Flow Battery Top 10 LDES, ESS Inc 50 MWh Pilot with SRP & $17 B Market Projections (2024 to 2025)

The Long-Duration Energy Storage (LDES) market is undergoing a critical diversification beyond the 4-hour lithium-ion standard, with a portfolio of alternative technologies gaining significant commercial traction. This shift is driven by the urgent need for grid resilience in the face of intermittent renewables and soaring electricity demand from data centers. The global LDES market was valued at $4.81 billion in 2024 and is projected to reach $17.00 billion by 2034, with major projects like ESS Inc.‘s 50 MWh iron-flow pilot with Salt River Project and Form Energy‘s landmark 300 MW / 30 GWh iron-air system demonstrating the move toward bankability. The dominant theme for 2025 is this technological diversification, underpinned by aggressive policy mandates, such as California’s 2 GW LDES target, and the private sector’s quest for 24/7 clean power.

Top 10 Long-Duration Energy Storage Technologies

The following ten technologies represent the leading non-lithium-ion solutions gaining commercial momentum in 2024 and 2025, offering a range of durations, costs, and applications to stabilize the future grid.

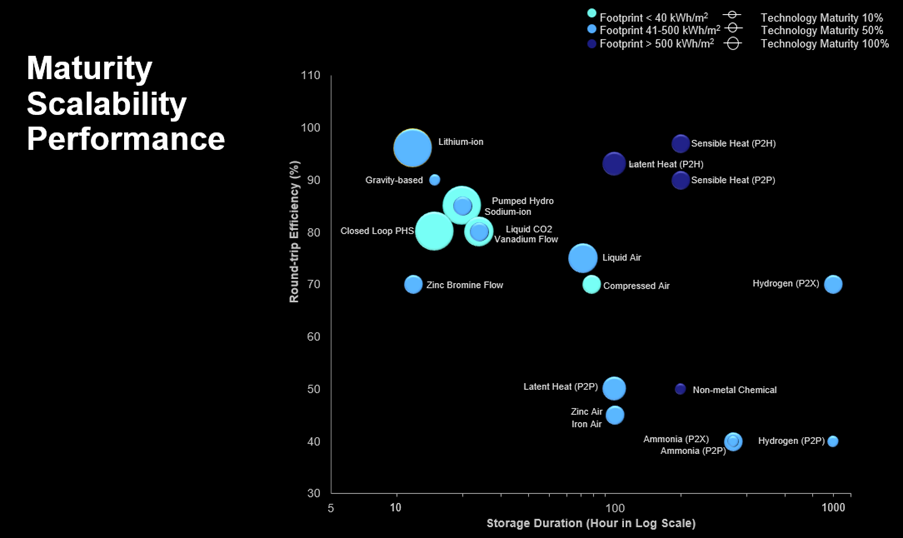

Chart Compares LDES Technologies on Key Metrics

An introductory section listing the ‘Top 10’ technologies is best accompanied by a chart that ‘Compares LDES Technologies on Key Metrics,’ offering a high-level overview.

(Source: Energy-Storage.News)

1. Iron-Air Batteries

Company: Form Energy

Installation Capacity: 300 MW / 30 GWh project with Xcel Energy

Applications: Multi-day (100+ hour) grid storage to provide year-round reliability with renewable energy.

Source: World’s ‘largest’ grid battery part of Google-Xcel Energy agreement

2. Vanadium Redox Flow Batteries (VRFB)

Company: Stryten Energy

Installation Capacity: Varies by project; scales MWh by increasing electrolyte volume.

Applications: Grid stability and long-duration applications (6-16 hours) requiring high cycle life (>20, 000 cycles).

Source: Flow Batteries: The Key to Long-Duration Energy Storage – NEWARE

3. Iron-Flow Batteries

Company: ESS Inc.

Installation Capacity: 50 MWh pilot project with Salt River Project (SRP)

Applications: Long-duration (10+ hours) flexible capacity using earth-abundant materials (iron, salt, water).

Source: SRP and ESS Announce New 50 MWh Long Duration Energy …

4. Sodium-Ion Batteries

Company: N/A

Installation Capacity: N/A

Applications: A cost-effective and safe alternative to lithium-ion for stationary storage durations beyond 4 hours.

Source: Sodium-ion battery momentum grows, but challenges remain – IEA

5. Compressed Air Energy Storage (CAES)

Company: N/A

Installation Capacity: Example projects feature 300 MW capacity for 5+ hours.

Applications: Very large-scale, long-duration (8+ hours) storage, often using underground caverns.

Source: Compressed Air Energy Storage: A Case Study

6. Liquid Air Energy Storage (LAES)

Company: Highview Power

Installation Capacity: Supported by a £377 million investment for plant development.

Applications: Geographically independent long-duration storage and grid stability services.

Source: Energy storage innovation powers Highview scale-up – UKRI

7. Gravity-Based Storage

Company: Energy Vault

Installation Capacity: Varies by system design.

Applications: Grid-scale energy storage converting potential energy from lifted weights into electricity.

Source: Top Energy Storage Stocks 2026: LDES & The Grid-Scale Buildout

8. Sand Batteries

Company: Polar Night Energy

Installation Capacity: Up to 1, 000 MWh thermal capacity.

Applications: Multi-week or seasonal thermal energy storage for district heating or industrial processes.

Source: Sand Battery – Polar Night Energy

9. Molten Salt Storage

Company: N/A

Installation Capacity: Varies; accounts for a significant portion of thermal storage.

Applications: Standalone grid storage and pairing with concentrated solar power, offering 8-12 hours of duration.

Source: Long-duration energy storage deployments rose 49% in 2025

10. Green Hydrogen

Company: N/A

Installation Capacity: Scales for seasonal storage requirements.

Applications: Very long-duration and seasonal energy shifting by converting renewable electricity to hydrogen for later use.

Source: The role of short- and long-duration energy storage in reducing the …

Table: Top 10 LDES Technology Demonstrations and Key Players

| Technology | Company / Key Player | Installation Capacity Example | Applications | Source |

|---|---|---|---|---|

| Iron-Air Batteries | Form Energy | 300 MW / 30 GWh | Multi-day grid storage | Utility Dive |

| Vanadium Flow Batteries | Stryten Energy | Scalable MWh | Grid stability (6-16 hours) | NEWARE |

| Iron-Flow Batteries | ESS Inc. | 50 MWh | Flexible capacity (10+ hours) | SRP |

| Sodium-Ion Batteries | N/A | N/A | Stationary storage (>4 hours) | IEA |

| Compressed Air (CAES) | N/A | 300 MW | Large-scale LDES (8+ hours) | World Bank |

| Liquid Air (LAES) | Highview Power | £377 M investment | Grid stability services | UKRI |

| Gravity-Based Storage | Energy Vault | Scalable | Grid-scale storage | Exoswan |

| Sand Batteries | Polar Night Energy | 1, 000 MWh (thermal) | Seasonal heat storage | Polar Night Energy |

| Molten Salt Storage | N/A | N/A | Standalone grid storage | Utility Dive |

| Green Hydrogen | N/A | Scalable | Seasonal energy shifting | Science Direct |

LDES Applications, Form Energy’s 30 GWh Project for Grid Firming

The diversity of applications highlights a strategic shift towards a portfolio approach for grid management. No longer a one-size-fits-all market, different LDES technologies are being deployed for specific use cases. Ultra-long-duration technologies like Form Energy‘s iron-air batteries are being procured to solve multi-day reliability challenges, effectively firming wind and solar generation on a near-seasonal basis. This is crucial for achieving 24/7 clean power goals, a driver behind Google‘s agreement to pair a 100-hour LDES system with its renewable energy portfolio. Meanwhile, flow batteries from companies like ESS Inc. are carving out a niche in the 10-16 hour duration market, providing daily cycling and flexible capacity. At the same time, thermal technologies like Polar Night Energy’s sand batteries are targeting an entirely different market—low-cost seasonal heat storage for district heating—demonstrating that LDES is expanding beyond purely electricity-to-electricity applications.

US Market Focus, California’s 2 GW Target for LDES

The United States is emerging as a key battleground for LDES technologies, driven by ambitious state-level policies and federal incentives. The U.S. market alone was valued at $0.86 billion in 2025 and is growing rapidly. Policy is a primary catalyst, with regulatory mandates like California’s target to procure up to 2 GW of LDES creating powerful demand signals that de-risk investment in nascent technologies. This has paved the way for landmark projects across the country, not just on the coasts. Xcel Energy‘s plan to deploy a 30 GWh iron-air system in the Upper Midwest demonstrates the growing need for long-duration assets to manage grids with high wind penetration. While the U.S. shows significant momentum, the market is global, as evidenced by Highview Power securing a £377 million investment in the UK to advance its Liquid Air Energy Storage plants.

Long-Duration Energy Storage Projects Mapped by Technology

The section’s ‘US Market Focus’ and mention of California aligns perfectly with a chart that ‘Mapped’ projects, providing a geographical visualization of technology distribution.

(Source: S&P Global)

49% Growth, Non-Lithium LDES Deployments in 2025

The LDES market is rapidly transitioning from demonstration to commercial bankability. The projected 49% growth in non-lithium LDES deployments in 2025 signals an inflection point where these technologies are becoming proven, scalable solutions. Some technologies, like Compressed Air Energy Storage (CAES), have been operational for decades and are seeing renewed interest. Others are hitting major commercial milestones. Form Energy and ESS Inc. are moving from pilot-scale to utility-scale with their iron-based chemistries, which benefit from abundant, low-cost materials that are insulated from the supply chain volatility of lithium or vanadium. The increasing number of large-scale procurements by major utilities serves as third-party validation, shifting funding from venture capital to mainstream project finance and accelerating the path to cost-competitiveness.

Non-Lithium Storage Technologies Show Steady Growth

The chart headline is a near-perfect match for the section heading ‘49% Growth, Non-Lithium LDES Deployments in 2025,’ as both focus on the growth of non-lithium technologies.

(Source: S&P Global)

Form Energy’s $20/k Wh Target for Iron-Air Storage (2025-2030)

The market’s trajectory over the next five years will be defined by whether emerging LDES technologies can meet their aggressive cost targets, particularly the sub-$20/k Wh capital cost goal pursued by innovators like Form Energy. Achieving this price point would make renewable energy paired with multi-day storage cheaper than thermal generation, fundamentally altering utility resource planning.

- Critical Signal to Watch: The real-world operational and cost data from the first wave of large-scale deployments will be paramount. Performance metrics from Form Energy’s 30 GWh project with Xcel Energy and ESS Inc.’s 50 MWh SRP pilot will set the precedent for the bankability of iron-based chemistries.

- Emerging Driver: The explosive energy demand from AI and data centers is creating an urgent need for 24/7 firm, clean power. This was highlighted by Google’s plan to use a 100-hour LDES system, providing a powerful, non-utility demand stream that could accelerate deployment faster than grid modernization alone.

- Traction Gained: Iron-based storage chemistries are rapidly gaining credibility. Their reliance on globally abundant, low-cost materials like iron, water, and air offers a stable and scalable supply chain, a decisive advantage over technologies dependent on critical minerals like lithium and vanadium.

Cost Comparison of Long-Duration Grid Storage

The section discusses a specific cost target for a single technology. This chart provides the necessary broader context by showing a ‘Cost Comparison’ across various grid storage options.

(Source: ScienceDirect.com)

The questions your competitors are already asking

This report covers one angle of the competition to commercialize long-duration energy storage technologies beyond lithium-ion. The questions that matter most depend on your work.

- Which LDES companies like Form Energy and ESS Inc. are gaining or losing ground in the race for bankability?

- What is the outlook for the deployment of iron-air and iron-flow batteries in the utility sector by 2025?

- How do multi-day iron-air batteries compare to 10-hour flow batteries on lifetime cost and performance for grid-scale applications?

- Which utilities, beyond early adopters like Salt River Project and Xcel Energy, are actively procuring non-lithium LDES solutions?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.