, Validating TRL 8-9 SOFC Maturity

SOFC technology for stationary power is commercially mature (TRL 8-9), but its economic performance varies significantly by region, creating a split market. While the underlying technology is proven, with leading systems achieving high electrical efficiencies, a persistent gap in cost and performance between Japanese and European residential models remains a key challenge. Innovation is now centered on closing this gap by developing lower-temperature systems to reduce costs and improve long-term durability.

- Leading Japanese SOFC systems have demonstrated high performance, achieving electrical efficiencies of up to 60% and total CHP efficiencies of up to 90%. This high efficiency is the technology’s core value proposition.

- In contrast, European residential fuel cell systems available through 2025 have lagged, offering lower electrical efficiencies in the 30-35% range. This performance gap has hindered widespread consumer adoption in the region without significant subsidies.

- The primary technological hurdle remains the high installed cost, which ranges from $4, 000 to $6, 000 per k W in 2026. This cost barrier limits adoption to subsidized markets or applications with very high-reliability requirements.

- To address this, R&D has intensified around lower-temperature SOFCs operating below 600°C. This shift, pursued by companies like Doosan and LG, aims to enable the use of cheaper materials and improve system longevity, which is critical for achieving unsubsidized market competitiveness.

SWOT Analysis, SOFC Strengths vs. Market and Policy Risks

The strategic position of SOFC-CHP in 2026 is defined by a balance between its superior technical performance and its heavy dependence on external market factors. While its high efficiency is a durable strength, its growth is constrained by high capital costs and a reliance on supportive, but potentially volatile, government policies. The key change between the 2021-2024 period and the current outlook is the validation of new markets like data centers and industrial CHP, offering pathways to growth beyond the subsidized residential sector.

Table: SWOT Analysis for SOFC in Residential and Commercial CHP

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency (45-60%) and CHP efficiency (up to 90%). Fuel flexibility (natural gas, hydrogen). | Efficiency remains a core advantage. Fuel flexibility is increasingly valued for energy transition. | The technology’s high efficiency continues to be its primary competitive advantage, validated in over 400, 000 Japanese homes. |

| Weaknesses | High capital cost and dependence on subsidies (e.g., Ene-Farm). Durability and degradation concerns for high-temperature operation. | Installed costs remain high ($4, 000-$6, 000/k W). Subsidy dependence persists in residential markets. | The fundamental weakness of high CAPEX has not been resolved, confirming that unsubsidized growth is still limited. The push to sub-600°C systems validates ongoing durability and cost challenges. |

| Opportunities | Growing demand for decentralized energy and grid resilience. Green hydrogen production (SOEC mode). | New markets validated: data centers (GDS pilot), industrial CHP (EET project), and maritime shipping. Reversible SOFCs (r-SOFCs) gain traction for grid balancing. | The market opportunity has broadened significantly beyond residential CHP, with commercial projects now providing concrete evidence of demand in new, high-value sectors. |

| Threats | Political risk of subsidy reduction or termination. Competition from rapidly falling costs of solar PV + battery storage. | Policy uncertainty remains the primary threat. Competition from other clean technologies intensifies as their costs continue to decline. | The threat of policy shifts is unchanged and remains the most significant risk to market growth, especially in the mature Japanese residential segment. |

2026 Forward Outlook, Monitoring Large-Scale Project FIDs

The most critical determinant for the SOFC-CHP market’s trajectory beyond 2026 will be the financial viability of large-scale industrial projects operating without direct consumer subsidies. If major projects like EET Hydrogen’s 350 MW facility reach a final investment decision, it will signal a pivotal shift for the industry, proving a commercial model based on industrial decarbonization needs rather than government-funded residential programs. Conversely, delays or cancellations in these bellwether projects would suggest the market remains dependent on policy support for the foreseeable future.

Stationary Applications to Drive Future SOFC Market

This forecast reinforces the section’s forward outlook by visually showing that stationary applications, which include the large-scale industrial projects mentioned, are the dominant market segment.

(Source: Grand View Research)

Commercial Sector Validates SOFC Market Shift

This chart’s 2023 application breakdown, showing commercial and utility dominance, visually confirms the market evolution toward new segments noted in the SWOT analysis.

(Source: IDTechEx)

- Watch this signal: The final investment decision for EET Hydrogen’s project in H 2 2026. A positive outcome would validate the business case for large-scale, hydrogen-ready CHP in Europe.

- If this happens: Manufacturers secure large, multi-megawatt orders for industrial projects. Then this is likely: Investment will accelerate into manufacturing capacity for larger-format SOFC systems, and developers will increasingly target industrial clients in hard-to-abate sectors.

- Watch this signal: Performance and cost data from the pilot deployments of sub-600°C residential units by LG and Doosan. If this happens: The units demonstrate significant cost reductions or durability improvements. Then this is likely: SOFC technology will become more competitive against alternatives like heat pumps and solar+storage in the residential sector, potentially reducing reliance on subsidies.

- Watch this signal: Policy announcements from Japan’s Ministry of Economy, Trade and Industry (METI) regarding the future of the Ene-Farm program. If this happens: Subsidies are reduced or phased out. Then this is likely: The world’s largest residential fuel cell market could contract, impacting the global production volumes of leading Japanese manufacturers.

The questions your competitors are already asking

This report covers one angle of the divergent regional models driving the SOFC CHP market. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in Japan’s residential SOFC market versus South Korea’s industrial power market?

- EET Hydrogen investments and funding. Is the 350 MW blue hydrogen project on track for a final investment decision in late 2026?

- What are the opportunities for SOFC CHP in Europe’s commercial and industrial sectors, driven by the EU Green Deal?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.