Top 10 BESS Projects: 10 GWh Samsung C&T Deal, 8.5 GWh Alsym Partnership (2024-2026)

The Battery Energy Storage System (BESS) market is undergoing a fundamental shift towards gigawatt-hour-scale projects, driven by the dual demands of grid modernization and powering energy-intensive data centers. Analysis of major announcements from 2024 to 2026 reveals that multi-GWh supply agreements and project pipelines are becoming the new standard. Key data points confirming this trend include a Texas developer securing over 10 GWh of capacity for data centers, Hithium and Samsung C&T partnering on a 10 GWh global pipeline, and ESS Inc. procuring 8.5 GWh of sodium-ion cells. The dominant theme emerging through 2025 and into 2026 is this immense scaling, where BESS moves from an ancillary grid service to a core infrastructure asset class essential for both public and private sector energy security.

1. ESS Inc. & Alsym Energy Sodium-Ion Partnership

Companies: ESS Inc., Alsym Energy

Capacity: 8.5 GWh (8, 500 MWh)

Application: Strategic supply of US-made sodium-ion battery cells for stationary storage, diversifying beyond lithium-ion.

Source: ESS Inc partners with Alsym for 8.5 GWh of US na-ion BESS cells

2. Recurrent Energy Sells Texas BESS Project

Companies: Recurrent Energy, Hunt Energy Network

Capacity: 200 MWh

Application: Utility-scale BESS project contributing to the Texas grid, highlighting an active asset development and sales market.

Source: Recurrent Energy sells 200 MWh Texas BESS to Hunt Energy Network

3. Texas Developer Secures Capacity for Data Centers

Company: Unnamed Texas Developer

Capacity: Over 10 GWh (10, 000 MWh)

Application: Providing reliable power to the rapidly expanding data center industry, marking a significant new demand driver for BESS.

Source: Texas developer secures 10 GWh+ of BESS capacity to supply data …

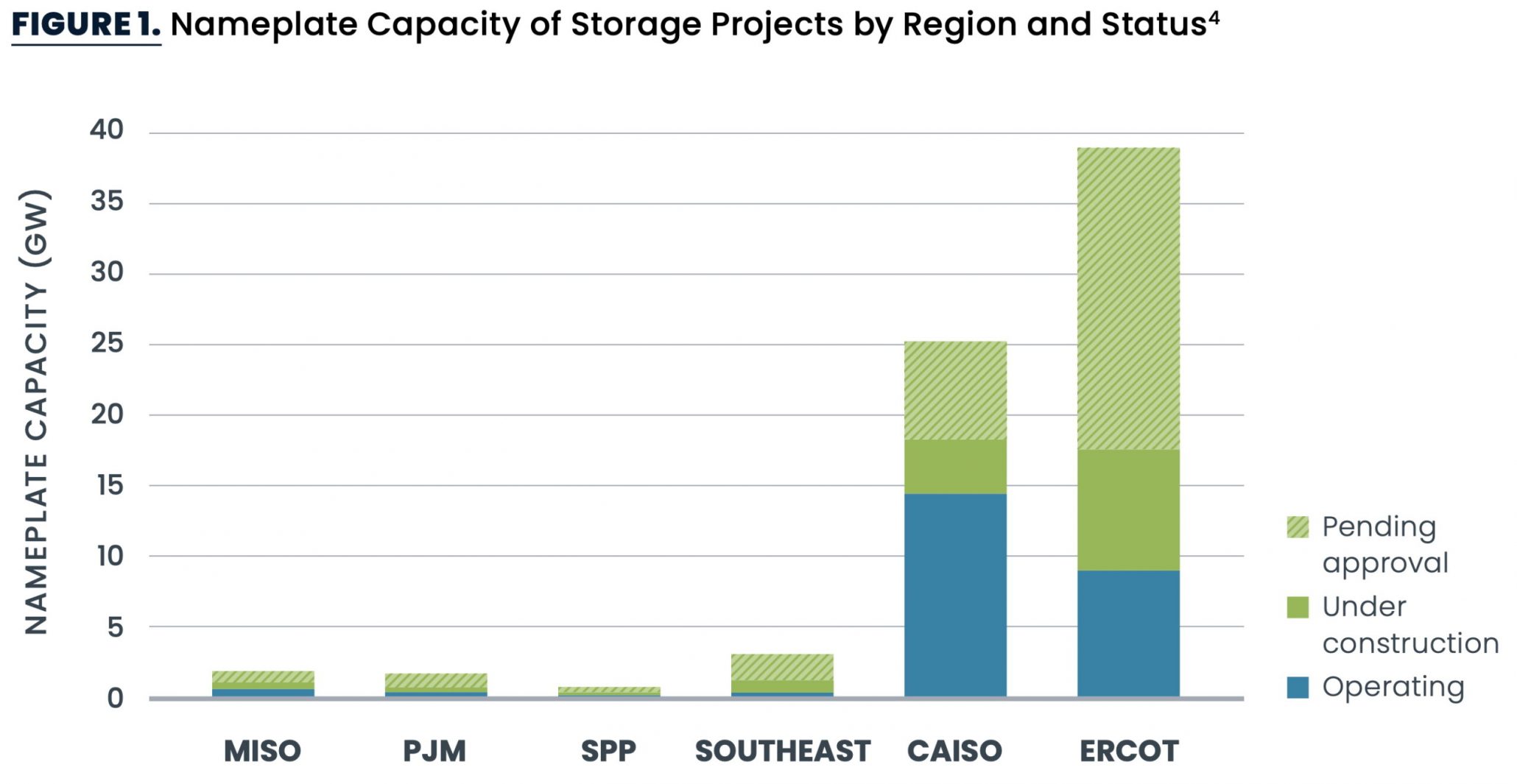

ERCOT and CAISO Dominate US Energy Storage Pipeline

The section discusses a Texas developer securing capacity for data centers. The chart is a perfect match, as ERCOT is the grid operator for most of Texas, and its dominance in the US storage pipeline explains the high level of development activity in the state.

(Source: ESS News)

4. Boralex Commissions Sanjgon BESS Project

Company: Boralex

Capacity: 80 MW / 320 MWh

Application: The company’s first North American BESS project, providing grid capacity and services in Ontario, Canada.

Source: Boralex commissions its first BESS project in North America

European BESS Market to Reach $18B by 2030

The section reports the commissioning of the Sanjgon BESS project in France by Boralex. The chart provides the broader market context, showing that the European BESS market is expanding significantly, and this project is a concrete example of that growth trend.

(Source: MarketsandMarkets)

5. RWE Launches Bavaria BESS Project

Company: RWE

Capacity: 400 MW / 700 MWh

Application: Germany’s largest BESS project at the time of its announcement, designed to enhance grid stability and integrate renewable energy.

Source: BESS — China Energy Storage Alliance

TotalEnergies & Allianz Detail German BESS Projects

The section covers RWE’s launch of a BESS project in Bavaria, Germany. The chart, which details projects from other major players in Germany, highlights the intense activity and competition within the German BESS market, providing direct context for the RWE announcement.

(Source: Energy-Storage.News)

6. Adani Group Enters BESS Sector

Company: Adani Group

Capacity: 1, 126 MW / 3, 530 MWh

Application: A large-scale project marking the company’s strategic entry into the BESS market as part of a massive renewable energy park in India.

Source: Adani Group Announces Strategic Entry into Battery Energy Storage …

BESS Market to Near $200B by 2031

The section announces the entry of a major conglomerate, Adani Group, into the BESS sector. The chart’s projection of a massive future market size provides the clear financial motivation for why a large corporation like Adani would make such a strategic move.

(Source: Mordor Intelligence)

7. Saudi Electricity Company (SEC) BESS Procurement

Company: Saudi Electricity Company (SEC)

Capacity: 1, 000 MW (combined)

Application: A large-scale procurement of multiple BESS projects to support Saudi Arabia’s grid modernization and renewable energy goals.

Source: SEC awards 1, 000 MW Battery Energy Storage System Projects

Financial Model for BESS Project Valuation

The section describes a large BESS procurement by the Saudi Electricity Company (SEC). The chart on financial modeling for project valuation is directly relevant, as such models are essential tools used in any major procurement process to evaluate bids and assess project viability.

(Source: ESS News)

8. Darden Clean Energy Project Approval

Company: Project approved by the California Energy Commission (CEC)

Capacity: 1, 150 MW / 4, 600 MWh

Application: The world’s largest approved solar-plus-storage project, combining a massive solar farm with an equally large battery system in California.

Source: CEC Approves World’s Largest Solar + Battery Storage Project in …

9. Hithium & Samsung C&T Global Partnership

Companies: Hithium, Samsung C&T Corporation

Capacity: 10 GWh pipeline

Application: A global partnership to develop a massive pipeline of BESS projects, combining manufacturing scale with project development expertise.

Source: Hithium, Samsung C&T claim 10 GWh pipeline for global BESS

China-Based Firms Lead Global BESS Integrator Market

The section reports on a global partnership between Chinese manufacturer Hithium and Samsung C&T. The chart, which shows that Chinese firms lead the global BESS integrator market, provides the context for this partnership as an example of a Chinese leader expanding its global reach.

(Source: Energy-Storage.News)

10. Sungrow & Spearmint Energy Supply Deal

Companies: Sungrow, Spearmint Energy

Capacity: Over 1 GWh (1, 000 MWh)

Application: A major supply agreement for BESS solutions to be deployed across multiple projects in Texas through 2025.

Source: Sungrow in 1 GWh+ BESS deal with US developer Spearmint Energy

Table: Top 10 BESS Announcements (Jan 2024 – Jun 2026)

| Companies | Capacity | Application | Source |

|---|---|---|---|

| ESS Inc., Alsym Energy | 8.5 GWh | Supply of sodium-ion battery cells | Source |

| Recurrent Energy, Hunt Energy Network | 200 MWh | Utility-scale BESS project sale | Source |

| Unnamed Texas Developer | 10 GWh+ | Powering data centers | Source |

| Boralex | 80 MW / 320 MWh | Grid capacity in Ontario | Source |

| RWE | 400 MW / 700 MWh | Grid stability and renewable integration | Source |

| Adani Group | 1, 126 MW / 3, 530 MWh | Large-scale renewable park storage | Source |

| Saudi Electricity Company | 1, 000 MW | Grid modernization | Source |

| CEC-Approved Project | 1, 150 MW / 4, 600 MWh | Solar-plus-storage | Source |

| Hithium, Samsung C&T | 10 GWh Pipeline | Global project development | Source |

| Sungrow, Spearmint Energy | 1 GWh+ | Supply for Texas projects | Source |

Energy Storage System Costs Drop 40% in 2024

The section discusses a major supply deal between Sungrow and Spearmint Energy. The chart, showing a significant drop in system costs, illustrates the key economic driver behind such agreements. Lower costs make BESS projects more viable, stimulating procurement and supply deals.

(Source: Energy-Storage.News)

BESS Applications, Adani Group’s 3, 530 MWh Project

The diversity of applications demonstrates the expanding role of BESS in the energy transition. Projects are moving beyond traditional grid services to become foundational infrastructure for new industries. The most striking example is the January 2026 announcement of a Texas developer securing over 10 GWh of capacity specifically to provide reliable power for data centers. This indicates a powerful new vertical market for energy storage. Concurrently, BESS remains critical for large-scale renewable integration, as shown by the Adani Group’s 3, 530 MWh project in India and California’s approval of the 4, 600 MWh Darden solar-plus-storage facility. Standard grid support remains a core function, with Boralex commissioning its 320 MWh Sanjgon project in Canada and RWE beginning construction on a 700 MWh system in Germany to bolster grid stability.

Illustration Highlights Global Scale of BESS Projects

The section focuses on a massive 3,530 MWh project by Adani Group. The chart’s headline about the ‘Global Scale of BESS Projects’ directly corresponds to the theme of the section, with the Adani project serving as a prime example of this large-scale trend.

(Source: Blackridge Research & Consulting)

US Dominance, Hithium & Samsung C&T Global BESS Pipeline

Geographically, the United States continues to lead BESS deployment, with Texas and California as epicenters of GWh-scale activity. Texas stands out with multiple major announcements, including the 10 GWh data center supply, Sungrow’s 1 GWh deal with Spearmint Energy, and Recurrent Energy’s 200 MWh asset sale, driven by favorable market structures and massive industrial demand. California’s regulatory push for decarbonization is the force behind massive projects like the 4, 600 MWh Darden facility. However, global activity is rapidly accelerating, confirming that large-scale BESS is now a worldwide phenomenon. Major procurements by the Saudi Electricity Company (1, 000 MW) and the Adani Group’s entry in India signal that emerging energy powerhouses are making substantial investments. Global supply chain integration, exemplified by the 10 GWh global pipeline partnership between China’s Hithium and Korea’s Samsung C&T, further highlights the international nature of the market.

ESS Inc. 8.5 GWh Sodium-Ion Bet Beyond Lithium (2026)

While lithium-ion technology underpins most of the currently announced large-scale projects, recent deals signal a strategic diversification in battery chemistry. The most significant development is the May 2026 partnership between flow battery manufacturer ESS Inc. and Alsym Energy for an 8.5 GWh supply of sodium-ion battery cells. This is not a demonstration project but a massive commercial agreement, indicating that non-lithium chemistries are reaching a level of maturity and scale required for grid applications. The move highlights a concerted effort within the industry to mitigate supply chain risks associated with lithium and cobalt while exploring chemistries better suited for long-duration stationary storage. This suggests a future market where lithium-ion coexists with alternatives like sodium-ion and flow batteries, each optimized for different performance and cost requirements.

10 GWh Projects, BESS Developers Target Data Centers

Expect BESS developers to increasingly forge direct partnerships with large industrial and technology clients, bypassing traditional utility procurement pathways to secure offtake for GWh-scale projects. This shift from public tender to private contract will accelerate deployment and create new financing models.

- The primary signal is the January 2026 report of a developer securing 10 GWh of BESS capacity in Texas specifically for data center clients. This establishes a clear precedent for energy storage as a direct-to-consumer infrastructure asset for high-load industries.

- The May 2026 agreement between ESS Inc. and Alsym Energy for 8.5 GWh of sodium-ion cells demonstrates that the supply chain is maturing to support these massive deals with alternative, potentially lower-cost technologies, which is critical for the economics of direct power purchase agreements.

- The commissioning of the Sanjgon BESS in January 2026 shows that as markets mature, the focus shifts from simply winning bids to successfully executing and operating large, complex assets, a capability essential for servicing demanding private clients.

North American BESS Market to Surpass $19B

The section describes a trend of developers building huge, 10 GWh projects to serve data centers. The chart, forecasting significant growth in the North American BESS market, explains the financial incentive and market size that supports these large-scale, capital-intensive developments.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of the gigawatt-hour scale-up in the BESS market. The questions that matter most depend on your work.

- Which companies are gaining ground in the GWh-scale BESS supply market?

- What is the outlook for multi-GWh BESS deployment as a core grid infrastructure asset by 2026?

- How does sodium-ion compare to lithium-ion for GWh-scale stationary storage projects?

- Which data center operators are adopting utility-scale BESS for power security?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.