SBTi Corporate Climate Scheme, 10, 000+ Validated Targets, and the Rise of Audit-Ready Carbon Accounting (2021 to 2026)

SBTi V 2.0 Triggers Shift from Pledges to Auditable Performance

SBTi V 2.0 Triggers Shift from Pledges to Auditable Performance

The Science Based Targets initiative (SBTi) has fundamentally shifted corporate climate strategy from aspirational pledges to a mandate for auditable performance with its updated Corporate Net-Zero Standard Version 2.0 (CNZS V 2.0). The prior period was defined by target-setting and broad commitments, whereas the current environment, driven by the new rulebook, necessitates deep, verifiable value chain decarbonization and significant investment in compliance infrastructure. This evolution forces companies to move beyond public declarations and implement robust, data-driven systems to manage and report emissions across their entire operations.

- Between 2021 and 2024, corporate focus was primarily on establishing and announcing net-zero goals, often without a clear implementation roadmap. The controversy over allowing carbon credits for Scope 3 abatement highlighted the immense pressure from companies, like Walmart and those in hard-to-abate sectors, struggling with the complexity of value chain reductions.

- Starting in 2025, the release of CNZS V 2.0 created a clear structural shift. The standard mandates a 90-95% absolute emissions reduction before using carbon removals, making granular and auditable carbon accounting a mission-critical function rather than an optional reporting exercise.

- This change is demonstrated by the rapid adoption of SBTi-validated targets, which surpassed 10, 000 companies by early 2026, covering 41% of global market capitalization. The new standard’s requirement for cyclical 5-year revalidation transforms target-setting into a continuous performance management cycle.

- Consequently, the market for carbon accounting platforms offered by firms such as Normative, Persefoni, and Watershed has expanded significantly. These platforms are no longer just for reporting but are essential tools for operationalizing decarbonization to meet the stricter Scope 3 coverage requirements and prepare for mandatory disclosure rules like the EU’s Corporate Sustainability Reporting Directive (CSRD).

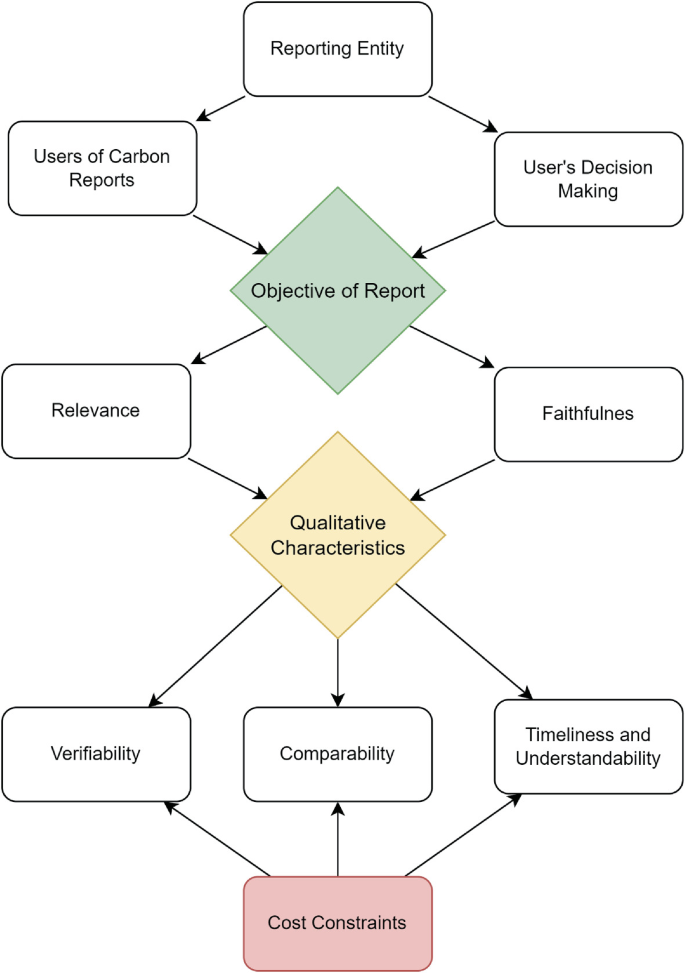

Framework for Quality Climate Reporting Visualized

The chart visualizes a framework for quality climate reporting, which directly supports the section’s theme of SBTi V 2.0 driving a shift towards auditable performance and structured reporting.

(Source: Springer Nature)

$25 B Voluntary Carbon Market, SBTi Rule Change Creates Bifurcated Demand

The SBTi’s new standard is set to restructure the voluntary carbon market (VCM), creating a distinct, premium-priced segment for carbon removal credits while depressing demand for avoidance-based projects. By explicitly allowing only high-integrity *removals* to neutralize the final 5-10% of residual emissions, the V 2.0 rulebook sends a powerful demand signal that will accelerate investment in technologies like Direct Air Capture. This bifurcation will force a re-evaluation of corporate offsetting strategies and project investment portfolios.

- Market forecasts reflect this anticipated growth, with one projection showing the VCM growing from $25.62 billion in 2026 to over $1 trillion by 2035, a compound annual growth rate of 53.56%. This growth is directly tied to the rising number of corporations making net-zero commitments under frameworks like SBTi.

- The standard’s strict distinction between credit types will cement a significant price divergence. High-integrity carbon removal credits, such as those from Occidental Carbon Capture, which can cost over $600 per ton, are positioned to command a premium, while many avoidance credits trading under $20 per ton may see their role limited to “Beyond Value Chain Mitigation” (BVCM) claims rather than net-zero target achievement.

- This market split is also influenced by increasing scrutiny and integrity initiatives like the Core Carbon Principles (CCPs) from the Integrity Council for the Voluntary Carbon Market (ICVCM). Companies are moving away from low-quality credits to avoid accusations of greenwashing, aligning their purchasing with the stringent requirements now formalized by the SBTi.

Table: Carbon Market Size Forecasts by Segment

| Forecast Provider | Market Segment | 2026 Market Size ($B) | CAGR (%) | Source |

|---|---|---|---|---|

| Market Research Future | Voluntary Carbon Credit Market | $25.62 | 53.56% (to 2035) | Market Research Future |

| Polaris Market Research | Total Carbon Credit Market | $1, 109.1 | 32.5% (to 2034) | Polaris Market Research |

| Regreener | Voluntary Carbon Market (Europe) | $3.22 | 20.59% (to 2035) | Regreener |

EU Enforcement Drives Global Adoption of SBTi’s Corporate Climate Scheme

While the SBTi is a global standard-setter, its practical enforcement and the urgency for corporate compliance are most pronounced in regions with robust, parallel regulatory frameworks, particularly the European Union. The EU’s Corporate Sustainability Reporting Directive (CSRD) acts as a powerful enforcement mechanism, compelling companies to adopt rigorous, auditable climate reporting methodologies for which the SBTi framework is the clear benchmark. This dynamic makes Europe a leading indicator for global adoption trends and the associated compliance market.

- Between 2021 and 2024, SBTi adoption was driven by voluntary corporate leadership and investor pressure, with North American and European companies leading the way. However, the connection to mandatory regulation was less direct.

- The period from 2025 onward shows a clear geographic focus catalyzed by regulation. The CSRD, which came into force for many large companies in the 2025 reporting year, requires detailed disclosure on climate transition plans, including Scope 3 emissions. This makes adherence to a credible standard like SBTi’s a practical necessity for EU-based or operating firms.

- This regulatory pressure in Europe is accelerating the market for compliance solutions. Carbon accounting platforms are explicitly marketing themselves as “audit-ready” and CSRD-compliant, recognizing that European regulations are setting a de facto global standard for corporate accountability.

Carbon Accounting Software Matures to Enable SBTi’s Corporate Climate Scheme

The successful implementation of SBTi’s stringent V 2.0 standard is directly enabled by the maturation of carbon accounting software from a simple reporting tool into a sophisticated, AI-powered compliance and strategy platform. The enhanced requirements for Scope 3 emissions measurement and cyclical target validation would be operationally infeasible for most large corporations without these advanced technological solutions. This technological readiness has allowed the SBTi to enforce a level of rigor that would have been impractical just a few years ago.

- From 2021 to 2024, carbon accounting platforms were often used for high-level footprinting and voluntary disclosures. The primary challenge was data acquisition, and methodologies for Scope 3 were less standardized and often relied on spend-based estimates.

- In 2025 and 2026, the technology has evolved to meet the demands of auditable reporting. Leading platforms from Normative and Persefoni now offer AI-driven data ingestion, supplier-specific data collection, and integration with enterprise resource planning (ERP) systems to provide granular, activity-based emissions calculations across all 15 Scope 3 categories.

- The technology now serves a strategic function beyond compliance. These platforms help companies model decarbonization pathways, identify emission hotspots in their supply chains, and track progress against science-based targets in real-time, turning the SBTi framework into an actionable operational plan.

- The cost of this technology, with subscriptions ranging from €6, 000 to over €50, 000 annually, plus significant validation and consulting fees, reflects its new status as a core component of corporate risk management and strategic planning infrastructure.

SWOT Analysis of SBTi’s Corporate Climate Scheme

The SBTi’s strategic position is defined by its unparalleled credibility, which serves as a powerful market-moving force but also creates challenges related to scalability and corporate pragmatism. Its evolution through the CNZS V 2.0 reflects an attempt to balance its scientific authority with the practical implementation hurdles faced by a diverse corporate base, exposing both opportunities for market creation and threats from potential fragmentation.

Table: SWOT Analysis for SBTi Corporate Climate Standard

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | Seen as the gold standard for climate pledges, attracting climate-leading companies like Microsoft and Sumitomo. Authority derived from its scientific backing and multi-stakeholder model. | Credibility is reinforced by alignment with emerging mandatory disclosure rules (e.g., CSRD). Validation surpasses 10, 000 companies, solidifying its market dominance. | The standard’s market power was validated; it successfully transitioned from a voluntary framework for leaders to a baseline for mainstream corporate compliance. |

| Weakness | Perceived as too rigid, particularly its strict stance on carbon credits for Scope 3, risking alienation of hard-to-abate sectors. Internal governance struggles were exposed during the carbon credit debate. | The “delicate tightrope” walk continues. While V 2.0 provides clarity, its stringency on the 90-95% reduction target remains a significant implementation hurdle for many. | The core weakness persists: balancing scientific purity with corporate feasibility. The V 2.0 clarification on credits is a pragmatic step but does not fully resolve the underlying tension. |

| Opportunity | Potential to drive billions in investment into the voluntary carbon market (VCM) by clarifying the role of offsets. Growing regulatory alignment could make SBTi a quasi-regulatory standard. | V 2.0 creates a premium market for high-quality carbon removals and audit-ready carbon accounting software. The 5-year revalidation cycle creates a recurring revenue and engagement model. | SBTi successfully catalyzed new markets. Its rules are now directly shaping investment flows into carbon removal technologies and enterprise compliance software. |

| Threat | Risk of corporate abandonment, as seen with some companies stepping back from climate promises due to difficulty. Rise of less-rigorous, industry-led standards as alternatives. | If seen as too inflexible, a significant number of the 10, 000+ committed companies may fail revalidation, potentially undermining the standard’s perceived success and momentum. | The threat of corporate apathy or fragmentation remains. The success of V 2.0 depends on whether the ecosystem of supporting technologies and services can scale to meet its demands. |

SBTi to Adopt a Hybrid “Reduction and Abatement” Model

The most probable scenario for the SBTi’s evolution is the formalization of a hybrid model that maintains a strict “reduction-first” principle while allowing a limited and highly governed use of certified carbon credits for Scope 3 abatement. If the market continues to struggle with deep value-chain cuts, watch for the SBTi to introduce this guarded flexibility in future standard revisions (V 2.1 or V 3.0) to maintain corporate engagement and prevent market fragmentation. The current V 2.0 standard sets the stage for this by formalizing “Beyond Value Chain Mitigation” and creating a clear quality distinction for carbon removal credits, which could be the first type allowed for target neutralization in the future.

- A key signal is the ongoing pressure from corporations in hard-to-abate sectors and those with complex supply chains, such as consumer goods giant Nestlé, which cannot achieve 90% absolute reductions in the near term through direct action alone.

- The maturation of carbon credit integrity bodies like the ICVCM provides the SBTi with a credible, third-party mechanism to ensure that any allowed credits meet high-quality standards, mitigating the risk of greenwashing.

- The development of an advanced carbon accounting software market, with players like Normative providing audit-ready data, makes a hybrid model technically feasible. Such systems can transparently track and report direct reductions separately from abatement via credits, ensuring accountability.

Charts Compare DAC vs. Renewables Cost-Benefit

The chart comparing the cost-benefit of Direct Air Capture (abatement/removal) and renewables (reduction) directly illustrates the core components and trade-offs of the hybrid “Reduction and Abatement” model discussed in the section.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of the shift to auditable corporate climate performance under SBTi’s new rules. The questions that matter most depend on your work.

- What is actually happening with corporate value chain decarbonization since the SBTi’s Corporate Net-Zero Standard V 2.0 was released?

- Which carbon accounting platforms are gaining ground in the new audit-ready compliance market created by SBTi?

- Which hard-to-abate sectors are adopting solutions to meet the SBTi’s 90-95% absolute reduction rule?

- What are the opportunities for compliance and software providers created by the SBTi’s mandatory 5-year revalidation cycle?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.