Top 10 Renewable M&A Deals, Alphabet’s $4.75 B Buy, Pattern Energy’s 16 GW Pipeline (2024-2026)

The renewable energy M&A landscape is undergoing a fundamental shift, defined by the strategic acquisition of large-scale development platforms and the vertical integration by non-traditional buyers. This trend is driven by a race to secure gigawatt-scale clean energy to meet future demand, particularly from the AI and data center industries. Landmark transactions, such as Alphabet’s $4.75 billion acquisition of Intersect Power and Pattern Energy’s move to absorb Cordelio Power’s massive 16 GW development pipeline, underscore this new reality. The dominant theme for 2025 and beyond is the “platform play, ” where acquirers are buying not just assets, but entire development companies to secure growth, market access, and technical expertise for years to come.

1. Pattern Energy Acquires Cordelio Power

Acquirer: Pattern Energy Group

Capacity: The deal includes 1, 200 MW of operational assets and a significant 16 GW development pipeline.

Application: Platform acquisition to create one of North America’s largest independent clean energy companies.

Source: Pattern Energy Announces Completion of Acquisition of Cordelio …

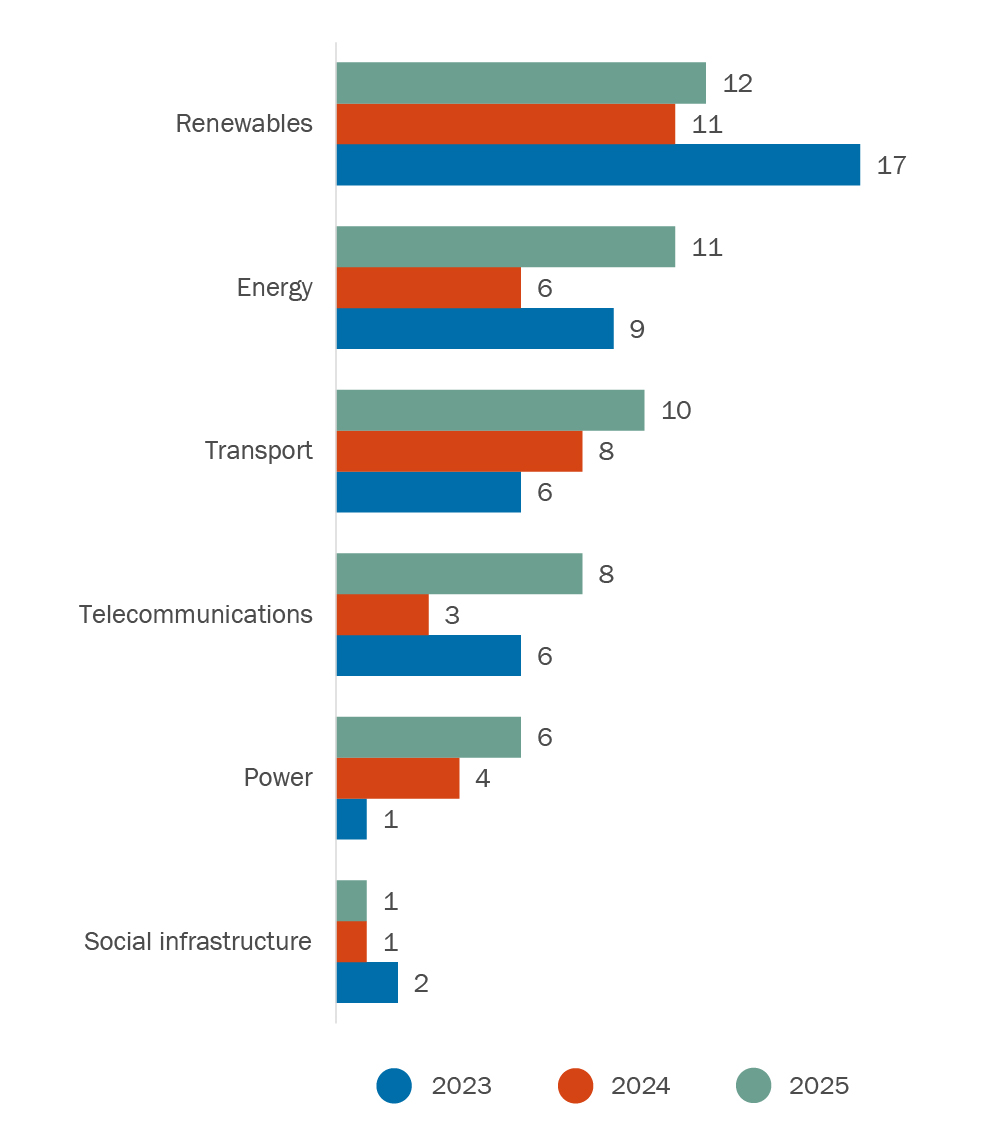

Renewables Lead Infrastructure M&A Activity

The acquisition of a renewable power company by an infrastructure investor like Pattern Energy is a prime example of the trend where renewables are the most active M&A area within the broader infrastructure sector.

(Source: Torys LLP)

2. Lydian Energy Acquires Atlas North Portfolio

Acquirer: Lydian Energy

Capacity: 1.5 GW

Application: Strategic portfolio acquisition of solar and battery energy storage systems (BESS).

Source: Lydian Energy Acquires 1.5 GW Solar and Storage Portfolio

3. Alphabet (Google) Acquires Intersect Power

Acquirer: Alphabet Inc.

Capacity: 2.2 GW of solar generation and 1.4 GWh of battery storage.

Application: Vertical integration to secure clean energy supply for AI and data center operations.

Source: Analysis: Why Google Bought Intersect for AI Energy Supply

Top Solar M&A Deals of 2025 Revealed

The multi-billion dollar acquisition of Intersect Power, a major U.S. solar and storage developer, would be featured prominently in any ranking of top solar M&A deals for the year.

(Source: Mercom Capital Group)

4. Enel Acquires U.S. Wind and Solar Portfolio

Acquirer: Enel

Capacity: 830 MW

Application: Expansion of operational renewable asset base in the United States.

Source: Enel signed agreements for the acquisition of an 830 MW portfolio of …

5. ONGC-NTPC Acquires Ayana Renewable Power

Acquirer: A consortium of Oil and Natural Gas Corporation (ONGC) and NTPC Limited

Capacity: 4.1 GW portfolio

Application: A major platform play to dominate India’s rapidly growing renewable energy market.

Source: Why Platform Plays Are Dominating India’s Renewable M&A Market

Renewables to Dominate Future Energy Investment

The acquisition of a renewable platform by two of India’s largest state-owned fossil fuel companies illustrates the strategic pivot towards renewables, which are projected to dominate future energy investment.

(Source: Wood Mackenzie)

6. Cox Acquires Iberdrola Mexico’s Renewable Assets

Acquirer: Cox

Capacity: 1, 232 MW of renewable assets within a larger mixed-generation portfolio.

Application: Acquisition of a mixed-asset portfolio including significant renewable generation capacity.

Source: Cox Acquires Iberdrola Mexico for $4.2 Billion

Global M&A Activity Hits Second-Highest Level

This large, complex, cross-border transaction involving major corporations from different sectors is emblematic of a near-record-breaking global M&A environment.

(Source: Morrison Foerster)

7. HELLENi Q Energy Acquires ABO Energy Hellas

Acquirer: HELLENi Q Energy

Capacity: 1.5 GW development pipeline

Application: Acquisition of a pure-play development pipeline to expand future renewable capacity in Greece.

Source: HELLENi Q Energy buys ABO Energy Hellas, adding 1.5 GW in …

Energy M&A Deal Value and Volume Declining

This targeted, regional acquisition in Greece can be presented as a counterpoint to a broader global trend of declining deal volume, highlighting that strategic consolidation continues in specific national markets.

(Source: PwC)

8. Potentia Energy Acquires Australian Renewable Portfolio

Acquirer: Potentia Energy (a joint venture including Enel Green Power)

Capacity: Over 1 GW

Application: Purchase of a high-quality portfolio of operational wind and solar assets in Australia.

Source: Potentia Energy Completes Acquisition of a 1 GW+ Portfolio of …

9. LS Power Acquires Algonquin Power’s Renewable Business

Acquirer: LS Power

Capacity: Approximately 2, 900 MW of operating wind, solar, and battery storage.

Application: Large-scale consolidation to expand its North American renewable energy platform.

Source: LS Power Completes Acquisition of Algonquin Power & Utilities …

Renewable Stocks Underperform, Fueling Take-Private Deals

The acquisition of a public company’s (Algonquin) renewable assets by a private entity (LS Power) perfectly exemplifies the trend of take-private style deals, often driven by the underperformance of public renewable stocks.

(Source: S&P Global)

10. Masdar Acquires Saeta from Brookfield

Acquirer: Masdar

Capacity: 745 MW of operating assets and a 1.6 GW development pipeline.

Application: Strategic acquisition to gain a foothold in the Iberian market with both operational assets and a growth pipeline.

Source: Masdar to Acquire Saeta from Brookfield for $1.4 Billion

Table: Top Renewable M&A Deals (2024-2026)

| Acquirer | Target/Asset | Key Capacity/Value | Region | Source |

|---|---|---|---|---|

| Pattern Energy | Cordelio Power | 1.2 GW Ops + 16 GW Pipeline | North America | Pattern Energy |

| Lydian Energy | Atlas North Portfolio | 1.5 GW | United States | Mercom Capital |

| Alphabet (Google) | Intersect Power | $4.75 Billion / 2.2 GW | United States | Intuition Labs.ai |

| Enel | U.S. Portfolio | 830 MW | United States | Enel |

| ONGC-NTPC | Ayana Renewable Power | $2.3 Billion / 4.1 GW | India | Lamberton Power |

| Cox | Iberdrola Mexico | $4.2 Billion / 1.2 GW Renewables | Mexico | Grupo Cox |

| HELLENi Q Energy | ABO Energy Hellas | 1.5 GW Pipeline | Greece | Balkan Green Energy |

| Potentia Energy | Australian Portfolio | 1 GW+ | Australia | Potentia Energy |

| LS Power | Algonquin Power Renewables | 2.9 GW | North America | LS Power |

| Masdar | Saeta Yield | $1.4 Billion / 2.3 GW Total | Iberian Peninsula | Brookfield |

Platform Plays, Pattern Energy’s 16 GW Pipeline Acquisition

The most significant pattern emerging from recent M&A activity is the prioritization of “platform plays” over single-asset acquisitions. Acquirers are targeting entire companies to secure not just operational assets but also development pipelines, market access, and specialized talent. Pattern Energy’s acquisition of Cordelio Power is the prime example, bringing in a staggering 16 GW development pipeline that instantly positions the company for long-term growth. Similarly, the $2.3 billion acquisition of Ayana Renewable Power by an ONGC-NTPC consortium in India and LS Power’s purchase of Algonquin’s 2.9 GW renewable business highlight a clear strategy: buy the entire development engine, not just the finished product. This approach allows consolidators to achieve scale rapidly and control a larger portion of the value chain from development to operation.

Investors Target Late-Stage Renewable Energy Projects

The section’s focus on ‘Platform Plays’ and acquiring a massive ’16 GW Pipeline’ directly aligns with the chart’s finding that investors are targeting late-stage development projects to secure future growth.

(Source: Deloitte)

North America Leads, LS Power’s 2.9 GW Portfolio Consolidation

Geographically, North America remains the epicenter of high-value renewable M&A, driven by a mature market, clear policy support, and soaring energy demand from data centers. A majority of the top deals, including those by Pattern Energy, Lydian Energy, Alphabet, Enel, and LS Power, were focused on assets in the United States. This reflects a deep, liquid market where large-scale portfolios can be transacted. However, significant strategic moves are occurring globally. The ONGC-NTPC deal for Ayana Power shows the immense scale of consolidation in India’s high-growth market. Elsewhere, targeted acquisitions like HELLENi Q Energy’s purchase of a 1.5 GW pipeline in Greece and Masdar’s entry into the Iberian Peninsula signal a strategic hunt for growth in key European sub-markets with strong renewable potential.

Alphabet’s $4.75 B Intersect Power Deal Signals New Buyer Class

The strategic drivers behind these acquisitions are becoming more diverse. The market is no longer dominated solely by traditional utilities and private equity. The entrance of big tech as a market-shaping acquirer is the most critical new development. Alphabet’s $4.75 billion purchase of Intersect Power is a landmark deal, representing a strategic pivot towards vertical integration to directly control the clean energy supply needed for its power-hungry AI operations. This move by a non-traditional energy player introduces a new level of competition and capital into the market. Concurrently, established energy players continue to pursue consolidation to enhance scale and competitiveness. Deals are bifurcated between acquiring operational portfolios for immediate cash flow, like Enel’s 830 MW US portfolio purchase, and acquiring development pipelines, like HELLENi Q’s bet on ABO Energy Hellas, to secure future growth.

Global Energy M&A Value Surges in 2025

The entry of a ‘New Buyer Class’ like Big Tech, signalized by a landmark multi-billion dollar deal, is a primary driver for the surge in overall global energy M&A value.

(Source: S&P Global)

$4.75 B Deals, Big Tech’s Vertical Integration in Energy Markets

If big tech continues its direct acquisition of renewable platforms, expect a significant inflation in asset valuations and increased competition for traditional utilities. The market should anticipate a wave of M&A targeting developers with large, de-risked interconnection queues, as grid access becomes the new bottleneck and a primary source of value.

- The trend of vertical integration by non-energy players is gaining significant traction, directly evidenced by Alphabet’s acquisition of Intersect Power in March 2026 to secure its own power supply.

- The valuation of pre-construction assets is soaring. This is highlighted by Pattern Energy’s deal for Cordelio Power’s massive 16 GW development pipeline, indicating the market is placing a premium on future growth potential over existing operational assets.

- Consolidation among large, established energy players is accelerating. Moves like LS Power’s absorption of Algonquin’s renewable business in January 2025 show that scale is considered critical for competing in the North American market.

Global Power & Renewable M&A Activity Peaks

The discussion of massive, multi-billion dollar deals and strategic shifts like vertical integration are characteristic of a market reaching a peak in activity, as depicted by the chart.

(Source: S&P Global)

The questions your competitors are already asking

This report covers one angle of the strategic shifts in renewable energy M&A. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the race to acquire large-scale renewable development platforms in North America?

- What is the outlook for platform-level M&A to meet the clean energy demands of the AI and data center industry through 2030?

- Which non-traditional buyers, following Alphabet’s lead, are acquiring renewable energy platforms instead of signing traditional power purchase agreements (PPAs)?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.