BESS Supply Chain Delivery, 914 Projects vs. 63 GW Grid Queue, Spearmint Energy $450 M Financing (2025-2028)

Grid Interconnection Risk, BESS Developers Face 8.5-Year Delays for 914 Projects

The primary risk to delivering the planned 914 U.S. Battery Energy Storage System (BESS) projects by 2028 is not manufacturing capacity but systemic, non-hardware bottlenecks. While domestic system assembly is scaling rapidly, the project pipeline is colliding with severe constraints in grid interconnection and permitting, which can extend development timelines to nearly a decade and make the 2028 target for the full pipeline improbable.

- From 2025, the central challenge for BESS deployment shifted from manufacturing hardware to navigating the complex, under-resourced processes of grid integration. While U.S. factories now possess the capacity to supply 100% of domestic demand for American-built BESS systems, this production capability is rendered moot if projects cannot connect to the grid.

- The complete project lifecycle for a utility-scale BESS project can take up to 8.5 years from initial design to commercial operation, according to a July 2025 study. This timeline is fundamentally incompatible with a 2028 completion goal for any project not already in late-stage development.

- The most significant constraint is the grid interconnection queue, where an estimated 2, 600 GW of total generation and storage capacity is waiting for approval. Projects face average wait times of five to seven years, creating a severe bottleneck that paces the entire industry.

- Beyond grid access, local permitting and opposition create further delays. For example, in early 2025, Solana County, California, one of the nation’s most active BESS markets, enacted a two-year ban on new projects, demonstrating how local-level decisions can stall even the most robust development pipelines.

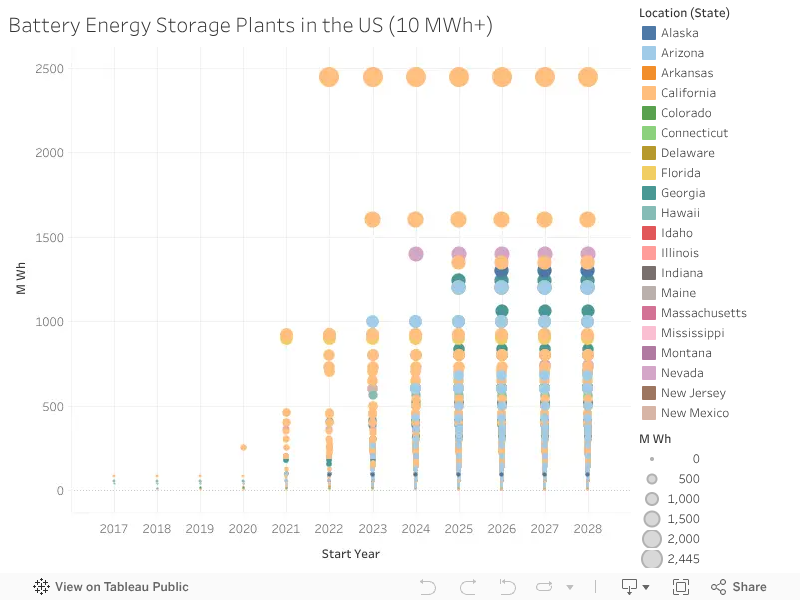

US BESS Project Pipeline Surges Through 2028

The section describes the risks and delays caused by a large project pipeline (914 projects). The chart directly illustrates the underlying cause by showing that the ‘US BESS Project Pipeline Surges,’ which explains why the grid interconnection queue is so strained.

(Source: OCBridge)

$400 B in Cancellations, Clean Energy Developers Face Policy & Economic Headwinds

The announced BESS project pipeline represents potential demand, not guaranteed deployment, with a high rate of project attrition significantly reducing the actual volume the supply chain must deliver. In 2025, economic and policy headwinds led to the cancellation of nearly 1, 900 clean power projects, underscoring the fragility of project economics and the speculative nature of a large portion of the development queue.

- In 2025 alone, 266 GW of clean power projects, valued at approximately $400 billion, were canceled. This high attrition rate demonstrates that a substantial number of projects in the pipeline will not reach commercial operation, tempering raw demand figures.

- The supply-side investment is equally fragile. In the first half of 2025, over 20 GWh of planned U.S. battery manufacturing capacity slated for 2028 was canceled due to financing challenges and policy uncertainty, highlighting the risk to future domestic component supply.

- The “One Big Beautiful Bill Act” (OBBBA) of July 2025, while preserving BESS tax credits, cut incentives for wind and solar. This indirectly threatens BESS demand by slowing the deployment of the very renewable resources that drive the need for energy storage.

Energy Storage Market to Exceed $700B by 2034

The section’s focus on ‘$400 B in Cancellations’ and ‘Economic Headwinds’ provides a stark, cautionary contrast to the massive global market potential ($700B) illustrated in the chart. The pairing highlights the gap between market opportunity and project reality.

(Source: Market.us)

Table: BESS Project Financing and Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Spearmint Energy | May 2026 | Secured a $450 million financing package for its BESS portfolio in Texas (ERCOT), demonstrating the bankability of well-structured projects with secure revenue streams. | Spearmint Energy Secures $450 Million |

| es Volta / Boxcar Energy Storage | Mar 2026 | Obtained $139.6 million in project financing for a utility-scale BESS project in Texas, highlighting continued investor confidence in the ERCOT market. | Solar Builder Mag |

| U.S. Manufacturing Pipeline | H 1 2025 | Over 20 GWh of planned battery manufacturing capacity for 2028 was canceled due to policy and financing headwinds, signaling fragility in the domestic supply chain ramp-up. | Saur Energy International |

| Good Peak | Apr 2025 | Secured $22 million in construction debt for two 10 MW / 20 MWh BESS projects in Texas, showing that financing remains available for smaller-scale, strategically sited projects. | Energy-Storage.News |

ERCOT vs. CAISO, BESS Developers See 40 GW Pipeline Strained by Grid Lock

BESS development is heavily concentrated in high-demand markets like Texas (ERCOT) and California (CAISO), which together account for a massive portion of the U.S. project pipeline. However, this geographic concentration also means these regions suffer from the most acute grid interconnection challenges, creating a paradox where the highest demand meets the highest deployment friction.

- ERCOT and CAISO lead the nation with a combined BESS pipeline of approximately 40 GW (29 GW in ERCOT and 11 GW in CAISO) under construction or pending approval. This concentration reflects strong market signals and state-level renewable goals.

- This intense regional focus has overwhelmed grid operators, contributing significantly to the interconnection backlog. While these markets were pioneers for BESS deployment between 2021-2024, from 2025 onward they have become test cases for the structural limits of grid integration capacity.

- The prevalence of short-duration (2-4 hour) BESS in these markets is creating a new challenge: revenue cannibalization and price volatility. This dynamic increases the urgency for long-duration storage solutions from companies like Form Energy to provide stability over longer periods, a need that was less critical in the earlier stages of deployment.

- The problem is not limited to utility-scale projects. The power demands of new AI data centers, also concentrated in these regions, are creating a new layer of grid strain and an urgent need for behind-the-meter storage that must also navigate complex local utility interconnection rules.

Battery Storage to Comprise 29% of 2025 Capacity Additions

The chart provides critical context for why regional grids like ERCOT and CAISO are ‘strained.’ It shows that battery storage is becoming a significant portion of all new capacity, explaining the source of the ‘Grid Lock’ mentioned in the section.

(Source: PV Tech)

BESS Integrators Shift to LFP, Mature Tech Faces Deployment Barriers (2024-2026)

The core BESS technology, particularly Lithium Iron Phosphate (LFP) chemistry, is commercially mature and cost-effective, but this technological readiness is increasingly overshadowed by downstream deployment barriers. The industry’s primary challenge is no longer technology development but the physical and administrative logistics of deploying proven systems at scale.

- Between 2021 and 2024, the market began a decisive shift away from Nickel Manganese Cobalt (NMC) chemistry towards LFP for stationary storage, a trend that solidified in 2025-2026. LFP’s advantages in lower cost, enhanced safety, and longer cycle life, along with reduced exposure to volatile cobalt and nickel prices, made it the dominant choice.

- This technological maturity means that for the 2028 pipeline, the problem is not a lack of viable hardware. Instead, bottlenecks are emerging in the supply of Balance of Plant (BOP) components, such as high-voltage transformers, and in the “soft infrastructure” of permitting and grid studies.

- While the technology is ready, the supply chain remains concentrated. Chinese manufacturers like CATL and LONGi continue to dominate the LFP cell market, creating dependencies that expose U.S. projects to geopolitical and trade policy risks.

- Emerging technologies like sodium-ion batteries are advancing but are not yet at the scale needed to impact the 2028 timeline. For the current pipeline, the focus is on deploying existing LFP technology, a task constrained by logistics, not innovation.

US BESS Factory Count Projected to Grow by 2028

The section discusses a technology shift (LFP) and ‘Deployment Barriers.’ The chart complements this by showing the domestic manufacturing response, illustrating how the ‘US BESS Factory Count’ is growing to support deployment and new technologies.

(Source: OCBridge)

SWOT Analysis, US BESS Market Faces 914-Project Pipeline Challenge

An analysis of the U.S. BESS market reveals that its considerable strengths in policy support and market demand are directly undermined by profound weaknesses in grid infrastructure and significant external threats from trade policy and economic instability. This dynamic creates a high-stakes environment where project success is contingent on navigating factors far outside a developer’s direct control.

Table: SWOT Analysis for US BESS Supply Chain Delivery

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | IRA provided a 30% ITC for co-located storage. Falling lithium-ion costs improved project economics. Growing renewable penetration created clear demand signals. | Standalone storage ITC survived the OBBBA of 2025. Demand from AI data centers emerged as a major new driver. Domestic system assembly capacity reached 100% of U.S. demand. | The strategic importance of BESS was validated when its tax credits were protected from cuts, solidifying investor confidence and separating it from solar/wind policy risks. |

| Weaknesses | Grid interconnection queues were growing. Permitting was complex and inconsistent across states. Heavy reliance on Asian supply chains for battery cells. | Interconnection queues became the primary bottleneck, with 5-7 year wait times. Permitting timelines extended to as long as 8.5 years. Upstream cell supply remains a key import dependency. | The central constraint definitively shifted from manufacturing capacity to “soft infrastructure” like grid access and permitting, confirming these as the key barriers to deployment. |

| Opportunities | FERC Order 841 enabled storage to participate in wholesale markets. States like CA, NY, and TX established aggressive storage targets. | FERC Order 2023 aims to reform interconnection queues. New revenue streams from Virtual Power Plants (VPPs) are developing. Sodium-ion offers a future non-lithium alternative. | The explosive growth of AI data centers created an entirely new, massive, and immediate demand source for BESS to provide grid stability and fast-response capacity. |

| Threats | Supply chain disruptions from the pandemic. Concerns over potential tariffs on Chinese components. Rising interest rates began to pressure project financing. | High tariffs could increase BESS project costs by up to 50%, leading to cancellations. Sustained high interest rates continue to strain project IRRs. A potential market contraction was forecast for 2026. | Trade policy risk became more concrete, with analysis showing tariffs could render many projects unviable. The threat moved from theoretical to a primary factor in financial models. |

2, 600 GW Backlog, BESS Developers Hinge on Interconnection Reform

The single most critical factor for the U.S. BESS market in the near term is the effective implementation of grid interconnection reform. Without a clear path to connect projects to the grid in a timely and cost-effective manner, the ambitious project pipeline will remain largely unrealized, regardless of manufacturing capacity or project demand.

- If this happens: Federal and state efforts to streamline interconnection, such as FERC Order 2023’s “first-ready, first-served” cluster studies, are successfully implemented and widely adopted by grid operators.

- Watch this: Key metrics to monitor are the quarterly volume of generation and storage capacity clearing interconnection studies, a reduction in the average queue wait time, and the number of projects reaching financial close after receiving an interconnection agreement.

- These could be happening: A successful reform would unlock a wave of BESS projects to move from speculative development to construction, validating the thesis that deployment bottlenecks were the primary constraint. Conversely, a failure to reform the process will lead to more project cancellations, a likely market contraction as forecast by some analysts, and a continued stall in the energy transition.

The questions your competitors are already asking

This report covers one angle of the BESS deployment challenge: the non-hardware bottlenecks threatening the US project pipeline. The questions that matter most depend on your work.

- What is the actual status of the 914 planned BESS projects, and how many are at risk of missing the 2028 deadline due to non-hardware delays?

- What is the outlook for the 63 GW of BESS in the grid interconnection queue, and what are the financial risks for developers?

- What are the opportunities for firms that specialize in accelerating grid interconnection and permitting for BESS projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.