BP DAC Strategy, $5 B Spending Cut vs Occidental’s $1.3 B Stratos Project (2024 to 2026)

BP Strategic Pivot Creates Divergence in Carbon Capture Adoption

BP’s 2025 strategy marks a significant pivot away from capital-intensive, early-stage decarbonization technologies like Direct Air Capture (DAC), creating a clear strategic divergence from competitors who are aggressively investing to establish first-mover advantage. The company is prioritizing near-term financial performance from its core oil and gas operations, positioning itself as a market observer in the DAC sector while competitors like Occidental Petroleum commit billions to commercial-scale projects.

- Before 2025, BP was an active partner in large-scale, point-source Carbon Capture and Storage (CCS) projects in the UK, such as its collaboration with Equinor and Total Energies. This demonstrated a focus on decarbonizing existing industrial emissions.

- Starting in 2025, BP‘s strategy shifted, marked by a $5 billion reduction in planned energy transition spending and a renewed focus on upstream oil and gas production. This reflects a “selective and with discipline” approach to low-carbon investments.

- This caution is underscored by reports in May 2026 that BP is exploring the sale of its stakes in its flagship UK CCS projects, signaling a potential retreat from large-scale carbon management infrastructure.

- In sharp contrast, Occidental is moving forward with its $1.3 billion ‘Stratos’ DAC facility in Texas, which is scheduled to launch by the end of 2025 and capture approximately 850, 000 tonnes of CO 2 annually.

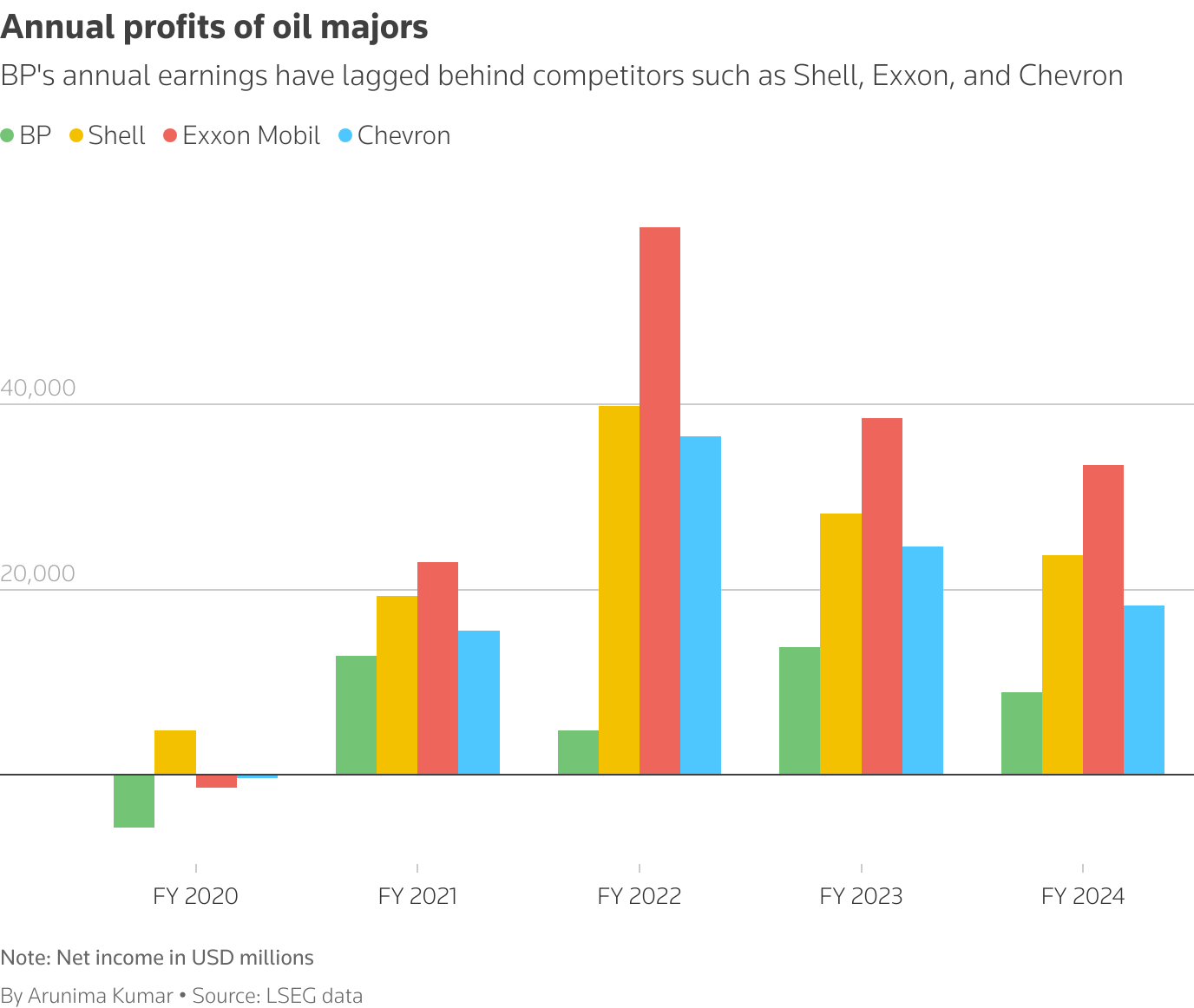

BP Profits Lag Behind Oil Major Peers

This chart shows BP’s underperformance in profitability compared to its peers, offering a compelling financial reason for the strategic pivot and shift in its carbon capture strategy mentioned in the heading.

(Source: Reuters)

$5 B Transition Spending Cut Shows BP Prioritizing Oil & Gas

BP‘s capital allocation in 2025 confirms a strategic deprioritization of its low-carbon business in favor of maximizing returns from its legacy fossil fuel assets. This move conserves capital and avoids the high financial risks associated with the uncertain cost-reduction trajectory of DAC, but it stands in stark opposition to the heavy investment seen from direct competitors.

- In February 2025, BP announced a strategy reset that included cutting planned energy transition spending by $5 billion to increase investment in its oil and gas business.

- This was followed by a revision of its low-carbon investment targets in April 2025, scaling back from a previously planned $4 billion per year in low-carbon initiatives.

- This financial caution contrasts with Occidental‘s deployment of $1.3 billion in capital for its Stratos DAC hub, a project underwritten by strong policy incentives like the US 45 Q tax credit.

- Furthermore, Occidental is exploring a new joint venture with ADNOC for another DAC facility with a potential investment of up to $500 million, demonstrating continued appetite for large-scale capital deployment in the sector.

Energy Outlooks Show BP’s Reliance on Gas

The chart visually confirms BP’s significant dependence on natural gas, providing a clear rationale for the company’s strategic decision to cut transition spending and prioritize its core oil and gas operations.

(Source: RFF.org)

Table: Investment in Carbon Capture Technologies (BP vs. Occidental)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Occidental (Stratos DAC Hub) | 2025 | $1.3 billion investment for the launch of a commercial-scale DAC facility in Texas with a capacity of 850, 000 tonnes per year. | Energy Capital HTX |

| Occidental / XRG (JV Evaluation) | May 2025 | Evaluation of a joint venture for a 500, 000 tonne/year DAC facility, with XRG considering an investment of up to $500 million. | Gas Compression Magazine |

| BP (Strategic Capital Re-allocation) | February 2025 | A $5 billion reduction in planned spending for energy transition initiatives to redirect capital towards the oil and gas sector. | Offshore Energy Biz |

BP’s CCS Alliances vs Occidental’s DAC Joint Ventures (2025 to 2026)

Partnership activity clearly delineates the differing strategic priorities between BP and its competitors. While BP has engaged in broad collaborations for conventional, point-source CCS, Occidental is building a focused ecosystem of technology and financial partnerships specifically to scale Direct Air Capture.

- BP‘s primary carbon capture partnership involves Equinor and Total Energies to develop CCS infrastructure for industrial clusters in the UK. This focuses on capturing emissions at the source.

- The long-term viability of this collaboration is now in question, as BP was reported in May 2026 to be seeking buyers for its stakes in these very projects.

- In contrast, Occidental‘s partnerships are DAC-centric. It has agreements to evaluate joint ventures with both ADNOC and XRG for new 500, 000-tonne-per-year DAC plants in Texas, with each deal potentially valued at $500 million.

- Occidental‘s strategy is further reinforced by a technology partnership with Carbon Engineering and a $500 million investment from Black Rock for its STRATOS DAC hub.

Carbon Removal Market to Reach $3.2B by 2035

This chart quantifies the future market opportunity that both BP and Occidental are targeting, providing the economic context for their differing strategic investments in carbon capture technologies.

(Source: Precedence Research)

Table: Strategic Carbon Capture Partnerships

| Lead Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Occidental / ADNOC | May 2025 | Exploration of a joint venture to construct a 500, 000 tonnes/year DAC facility in Texas, marking a significant international collaboration. | ESG Today |

| BP / Equinor / Total Energies | Jan 2025 | Collaboration to secure investment for UK point-source CCS projects. BP is now reportedly seeking to divest its stake. | Carbon Credits.com |

| Siemens Energy / Occidental | Jan 2025 | Siemens Energy is a partner in the DOE-backed Teras Direct Air Capture Hub, which includes Occidental, to advance regional DAC development. | Department of Energy |

US vs UK, BP’s Geographic Focus Shifts from Carbon Capture

The global geography of carbon capture development is becoming highly concentrated, with North America emerging as the clear leader for DAC investment due to strong policy support. BP‘s focus on the UK market now appears to be weakening, placing it outside the primary nexus of DAC innovation and deployment.

- The United States, particularly Texas, has become the global hub for DAC development, driven by the lucrative 45 Q tax credit that offers up to $180 per ton for stored CO 2 from DAC. This is where Occidental is concentrating its multi-billion-dollar investments.

- By 2025, North America is projected to account for 91% of the world’s CO 2 removal capacity, underscoring the powerful influence of US policy in shaping the market.

- BP‘s carbon capture activities have been centered on the UK, through its involvement in projects like the Viking CCS and East Coast Cluster.

- However, the reported move to sell its stakes in these UK projects suggests a strategic withdrawal from large-scale carbon management in its home market, further distancing the company from the centers of global DAC growth.

DAC Technology Risk, BP Avoids TRL 6-7 Investment

BP‘s current strategy is a calculated decision to avoid the significant technical and financial risks associated with scaling DAC technology, which remains at an early stage of commercial maturity. While competitors work to drive down costs, BP is adopting a wait-and-see approach, a move that conserves capital but risks creating a long-term technology and market share gap against carbon capture leaders.

- DAC technology is currently estimated to be at a Technology Readiness Level (TRL) of 6-7, signifying that it has been demonstrated at a pilot scale but is not yet proven at full commercial scale.

- The primary barrier to widespread adoption is cost, with current estimates ranging from $400 to $1, 000 per ton of captured CO 2, well above the value of most incentives and carbon credits.

- Companies like Occidental, through projects like Stratos, are taking on the risk of scaling the technology with the goal of driving costs down the experience curve.

- BP is opting to let competitors de-risk the technology. This strategy is financially prudent in the short term but risks leaving the company far behind if costs fall rapidly and first-movers lock up supply chains, offtake agreements, and intellectual property.

DAC Viability Hinges on Technological Breakthroughs

The chart’s headline directly supports the section’s theme of technological risk and immaturity in Direct Air Capture (DAC), explaining BP’s cautious investment approach toward TRL 6-7 technologies.

(Source: Nature)

SWOT Analysis of BP’s DAC Strategy

BP‘s 2025 strategic realignment strengthens its near-term financial position by focusing on proven assets, but it introduces significant long-term threats related to competitiveness in a future, deeply decarbonized energy system. The decision to observe rather than lead in the DAC market is a high-stakes choice with lasting implications.

BP Stock Performance Trails Competitor Shell

This chart, highlighting BP’s stock underperformance against a key competitor, directly illustrates a major ‘Weakness’ or ‘Threat’ that would be a cornerstone of the SWOT analysis for BP’s strategy.

(Source: Reuters)

Table: SWOT Analysis for BP’s Carbon Capture Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Participation in large, multi-partner CCS projects (East Coast Cluster), leveraging existing industrial integration. | Strong capital discipline, focus on maximizing returns from core oil and gas assets. Avoids high-risk, high-cost technology ventures. | The company validated its short-term financial optimization strategy by cutting $5 B in transition spending to bolster its core business. |

| Weaknesses | Lack of distinct, company-led DAC projects or proprietary technology development. Reliance on partnerships for CCS execution. | No institutional expertise in DAC. Potential reputational damage from pivoting away from stated climate ambitions. | The absence of any announced DAC projects in 2025, while competitors launched multi-billion dollar initiatives, confirmed a growing capability gap. |

| Opportunities | Leverage UK government support for CCS to build a carbon management business. | Act as a “fast follower” if competitors successfully de-risk DAC technology and costs decline. Acquire a DAC technology company later. | BP‘s opportunity to wait for technology maturation was validated by the high upfront cost ($1.3 B) of Occidental‘s Stratos project. |

| Threats | Falling behind competitors like Occidental who were making early moves in DAC. | Being locked out of a critical future market for negative emissions. Losing market share and technology leadership to first movers. Sustained pressure from ESG investors. | The threat became concrete with Occidental‘s plans to launch Stratos in 2025 and explore further JVs, solidifying its market-leading position. |

BP’s 2026 Watch List: Stratos Performance and UK Asset Sales

The most critical factor influencing BP‘s future DAC strategy is the operational and economic performance of competitor projects. The success or failure of Occidental‘s Stratos plant will be the primary external signal determining whether BP reconsiders its observer status and accelerates its own entry into the market.

- If Stratos operates successfully and shows a path to lower costs, watch for BP to potentially make a strategic acquisition of a DAC technology startup or announce a pilot project in late 2026 or 2027 to begin building internal expertise.

- If BP completes the sale of its UK CCS assets, this would confirm a broader retreat from carbon management infrastructure. This could mean the company is doubling down on its oil and gas focus or reallocating capital to other transition areas like hydrogen or biofuels.

- The cost-per-ton data from Stratos and other large-scale DAC projects will be a key metric. A rapid cost decline below the $400/ton mark could invalidate the economic rationale for BP‘s cautious stance and increase pressure to engage.

- Monitor for new policy incentives in Europe. While the US 45 Q credit is driving American projects, the introduction of a similar, powerful incentive mechanism in the UK or EU could alter BP‘s investment calculus for DAC in its home markets.

Fossil Fuels Retain ~80% Share of Energy Mix

This chart establishes the macro energy context, showing the persistent dominance of fossil fuels. This underscores the critical importance of the items on the 2026 watch list, such as carbon capture project performance.

(Source: REN21)

The questions your competitors are already asking

This report covers one angle of the strategic divergence in carbon capture adoption among oil and gas majors. The questions that matter most depend on your work.

- Which oil and gas majors are gaining or losing ground in the commercial-scale DAC and CCS market?

- What is the outlook for large-scale DAC deployment by oil and gas operators by 2030?

- What is actually happening with BP’s planned sale of its UK CCS project stakes since the May 2026 reports?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.