AI’s Power Grid Constraint: How Big Oil Is Building a New Energy Market in 2026

From Internal AI Tools to External Power Plays: The 2026 Energy Market Shift

Energy supermajors are executing a strategic pivot from solely using AI for internal operational efficiency to building a new, high-margin business line that directly powers the AI industry, creating a market solution to the public grid’s inability to meet exponential data center demand.

- Between 2021 and 2024, Chevron’s AI strategy was primarily focused on internal optimization, such as using AI for seismic interpretation with Eliis, deploying digital twins for gas plants, and enhancing refinery performance with partners like Honeywell. The goal was cost reduction and hydrocarbon recovery maximization.

- Starting in January 2025, the strategy fundamentally shifted outwards. Chevron formed a joint venture with Engine No. 1 and GE Vernova to build up to 4 gigawatts (GW) of natural gas-fired power generation capacity specifically for U.S. data centers, marking a move from being an AI user to an AI enabler.

- This transition reflects a recognition of a critical infrastructure bottleneck. While internal AI applications yielded significant savings, such as cutting drilling costs by 50%, the new strategy targets a revenue opportunity created by the AI industry’s massive power requirements that outstrip grid capacity.

- The commercial model has evolved from internal pilots to large-scale, external-facing projects. The first major project is a planned 2.5 GW natural gas power plant in West Texas, designed to provide “behind-the-meter” power directly to data center clients, bypassing grid constraints.

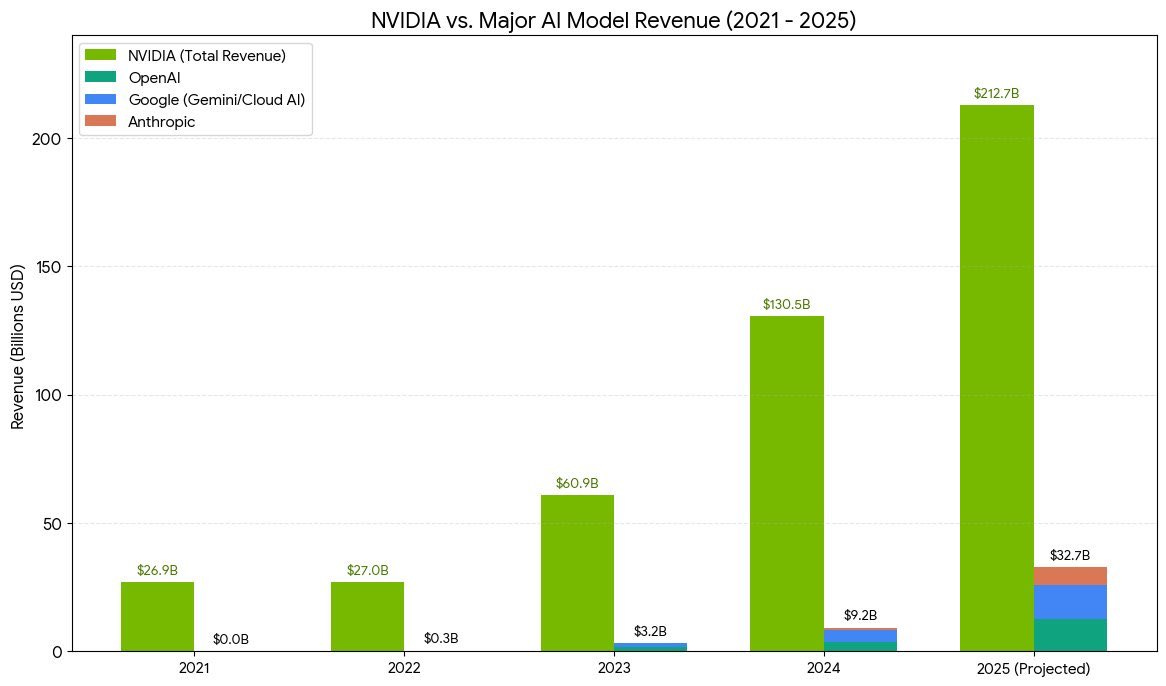

AI Revenue Boom Drives Energy Demand

This chart shows the explosive revenue growth of leading AI companies. This growth is the primary driver for the massive new energy demand that supermajors are now pivoting to supply.

(Source: Deb Liu | Substack)

Capital Flows into AI Infrastructure: Analyzing the Investments Fueling Data Center Power Projects

Massive, multi-billion dollar capital injections from both the energy and technology sectors are validating the business model of developing dedicated power infrastructure for AI, confirming that co-located power generation is now a primary solution to the industry’s energy needs.

Venture Capital Investment in AI Skyrockets

This chart illustrates the massive influx of venture capital into the AI sector post-ChatGPT. This capital explosion validates the need for dedicated power infrastructure projects to support this rapid expansion.

(Source: Deb Liu | Substack)

- Chevron committed $1.5 billion to a new business unit specifically targeting AI data centers with natural gas power and carbon capture technologies, a clear signal of a long-term strategic investment in this new market segment.

- The demand side is confirmed by technology giants’ colossal spending. A partnership involving Open AI, Oracle, and Soft Bank is reportedly planning to invest up to $500 billion in AI-related infrastructure, while Meta announced a $10 billion AI data center in Louisiana in January 2025.

- These investments dwarf previous funding rounds for internal AI software or niche applications. The scale of capital now being deployed is for building foundational infrastructure, signifying a new phase of industrial-level build-out for the AI economy.

Table: Key Investments in AI and Supporting Infrastructure (2025-2026)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Stargate (Open AI, Oracle, Soft Bank) | Jan 28, 2025 | Up to $500 Billion planned for AI infrastructure development. This massive capital pool creates unprecedented demand for reliable, large-scale power sources, which is the market Chevron and others aim to capture. | The Globe and Mail |

| Open AI | Jan 2, 2026 | Raised a $40 Billion funding round led by Soft Bank. This capital is intended to fund the development of more powerful AI models, which in turn require exponentially more computing power and energy. | Crunchbase News |

| Chevron | Jan 28, 2025 | $1.5 billion investment into a new business unit to build natural gas power plants for data centers. This represents a direct capital allocation to monetize its gas reserves by serving the AI market. | Enki AI |

| Meta | Jan 10, 2025 | $10 Billion investment in a new AI data center in Louisiana. This project is a concrete example of the hyperscale demand that requires dedicated power solutions beyond what local grids can typically provide. | Louisiana Economic Development |

Forging the AI Power Ecosystem: Strategic Alliances Driving 2026 Infrastructure Growth

The development of dedicated power for AI is not being driven by single entities but by a new ecosystem of cross-industry partnerships, combining energy producers, investment firms, and equipment manufacturers to de-risk and accelerate project execution.

Venture Capital Bets Big on Top AI Players

This chart visualizes the trend of venture capital concentrating in a few massive AI deals. It provides the macro context for the specific, large-scale investments in companies like OpenAI detailed in the table.

(Source: Deb Liu | Substack)

- The definitive partnership in this space is the January 2025 joint venture between Chevron, activist investment firm Engine No. 1, and energy equipment giant GE Vernova. This alliance brings together the fuel source (Chevron), project financing and strategy (Engine No. 1), and power generation technology (GE Vernova).

- This collaborative model is essential for managing the complexity of building large-scale power plants. It contrasts with the 2021-2024 period, where partnerships like Chevron’s collaboration with Microsoft and SLB were focused on data platforms for internal use.

- On the consumer side, the alliance between Open AI, Oracle, and Soft Bank under the Stargate entity shows that technology companies are also pooling resources to secure the infrastructure they need, creating a concentrated and powerful customer base for energy providers.

- Other energy companies, such as Total Energies and Exxon Mobil, are now exploring similar strategies, indicating that this partnership-driven model is becoming the industry standard for addressing the AI data center market.

Table: Key Partnerships for AI Data Center Power (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Chevron / Engine No. 1 / GE Vernova | Jan 28, 2025 | A joint venture formed to develop up to 4 GW of natural gas-fired power plants for U.S. data centers. This is the flagship project defining the new market of co-located power generation. | Reuters |

| Chevron / Halliburton | Jun 12, 2025 | Deployed the first closed-loop, autonomous fracking system. While an internal efficiency project, it generates the cost savings and production gains that help fund capital-intensive external projects like data center power plants. | World Oil |

Geographic Focus: Why the Texas Permian Basin is the Epicenter of AI’s New Power Demand

The Permian Basin in West Texas has emerged as the primary geography for the first wave of dedicated data center power projects due to its unique combination of abundant natural gas, available land, and a supportive regulatory environment.

- Chevron’s inaugural project, a 2.5 GW natural gas power plant, is sited in the Permian Basin. This location is not coincidental; it allows the company to directly monetize its extensive natural gas reserves at the source, avoiding transportation costs and pipeline constraints.

- Prior to 2025, AI-related activity in the Permian was focused on optimizing drilling and extraction. The region is now a hub for a new value chain: converting hydrocarbons directly into electricity for a captive, high-value customer.

- The “behind-the-meter” strategy is particularly effective in Texas, where the regional grid (ERCOT) faces significant congestion challenges. Building power plants co-located with data centers allows operators to bypass these grid issues, offering a more reliable power supply.

Technology Readiness: The Commercialization of Co-Located Data Center Power Generation

The strategy of building dedicated, co-located natural gas power plants for data centers has advanced from exploratory talks in 2024 to commercially viable, large-scale projects with defined timelines and significant capital backing in 2025.

- In late 2024, reports indicated that energy majors were in early discussions to supply power to data centers. This was largely conceptual.

- By January 2025, this concept was validated with the announcement of Chevron’s joint venture and its specific plans for a 2.5 GW plant in Texas with a target operational date of 2027. This marks the transition from R&D to commercial execution.

- The core technology, natural gas-fired turbines from manufacturers like GE Vernova, is mature and proven. The innovation lies in the business model and project structure: dedicating entire power plants to specific industrial customers to circumvent public infrastructure weaknesses.

- A key remaining technological and economic challenge is the integration of carbon capture and sequestration (CCS) at scale. While included in the strategic plans, the commercial viability of CCS for these plants has yet to be fully proven.

SWOT Analysis: The Strategic Risks and Rewards of Powering the AI Revolution

The strategy to power the AI industry offers energy producers a pathway to revalue their core assets and capture a high-growth market, but it is accompanied by significant environmental and regulatory risks that will determine its long-term viability.

AI Software Market Growth Creates Opportunity

The projected growth of the AI software market quantifies the massive opportunity available. This expanding market is the primary reward that energy companies hope to capture by powering the AI industry.

(Source: Vention)

- Strengths: The strategy directly leverages existing natural gas reserves and core competencies in developing large-scale energy projects.

- Weaknesses: The reliance on natural gas carries a significant carbon footprint, creating a potential clash with the ESG goals of technology clients and investors.

- Opportunities: The demand for data center power is growing exponentially and is relatively price-inelastic, creating a premium market for reliable energy.

- Threats: Regulatory hurdles for carbon capture technologies and potential backlash from environmental groups could delay or derail projects.

Table: SWOT Analysis for the Data Center Power Generation Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Internal AI expertise (e.g., APOLO platform) and operational efficiency in hydrocarbon extraction. | Direct monetization of natural gas reserves by converting them to premium-priced electricity for a dedicated market. | The strategy shifted from using assets to cut costs to using them to create a new, high-margin revenue stream. The value of gas reserves is re-framed as a direct input for the digital economy. |

| Weaknesses | General ESG pressure on the oil and gas industry and the carbon intensity of core operations. | The explicit linking of future growth to new fossil fuel-based power generation, even with planned carbon capture. | The weakness became more acute. Instead of just powering its own operations, the model proposes building new carbon-emitting infrastructure to enable another high-growth industry. |

| Opportunities | Cost savings and production increases through internal AI deployment in areas like the Permian Basin. | Capturing a share of the massive, grid-constrained power demand from AI hyperscalers, validated by multi-billion dollar investments. | The opportunity grew from incremental efficiency gains to a multi-billion dollar market opportunity. The problem (AI power demand) became a tangible business case. |

| Threats | Commodity price volatility and long-term energy transition policies favoring renewables. | Failure to deliver on carbon capture at an economically viable scale could alienate tech clients and attract regulatory penalties. Competition from other energy providers like Southern Company is also emerging. | The threat became more specific. It is no longer just about the general energy transition but about the specific technological and economic viability of the carbon capture component of this new strategy. |

2026 Forward Outlook: Key Signals for the Energy-AI Infrastructure Market

If AI compute demand continues its exponential growth, the primary signal to watch in 2026 will be the replication of Chevron’s data center power play by other energy majors, transforming this niche strategy into a mainstream infrastructure asset class.

AI Model Performance Continues Rapid Climb

This chart tracks the accelerating performance of leading AI models, which is the core technological driver of future compute demand. This ongoing surge in capability validates the forward outlook that demand for power will continue to grow exponentially.

(Source: Stanford HAI – Stanford University)

AI and Tech Giants Dominate Market

The chart shows the immense market capitalization of the tech firms that are the end-users for dedicated data center power. This market dominance underscores the strategic value of becoming a key supplier to this sector.

(Source: J.P. Morgan Asset Management)

- Watch for new joint ventures: The key indicator of market expansion will be announcements of similar partnerships between other oil and gas producers, private equity firms, and equipment suppliers. Reports that Exxon Mobil is exploring opportunities in this space are a critical early signal.

- Monitor first-of-a-kind project execution: The progress of Chevron’s 2.5 GW Texas plant toward its 2027 startup date will serve as the commercial proof-of-concept for the entire market. Any delays or major cost overruns could slow follow-on investments.

- Track technology offtake agreements: Watch for definitive power purchase agreements (PPAs) signed between these new energy ventures and AI hyperscalers like Meta, Google, or the Stargate entity. These contracts will validate the financial model and de-risk future projects.

Frequently Asked Questions

What is the primary strategic change for energy companies like Chevron regarding AI?

Chevron is shifting from using AI for internal purposes (like optimizing drilling and refining) to building an external business that provides dedicated power to the AI industry. Before 2025, the focus was on cost reduction; now, it’s on creating a new revenue stream by building natural gas power plants specifically for data centers.

Why are oil companies building these power plants instead of just using the public grid?

The public power grid is unable to keep up with the massive and rapidly growing electricity demand from the AI industry. This creates a critical infrastructure bottleneck. By building dedicated, co-located power plants, energy companies can provide reliable “behind-the-meter” power directly to data centers, bypassing grid constraints and capturing a new, high-margin market.

What makes the Permian Basin in Texas the ideal location for these projects?

The Permian Basin is the epicenter for these initial projects because it offers a unique combination of abundant and low-cost natural gas, available land for large-scale construction, and a supportive regulatory environment. This allows companies like Chevron to directly monetize their gas reserves at the source, avoiding transportation costs.

What are the main risks or downsides to powering AI with natural gas?

The primary risk is environmental. The strategy relies on building new fossil fuel infrastructure, which carries a significant carbon footprint. This creates a potential clash with the ESG (Environmental, Social, and Governance) goals of tech clients and investors. The long-term success of this strategy is also threatened by the technological and economic challenge of implementing carbon capture and sequestration (CCS) at a viable scale.

Who are the key players in this new energy-for-AI ecosystem?

The ecosystem is built on cross-industry partnerships. The flagship alliance is a joint venture between Chevron (providing the natural gas), Engine No. 1 (providing investment and strategy), and GE Vernova (providing the power generation technology). On the demand side, entities like the Stargate partnership (OpenAI, Oracle, SoftBank) represent the concentrated customer base requiring this power.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.