Top 10 DAC Offtakes: Amazon’s 250, 000-ton deal and 9 other agreements scaling carbon removal (2024-2026)

The Direct Air Capture (DAC) market is rapidly transitioning from speculative pilots to bankable, large-volume offtake agreements, primarily driven by corporate net-zero commitments. This shift is solidified by major deals, including Amazon‘s purchase of 250, 000 metric tons and JPMorgan Chase‘s 50, 000-ton agreement with 1 Point Five, which highlight a significant trend. These multi-year commitments provide the revenue certainty required to finance and develop capital-intensive, megaton-scale facilities. The dominant theme for 2025-2026 is the maturation of the demand side, with technology and financial sector giants acting as anchor buyers. This de-risks the supply side and is a critical enabler for the next wave of DAC project development.

1. Amazon and 1 Point Five

Buyer: Amazon

Volume: 250, 000 metric tons

Application: Carbon removal credits over 10 years from the STRATOS DAC facility to help meet corporate climate goals.

Source: Status Report: American Competitiveness in Direct Air Capture

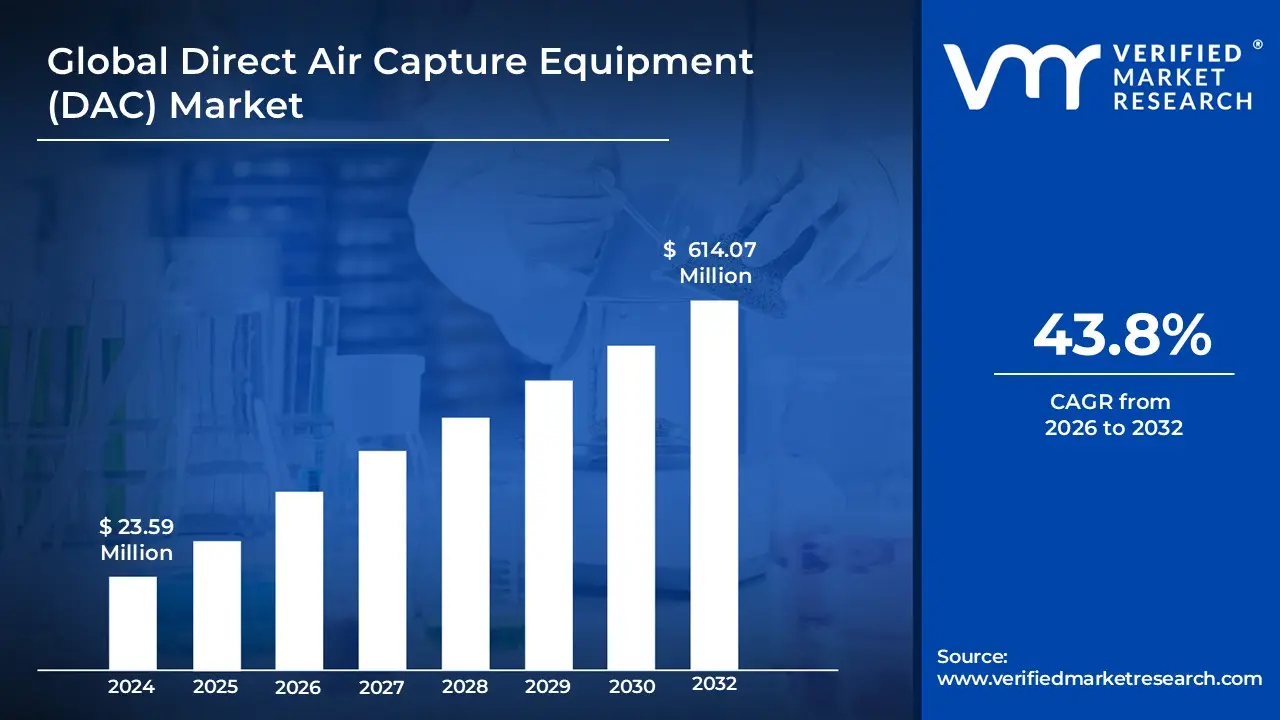

Direct Air Capture Market Poised for Major Growth

This chart provides the broad market context for the first major deal listed, involving Amazon. It illustrates the growing momentum that is attracting large corporations to make significant DAC offtake agreements.

(Source: Verified Market Research)

2. JPMorgan Chase and 1 Point Five

Buyer: JPMorgan Chase

Volume: 50, 000 metric tons

Application: DAC-enabled carbon removal credits purchased over a 10-year period to support durable carbon removal.

Source: 1 Point Five Announces 50000 Metric Ton Carbon Removal…

Chart Shows a Company’s Path to Net-Zero

This chart illustrates the strategic ‘why’ behind a company’s investment in DAC. It is a perfect fit for the JPMorgan Chase section, explaining how carbon removal purchases fit into a larger corporate net-zero strategy.

(Source: Senken)

3. TD Bank Group and Deep Sky

Buyer: TD Bank Group

Volume: Over 18, 000 metric tons

Application: 10-year purchase of CDR credits from future Canadian DAC facilities to meet net-zero targets.

Source: TD Signs 10-Year Carbon Removal Deal with Deep Sky – ESG Today

4. ENGIE and Deep Sky

Buyer: ENGIE

Volume: Up to 15, 000 metric tons

Application: Strategic partnership including an offtake agreement for carbon removal credits from Deep Sky‘s DAC projects.

Source: Deep Sky Announces Partnership to Advance Direct Air Capture …

European DAC Market to Exceed $4B by 2034

The section details a deal involving ENGIE, a major French multinational corporation. This provides a strong link to the European market, making the chart’s projection for European growth highly relevant.

(Source: Market Data Forecast)

5. Microsoft and Unnamed DAC Supplier

Buyer: Microsoft

Volume: 10, 000 metric tons

Application: Purchase of DAC credits as part of a broader carbon removal portfolio to stimulate the durable CDR market.

Source: Microsoft signs 4.9 million-tonne carbon removal deal with Vaulted …

6. Microsoft and Atmos Clear

Buyer: Microsoft

Volume: Undisclosed

Application: A 15-year offtake agreement for CO₂ removal credits, with permanent storage managed by Exxon Mobil.

Source: Growing Low Carbon Solutions | Exxon Mobil Sustainability

7. Frontier and Carbon Capture Inc.

Buyer: Frontier

Volume: Undisclosed

Application: Pre-purchase agreement facilitated by the advance market commitment to help scale emerging DAC technology.

Source: Writing – Frontier Climate

Carbon Removal Purchases Grow, BioCCS Dominates

This chart contextualizes Frontier’s investment by showing that while carbon removal is growing, DAC is not yet the dominant method. It highlights the importance of Frontier’s mission to scale newer technologies like DAC.

(Source: Carbon Removal Updates – Substack)

8. Frontier and 280 Earth

Buyer: Frontier

Volume: Undisclosed

Application: Offtake agreement to support a novel DAC technology, diversifying the portfolio backed by the buyers’ coalition.

Source: Writing – Frontier Climate

DAC Sorbent Market Poised for Major Growth

Investment in DAC technology developers like 280 Earth directly stimulates the underlying supply chain. This chart shows the projected growth of a critical component, sorbents, which is a direct consequence of scaling the core technology.

(Source: Fact.MR)

9. Bain & Company and 1 Point Five

Buyer: Bain & Company

Volume: Undisclosed

Application: First DAC carbon removal deal for the consulting firm, securing high-durability credits for its climate commitments.

Source: Bain signs first direct air capture carbon removal deal with 1 Point Five

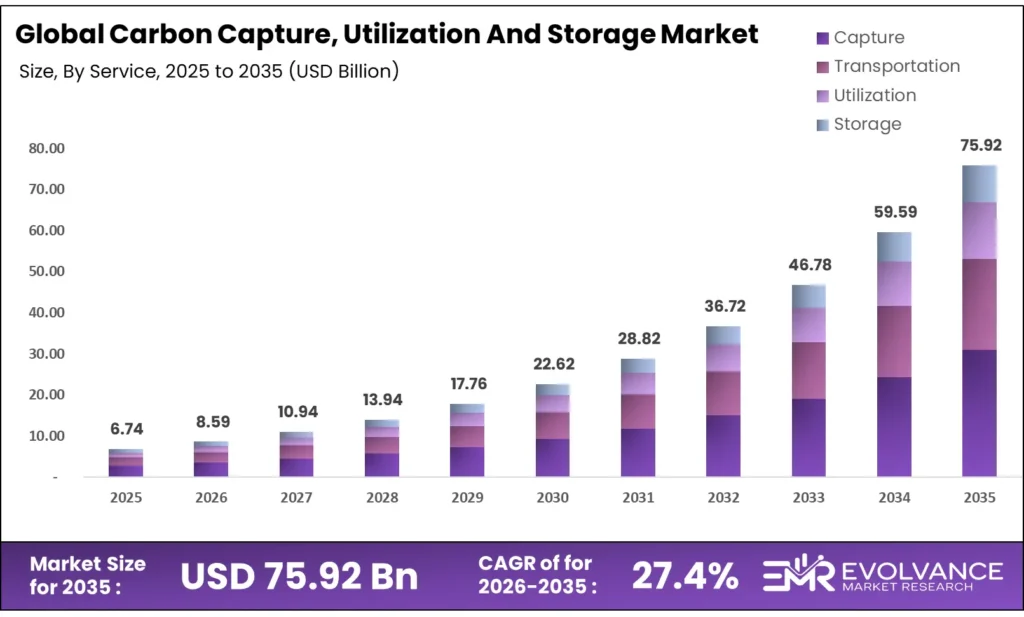

Carbon Capture Market to Reach $75.9B by 2035

The chart’s projection of massive growth for the broader carbon capture market provides the strategic context for why a management consulting firm like Bain & Company would invest in the sector.

(Source: Evolvance Market Research)

10. Unnamed Buyer and Octavia Carbon

Buyer: Unnamed (via Carbon Direct)

Volume: Undisclosed

Application: Offtake agreement secured to support the development of DAC projects in Kenya and the Global South.

Source: Octavia Carbon Secures An Offtake Agreement Via Carbon Direct

Table: Top 10 Direct Air Capture (DAC) Offtake Agreements (2024-2026)

| Date | Buyer | Supplier | Volume (metric tons CO₂) | Agreement Duration (Years) |

|---|---|---|---|---|

| Jun 8, 2026 | TD Bank Group | Deep Sky | >18, 000 | 10 |

| May 5, 2026 | Microsoft | Atmos Clear | Undisclosed | 15 |

| Apr 30, 2026 | ENGIE | Deep Sky | Up to 15, 000 | Not specified |

| Mar 4, 2026 | Unnamed (via Carbon Direct) | Octavia Carbon | Undisclosed | Not specified |

| Jan 27, 2026 | Frontier | Carbon Capture Inc. | Undisclosed | Not specified |

| Jan 27, 2026 | Frontier | 280 Earth | Undisclosed | Not specified |

| Jan 13, 2026 | Bain & Company | 1 Point Five | Undisclosed | Not specified |

| Jul 21, 2025 | Microsoft | Unnamed DAC Supplier | 10, 000 | Not specified |

| Jun 24, 2025 | JPMorgan Chase | 1 Point Five | 50, 000 | >10 |

| Jul 23, 2024 | Amazon | 1 Point Five | 250, 000 | 10 |

Global CCUS Market to Grow Significantly by 2029

The deal in this section involves Octavia Carbon, a Kenyan company, highlighting the geographic diversification of DAC. A chart projecting ‘Global’ CCUS market growth aligns perfectly with this theme of new international hubs emerging.

(Source: CarbonCredits.com)

DAC Offtake Agreements, Corporate Buyers Expand Beyond Tech to Finance

The profile of the typical DAC credit buyer is expanding significantly. While technology giants like Microsoft and Amazon remain foundational pillars of demand, the period between 2024 and 2026 has been marked by the entry of major players from other sectors. The 50, 000-ton agreement between JPMorgan Chase and 1 Point Five and the 18, 000-ton deal between TD Bank Group and Deep Sky signal a crucial trend: the financial services industry is now actively purchasing high-durability carbon removals at scale. This diversification is further evidenced by participation from the energy sector (ENGIE) and professional services (Bain & Company). This broadening buyer base demonstrates growing cross-industry confidence in DAC as a credible tool for meeting net-zero targets and reduces the market’s reliance on a handful of tech companies.

CO2 Credit Sales More Than Double in 2024

This chart provides direct quantitative evidence for the trend described in the section, as the expansion of corporate offtake agreements is what drives the doubling of CO2 credit sales.

(Source: Carbon Removal Updates – Substack)

USA Leads DAC Development, Canada and Kenya Emerge as New Hubs

The geographic landscape of DAC development is dominated by the United States, largely due to robust policy incentives. The Inflation Reduction Act’s enhanced 45 Q tax credit, offering $180 per ton for stored CO₂, has made large-scale projects like 1 Point Five‘s STRATOS facility in Texas economically viable, attracting major buyers like Amazon. However, other regions are emerging as important hubs. Canada is fostering a unique project development model through Deep Sky, which is building facilities to host multiple DAC technologies and has successfully secured offtakes from TD Bank Group and ENGIE. Furthermore, the offtake agreement secured by Kenya-based Octavia Carbon marks an important step in building a DAC industry in the Global South, highlighting the potential for geographic diversification in the supply of carbon removal credits.

Map Shows US Carbon Capture Project Locations

The chart is a map showing US project locations, which directly visualizes the central claim of the section heading: that the USA leads DAC development.

(Source: ClearPath)

1 Point Five’s STRATOS Project Signals DAC Commercial Scale (2024-2026)

These large-scale offtake agreements are a direct reflection of DAC technology’s progression toward commercial maturity. The deals signed by 1 Point Five for its STRATOS project, totaling over 300, 000 tons from buyers like Amazon and JPMorgan Chase, are predicated on the facility’s ability to deliver carbon removal at scale. This represents a significant step up from the smaller, pilot-scale purchases that characterized the market in earlier years. At the same time, the market is supporting technological diversity. The advance market commitment from Frontier, which backed both Carbon Capture Inc. and 280 Earth, is designed to help promising but less mature technologies bridge the commercial valley of death. This dual approach of backing large-scale deployment while nurturing innovation is critical for achieving long-term cost reductions and market growth.

Direct Air Capture Market Projected to Surge

The section discusses the STRATOS project signaling commercial scale for DAC, which is a primary driver for the overall market surge projected in this chart.

(Source: Market Research Future)

$180 per Ton Tax Credit, US Policy Spurs DAC Project Investment

The critical factor for the DAC market in the next 18 months is whether developers can leverage policy support and initial anchor agreements to secure full project financing and begin lowering the cost curve. While large corporate offtakes de-risk projects, the divergence between strong policy incentives and recent dips in early-stage venture capital suggests the market is entering a new phase of scrutiny. Watch for signs that project developers can attract traditional infrastructure capital beyond their initial, high-profile buyers.

- A key positive signal is the emergence of integrated value chains, such as the partnership between Atmos Clear and Exxon Mobil for CO₂ transport and geologic storage. This indicates that the necessary midstream infrastructure is developing in parallel with capture facilities, a crucial step for market scaling.

- The continued expansion of the buyer pool to include sectors like finance and professional services, demonstrated by deals with TD Bank Group and Bain & Company, provides a growing demand base that is essential for absorbing future supply.

- A potential headwind to monitor is investor sentiment. The 60% drop in DAC venture funding in Q 1 2025, even as broader climate tech investment recovered, suggests a flight to quality. This places greater pressure on DAC companies to prove their economic models are viable with existing policy support and offtake prices.

Direct Air Capture Costs Could Fall Over 90%

The section describes how US policy and tax credits spur investment in DAC. This chart illustrates the primary long-term goal and expected result of that investment: a dramatic reduction in technology costs.

(Source: Senken)

The questions your competitors are already asking

This report covers one angle of Direct Air Capture’s commercial trajectory, driven by corporate offtake agreements. The questions that matter most depend on your work.

- Which DAC companies are gaining ground in the corporate offtake market?

- What is the development status of 1 Point Five’s STRATOS facility following the Amazon and JPMorgan Chase offtake deals?

- What is the outlook for megaton-scale DAC deployment by 2030, based on the current offtake pipeline?

- Which corporate sectors, beyond tech and finance, are emerging as major buyers of DAC credits?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.