Canada DAC Policy, 60% Tax Credit Attracts Carbon Capture Inc., $11 M Deep Sky Financing, and 3 Project Announcements (2025)

Deep Sky & Carbon Capture Inc. 3 DAC Projects Shift to Canada (2025)

Canada’s aggressive 2025 policy incentives directly caused a shift in commercial Direct Air Capture pilot project activity, attracting international developers and accelerating technology validation on Canadian soil. This strategic pivot uses public funds to de-risk a nascent industry, successfully positioning Canada as a preferred location for early commercial deployments over the United States. The movement indicates a clear transition from foundational research and development to the deployment of commercially-oriented pilot projects, a critical step in the path toward large-scale carbon removal.

- Prior to 2025, Canada’s carbon management sector was characterized by a strong research base, including companies like Svante and Carbon Engineering, and foundational infrastructure like the Alberta Carbon Trunk Line. However, it lacked significant, dedicated Direct Air Capture project announcements.

- The pivotal event in 2025 was US-based Carbon Capture Inc. relocating its first commercial pilot project from Arizona to Canada. The company explicitly cited the stability and generosity of Canada’s new 60% Investment Tax Credit (ITC) for DAC capital expenditures as the primary driver for the move.

- Montreal-based Deep Sky further solidified this trend, announcing plans in October 2025 for a large-scale DAC facility in Manitoba slated for a 2026 start-up. The company also initiated a smaller pilot project in Alberta to deploy pioneering DAC technology from GE Vernova.

- This activity contrasts with the larger-scale projects in the U.S., such as 1 Point Five’s 500, 000 tonne-per-year Stratos facility in Texas. Canada’s strategy is currently winning smaller, first-of-a-kind commercial pilots, which are essential for operational learning and technology validation. This trend highlights the developing DAC market and its key players.

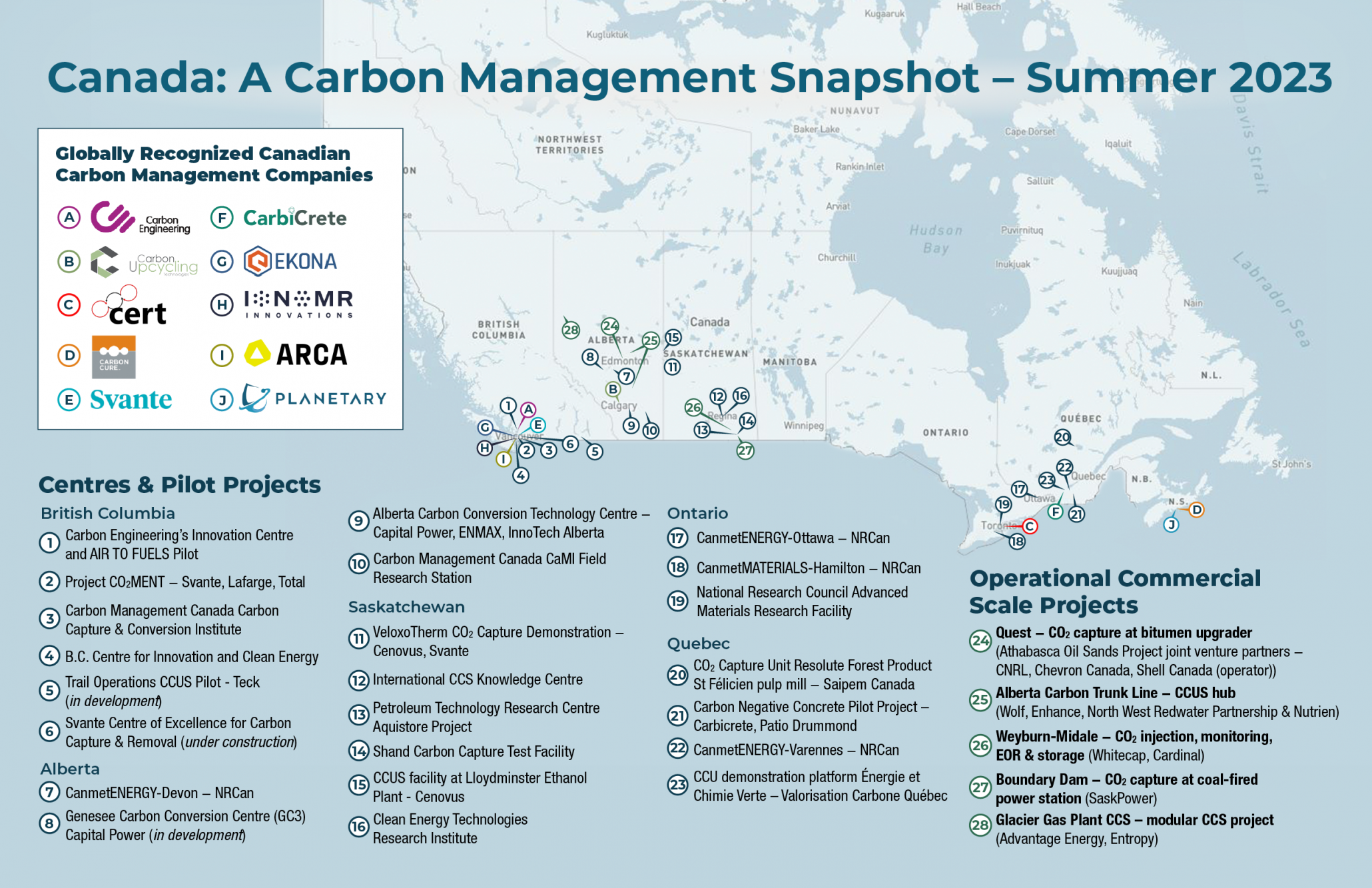

Map Details Canada’s Carbon Management Project Landscape

The section discusses specific projects shifting to Canada. The map provides the direct geographical context, showing where these and other carbon management projects are located across the country, visually grounding the article’s central news.

(Source: Natural Resources Canada – Canada.ca)

$11 M Credit Facility, Deep Sky Secures Financing for DAC Projects

The 2025 policy stack, led by the 60% capital expenditure credit, has begun to unlock project-level financing and attract corporate capital essential for building the first wave of Canadian DAC facilities. These early financial commitments, though modest, validate the government’s strategy of using public incentives to make high-cost, early-stage projects bankable. This initial flow of capital is critical for bridging the gap until technology costs decline and larger, traditional project financing becomes accessible.

- In September 2025, Deep Sky secured a crucial $11 million credit facility from Finalta Capital. This first-of-its-kind financing arrangement is specifically structured to allow the company to borrow against future government tax credits, providing upfront capital to advance its carbon removal projects in Canada.

- Corporate offtake agreements are emerging as a vital revenue source, signaling market confidence. In October 2025, Microsoft signed a significant agreement to purchase 626, 000 tonnes of carbon removal credits from a Canadian Bioenergy with Carbon Capture and Storage (BECCS) project developed by Svante and the Meadow Lake Tribal Council. This deal demonstrates strong corporate demand for high-quality, durable carbon removal credits originating from Canada, underpinning the business case for future DAC projects.

- International corporate interest is also materializing through direct technology investment. In February 2025, Rep Air Carbon Capture announced a commercial agreement with Shell and Mitsubishi Corporation valued at up to $3 million to advance its DAC technology, highlighting how global energy majors are allocating capital to promising technologies with a potential foothold in the Canadian market.

OECD Outlines Blended Finance Principles for 2025

This section reports on a specific credit facility for Deep Sky. The chart on OECD’s blended finance principles offers a macro-level framework, contextualizing the specific deal within the broader strategies used to finance capital-intensive climate technologies.

(Source: OECD)

Table: Notable 2025 Canadian Carbon Removal Investments and Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Svante & MLTC / Microsoft | Oct 2025 | Microsoft signed a CDR Offtake Agreement to purchase 626, 000 tonnes of credits from a BECCS facility. This validates corporate demand for high-quality Canadian carbon removal credits. | Svante |

| Deep Sky / Finalta Capital | Sep 2025 | Deep Sky secured an $11 million credit facility. The financing structure is designed to leverage government tax credits to provide upfront project capital. | Deep Sky |

| Rep Air Carbon Capture / Shell & Mitsubishi | Feb 2025 | A commercial agreement valued at up to $3 million was signed to fund the development of Rep Air’s DAC technology, showing international corporate investment in the sector. | CDR.fyi |

Carbon Removal Purchases Quadrupled in 2025

The section is a table detailing 2025 investments and agreements. A chart showing that purchases quadrupled in the same year provides the high-level market trend that explains the surge in investment activity listed in the table.

(Source: Carbon Removal Updates – Substack)

Canada vs. USA, Carbon Capture Inc. DAC Policy Arbitrage

In 2025, Canada successfully executed a policy arbitrage strategy to establish itself as the preferred North American jurisdiction for early-stage DAC commercialization, directly pulling at least one significant project away from the United States. This was achieved by offering more attractive upfront capital support compared to the production-based incentives available in the U.S. While America still leads in announced large-scale capacity, Canada’s approach has proven more effective at securing the critical first wave of pilot and demonstration facilities.

- Prior to 2025, the U.S. was the presumptive leader for DAC deployment, anchored by the Inflation Reduction Act’s 45 Q tax credit, which offers up to $180 per tonne, and major projects like 1 Point Five’s Stratos facility.

- The most significant validation of Canada’s strategy occurred in October 2025 with Carbon Capture Inc.’s decision to relocate its first commercial pilot from Arizona to Alberta. The company’s leadership explicitly stated that Canada’s 60% refundable capital expenditure tax credit provided greater financial certainty for a first-of-a-kind project than the U.S. production-based credit.

- Canadian DAC activity is now concentrating in Western Canada, particularly Alberta and Manitoba. These provinces offer abundant low-cost energy, favorable geology for permanent CO₂ sequestration, and established industrial expertise in managing large energy projects.

Government Policy a Key Driver for Carbon Capture

The section analyzes the policy differences between Canada and the USA. The chart’s headline directly supports the section’s premise, confirming that government policy is a critical factor, thus making ‘policy arbitrage’ a valid strategic consideration.

(Source: Coherent Market Insights)

DAC Technology Pilots, Deep Sky and GE Vernova Target Cost Reduction

Canadian Direct Air Capture initiatives in 2025 are centered on technologies at a Technology Readiness Level (TRL) of 6 to 7, a crucial phase focused on moving systems from controlled R&D settings to operational pilots in relevant industrial environments. The primary objective of these deployments is not large-scale carbon removal but rather to gather operational data, validate performance, and accelerate the innovation required to reduce the technology’s prohibitively high costs. Canada’s policy framework is effectively subsidizing this essential, high-cost learning phase.

- The period before 2025 was defined by foundational technology development from DAC leaders in Canada, but operational pilots were not the main focus within the country. The acquisition of B.C.-based Carbon Engineering by Occidental Petroleum underscored the value of Canadian-developed intellectual property.

- In 2025, the focus shifted to in-field validation. The planned GE Vernova pilot with Deep Sky, for instance, is a 1, 500 tonne-per-year system designed specifically to advance and de-risk GE’s proprietary sorbent-based DAC technology in a real-world setting.

- The fundamental technological barrier remains cost. As of October 2025, operational costs for current DAC technologies are cited in the range of $600 to $1, 000 per tonne of CO₂, figures confirmed by operators like Carbon Capture Inc. This is substantially higher than the sub-$200 per tonne level widely considered necessary for economically viable, large-scale deployment without heavy reliance on subsidies.

Chart Outlines Uses for Captured Carbon Dioxide

The section discusses technology pilots aimed at capturing carbon. This chart is a logical fit as it illustrates the end-use applications and potential value chains for the CO2 that the pilot technologies are being developed to capture.

(Source: Natural Resources Canada – Canada.ca)

SWOT Analysis, Canada’s DAC Policy Strengths and Commercialization Gaps

Canada’s primary strength in 2025 is its world-leading policy stack, which has successfully attracted international attention and early-stage projects. However, this strength is counterbalanced by the significant weakness of a nascent domestic industry facing high technology costs and the overarching threat of future policy instability. The opportunity lies in leveraging the current policy window to drive down the cost curve before incentives potentially change.

- Strengths: The combination of a 60% ITC for DAC, a federal offset protocol, and the Canada Growth Fund’s offtake agreements creates an unmatched financial incentive package.

- Weaknesses: The current cost of DAC technology, at $600-$1, 000 per tonne, makes projects entirely dependent on subsidies and far from being commercially competitive with other carbon abatement methods.

- Opportunities: Canada can become a global hub for DAC technology validation, using its policy advantage to attract more developers and build a first-mover advantage in a future multi-trillion-dollar industry.

- Threats: The long-term viability of these projects is exposed to political risk, as future governments could alter carbon pricing mechanisms or investment tax credits, creating uncertainty for long-term investors.

Canadian Net-Zero Pathways Require Carbon Removal

This section provides a SWOT analysis of Canada’s DAC policy. The chart establishes the fundamental ‘why’—the strategic necessity of carbon removal for meeting national net-zero goals—which serves as the foundational ‘Opportunity’ in the SWOT analysis.

(Source: Nature)

Table: SWOT Analysis for Canada’s Direct Air Capture Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong carbon management R&D base (e.g., Carbon Engineering, Svante); existing CO 2 infrastructure (Alberta Carbon Trunk Line). | World-leading 60% DAC ITC, a federal offset protocol for DAC, and the introduction of Carbon Credit Offtake agreements by the Canada Growth Fund. | The federal government translated R&D leadership into a powerful, targeted commercialization policy that is actively attracting investment. |

| Weaknesses | Lack of dedicated DAC policy incentives; few commercial-scale project announcements. Brain drain risk to U.S. | Prohibitively high technology costs ($600-$1, 000/tonne); operational capacity is negligible (projects are small pilots of a few thousand tonnes/year). | Policy solved the incentive problem but exposed the stark reality of the technology’s high cost and low commercial maturity. |

| Opportunities | Potential to leverage R&D leadership and geological storage advantages into commercial projects. | Attract international projects (validated by Carbon Capture Inc.); use pilots to drive down costs; meet rising corporate demand for high-quality credits (Microsoft deal). | Canada proved it can win projects from the U.S. The opportunity is now to convert these wins into a sustainable, cost-competitive industry. |

| Threats | Losing R&D talent and companies to more aggressive policy environments like the U.S. Inflation Reduction Act. | Future changes to carbon pricing and incentive programs after the next federal election create investor uncertainty. Failure to reduce costs before subsidies wane. | The threat shifted from losing R&D to the risk that the entire nascent industry, built on current policy, could collapse if political support falters. |

North America Leads the Global DAC Market

This section, a table-based SWOT analysis, is contextualized by the chart showing North America’s leadership position. This highlights a key ‘Strength’ or ‘Opportunity’ for Canada, which is a major player within this leading market.

(Source: TechSci Research)

Beyond 2025, Deep Sky’s Next Move in Canadian DAC

The critical signal to watch in the next 12 to 18 months is whether Canada’s powerful policy incentives can successfully shepherd announced projects like those from Deep Sky from the planning stage to a final investment decision (FID) and the start of construction. This will be the ultimate validation of the government’s strategy, proving it can not only attract project announcements but also facilitate the deployment of capital for physical infrastructure.

- If this happens: Deep Sky announces it has secured full project financing for its large-scale Manitoba facility and officially begins construction in 2026.

- Watch this: The Canada Growth Fund signing its first Carbon Credit Offtake agreement directly with a DAC project. Such a deal would provide the long-term revenue certainty that is essential for unlocking the large-scale, traditional debt financing required for these capital-intensive facilities.

- These could be happening: Additional U.S. or European DAC technology companies announce plans for Canadian pilot projects to leverage the 60% ITC. Watch for commitments from venture-backed developers who have not yet selected a location for their first commercial-scale system, as they may follow Carbon Capture Inc.’s lead.

Direct Air Capture Market Sees Explosive Growth

The section speculates on a company’s ‘Next Move’ beyond 2025. The chart forecasting explosive market growth provides the essential backdrop for this strategic discussion, illustrating the massive opportunity the company is planning for.

(Source: P&S Intelligence)

The questions your competitors are already asking

This report covers one angle of Canada’s emerging leadership in Direct Air Capture commercialization. The questions that matter most depend on your work.

- Which companies are gaining ground in the Canadian DAC market due to the new 60% ITC?

- What is the outlook for commercial DAC pilot deployment in Canada by 2026?

- Deep Sky investments and funding. Are the Manitoba and Alberta pilot projects on track for their 2026 targets?

- What are the opportunities for DAC technology developers in the Canadian market following the 2025 policy shift?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

DAC Purchase Volumes Fluctuate from 2022-2025

This section considers what competitors are thinking. The chart showing recent fluctuations in purchase volumes is exactly the kind of granular, tactical data that competitors would analyze to understand market volatility and predict future trends.

(Source: CDR.fyi)