Transocean CCUS Strategy, No 2025 Projects, >$189 M in Oil & Gas Contracts (2025)

CCUS Market Projects vs. Transocean’s 2025 Commercial Inaction

In 2025, Transocean maintained a strategic posture toward the carbon capture market, focusing on its core oil and gas drilling business while the broader CCUS industry accelerated with new projects and investments. The company’s actions indicate a deliberate strategy of preparing its fleet and balance sheet to act as a critical “picks and shovels” service provider for a future market, rather than directly investing in or developing carbon capture technology itself.

- While the global Carbon Capture, Utilization, and Storage (CCUS) market was valued between $3.6 billion and $7.85 billion in 2025 and is projected to grow substantially, Transocean announced no specific contracts for CCS well drilling or CO 2 injection services during the year.

- The company’s 2025 Form 10-K acknowledged its role in supporting “carbon capture and sequestration, ” yet its commercial wins, including over $189 million in new drilling options, were exclusively for traditional oil and gas programs in regions like Brazil and Norway.

- This contrasts with the activity of energy majors like Exxon Mobil, Shell, and Chevron, which accounted for around 80% of active CCUS projects in 2025, positioning them as the primary future clients for the drilling services Transocean is preparing to offer.

- Forward-looking signals in early 2026, such as a planned merger with Valaris, underscore a strategic shift toward consolidating market power to serve future large-scale offshore infrastructure projects, including CCS hubs.

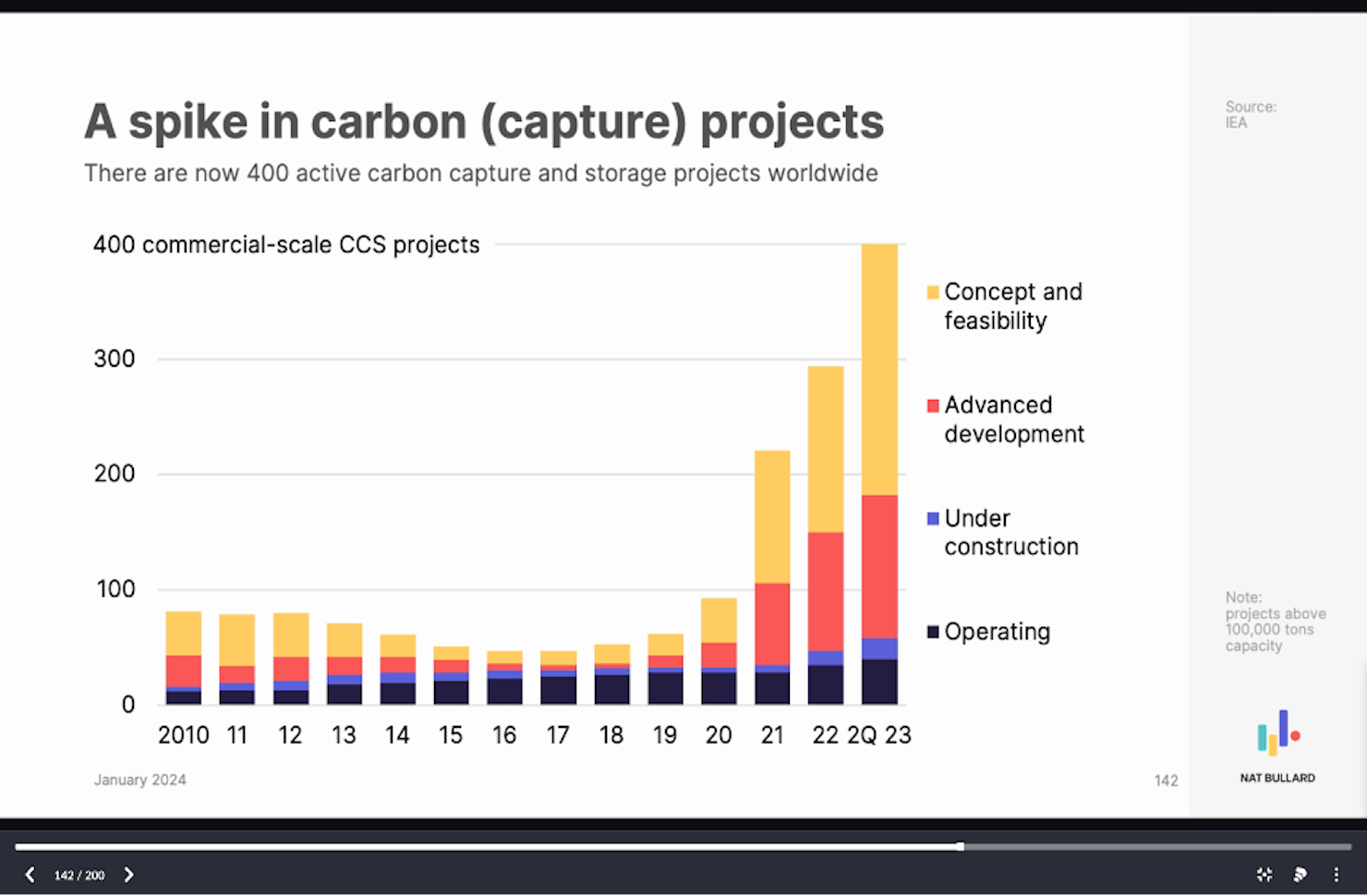

Global Carbon Capture Projects Spike to 400

The section contrasts the growing CCUS market, characterized by an increasing number of projects, with Transocean’s current lack of commercial involvement. This chart directly quantifies the ‘market projects’ side of the argument, showing a significant spike that highlights Transocean’s potential missed opportunity.

(Source: Trellis)

Transocean Balance Sheet Fortification, $750 M Debt Retirement Goal

In 2025 and into 2026, Transocean prioritized financial strengthening over direct investment in new CCS ventures, a move that prepares the company for future capital-intensive projects by deleveraging its balance sheet. This disciplined financial management allows the company to invest in strategic fleet upgrades while maintaining the stability to weather long CCS project development cycles.

- Transocean announced its expectation to retire $750 million in total debt during 2026, a significant deleveraging that strengthens its financial position and enhances its capacity to invest in fleet upgrades or pursue new market opportunities.

- The company maintained strict capital discipline, with CAPEX reported at only $24 million during the second quarter of 2025, preserving capital for strategic deployment as the CCS market matures.

- This financial strategy is supported by a strong core business, which secured over $1.185 billion in new traditional drilling contracts in early 2026, providing the cash flow necessary to fund both debt reduction and future strategic pivots.

Table: Transocean Financial and Contract Highlights (2025-2026)

| Date Announced | Financial Action / Contract | Value (USD) | Details and Strategic Purpose | Source |

|---|---|---|---|---|

| Jun 18, 2026 | New Oil & Gas Contracts | $185 Million | Added to backlog from new contracts for two harsh-environment semisubmersible rigs in Norway and Australia, strengthening core revenue. | The Globe and Mail |

| Apr 2, 2026 | Aggregate New Contracts | $1 Billion | Total value of new contracts secured, reinforcing the company’s strong backlog and financial performance ahead of potential CCS market entry. | Investing.com |

| Apr 2, 2026 | Planned Debt Retirement | $750 Million | Expected debt retirement for 2026, aimed at deleveraging the balance sheet and increasing financial flexibility for future investments. | Investing.com |

| Nov 18, 2025 | Contract Options Exercised | $89 Million | Added to backlog from operators exercising options for three rigs in Brazil, Norway, and Romania, confirming the health of the traditional drilling market. | World Oil |

| Jun 5, 2025 | Contract Option Exercised | $100 Million | A two-well option was exercised for the Transocean Spitsbergen rig in Norway, highlighting continued demand for high-specification assets. | Drilling Contractor |

The Valaris Merger, Transocean’s Market Consolidation for CCS Scale

Transocean’s most significant strategic alliance initiative during the 2025-2026 period is the planned merger with Valaris, a consolidation play aimed at creating a dominant service provider for future large-scale offshore drilling, including CCS. While not a direct CCS partnership, the move is foundational to servicing the capital-intensive drilling campaigns that large-scale carbon sequestration projects will require.

- In February 2026, reports emerged of a planned merger between Transocean and competitor Valaris, a move that would create the world’s largest offshore drilling contractor.

- The primary strategic objective is to consolidate fleet size, technical expertise, and market power, providing the combined entity with unparalleled scale and pricing leverage.

- This scale directly addresses the anticipated needs of future offshore CCS hubs, such as those planned in the North Sea and the U.S. Gulf of Mexico, which will require extensive and technically complex drilling programs for CO 2 injection wells.

Table: Transocean Strategic Partnership Initiatives

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Valaris | Feb 2026 | A planned merger to create the world’s largest offshore drilling contractor. The strategic purpose is to gain market scale and pricing power to service both legacy energy clients and the emerging large-scale CCS drilling market. | Africa Oil+Gas Report |

Norway and Brazil, Transocean’s Core O&G Focus Over CCS Hubs

Transocean’s commercial activities in 2025 remained concentrated in established oil and gas provinces like Norway and Brazil, while key future CCS hubs in the North Sea and U.S. Gulf of Mexico represent future, not current, operational targets for its carbon sequestration services. The company’s geographical focus reflects its strategy of capitalizing on the strong traditional drilling market to build financial strength before pivoting to CCS.

- In November 2025, the company secured $89 million in new backlog from contract options exercised for projects in the established oil and gas regions of Brazil, Norway, and Romania.

- In June 2025, a $100 million, two-well option was exercised for the harsh-environment rig Transocean Spitsbergen in Norway, further cementing its operational focus in the region’s traditional energy sector.

- This activity contrasts with the immense but unrealized potential of CCS in these same geographies. The UK North Sea alone is estimated to hold 78 billion tonnes of CO 2 storage capacity, representing a massive future market for specialized offshore drilling services.

- The company’s presence in the U.S. Gulf of Mexico positions it well to serve future projects driven by the 45 Q tax credit, but in 2025 its contracts remained tied to oil and gas exploration and development.

Oil & Gas Dominates 2024 CCS Market

The section contrasts Transocean’s focus on its core O&G business with a potential shift to CCS. This chart illustrates the strong overlap between the two sectors, showing that O&G currently dominates the CCS market. This justifies Transocean’s interest while also explaining its prioritization of its core, highly related business.

(Source: Global Market Insights)

>60% MPD Fleet Readiness, Transocean Prepares for CO 2 Wells

Transocean’s primary technological advancement for the CCS market is the strategic upgrade of its fleet with Managed Pressure Drilling (MPD) systems, positioning its existing assets to meet the technical demands of CO 2 injection wells before securing any contracts. This technology-led approach prepares a significant portion of its fleet to service the specific technical challenges of carbon sequestration.

- Transocean set a strategic goal to equip over 60% of its active drillships with integrated MPD capabilities by the end of 2025.

- MPD technology provides precise control over the wellbore pressure profile, a critical requirement for ensuring the long-term integrity of CO 2 injection wells and preventing subterranean leaks.

- This proactive fleet enhancement is a direct enabler for entering the CCS drilling market, transforming a portion of its assets from pure rig leasing to providing integrated, high-tech solutions for a new client base.

- By focusing on adapting its existing high-specification fleet, Transocean avoids the high R&D risk of developing novel capture technologies and instead reinforces its role as a specialized service provider.

Chart Models Carbon Capture Technology Lifecycle

This section focuses on Transocean’s technical readiness and specific equipment (MPD) for CO2 wells. The technology lifecycle chart provides context by illustrating the maturity of carbon capture technology, helping to position Transocean’s fleet readiness and investment within the broader technological development curve.

(Source: Nature)

SWOT Analysis, Transocean’s CCS Enabler Position

Transocean’s SWOT profile for CCS reveals a company leveraging its core drilling strengths to patiently prepare for a market opportunity, while managing the risks of delayed entry and continued reliance on the cyclical oil and gas sector. The analysis shows a clear strategy of financial and technical preparation over immediate commercial engagement in 2025.

Decarbonization Imperatives Driving Future Revenue

A SWOT analysis requires an understanding of external drivers, which represent opportunities and threats. This chart identifies ‘decarbonization imperatives’ as a key driver of future revenue, directly informing the ‘Opportunities’ aspect of Transocean’s strategic position in the CCS market.

(Source: MarketsandMarkets)

Table: SWOT Analysis for Transocean’s Carbon Capture Strategy

| SWOT Category | Description | Supporting Evidence (2025-2026) |

|---|---|---|

| Strengths | Dominant position in deepwater and harsh-environment drilling, a high-specification fleet, and a strengthening balance sheet. | Expertise in complex well construction applicable to CO 2 injection. A strategic goal to equip >60% of drillships with MPD technology. Over $1.1 B in new O&G contracts and a plan to retire $750 M in debt in 2026. |

| Weaknesses | No direct commercial experience or contracts in the CCS sector as of mid-2026. A reactive rather than proactive project development strategy. | All major contracts announced in 2025 and H 1 2026 were for traditional oil and gas. Acknowledged CCS in 10-K but no tangible projects. |

| Opportunities | A burgeoning offshore CCS market projected to reach over $17 billion by 2030. Ability to leverage existing assets and expertise to become a go-to service provider. | Market growth is driven by policy like the 45 Q tax credit ($85/ton). The planned Valaris merger creates the scale to dominate CCS drilling services. |

| Threats | Competitors could gain first-mover advantage and critical expertise by engaging in early CCS projects. Continued reliance on the volatile oil and gas market. | While Transocean waits, other service companies could build relationships with CCS project developers. A downturn in oil prices could hinder its ability to fund a pivot to CCS. |

Scenario Modeling for Transocean’s First CCS Contract

The primary signal to watch for a shift in Transocean’s strategy is the announcement of its first significant drilling contract for a commercial-scale offshore CCS project, which would validate its “enabler” positioning and mark its formal entry into the market. Its current activities are precursors to this event, which depends on both internal readiness and external market maturation.

- If the Valaris merger is finalized as planned, watch for a unified marketing push from the combined entity specifically targeting large-scale CCS projects. The increased scale and market power would make it the default bidder for major drilling campaigns.

- If a major energy operator announces a final investment decision (FID) on an offshore CCS hub in the North Sea or Gulf of Mexico, watch for Transocean to be named as a key contractor. This would be the catalyst that turns its strategic preparation into commercial reality.

- If Transocean publicly confirms it has met its year-end 2025 goal of >60% MPD integration on its drillship fleet, this signals full operational readiness to execute complex CO 2 injection well drilling, increasing the likelihood of a near-term contract award.

The questions your competitors are already asking

This report covers one angle of Transocean’s commercial strategy for the carbon capture market. The questions that matter most depend on your work.

- Which offshore drilling companies are gaining or losing ground in the emerging market for CCUS well services?

- Is Transocean a good investment for CCUS exposure, given its current focus on traditional oil and gas contracts?

- Which energy majors like ExxonMobil and Shell are contracting offshore drillers for their large-scale CCUS projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.