DAC Infrastructure Financing, Black Rock $550 M Occidental JV, $670 M Eni Partnership, and 2 Major Projects (2023 to 2026)

DAC Project Scale, Black Rock Signals Shift from Venture to Infrastructure

The Direct Air Capture (DAC) market has fundamentally shifted from a technology subsidized by venture capital and corporate R&D to a bankable infrastructure asset class, a transition validated by Black Rock‘s large-scale project finance commitments. Prior to 2024, the sector was defined by early-stage technology pilots and advance market commitments from corporate buyers. The period from 2025 to today is defined by the entry of institutional capital into first-of-a-kind commercial plants, treating them as long-duration, revenue-generating assets similar to power plants or pipelines.

- Between 2021 and 2024, market activity was characterized by technology developers like Climeworks and Carbon Engineering securing funding and early offtake agreements. For example, the Frontier consortium launched a $1 billion advance market commitment in April 2022 to guarantee revenue for nascent projects, while corporate buyers like Microsoft and H&M Group signed multi-year credit purchase agreements.

- The turning point was Black Rock‘s $550 million investment in Occidental‘s STRATOS project in November 2023, which began to draw a clear line between technology risk and project execution risk. This deal structure, described as having “classic infra-like protections, ” signaled that the financial architecture for scaling DAC was maturing beyond venture equity.

- From 2025 onward, this trend accelerated with institutional investors directly financing project construction and development. Black Rock‘s involvement expanded through its Global Infrastructure Partners (GIP) arm, which secured a $670 million financing facility in May 2026 for Eni‘s carbon capture initiatives, demonstrating a repeatable model for deploying large-scale capital into the carbon management value chain.

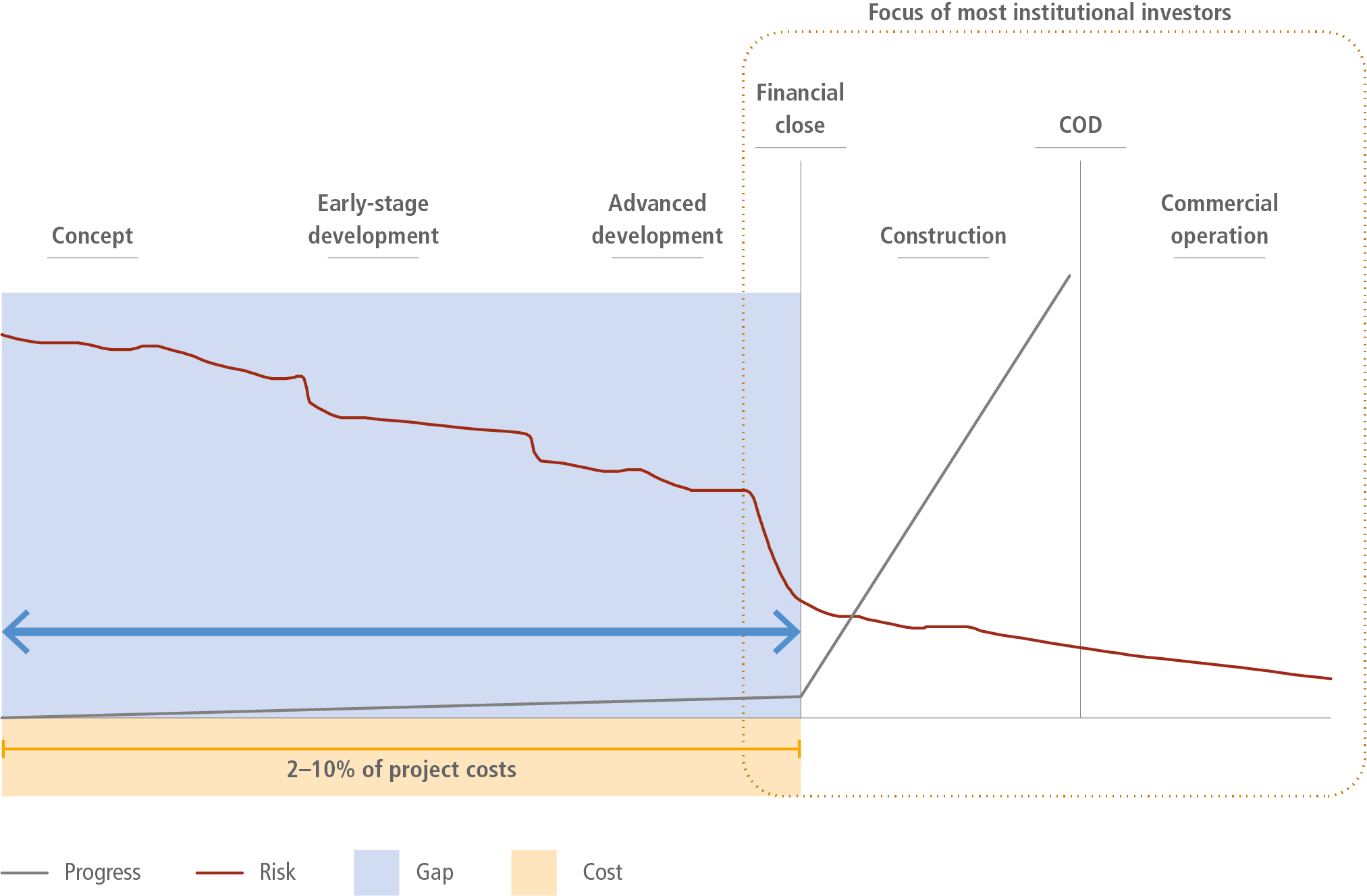

Chart Maps Project Risk to Investor Entry Point

The section discusses BlackRock’s shift from venture capital to infrastructure investment in DAC. This chart perfectly illustrates this concept by mapping how different investor types enter at various stages of a project’s lifecycle, corresponding to decreasing risk, with infrastructure funds entering at a later, de-risked phase.

$1.2 B in Commitments, Black Rock Financing De-Risks DAC Projects

Institutional financing, led by Black Rock, is now the primary enabler for scaling capital-intensive DAC projects, providing the multi-hundred-million-dollar commitments necessary to move from pilot to commercial operation. This capital inflow is directly tied to policy incentives like the U.S. 45 Q tax credit, which provides a predictable revenue floor that makes projects attractive to infrastructure investors seeking stable, long-term returns. The scale of these investments far surpasses the venture rounds that characterized the industry’s early years.

- The most significant financial signal was Black Rock‘s $550 million equity investment in 1 Point Five’s STRATOS project in May 2026. This commitment covered a substantial portion of the plant’s capital cost, enabling the construction of the world’s largest DAC facility and establishing a financial blueprint for future projects.

- Expanding its carbon management portfolio, Black Rock‘s infrastructure arm, GIP, was a key partner in securing a $670 million financing facility for Eni’s CCUS ventures in May 2026. This move shows a broader strategy to invest across the carbon capture value chain, from point-source to direct air capture.

- This institutional-led financing contrasts sharply with the earlier venture-led model. While crucial, earlier investments were smaller in scale, such as Grey Rock Investment Partners’ $150 million commitment to Vault Carbon in June 2022. The entry of players like Black Rock represents an order-of-magnitude increase in available capital.

Climate Finance Flows Total $1.27 Trillion Annually

This chart provides the macroeconomic context for the $1.2 billion commitment mentioned in the section. It places BlackRock’s significant investment within the vast landscape of annual climate finance, underscoring its scale and importance in catalyzing the DAC sector.

(Source: CTVC by Sightline Climate)

Table: Black Rock Carbon Management Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Eni CCUS Holding | May 2026 | Secured a $670 million (€625 million) financing facility through Global Infrastructure Partners (GIP) to develop carbon capture and storage projects. | Seeking Alpha |

| Occidental / 1 Point Five (STRATOS) | Nov 2023 / May 2026 | Committed $550 million in a joint venture to develop the STRATOS plant, the world’s largest DAC facility, designed to capture 250, 000-500, 000 tonnes of CO 2 per year. | ESG News |

| Alterra | Dec 2023 | Partnered with the UAE-based climate fund, which awarded Black Rock a mandate to invest $2 billion in climate transition infrastructure projects. | Alterra |

Black Rock Joint Ventures, Occidental and Eni Infrastructure Partnerships

Black Rock‘s strategy relies on forming joint ventures with established energy and industrial companies to execute complex, large-scale carbon capture projects. This partnership model leverages Black Rock‘s access to capital and infrastructure expertise with its partners’ project management experience and existing assets, effectively de-risking first-of-a-kind deployments. The collaborations with Occidental and Eni serve as templates for future institutional investment in the sector.

- The partnership with Occidental to build the STRATOS plant is the cornerstone of this strategy. It combines Black Rock‘s capital with Occidental‘s decades of experience in geological sequestration and large-scale project execution, a necessary combination to build a facility with a total cost of over $1.3 billion.

- The joint venture with Eni, through GIP, focuses on developing a portfolio of carbon capture and storage (CCUS) projects. This demonstrates a strategic intent to build and operate integrated carbon management hubs, moving beyond single-project investments to platform-level partnerships.

- These partnerships are distinct from earlier collaborations in the DAC space, which were often focused on technology licensing or credit sales. For instance, Carbon Engineering licensed its technology to Occidental, while Climeworks signed offtake agreements with corporate buyers. Black Rock‘s model involves direct equity ownership and co-development of the underlying infrastructure.

Energy Transition Investment Cycle Modeled

The section describes joint ventures for building infrastructure. This chart models the investment cycle for energy transition technologies, and the partnerships with Occidental and Eni represent the ‘Deployment’ and ‘Scale-Up’ phases, where mature technology is built out as critical infrastructure.

Table: Black Rock Strategic Carbon Management Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Eni | May 2026 | Formed a strategic partnership via Global Infrastructure Partners (GIP) to finance and develop CCUS projects, securing a $670 million financing facility. | Seeking Alpha |

| Occidental (1 Point Five) | Nov 2023 | Entered a joint venture with a $550 million investment to build and operate STRATOS, the world’s largest DAC plant in Texas. | Bloomberg |

| Temasek | June 2024 | Partnered with the Singaporean state investment firm to invest in Decarbonization Partners, a fund targeting climate solutions, including a strategy with Swiss provider Neustark. | Net Zero Investor |

US Policy Drives Deployment, Black Rock’s STRATOS Project in Texas

The United States, particularly Texas, has become the global epicenter for large-scale DAC deployment, a direct result of strong federal policy support that has created a bankable revenue stream for carbon removal. Black Rock‘s decision to invest heavily in the STRATOS project in Texas underscores the critical role of policy certainty in attracting institutional capital to climate infrastructure. Without these incentives, the economic case for multi-billion-dollar DAC projects would remain untenable.

- The primary driver is the U.S. Inflation Reduction Act of 2022, which enhanced the Section 45 Q tax credit to provide $180 per tonne for CO 2 captured via DAC and permanently stored. This government-backed revenue stream is the financial bedrock that makes projects like STRATOS viable for infrastructure investors like Black Rock.

- Texas offers a unique combination of favorable policy, geological suitability for CO 2 storage, a skilled energy workforce, and existing pipeline infrastructure. This makes it the logical location for first-of-a-kind, capital-intensive projects.

- In April 2026, the U.S. Department of Energy (DOE) restored federal funding for key carbon removal projects, including STRATOS, after a potential cut was considered. This action further solidified the project’s financial footing and reinforced the government’s commitment to building a domestic DAC industry.

Vast Investment Gap Exists for Climate Mitigation

The section highlights how US policy drives project deployment. This chart quantifies the investment gap that supportive policies, like the 45Q tax credit, are designed to close. These policies make projects like STRATOS economically viable, attracting private capital to help fill this funding void.

Commercial Viability, Black Rock’s Investment Validates DAC at Scale

Black Rock‘s project-finance approach to Direct Air Capture validates the technology’s transition from a high-cost, experimental concept to a commercially deployable infrastructure solution. While the cost of DAC remains high, the combination of policy support and long-term offtake agreements is creating a clear pathway to economic viability. The firm’s involvement signals that at least for large, integrated projects, the technology risk is now considered manageable enough for institutional investment.

- In the 2021-2024 period, DAC costs were estimated at $250 to $600 per ton, limiting deployment to small-scale pilots funded by venture capital and corporate climate commitments. The industry’s primary focus was on technology demonstration and securing early adopters.

- Starting in 2025, the conversation shifted from pure cost per ton to the bankability of projects. With the 45 Q credit providing a $180/tonne floor, the focus is now on securing long-term carbon removal purchase agreements to cover the remaining cost and guarantee revenue for financiers.

- Current operational plants still capture CO 2 at costs ranging from $400 to $1, 000 per tonne. However, the industry-wide target remains to bring costs below $100 per tonne through scale, learning-by-doing, and technological improvements, which is the long-term objective for facilities like STRATOS.

Growth Projected for Tech-Based Carbon Removal Credits

The section argues that BlackRock’s investment validates DAC’s commercial viability. This chart substantiates that claim by projecting massive growth in the market for carbon removal credits, which is the key revenue stream that underpins the commercial viability and bankability of large-scale DAC projects.

(Source: CTVC by Sightline Climate)

Black Rock SWOT Analysis, DAC Strengths and Market Risks (2021-2026)

Black Rock‘s entry has capitalized on the growing strength of policy support for DAC while exposing the sector’s continued reliance on those same subsidies for commercial viability. The firm’s strategy effectively leverages the transition from venture-backed technology development to government-supported infrastructure deployment. This shift is highlighted by comparing the market dynamics before and after the full implementation of the Inflation Reduction Act’s enhanced 45 Q tax credits.

- Strengths: The primary strength has shifted from novel technology in 2021-2023 to bankable revenue streams in 2024-2025, underpinned by the $180/tonne 45 Q tax credit.

- Weaknesses: High capital and operational costs remain a persistent weakness, though the risk is now being managed through infrastructure-style financing rather than VC funding.

- Opportunities: The key opportunity has evolved from securing corporate offtake deals to developing integrated carbon management hubs, as seen with Black Rock‘s acquisition of GIP.

- Threats: The main threat has transitioned from technological scaling risk to policy and political risk, including potential changes to crucial subsidies like 45 Q.

MSCI Climate Segment Revenue Soars

This chart directly supports the ‘Opportunities’ aspect of the SWOT analysis mentioned in the section title. The soaring revenue in a major climate-focused market segment demonstrates strong market demand and investor interest, representing a key opportunity for DAC financing.

(Source: Quartr)

Table: SWOT Analysis for DAC Infrastructure Financing

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Technology innovation from pioneers like Climeworks and Carbon Engineering. Strong corporate interest (e.g., Frontier’s $1 B fund). | Bankable revenue from enhanced 45 Q tax credit ($180/tonne). Access to institutional project finance from players like Black Rock. | The business model was validated as an infrastructure asset class, moving beyond just a technology play. |

| Weaknesses | Extremely high cost ($250-$600+/tonne). Dependence on venture capital and small-scale financing. | Continued high capital cost for FOAK projects (e.g., STRATOS at $1.3 B). Long-term revenue models are still maturing. | The financing gap is being addressed by institutional investors, but the underlying cost challenge remains the primary focus for technology developers. |

| Opportunities | Growing demand for high-quality carbon removal credits from corporations like Microsoft and Shopify. | Development of large-scale carbon management hubs. Access to trillions in infrastructure capital. Global expansion of policy support. | The opportunity expanded from selling credits to building and operating integrated infrastructure, attracting firms like Black Rock‘s GIP. |

| Threats | Technological failure at scale. Inability to secure long-term offtake agreements. Competition from cheaper abatement solutions. | Policy risk and political uncertainty surrounding climate subsidies like 45 Q. Public and investor backlash against fossil-fuel-led CCUS projects. | The primary risk shifted from whether the technology works to whether the policies that support it will last. |

Future Financing Models, Black Rock and the Need for Bankable Offtakes

The next phase of DAC financing will center on creating a robust market for long-term, bankable offtake agreements, mirroring the role that Power Purchase Agreements (PPAs) played in scaling renewable energy. For institutional investors like Black Rock to deploy capital more broadly, project developers must secure multi-decade contracts for carbon removal credits, which serve as the primary source of guaranteed revenue beyond government subsidies. This is the critical step to move from one-off, landmark deals to a repeatable, project-finance-driven market.

- If developers can secure 10 to 15-year offtake agreements from investment-grade corporations, then institutional investors can use these contracts to underwrite debt and equity financing with much lower risk. This is the model that unlocked the solar and wind industries.

- Watch for the evolution of buyer coalitions like Frontier and corporate leaders like Microsoft. Their willingness to sign larger, longer-term contracts at commercially viable prices will be the most critical signal for the next wave of project financing.

- This could be happening as a more liquid and transparent market for high-durability carbon credits emerges. The development of standardized contracts, independent verification, and liquid trading venues will be essential for attracting a wider pool of capital beyond specialized infrastructure funds.

Framework for Shifting Climate Finance Flows

The section discusses the need for ‘future financing models’ and ‘bankable offtakes’. This chart provides a conceptual model for exactly that—a framework outlining how to redirect and mobilize large-scale capital, which is essential for creating the novel financial structures DAC requires.

The questions your competitors are already asking

This report covers one angle of the transition to large-scale DAC infrastructure financing. The questions that matter most depend on your work.

- What is actually happening with BlackRock’s $550M investment in Occidental’s STRATOS project since the announcement?

- Which institutional investors are gaining ground in the carbon removal market, and which project developers are best positioned to attract them?

- Which oil & gas operators, beyond Occidental and Eni, are adopting the infrastructure JV model for DAC deployment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.