BESS Project Pipeline, 1.4 GW Anza Power Acquisition, $158 M Solar Max EPC Contract, and 5 Major Project Agreements (2025 to 2026)

BESS Commercial Adoption, EPC Firms Target $90 B Market

The Battery Energy Storage System market is accelerating into a high-growth phase, driven by compelling project economics and supportive policies, creating a substantial diversification opportunity for Engineering, Procurement, and Construction firms. This shift is marked by a rapid transition from smaller, speculative projects before 2025 to the execution of gigawatt-scale developments and strategic vertical integration to secure supply chains.

- The BESS market is projected to expand from $50.81 billion in 2025 to nearly $90 billion in 2026, propelled by the critical need for grid stability and the integration of renewable energy sources. The economic case is solidifying, with the cost of new solar-plus-storage projects now more competitive than new combined-cycle gas turbines.

- The scale of commercial projects has increased significantly since 2025. A landmark deal in January 2026 saw the acquisition of a development pipeline in Australia that includes 1.4 GW of solar and 3.4 GWh of battery storage, positioning the acquirer as a major player in one of the world’s top three BESS markets.

- EPC contract values reflect this growth. In the U.S., Solar Max Technology secured $158 million in EPC contracts in January 2026 for the construction of 400 MW of commercial solar projects, indicating robust demand for construction services in the sector.

- To mitigate supply chain risks and capture more value, some firms are vertically integrating. This is demonstrated by a joint venture formed in January 2026 between a construction leader and Neo Volta to establish a BESS manufacturing platform in Georgia, aiming to serve growing U.S. demand.

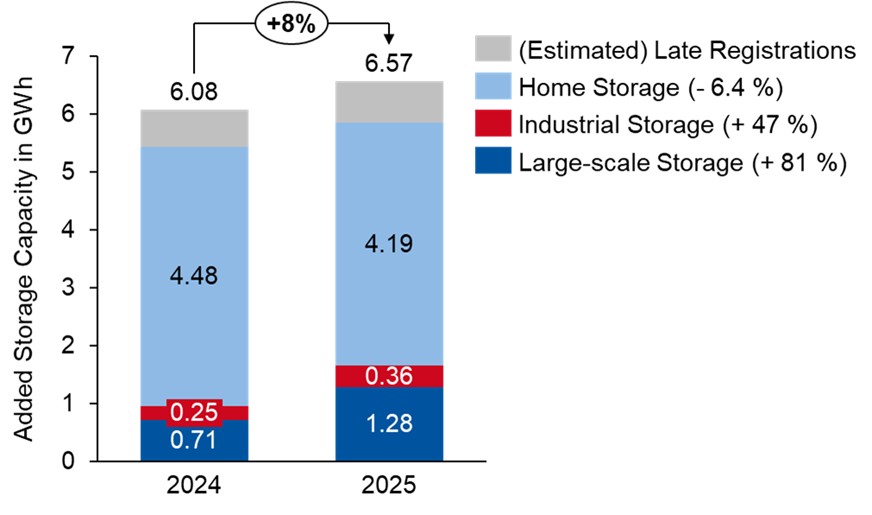

Large-Scale Storage Growth Surges 81% in 2025

This chart’s 81% growth metric directly quantifies the ‘Commercial Adoption’ mentioned in the section heading, providing strong evidence for the $90 billion market opportunity that EPC firms are targeting.

(Source: ESS News)

$1.1 B CAPEX, Murphy Oil Prioritizes Fossil Fuels Over BESS

While the renewable sector attracts massive investment, strategic divergence persists as established oil and gas companies like Murphy Oil Corporation direct their 2026 capital programs toward traditional assets. This highlights a split in capital allocation strategies within the broader energy industry, where incumbents are prioritizing returns from existing high-margin fossil fuel operations over pivoting to the burgeoning BESS market.

- Murphy Oil Corporation’s 2026 guidance allocates a $1.1 billion capital expenditure budget, with over 60% designated for high-margin offshore oil projects. This strategy shows a clear focus on maximizing returns from its core fossil fuel business rather than investing in the energy transition.

- In direct contrast, engineering and construction firms are making significant capital commitments to enter the renewables space. One construction major committed an initial $250 million as part of its joint venture to build a domestic BESS manufacturing facility in Georgia.

- The broader competitive field is also heavily invested in the energy transition. Competitor Burns & Mc Donnell reported $7.5 billion in revenue for 2025, with growth substantially driven by its work on energy-transition projects, data centers, and semiconductor facility expansions.

Solar PV Market to Reach $222B by 2035

This chart provides a counter-narrative to Murphy Oil’s strategy. By illustrating the massive long-term market value of solar (closely tied to BESS), it highlights the potential opportunity cost of prioritizing fossil fuels over renewables.

(Source: Research Nester)

Table: Strategic Investments and Capital Allocations (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Murphy Oil Corporation | 2026 | $1.1 Billion Capital Expenditure Program, with over 60% allocated to high-margin offshore oil and gas projects. The plan does not include any allocation for solar or BESS. | Matrix BCG |

| Murphy Group / Neo Volta Power, LLC JV | Jan 2026 | $250 Million initial investment to establish a domestic BESS manufacturing facility in Georgia. The purpose is to secure the supply chain for North American projects and mitigate geopolitical risks. | Quiver Quant News |

| Murphy Group Site Readiness Program | Sep 2025 | $50 Million investment to acquire and prepare land for utility-scale solar and BESS development. This initiative aims to reduce pre-construction timelines and de-risk early-stage development. | Site Selection Magazine |

Neo Volta JV, Murphy Group Secures BESS Manufacturing (2025 to 2026)

Leading construction firms are utilizing strategic partnerships and joint ventures to move up the value chain, securing technology access and domestic manufacturing capabilities to de-risk project execution. These collaborations are essential for navigating supply chain volatility and positioning for large-scale grid infrastructure contracts, moving beyond a traditional EPC role to become more integrated players in the energy transition.

- A key vertical integration move occurred in January 2026 with the formation of Neo Volta Power, LLC, a joint venture with Neo Volta Inc. This partnership will establish a BESS manufacturing plant in Georgia, backed by a $250 million initial commitment to onshore the supply chain.

- To capitalize on state-level policy, a partnership was formed in August 2025 with solar developer Verogy. This collaboration provides EPC services for a portfolio of community solar projects in New Jersey, directly leveraging new laws designed to add 3, 000 MW of capacity.

- Firms are also forming alliances to pursue major grid infrastructure work. In May 2026, a strategic alliance was established with the California Independent System Operator (CAISO) to jointly bid on transmission and utility-scale BESS projects outlined in CAISO’s ambitious 2025-2026 transmission plan.

Table: Key BESS and Solar Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Neo Volta Inc. / Potius Edge | Jan 2026 | Formation of the Neo Volta Power, LLC joint venture to establish a BESS manufacturing platform in Georgia. This move aims to serve growing U.S. demand and secure the supply chain for future EPC projects. | Quiver Quant News |

| California Independent System Operator (CAISO) | May 2026 | A strategic alliance was formed to bid on transmission and utility-scale BESS projects within CAISO’s 2025-2026 transmission plan, which is designed to support 45 GW of new solar capacity. | Mondaq |

| Verogy | Aug 2025 | EPC collaboration to construct a portfolio of community solar projects in New Jersey. The partnership was timed to capitalize on new state laws expanding the program by 3, 000 MW. | New Jersey Monitor |

Australia vs US, BESS Project Hotspots Attract EPCs

The global BESS market is concentrating in regions with strong policy frameworks, significant renewable penetration, and urgent grid modernization needs, with Australia and the United States emerging as primary hotspots for EPC and developer activity. Capital is flowing to these markets due to clear revenue opportunities and government support, creating distinct geographical centers for large-scale project deployment.

- Australia has solidified its position as one of the world’s top three markets for utility-scale BESS. This status was underscored by the January 2026 acquisition of a major development pipeline including 1.4 GW of solar and 3.4 GWh of battery projects, signaling intense interest from global construction players.

- The U.S. market is characterized by powerful state-level initiatives. In August 2025, New Jersey Governor Phil Murphy signed legislation to expand the state’s community solar program by 3, 000 MW, creating a large, localized market for developers and EPC firms like Verogy.

- California remains a critical U.S. market, driven by its aggressive decarbonization goals. The state’s grid operator, CAISO, approved a transmission plan in May 2026 to support an additional 45 GW of solar capacity, creating substantial opportunities for BESS and transmission construction.

- Canada is also an active market, particularly in regions with robust carbon pricing and renewable targets. The Jurassic BESS project in Alberta, supported by a 15-year offtake agreement, demonstrates the bankability of storage projects in the Canadian market.

German BESS Capacity To Grow Fivefold By 2026

While the section mentions Australia and the US, this chart provides a powerful, specific example of a regional ‘Project Hotspot.’ The explosive growth in Germany exemplifies the type of market opportunity that attracts EPCs globally.

(Source: ESS News)

BESS Commercial Scale, Co-located Solar and Storage is Bankable

BESS technology, especially when co-located with solar generation, has reached commercial maturity and is now considered a bankable asset class, enabling a shift from smaller pilots to gigawatt-hour scale deployments. This transition is underpinned by declining costs and the technology’s proven ability to provide essential grid services, making it a cornerstone of modern energy infrastructure planning.

- The market has progressed rapidly from the smaller-scale pilots common before 2024 to multi-gigawatt-hour projects in 2025-2026. Key examples include the 3.4 GWh BESS pipeline in Australia and the 170 MWp solar with 400 MWh BESS project in the U.S., both of which represent a new scale of commercial deployment.

- The economic viability is well-established, with hybrid solar-plus-storage projects demonstrating a levelized cost of electricity up to 10% lower than standalone projects. As costs for lithium-ion technology face supply pressures, alternative long-duration technologies like the iron-air systems developed by companies such as Form Energy are also advancing toward commercialization.

- BESS is now a fundamental component of grid planning. System operators like CAISO are designing multi-billion-dollar transmission expansions explicitly around the need to integrate vast amounts of solar and battery storage, confirming the technology’s central role in future grid architecture.

SWOT Analysis, BESS Market Opportunities vs. Policy Risks

The BESS market offers EPC firms enormous growth potential fueled by strong demand drivers and improving economics, but this opportunity is accompanied by considerable execution risks. Success will depend on the ability to manage supply chain disruptions, navigate complex interconnection queues, and adapt to a shifting and uncertain policy environment.

Global Renewable Capacity Additions Surge Through 2026

This chart directly supports the ‘Opportunities’ aspect of the SWOT analysis. The overall surge in renewable capacity is the primary driver creating the market need for BESS, setting the macro-level context for the section.

(Source: Oil Price)

Table: SWOT Analysis for BESS Market Entry by EPC Firms

| SWOT Category | 2021 – 2024 (Observed Trends) | 2025 – 2026 (Current State) | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Declining Li-ion battery costs; growing renewable deployment creating demand for grid balancing. | Demonstrated cost-competitiveness against gas peakers; strong demand from AI data centers and industrial electrification. Co-location with solar is a standard bankable model. | The economic case for BESS has been validated at scale. New demand drivers like AI have emerged, strengthening the business case beyond just renewable firming. |

| Weaknesses | Long project development cycles; reliance on nascent supply chains and incentive programs. | Severe grid interconnection backlogs in key markets like the U.S.; persistent supply chain bottlenecks for transformers and switchgear. | While BESS technology is mature, the surrounding infrastructure and supply chains have become the primary constraint, shifting the risk from technology to project execution. |

| Opportunities | Potential for federal incentives (e.g., Inflation Reduction Act); early-mover advantage in emerging markets. | Vertical integration via domestic manufacturing (e.g., Neo Volta JV); capturing 24/7 clean power contracts for AI; expanding EPC services to include grid modernization. | The IRA’s impact is now clearer, and firms are actively pursuing domestic manufacturing to capitalize on it. The AI-driven demand for power is a new, massive opportunity. |

| Threats | Geopolitical tensions affecting raw material supply; uncertainty over long-term policy support. | Policy uncertainty from potential legislative changes (e.g., the OBBBA Act) that could curtail tax credits; high interest rates affecting project financing. | Policy risk has become more acute, with specific legislative threats like the OBBBA Act creating direct uncertainty for project financing models that were built around IRA incentives. |

BESS EPCs in 2026, Execution on 3.4 GWh Pipeline is Critical

For EPC firms entering the BESS market, the primary determinant of success in 2026 will be the ability to execute on large-scale, multi-gigawatt-hour project pipelines while effectively navigating significant policy and supply chain headwinds. The focus has shifted from securing initial market entry to demonstrating tangible project delivery at an unprecedented scale.

- If EPCs successfully bring massive development pipelines, like the 3.4 GWh Australian portfolio, to financial close and begin construction, watch for a subsequent wave of industry consolidation as proven players acquire smaller development platforms to accelerate growth.

- EPCs could increasingly form exclusive partnerships with AI data center operators to develop and build dedicated 24/7 clean power solutions, creating a new, high-margin revenue stream that commands premium pricing due to its critical importance for the tech sector.

- The commissioning of domestic manufacturing facilities, such as the Neo Volta Power, LLC joint venture in Georgia, could begin to alleviate critical supply chain bottlenecks by late 2026, giving firms with local supply a significant cost and scheduling advantage on U.S. projects.

- Firms specializing in alternative battery chemistries, such as the vanadium flow batteries developed by companies like VRB Energy, may gain significant market traction if lithium-ion supply constraints and price volatility persist, offering a different value proposition for long-duration storage needs.

Battery Grid Usage Surges from 2025 to 2026

This chart directly visualizes the reason why execution is critical. The surge in grid usage creates the 3.4 GWh pipeline mentioned in the section, linking the market demand to the operational challenge for BESS EPCs in 2026.

(Source: ESS News)

The questions your competitors are already asking

This report covers one angle of the commercial opportunity for EPC firms in the high-growth solar and BESS market. The questions that matter most depend on your work.

- Which EPC firms are gaining or losing ground in the solar and BESS construction market?

- What is the outlook for gigawatt-scale BESS deployment by construction firms through 2026?

- What are the EPC and vertical integration opportunities in the $90 billion BESS market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.