DAC Market Creation, Denmark’s €3.8 B State Aid, 9.1 Mt CO₂ Removal Target, and 8 CCS Tender Bids (2025-2050)

Denmark’s 2025 DAC Market Acceleration

In 2025, Denmark transitioned from policy formation to active market creation for carbon dioxide removal, using legally binding net-negative emissions targets to generate structural demand for technologies like Direct Air Capture. This shift is defined by the execution of multi-billion-euro funding tenders and foundational infrastructure projects, moving beyond the theoretical climate goals of the 2021-2024 period toward building a functional, state-subsidized CDR industry.

- The Danish Climate Act mandates a 70% emissions reduction by 2030 and a 110% net-negative target by 2050, creating an unavoidable requirement for an estimated 9.1 million tonnes of annual technological carbon removal.

- Unlike the policy-setting phase of previous years, 2025 is marked by the Danish Energy Agency advancing a DKK 28.7 billion ($4.1 billion) funding tender for large-scale CO₂ capture and storage projects, with eight bidders submitting proposals.

- The focus has expanded from point-source capture to include all forms of negative emissions technologies, including Bioenergy with Carbon Capture and Storage (BECCS) and Direct Air Capture with Carbon Storage (DACCS), to meet long-term targets.

- This state-led approach directly confronts the prohibitive economics of nascent technologies by creating a subsidized market, a significant change from the prior period’s focus on research and road-mapping.

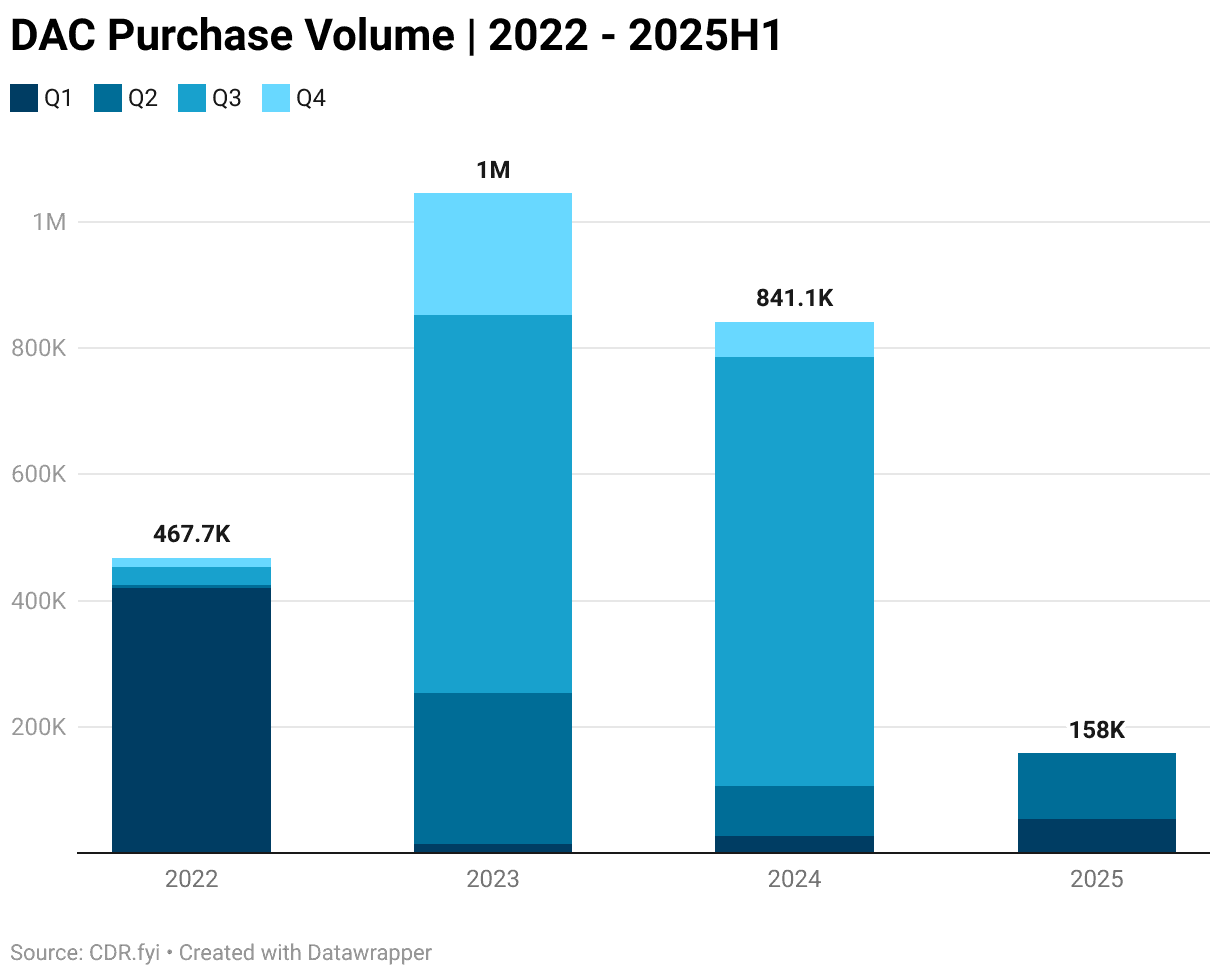

Global DAC Purchase Volume Peaks in 2023

This chart provides global context for Denmark’s market acceleration. By showing a recent peak in global purchase volume, it frames Denmark’s 2025 strategy as a timely response to growing international momentum in the DAC market.

(Source: CDR.fyi)

€3.8 Billion State Aid, Denmark’s De-risking of CDR Projects

Denmark is using substantial public funding to bridge the economic viability gap for high-cost carbon removal technologies, establishing a clear financial pathway for first-of-a-kind projects. The approval of a massive state aid scheme in late 2025 provides the revenue certainty needed to attract private investment and initiate the cost-reduction cycle through large-scale deployment.

- In December 2025, the European Commission approved a €3.8 billion Danish state aid program designed to subsidize carbon capture and storage projects through a competitive bidding process, offering a fixed payment per tonne of CO₂ stored.

- A separate DKK 2.5 billion ($360 million) funding pool was established specifically to procure 0.5 million tonnes of negative emissions annually starting in 2025, targeting both BECCS and DACCS.

- These direct subsidies are designed to make projects bankable despite current DAC costs, which range from $300 to over $1, 000 per tonne, far exceeding prevailing carbon market prices.

- This contrasts with the incentive structure in the United States, which relies on the 45 Q tax credit of $180 per tonne for DAC with storage, demonstrating Denmark’s more direct subsidy-based market intervention. The broader Carbon Capture DAC Market Report 2026: Key Growth Trends highlights different global policy approaches.

OECD Framework Outlines Blended Climate Finance Strategy

The section details Denmark’s use of state aid to de-risk projects. The OECD chart illustrates the strategic concept of blended finance, providing a theoretical framework that explains the mechanism Denmark is implementing to support its CDR projects.

(Source: OECD)

Table: Denmark’s Major Carbon Removal Funding Mechanisms (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| European Commission (Approver) | Dec 2025 | Approval of a €3.8 billion state aid scheme to subsidize CCS and CDR projects via competitive tenders. The goal is to provide a predictable revenue stream (fixed subsidy per tonne) for developers. | Carbon Capture Journal |

| Danish Energy Agency | Aug 2025 | Management of a DKK 28.7 billion (~$4.1 billion) tender for large-scale CO₂ capture projects. Eight bidders submitted preliminary proposals, signaling strong industry interest. | Nordea |

| Danish Government | From 2025 | Introduction of a DKK 2.5 billion ($360 million) funding pool to achieve 0.5 million tonnes of negative emissions per year from technologies including BECCS and DACCS. | Clean Air Task Force |

Normod Carbon Hub, Denmark’s $294 M Infrastructure Project

Partnerships in Denmark’s carbon removal sector in 2025 focused on building shared, enabling infrastructure rather than on deploying specific DAC plants. The development of CO₂ transport and processing hubs is a critical strategic decision to lower the capital barrier for individual capture projects and create an integrated value chain.

- In October 2025, Normod Carbon announced a $294 million investment to construct a CO₂ hub at the Port of Grenaa, designed to receive and process captured CO₂ for offshore storage.

- This project establishes a shared infrastructure model, allowing future DAC and other capture facilities to connect to a transport and storage network without needing to finance their own dedicated downstream solutions.

- The focus on midstream infrastructure in 2025 signals a pragmatic, phased approach: build the CO₂ highways first, then connect the capture facilities. This de-risks the entire value chain for future investors.

- This contrasts with projects in other regions, such as 1 Point Five‘s Stratos project in Texas, which is a vertically integrated capture and sequestration facility, highlighting different go-to-market strategies.

Table: Key Carbon Infrastructure Partnerships and Projects (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Normod Carbon Hub | Oct 2025 | A $294 million project to build a CO₂ reception and shipping hub at the Port of Grenaa, Denmark. It serves as essential midstream infrastructure for various carbon capture sources, including future DAC plants. | Carbon Credits.com |

| Carbonfuture / Danish Government | Nov 2025 | Carbonfuture opened a tender for government-backed BECCS projects with deliveries starting in 2026. While not DAC, this builds out the CO₂ supply chain and offtake agreements. | Carbon Herald |

| Deep Sky / Airbus | Nov 2025 | Launched a pilot DAC facility in Canada with a capacity of 250 tons per year. This serves as an international benchmark for the small-scale pilot phase preceding large-scale deployment. | Newswire |

Geography, Denmark Solidifies Role as EU’s CDR Market Incubator

In 2025, Denmark cemented its position as Europe’s primary geography for policy-driven carbon removal market development, moving far ahead of other EU nations in establishing operational deployment incentives. The country leverages its aggressive national climate laws and North Sea storage potential to attract capital and technology for both CDR and conventional CCUS projects.

- Denmark is the only EU member state with active, government-funded deployment incentives specifically for both Carbon Capture and Storage (CCS) and Carbon Dioxide Removal (CDR) as of 2025.

- The country’s strategy benefits from its proximity and access to significant geological CO₂ storage capacity in the North Sea, a key advantage over many land-locked European nations.

- The development of the Normod Carbon hub at the Port of Grenaa is designed to serve not just domestic emitters but also to position Denmark as a CO₂ storage service provider for industrial clusters across Northern Europe.

- While the 2021-2024 period saw multiple countries, including the UK, set targets, Denmark’s 2025 actions in executing large-scale funding tenders demonstrate a decisive move from ambition to implementation.

European DAC Market Forecasts Explosive Growth

This chart supports the section’s heading by quantifying the growth of the European market in which Denmark is positioning itself as an ‘incubator’. It provides the broader geographical context for Denmark’s role.

(Source: Market Data Forecast)

Technology Maturity, DAC’s High Cost Addressed with Subsidized Deployment

Direct Air Capture technology remains in a pre-commercial, high-cost phase globally in 2025, but Denmark’s strategy is to accelerate its maturity curve through subsidized deployment rather than waiting for independent cost reductions. The government’s financial interventions are explicitly designed to fund early, expensive projects to drive the learning-by-doing needed to make future facilities economically viable.

- Current levelized costs for DACCS in 2025 are estimated between $300 and $1, 000 per tonne, with some analyses showing costs up to $1, 900 for first-of-a-kind projects. This is significantly higher than the industry’s long-term target of $100 per tonne.

- Denmark’s policy acknowledges this gap by offering subsidies that cover the difference between project costs and market revenue, a departure from the 2021-2024 period which focused more on R&D funding.

- A key challenge remains the technology’s high energy intensity. A 0.5 Mt DAC plant requires approximately 1 TWh of energy annually, reinforcing the need for co-location with Denmark’s abundant offshore wind resources.

- The success of this strategy depends on whether deployment at scale can drive down capital and operational costs, a central question in the Carbon Capture & DAC Leaders: 2026 Market Analysis.

Government Regulations are a High-Impact Market Driver

The section discusses how subsidies address the high cost of DAC. This chart directly validates that premise by identifying government action (subsidies and regulations) as a key market driver, connecting the solution to the problem.

(Source: Coherent Market Insights)

SWOT Analysis of Denmark’s 2025 DAC Strategy

Denmark’s strategy leverages formidable policy and financial strengths to overcome the significant weakness of DAC’s current technological and economic immaturity. The primary opportunity is to establish global leadership in a future trillion-dollar market, while the threat lies in the risk that technology costs fail to decline as projected, straining public finances.

OECD Issues 2025 DAC Blended Finance Guidance

A SWOT analysis benefits from external benchmarks. The OECD guidance on blended finance represents an international standard and an ‘Opportunity’ or external factor that validates Denmark’s ‘Strength’ in this area, adding depth to the analysis.

(Source: OECD)

Table: SWOT Analysis for Denmark DAC Initiatives (2025)

| SWOT Category | 2021 – 2024 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Ambitious climate targets (70% by 2030) set in law. Strong political consensus on climate action. Access to North Sea storage. | Legally binding net-negative target (110% by 2050). Multi-billion-euro funding tenders (€3.8 B state aid) are operational. | Political ambition was converted into tangible, large-scale financial mechanisms, creating a bankable market signal for developers. |

| Weaknesses | Uncertainty on how to meet long-term negative emissions goals. High theoretical cost of DAC was a known barrier. | The high cost of DAC (up to $575/tonne) is confirmed as a primary obstacle. Nascent domestic supply chain for CDR projects. | The scale of the economic challenge became clear, and the government’s strategy of direct subsidy was validated as the primary tool to overcome it. |

| Opportunities | Potential to become a first-mover and leader in the European CDR market. Attract technology developers and investment. | Development of shared infrastructure (Normod Carbon Hub) to create a CO₂ service economy. Solidify status as EU’s premier CDR hub. | The strategy shifted from attracting individual projects to building an entire supporting ecosystem, creating a more durable competitive advantage. |

| Threats | Risk of policy reversal. Competition from other regions (e.g., US with 45 Q). Technology failing to mature. | Dependence on subsidies makes the market vulnerable to political shifts. Risk that tenders are won only by lower-cost BECCS/CCS, delaying DAC. | The primary risk was validated: the market is currently artificial and state-dependent. Its long-term survival depends on DAC costs falling dramatically. |

Scenario Modelling for Denmark’s DAC Tenders

The outcomes of the ongoing multi-billion-dollar carbon capture tenders are the single most critical variable for Denmark’s DAC ambitions in the year ahead. If a DAC project secures a contract, it will validate the policy-driven market creation model; if not, it will signal that DAC remains too expensive to compete even with substantial subsidies, delaying its deployment timeline.

- If a DAC project wins a tender: This will be a major validation point, proving that subsidies can make DAC bankable. Watch for an influx of new DAC developers and technology providers targeting Denmark for their European headquarters and pilot projects.

- If only BECCS/CCS projects win: This indicates that the cost gap for DAC remains too large. Expect Denmark’s near-term CDR efforts to be dominated by biomass and industrial sources, pushing DAC deployment out to the late 2020 s or early 2030 s.

- If infrastructure projects receive follow-on funding: Continued investment in transport and storage hubs like Normod Carbon, even without a major DAC plant, signals a long-term commitment to building the foundational “picks and shovels” for the eventual market.

The questions your competitors are already asking

This report covers one angle of Denmark’s state-led creation of a commercial carbon removal market. The questions that matter most depend on your work.

- What is actually happening with Denmark’s DKK 28.7 billion CCS tender now that eight bids have been submitted?

- What is the outlook for large-scale DACCS and BECCS deployment in Denmark to meet its 9.1 Mt annual removal target?

- What are the opportunities for technology suppliers and project developers in Denmark’s emerging state-subsidized market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Global DAC Market to Reach $17.5B by 2035

This section focuses on the competitive landscape. The global market forecast chart effectively illustrates the size of the prize, showing why competitors would be interested and what is at stake in the long term.

(Source: Research Nester)