DAC Policy Risk: Shell $17 M Avnos Deal, $7.5 B DOE Funding Cuts, and 2 Major Hub Cancellations (2024-2026)

DAC Project Viability, Shell’s 650 k Tonne Polaris Project, and Shifting Commercial Signals

The commercial viability of large-scale Direct Air Capture (DAC) projects is fundamentally undermined by policy instability, forcing companies like Shell to prioritize more mature, economically certain point-source capture while limiting DAC exposure to venture-style investments.

- In January 2026, Shell took a Final Investment Decision on its Polaris CCS project to capture approximately 650, 000 tonnes of CO₂ annually from its Scotford refinery in Canada. This major capital commitment to point-source capture contrasts sharply with its $17 million venture investment in DAC startup Avnos, revealing a clear corporate strategy that favors proven technology and policy environments over the high-risk DAC sector.

- The precariousness of DAC project financing was exposed in late 2025 when the U.S. Department of Energy (DOE) cancelled over $7.5 billion in funding for clean energy projects. This included the termination of awards for the two largest planned DAC Hubs in Louisiana and Texas, which were expected to remove over 2 million metric tons of CO₂ annually.

- This policy reversal demonstrates the fragility of the market, which is almost entirely dependent on government incentives like the U.S. 45 Q tax credit that offers up to $180 per tonne. The political volatility of these subsidies serves as a major deterrent to the long-term, multi-billion-dollar commitments required to build hundreds of facilities.

- This marks a significant shift from the 2021-2024 period, when industry optimism was high following the initial DOE hub announcements and a series of corporate offtake agreements from buyers like Microsoft. The recent cancellations have injected a deep sense of caution into the market.

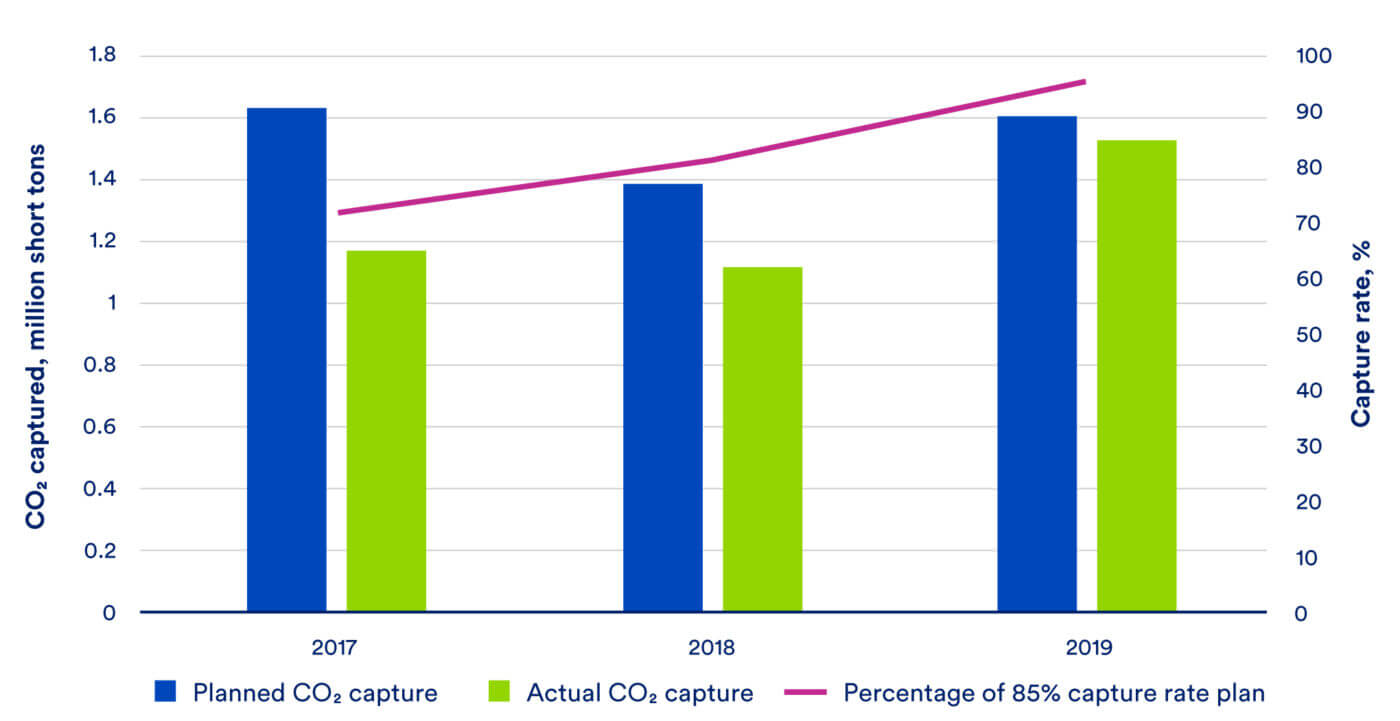

Carbon Capture Projects Underperform Planned Targets

This chart substantiates the section’s theme of questionable project viability and ‘shifting commercial signals’ by showing a historical trend of carbon capture projects failing to meet their planned targets. This data on underperformance provides a strong rationale for why the viability of new, large-scale projects like Shell’s is under scrutiny.

(Source: Clean Air Task Force)

$7.5 B in Cancellations, US DOE Halts Funding for 2 Major DAC Hubs

The most significant financial event impacting the DAC sector was not new investment but the abrupt cancellation of over $7.5 billion in U.S. Department of Energy (DOE) funding in late 2025. This action effectively halted the two largest planned DAC projects in the world and exposed the market’s extreme vulnerability to political shifts.

- The funding termination in October 2025 directly impacted Project Cypress in Louisiana, led by Battelle and Climeworks, and the South Texas DAC Hub, involving Occidental and Carbon Engineering.

- These projects were positioned as global flagships for the DAC industry, with each intended to scale up to capture at least 1 million tonnes of CO₂ per year, providing a critical pathway from pilot-scale to commercial-scale operations.

- The move creates immense uncertainty for technology developers who rely on such large-scale government programs to de-risk their initial megaton-scale plants and attract the private capital necessary for construction.

- This event marks a stark reversal from the preceding years, where the primary focus for developers was securing these initial government grants and building a book of smaller, private offtake agreements to demonstrate commercial interest.

Table: U.S. DAC Hub Project Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Project Cypress DAC Hub (Battelle, Climeworks) | October 2025 | The DOE cancelled funding for the project, which was planned to be one of two initial DAC Hubs with a capacity of over 1 million metric tons per year. The hub was a cornerstone of the U.S. strategy to scale carbon removal. | E&E News |

| South Texas DAC Hub (Occidental, Carbon Engineering, Worley) | October 2025 | Funding for the second major DAC hub was also terminated. This project was set to become one of the world’s largest DAC facilities, leveraging Occidental’s expertise in CO₂ transport and sequestration. | Heatmap News |

Visualizing the Impact of a 1M Tonne CO2 Capture Project

While the section provides a table of cancelled DAC Hub projects, this chart helps the reader visualize the real-world scale and impact of a large (1 million tonne) project. This provides crucial context for understanding the significance of the multi-hundred-kilotonne projects that were cancelled.

(Source: Renewable Carbon)

Shell $17 M Avnos Partnership Signals a Cautious Venture-Style Approach (2025)

Major energy companies are avoiding direct, large-scale DAC project partnerships, instead opting for smaller, strategic equity stakes in technology startups, as exemplified by Shell‘s $17 million joint investment with Mitsubishi in Avnos.

- Shell‘s investment in Avnos in November 2025 is directed at funding a “commercial demonstration” plant. This move indicates a strategy to acquire options on promising, next-generation technology rather than committing major capital to current high-cost DAC solutions.

- The Avnos technology is notable for its hybrid approach that captures CO₂ while also producing water, potentially lowering two of the largest operational costs for DAC and addressing a key operational constraint.

- This venture-style approach contrasts with the offtake agreement model, where companies like TD Bank Group commit to purchasing future carbon removal credits from developers like Deep Sky. These offtake deals help secure future revenue for developers but do not provide the upfront capital needed for construction.

- While the 2021-2024 period saw the formation of numerous offtake partnerships that created early market signals, the 2025-2026 period highlights a strategic pivot by players like Shell toward cautious, technology-focused venture investments.

Table: Shell DAC and Competitor Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Shell / Mitsubishi / Avnos | November 2025 | Jointly invested $17 million in project financing for Avnos to build a commercial-scale demonstration plant for its hybrid DAC technology, which captures both CO₂ and water. The goal is to validate the technology for future scaling. | Axios |

| TD Bank Group / Deep Sky | October 2024 | A 10-year offtake agreement for the purchase of over 18, 000 verified carbon dioxide removal credits. This deal helps provide revenue certainty for the DAC developer but is not a direct capital investment. | Carbon Capture Magazine |

DAC Market Forecast Shows Explosive Growth

This chart provides the market context for the competitor agreements detailed in the section’s table. The forecast of ‘explosive growth’ explains the strategic importance of these partnerships as companies, including Shell, position themselves to capture a share of a potentially massive future DAC market.

(Source: Market.us News)

US Policy Reversal, Shell’s Focus Shifts to Canadian Point-Source CCS

The United States’ position as the global leader for DAC deployment was severely damaged in late 2025 by federal funding cuts, pushing the focus for large-scale carbon management projects by companies like Shell toward more stable policy environments like Canada for its point-source CCS activities.

- The U.S. was the epicenter of announced DAC capacity, driven largely by the enhanced 45 Q tax credit and the DOE’s DAC Hubs program. The cancellation of funding for the Louisiana and Texas hubs in October 2025 has stalled this momentum and created a high-risk environment for investors.

- This represents a major negative shift from the 2021-2024 period, when the U.S. was viewed as the primary destination for DAC investment, attracting major international developers and capital.

- In contrast, Shell‘s Final Investment Decision for the 650, 000 tonne-per-year Polaris CCS project in Alberta, Canada, in January 2026 demonstrates corporate confidence in Canada’s more stable policy and regulatory framework for carbon management.

- While Polaris is a point-source capture project, not DAC, Shell‘s geographic capital allocation decision highlights a flight to policy certainty, a critical factor for any capital-intensive, long-lifecycle energy project.

Point-Source CCS to Dominate Carbon Capture Growth

The chart provides the strategic rationale for Shell’s shift in focus. By showing that point-source CCS is projected to dominate carbon capture growth, it validates the company’s decision to pivot away from the uncertainties of US DAC policy towards more established Canadian point-source projects.

(Source: Clean Air Task Force)

DAC Technology Maturity: High Costs and Energy Needs Constrain Shell’s Scale-Up

Despite advancements, Direct Air Capture technology remains commercially immature, with prohibitive costs of $400-$1, 000 per tonne and high energy intensity, preventing players like Shell from committing to gigaton-scale deployment and validating its strategy of focusing on more mature point-source CCS.

- As of early 2025, the total global operational DAC capacity was a mere 0.01 million tonnes per year. This negligible figure underscores the technology’s nascent stage and the monumental scaling challenge ahead to reach a billion-tonne ambition.

- The primary barrier is economic. A capture cost below $150 per tonne is widely seen as the tipping point for commercial viability, requiring at least a 75% cost reduction from the current range of most commercial technologies.

- Shell‘s investment in Avnos’s hybrid DAC system shows a strategic interest in next-generation technologies designed to lower operational expenditures, but this technology is still at the demonstration phase and has not proven its cost-reduction claims at scale.

- This is a continuation of the trend from 2021-2024, where the technology progressed from laboratories to small-scale pilots. However, it has not yet made the critical leap to cost-effective, megaton-scale operations, a step that the now-cancelled U.S. DAC hubs were intended to facilitate.

CO2 Capture Cost Inversely Correlated with Concentration

This chart provides a fundamental explanation for the ‘high costs and energy needs’ that constrain DAC scale-up, as mentioned in the section heading. It illustrates that capturing CO2 from ambient air (low concentration) is inherently more difficult and expensive than from a flue stack (high concentration), which is the core technological and economic barrier to scaling DAC.

(Source: Energy Industry Insights from Avanza Energy – Substack)

The Path Forward: Shell’s DAC Strategy Hinges on Policy Stability and Avnos Pilot Success

For Shell and the broader industry, the path to gigaton-scale DAC is blocked until policy risk is mitigated and a clear cost-reduction pathway is proven; the success of the Avnos demonstration plant and the future of the 45 Q tax credit are the two most critical signals to watch.

- If the Avnos demonstration plant, funded in November 2025, successfully validates its lower energy and operational cost claims, watch for Shell to make follow-on investments or announce a larger pilot project that leverages this specific technology.

- If the U.S. political climate remains volatile regarding clean energy subsidies, expect investment capital for large-scale DAC to flow towards regions with more stable, long-term policy frameworks, or for major project announcements in the U.S. to be indefinitely delayed.

- These could be happening: Other major energy companies may replicate Shell‘s risk-averse strategy by making multiple small venture bets on a portfolio of DAC technologies, diversifying their exposure instead of committing to a single technology or project.

- In the absence of reliable government subsidies, the growth of the voluntary corporate offtake market will become even more critical for providing an alternative, albeit smaller, revenue stream to keep technology developers afloat.

The questions your competitors are already asking

This report covers one angle of Direct Air Capture’s commercial viability, focusing on how policy instability is shaping corporate investment. The questions that matter most depend on your work.

- What is actually happening with the US DAC Hubs program since the major funding cancellations?

- What is the outlook for megaton-scale DAC deployment in the US following the 2025 policy reversals?

- How does Direct Air Capture compare to point-source carbon capture on commercial viability and policy risk?

- Shell’s activities in carbon capture. Is the Avnos DAC partnership progressing toward deployment at a scale comparable to the Polaris CCS project?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.