Top 10 AI Hardware Companies: Open AI & Broadcom Plan 10 GW Chips, NVIDIA Adopts 800 V Architecture (2024-2025)

The rapid proliferation of generative Artificial Intelligence has ignited a convergence between the semiconductor, data center, and energy sectors, transforming data centers into “AI Factories.” This evolution reframes electricity from a simple utility cost to a primary raw material for producing intelligence. The unprecedented demand for computational power has exposed energy supply as the most significant bottleneck, particularly in the United States. Projections show U.S. data center power demand could surge from approximately 25 GW in 2024 to over 80 GW by 2030, while global data center electricity consumption is forecast to more than double from 460 TWh to over 1, 000 TWh in the same period. For 2025, the dominant theme is the strategic pivot towards gigawatt-scale data center campuses with co-located power, a trend driven by deep partnerships between technology giants and energy producers to secure the massive power required for future AI growth.

1. NVIDIA

Key Metric/Activity: Developing 800 V HVDC architecture for 1 MW server racks.

Application: Dominant GPU designer for AI training and inference.

Source: Nvidia to boost AI server racks to megawatt scale…

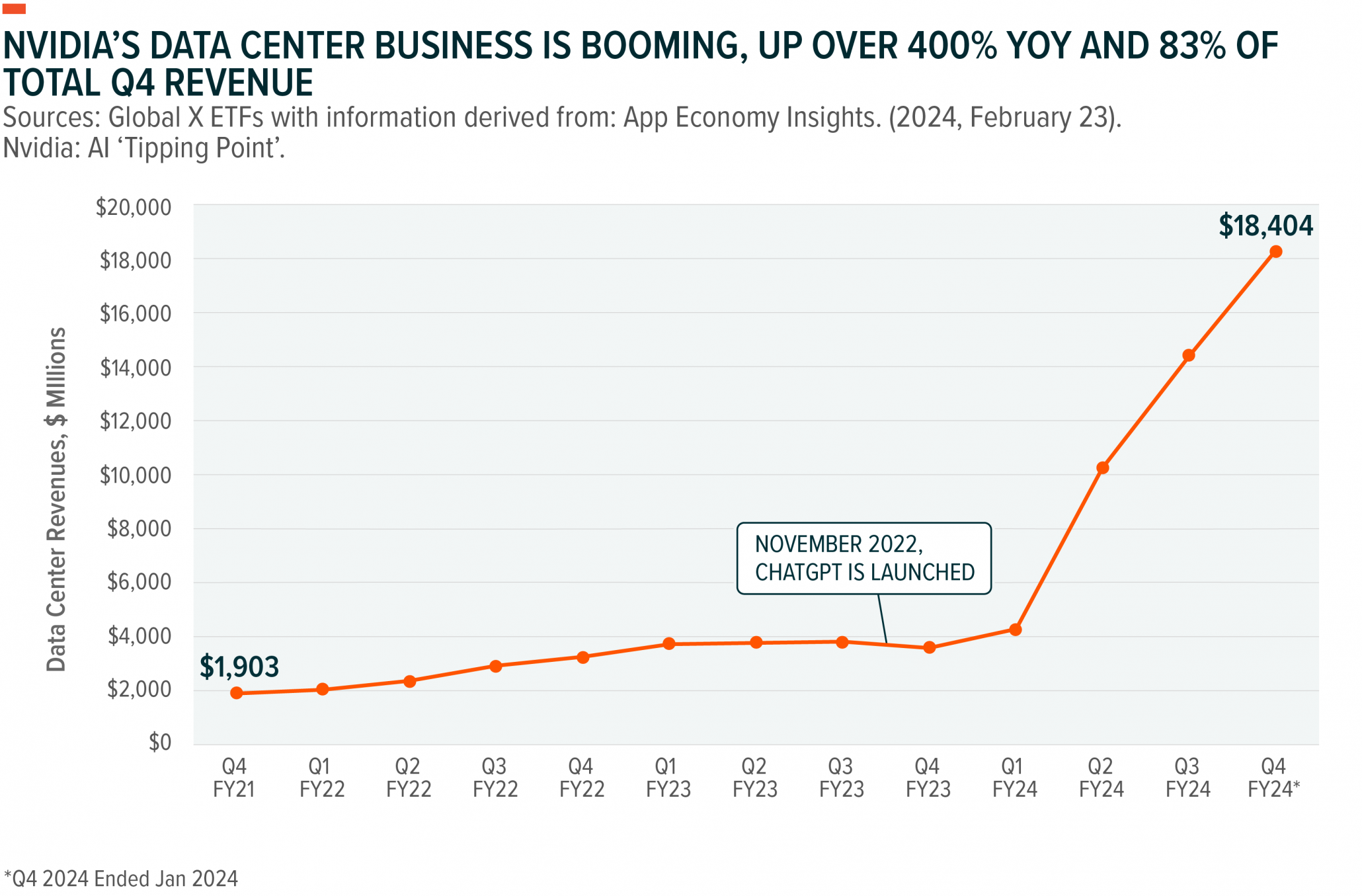

NVIDIA Data Center Revenue Surges to $18.4B

The chart provides a key financial metric (data center revenue) that quantifies NVIDIA’s success, making it a perfect fit for a section dedicated to the company.

(Source: Global X ETFs)

2. Advanced Micro Devices (AMD)

Key Metric/Activity: Targeting $5 billion in AI chip sales by 2025.

Application: Primary competitor to NVIDIA in the AI accelerator market.

Source: AI revolution drives demand for specialized chips…

3. Broadcom

Key Metric/Activity: Co-developing 10 GW of custom AI chips with Open AI.

Application: Custom silicon solutions (ASICs) for major tech companies.

Source: Open AI and Broadcom to co-develop 10 GW of custom AI chips…

4. Intel

Key Metric/Activity: Competing with its Gaudi platform for AI acceleration.

Application: AI-optimized hardware for data center and edge environments.

Source: The 25 Hottest AI Companies For Data Center And Edge…

5. Taiwan Semiconductor Manufacturing Company (TSMC)

Key Metric/Activity: Expanding U.S. investment by $100 billion for three new fabs.

Application: World’s leading foundry for advanced AI chip manufacturing.

Source: TSMC Intends to Expand Its Investment in the United States…

TSMC and NVIDIA Drive Explosive AI Growth

This chart highlights TSMC’s critical role in the AI ecosystem by showcasing its essential manufacturing partnership with NVIDIA, a central theme for any discussion about TSMC’s market position.

(Source: semivision – Substack)

6. Samsung Foundry

Key Metric/Activity: Leveraging AI to optimize its own production processes.

Application: Major foundry competitor to TSMC in advanced semiconductor manufacturing.

Source: AI is transforming the semiconductor industry in 2025 and beyond

7. Google

Key Metric/Activity: Partnership with Next Era Energy for GW-scale data center campuses.

Application: Custom AI silicon (TPUs) for its cloud and internal workloads.

Source: Next Era Energy and Google Cloud Announce Landmark Strategic…

8. Amazon (AWS)

Key Metric/Activity: Contracted over 50 GW of renewable energy PPAs.

Application: Custom silicon (Trainium, Inferentia) for AI workloads on AWS.

Source: The Data Center Balancing Act: Powering Sustainable AI Growth

AWS Revenue Growth Stabilizes on AI Demand

The chart directly presents revenue data for AWS, the subject of the section, and links it to the pivotal trend of AI-driven demand.

(Source: Global X ETFs)

9. Groq

Key Metric/Activity: Delivering exceptional inference speed with Language Processing Units (LPUs).

Application: Specialized chips focused on ultra-low latency and power efficiency.

Source: Top 10 AI Chip Startups to Watch in 2025

10. Samba Nova Systems

Key Metric/Activity: Offering a full-stack AI platform with a reconfigurable dataflow architecture.

Application: Enterprise AI hardware for a wide range of models.

Source: The 10 most innovative computing companies of 2025

Table: Top 10 AI Hardware Company Activities

| Company | Key Metric/Activity | Application | Source |

|---|---|---|---|

| NVIDIA | Developing 800 V HVDC architecture for 1 MW server racks. | Dominant GPU designer for AI training and inference. | Nvidia to boost AI server racks… |

| Advanced Micro Devices (AMD) | Targeting $5 billion in AI chip sales by 2025. | Primary competitor to NVIDIA in the AI accelerator market. | AI revolution drives demand for specialized chips… |

| Broadcom | Co-developing 10 GW of custom AI chips with Open AI. | Custom silicon solutions (ASICs) for major tech companies. | Open AI and Broadcom to co-develop… |

| Intel | Competing with its Gaudi platform for AI acceleration. | AI-optimized hardware for data center and edge environments. | The 25 Hottest AI Companies… |

| Taiwan Semiconductor Manufacturing Company (TSMC) | Expanding U.S. investment by $100 billion for three new fabs. | World’s leading foundry for advanced AI chip manufacturing. | TSMC Intends to Expand Its Investment… |

| Samsung Foundry | Leveraging AI to optimize its own production processes. | Major foundry competitor to TSMC in advanced semiconductor manufacturing. | AI is transforming the semiconductor industry… |

| Partnership with Next Era Energy for GW-scale data center campuses. | Custom AI silicon (TPUs) for its cloud and internal workloads. | Next Era Energy and Google Cloud Announce… | |

| Amazon (AWS) | Contracted over 50 GW of renewable energy PPAs. | Custom silicon (Trainium, Inferentia) for AI workloads on AWS. | The Data Center Balancing Act… |

| Groq | Delivering exceptional inference speed with Language Processing Units (LPUs). | Specialized chips focused on ultra-low latency and power efficiency. | Top 10 AI Chip Startups to Watch… |

| Samba Nova Systems | Offering a full-stack AI platform with a reconfigurable dataflow architecture. | Enterprise AI hardware for a wide range of models. | The 10 most innovative computing companies… |

660% Growth, AI Hardware Market Set for Explosive Surge by 2035

The diversity of companies leading the AI hardware charge signals a maturing market moving beyond one-size-fits-all solutions. While NVIDIA and AMD dominate the high-performance GPU space, the rise of custom silicon from hyperscalers like Google (TPUs) and Amazon (Trainium) indicates a powerful trend toward vertical integration. These companies are designing chips tailored to their specific software and workloads to maximize efficiency and reduce reliance on third-party vendors. Furthermore, the significant investment in custom ASICs by players like Broadcom, in partnership with model developers like Open AI, shows that the largest AI consumers are becoming major hardware designers. This diversification implies that the future of AI hardware is not a monopoly but a complex ecosystem of general-purpose, custom, and specialized architectures.

AI Hardware Spend to Reach $200B by 2027

The chart offers a specific financial projection ($200B spend by 2027) that substantiates the section’s claim of an ‘Explosive Surge’ in the AI hardware market.

(Source: Global X ETFs)

USA & Taiwan Lead, TSMC’s $100 B Fab Expansion in the US

The geographic landscape of AI hardware is highly concentrated, with the United States and Taiwan forming a critical axis of innovation and production. The U.S. is the undisputed center for chip design, hosting industry leaders NVIDIA, AMD, Intel, and Broadcom. However, the physical manufacturing of the most advanced chips relies heavily on foundries in Asia, primarily Taiwan Semiconductor Manufacturing Company (TSMC). Recognizing the strategic risk of this dependency, there is a major push to re-shore manufacturing. TSMC‘s landmark decision to expand its U.S. investment with a $100 billion plan for new fabrication plants in Arizona is the most tangible evidence of this shift. This move not only strengthens the U.S. supply chain but also brings massive energy and infrastructure demands to the region, linking national technology strategy directly to local utility planning.

AI-Focused Companies Dominate Global Market Cap

The chart, by ranking top AI-focused companies by market cap, visually demonstrates the dominance of companies from the USA (NVIDIA, Microsoft, Google) and Taiwan (TSMC), directly supporting the section’s theme of their leadership.

(Source: LinkedIn)

GPU Dominance, NVIDIA Commands 92% Market Share in Datacenter GPUs

The current state of AI hardware maturity is best understood as a tiered system. At the top, NVIDIA’s GPU platform, fortified by its proprietary CUDA software ecosystem, represents a fully mature and commercially dominant technology, capturing an estimated 92% of the data center GPU market. This is the established standard against which all others compete. In the next tier, custom silicon from hyperscalers like Google and Amazon is also mature but serves a more specialized, captive audience. This strategy is only viable for companies operating at extreme scale. The third tier consists of emerging innovators like Groq and Samba Nova Systems. Their novel architectures, such as Groq’s Language Processing Unit (LPU), are challenging the status quo by focusing on specific niches like high-speed, power-efficient inference. Their growing traction suggests the market is actively seeking alternatives to GPUs, especially as AI models become more widespread and inference costs become a critical business factor.

NVIDIA Dominates Datacenter GPU Market with 92% Share

The chart’s headline and data (92% share) are a direct and explicit illustration of the section’s title, providing the core evidence for NVIDIA’s GPU dominance.

(Source: IoT Analytics)

Google’s GW-Scale Campuses with Next Era Signal Energy Integration (2025)

The most critical strategic action for 2025 is the accelerated formation of deep, binding partnerships between AI hardware and infrastructure players and traditional energy providers. The era of data centers as passive consumers of grid power is over; they are now active partners in energy infrastructure development. Expect to see more technology companies co-investing in power generation assets to secure supply for decades to come.

- The landmark partnership announced between Google and Next Era Energy to develop gigawatt-scale data center campuses with co-located power generation sets the blueprint for this new model.

- NVIDIA‘s parallel work on a high-voltage 800 V HVDC architecture for 1 MW server racks, and its collaboration with industrial giant ABB, explicitly targets the development of next-generation gigawatt-scale data centers.

- The staggering power demand forecasts, with some estimates pointing to U.S. data centers requiring over 80 GW by 2030, make these energy-focused partnerships a matter of strategic survival, not just an optimization.

AI Server Rack Power to Hit 600kW

This chart explains the underlying technical challenge—soaring server power consumption—that drives the need for the ‘GW-Scale Campuses’ and advanced energy strategies mentioned in the section heading.

(Source: Data Gravity)

The questions your competitors are already asking

This report covers one angle of the AI hardware market’s energy requirements. The questions that matter most depend on your work.

- Tech companies investing in power generation

- US power grid upgrades for new chip fabs

- Data center liquid cooling adoption

- NVIDIA competitors custom AI chip performance

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.