CCUS in 2026: How Enhanced Gas Recovery is Forcing a Market Reckoning

CCUS Project Viability: Abatement vs. Enhanced Recovery

The Carbon Capture, Utilization, and Storage (CCUS) market is undergoing a strategic bifurcation, moving from a broad portfolio of decarbonization concepts to a narrow focus on projects with direct economic returns, primarily through Enhanced Gas Recovery (EGR). This shift forces a clear distinction between CCUS for industrial abatement, which remains dependent on subsidies and policy, and CCUS as a tool to maximize hydrocarbon asset value, which possesses a self-sustaining business case. The commercial filter is becoming increasingly stringent, prioritizing resource extraction over purely environmental applications.

- Between 2021 and 2024, the strategy appeared to be a wide-ranging exploration of CCUS applications, including partnerships for industrial clusters in China with Petro China, low-carbon hydrogen in the UK with BASF, and US Gulf Coast development with Linde. This period represented a broad, exploratory phase aimed at establishing a presence across multiple CCUS value chains.

- The period from January 2025 to today reveals a sharp strategic pivot. This is defined by the cancellation of commercially uncertain projects, such as the 1.2 GW H 2 Teesside blue hydrogen facility and the Indiana CCS project, which faced economic and public opposition. These pullbacks demonstrate that standalone CCUS for abatement or hydrogen production struggles to meet stricter investment hurdles.

- In contrast, the approval of capital-intensive projects is now explicitly linked to fossil fuel production. The Final Investment Decision (FID) for the $7 billion Tangguh UCC project in Indonesia in January 2026 is the primary example, as its core purpose is to unlock an additional 3 trillion cubic feet (TCF) of gas reserves through CO 2 injection, making the carbon capture component economically viable.

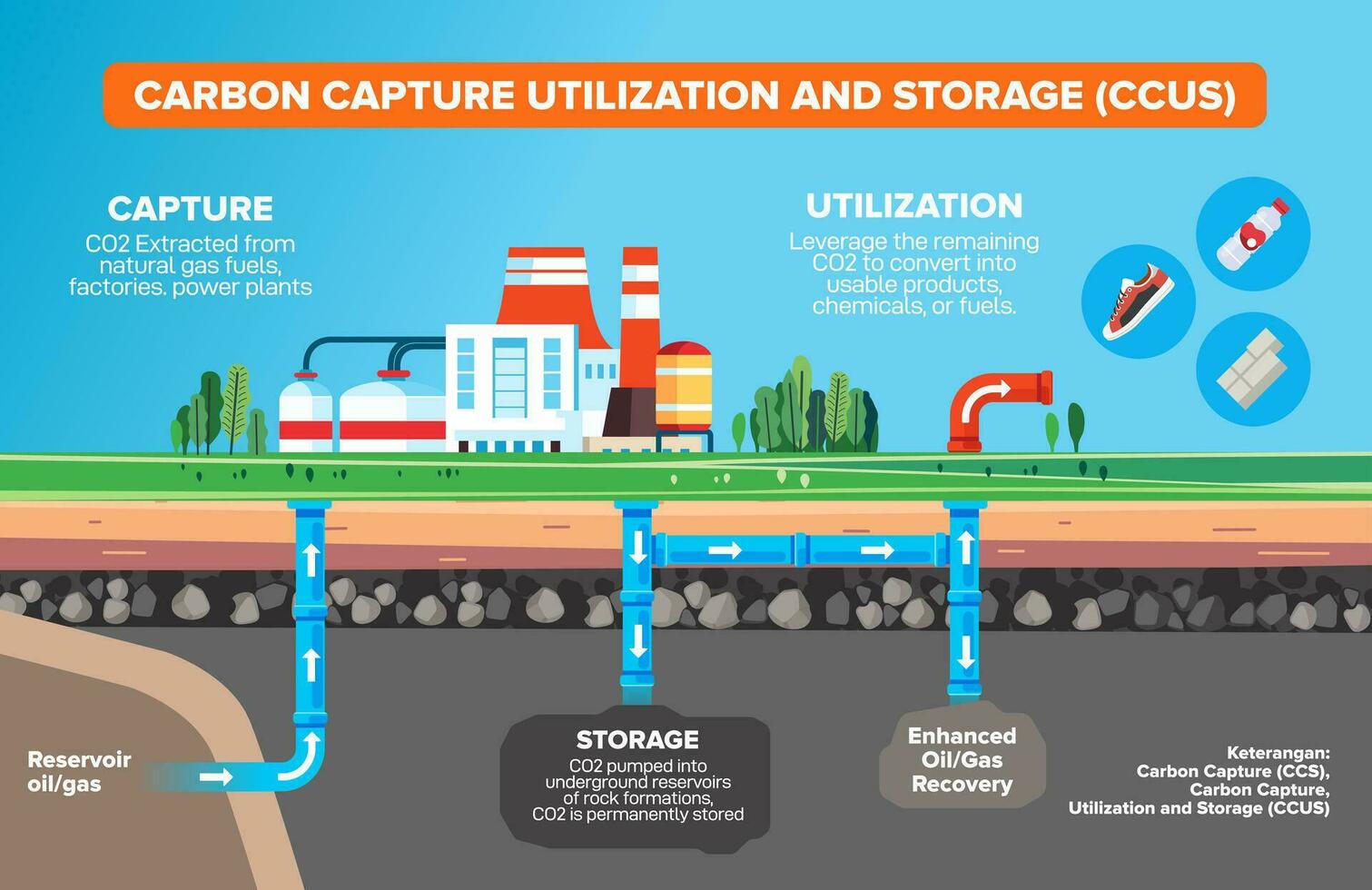

CCUS Pathways: Storage vs. Utilization

This diagram illustrates the strategic choice discussed in the section, showing how captured CO2 can be directed to either permanent storage (abatement) or used for enhanced recovery, which has a direct economic return.

(Source: Vecteezy)

Investment vs. Cancellation: The Economic Filter on CCUS Projects

Recent capital allocation decisions reveal a clear pattern: multi-billion-dollar investments are flowing into integrated CCUS projects that enhance fossil fuel recovery, while ventures reliant on speculative hydrogen or merchant storage models are being canceled or indefinitely halted. This trend is driven by a strategic realignment, where companies prioritize immediate returns from core hydrocarbon assets to fund a more selective and disciplined energy transition. The market is rewarding projects where CCUS serves as a direct enabler of profitable resource extraction.

- The most significant financial commitment is the $7 billion FID for the Tangguh UCC project in Indonesia. This investment is not primarily for decarbonization but to facilitate Enhanced Gas Recovery (EGR), directly linking CCUS to increased natural gas production and revenue.

- Conversely, BP scrapped its H 2 Teesside project in December 2025. This planned 1.2 GW blue hydrogen facility, which depended on CCUS, was abandoned due to land use conflicts and underlying economic uncertainties, highlighting the fragility of projects without an integrated economic driver like EGR.

- Similarly, the Indiana CCS project, designed to capture emissions from the Whiting Refinery for blue hydrogen production, was halted indefinitely in June 2025. This decision, driven by public opposition and economic concerns, underscores the dual challenge of securing social license and commercial viability for projects lacking a direct link to resource monetization.

Table: Key CCUS Project Fates (2025-2026)

| Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Tangguh UCC Project | 2026-01-22 (FID Approved) | $7 Billion investment to sequester ~15 M tonnes of CO 2 and unlock 3 TCF of gas via Enhanced Gas Recovery. Prioritizes asset value maximization. | Carbon Capture Magazine |

| H 2 Teesside | 2025-12-02 (Cancelled) | 1.2 GW blue hydrogen project cancelled. The project’s economics were not robust enough to overcome land use and commercial hurdles without a direct link to enhanced hydrocarbon recovery. | Institute of Materials, Minerals & Mining |

| Indiana CCS Project | 2025-06-18 (Halted Indefinitely) | Project to capture emissions from the Whiting Refinery was suspended due to public opposition and economic re-evaluation, showing the high barriers for standalone abatement projects. | Carbon Credits |

Partnerships in CCUS: De-Risking Hubs and Securing Offtake

The CCUS partnership model has evolved from broad, exploratory alliances to focused collaborations designed to execute large-scale infrastructure projects and secure offtake for captured CO 2. Post-2025 partnerships are increasingly transactional, aiming to connect CO 2 sources in one country with storage assets in another, reinforcing the development of specific, economically viable corridors rather than speculative, widespread networks.

- Between 2021 and 2024, partnerships were primarily focused on forming large-scale industrial decarbonization hubs. This included collaborations with Equinor and Total Energies for the Northern Endurance Partnership (NEP) in the UK and an agreement with Petro China to explore a CCUS cluster in southern China.

- From 2025 onward, the focus has shifted to operational execution and creating international value chains. The NEP partnership advanced by hiring Halliburton for monitoring services, signaling a move from planning to implementation.

- A key new development is the Mo U signed in September 2025 between BP and Japan’s Chubu Electric Power. This agreement explicitly aims to create a CO 2 transport and storage value chain between Japan and Indonesia, positioning the Tangguh UCC project as a commercial receptacle for Japanese industrial emissions and creating a potential carbon credit revenue stream.

Table: Evolution of Strategic CCUS Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Chubu Electric Power Co., Inc. | 2025-09-17 | Mo U to create a CCUS value chain between Japan (source) and Indonesia (storage at Tangguh). This establishes a commercial model for cross-border CO 2 management. | Norton Rose Fulbright |

| Halliburton (for NEP) | 2025-08-05 | Contracted by BP, Equinor, and Total Energies to provide monitoring for the UK’s first offshore CCS project. This marks a shift from planning to operational readiness for a major abatement hub. | Offshore Energy |

| Petro China | 2023-03-21 | Agreement to cooperate on a potential 2 million tons per year CCUS cluster in southern China, representing an earlier strategy of exploring large-scale industrial abatement hubs. | Carbon Herald |

| Linde | 2023-01-03 | Partnership to develop a major CCS project on the Texas Gulf Coast, capturing CO 2 from hydrogen production. This reflects the initial focus on enabling low-carbon hydrogen. | Akin Gump |

Geographic Focus: CCUS Activity Concentrates in the UK and Indonesia

CCUS development is not global but is concentrating in specific geographic pockets where geology, industrial density, and policy align to create a viable business case. The UK remains a key hub for large-scale industrial abatement projects supported by government policy, while Indonesia is emerging as a critical center for CCUS linked directly to enhancing natural gas production, representing two divergent models for regional growth.

- Between 2021-2024, BP‘s geographic strategy involved exploring opportunities in the UK (Northern Endurance Partnership, Viking CCS), the US (Texas with Linde), and Asia (China with Petro China), indicating a broader, more diversified approach.

- From 2025, this has narrowed significantly. The UK remains a priority with the Northern Endurance Partnership and Net Zero Teesside Power, driven by strong government support for industrial decarbonization clusters. The goal is to create CO 2 transport and storage infrastructure for third-party emitters.

- Indonesia has become the centerpiece of the CCUS-for-EGR strategy with the $7 billion Tangguh UCC project. This positions the country not just as a site for domestic emissions management but as a potential regional hub for storing CO 2 from other nations like Japan, creating a new geopolitical dynamic in carbon management.

- The US has seen a strategic retreat, evidenced by the indefinite halt of the Indiana CCS project. This suggests that despite favorable incentives like the Inflation Reduction Act, projects can stall due to local opposition and challenging economics if not perfectly aligned.

Technology Maturity: A Shift from R&D to Integrating Proven Solutions

The CCUS market is maturing from a phase of technology development and exploration to one focused on the commercial integration of proven, off-the-shelf solutions at a massive scale. Companies are no longer primarily investing in novel capture methods but are licensing established technologies and focusing their innovation on complex project integration, particularly combining CCUS with Enhanced Gas Recovery (EGR) to create a closed-loop economic model.

Mapping CCUS Technology Maturity

This chart visualizes the section’s theme by mapping CCUS technologies against readiness levels, highlighting the industry’s shift from R&D to deploying proven, commercial-scale solutions.

(Source: ScienceDirect.com)

- The 2021-2024 period involved partnerships to advance emerging technologies, such as the collaboration with Carbon Free on its Sky Cycle™ CCU technology. BP also licensed BASF‘s OASE® capture technology for its planned H 2 Teesside project, showing a reliance on specialized providers.

- The period since January 2025 demonstrates a clear focus on deployment over development. The core “technology” being advanced at the Tangguh UCC project is the large-scale integration of CCUS with EGR, a well-understood process, to unlock an additional 3 TCF of gas. This is a commercial and engineering innovation, not a chemical one.

- For abatement-focused projects like the Northern Endurance Partnership, the emphasis is on deploying advanced subsurface monitoring and well completion technologies from providers like Halliburton. This is about ensuring long-term storage integrity and de-risking the operational phase, rather than inventing new capture processes.

SWOT Analysis: BP’s Dual-Track CCUS Strategy in 2026

The strategic landscape for CCUS has shifted from broad ambition to pragmatic execution, creating new strengths in project delivery but exposing significant reputational threats. The abandonment of speculative projects has sharpened the company’s focus, but the heavy reliance on using CCUS to extend the life of fossil fuel assets creates a fundamental tension with its energy transition narrative.

Table: SWOT Analysis for BP and Carbon Capture, Utilization, and Storage

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Broad partnership network (Equinor, Linde, Petro China) and a diverse project pipeline (Viking CCS, H 2 Teesside). | Proven ability to reach FID on mega-projects ($7 B Tangguh UCC) and execute complex infrastructure builds (Northern Endurance Partnership). | The company validated its ability to move from planning to execution on capital-intensive projects. Focus shifted from portfolio breadth to depth in project delivery. |

| Weaknesses | High capital dependency on projects with uncertain commercial models (e.g., blue hydrogen). Abandoned oil production cut targets created strategic ambiguity. | Portfolio is now heavily skewed towards CCUS for Enhanced Gas Recovery, creating a dependency on hydrocarbon assets. Reduced low-carbon spending (to $1.5-2 B/year) limits portfolio diversification. | The weakness of uncertain returns was “resolved” by tying CCUS to EGR. However, this created a new weakness: over-exposure to fossil fuel-linked projects and a reduced capacity for purely “green” ventures. |

| Opportunities | Build new revenue streams from industrial decarbonization and low-carbon hydrogen production across multiple geographies (UK, US, China). | Monetize CO 2 storage as a service for other countries (e.g., Japan via Tangguh). Unlock vast gas reserves (3 TCF at Tangguh) that would otherwise be stranded. Generate carbon credits under frameworks like the JCM. | The opportunity shifted from speculative hydrogen markets to concrete, asset-backed revenue from EGR and international carbon storage services. This is a more tangible but less transition-oriented opportunity. |

| Threats | Policy uncertainty and reliance on government subsidies. Competition from rapidly falling costs of renewables. | Intensified public and investor scrutiny over “greenwashing” due to the explicit link between CCUS and increased fossil fuel production. Project cancellations (H 2 Teesside, Indiana) signal significant commercial and social license risks. | The threat of poor project economics was validated, leading to cancellations. This has been replaced by a growing reputational threat that CCUS is primarily a tool to prolong the fossil fuel era, which could impact future financing and regulation. |

Scenario Modeling: The Critical Path for CCUS in 2026 and Beyond

The central question for the CCUS market is whether it will primarily evolve as a climate mitigation tool for hard-to-abate industries or as an enabling technology for maximizing fossil fuel extraction. The trajectory will be determined by the relative success and replication of abatement-focused projects versus EGR-linked projects. The market is at a crossroads, and the next investment decisions will set the dominant path for the coming decade.

Forecasting CCUS Growth Under Different Scenarios

This forecast directly supports the section’s discussion on scenario modeling by projecting CCUS growth under different policy frameworks, visualizing the potential future paths for the market.

(Source: CarbonCredits.com)

- If FIDs for large-scale industrial abatement projects like Net Zero Teesside Power proceed without being tied to enhanced recovery, then watch for a wave of similar projects in other industrial clusters supported by strong policy frameworks. This could signal that the business case for pure decarbonization-as-a-service is strengthening.

- If, however, new major CCUS investments follow the Tangguh model and are predominantly linked to EGR or Enhanced Oil Recovery, then watch for increased investor and regulatory scrutiny on the “net-zero” claims of energy companies. This could signal that CCUS is becoming a niche, fossil-fuel-sustaining technology rather than a broad-based climate solution.

- The allocation of BP’s reduced low-carbon CAPEX ($1.5-$2 billion annually) is a critical signal. A significant portion directed toward the Northern Endurance Partnership and other abatement projects would confirm a continued commitment to the dual-track strategy. A diversion of that capital primarily to backfill EGR-related costs would confirm a strategic tilt towards hydrocarbons.

- The success of the Japan-Indonesia carbon credit framework for Tangguh is a key development to monitor. If it creates a profitable, replicable model for monetizing cross-border CO 2 storage, it could trigger a series of similar bilateral agreements across Asia, cementing the role of EGR-linked projects as regional carbon sinks.

Frequently Asked Questions

What is the main shift happening in the CCUS market in 2026?

The CCUS market is undergoing a major shift, moving away from a wide range of applications towards a narrow focus on projects with direct economic returns. Specifically, investments are prioritizing CCUS for Enhanced Gas Recovery (EGR), which uses CO2 to maximize hydrocarbon production, over projects aimed purely at industrial emissions abatement, which often struggle for commercial viability without subsidies.

Why are some major CCUS projects being cancelled while others are receiving billions in investment?

Projects are being cancelled if they lack a self-sustaining business case. For example, the H2 Teesside and Indiana CCS projects were halted due to economic uncertainties and public opposition. In contrast, projects like the $7 billion Tangguh UCC in Indonesia are being approved because the CCUS component is directly tied to a profitable outcome—unlocking an additional 3 trillion cubic feet of natural gas through EGR.

What is Enhanced Gas Recovery (EGR) and why is it so important for CCUS projects now?

Enhanced Gas Recovery (EGR) is the process of injecting CO2 into natural gas reservoirs to increase the pressure and extract more gas. It has become critically important because it provides a direct revenue stream that makes the high upfront cost of carbon capture economically viable. It transforms CCUS from a cost center for decarbonization into a profitable tool for maximizing the value of fossil fuel assets.

According to the article, what is the biggest risk or threat associated with this new focus on EGR?

The biggest threat is intensified public and investor scrutiny over “greenwashing.” By explicitly linking CCUS to increased fossil fuel production, companies risk their energy transition narrative being undermined. This could lead to reputational damage, making it harder to secure financing and favorable regulation in the future, as it appears the technology is being used to prolong the fossil fuel era rather than end it.

How are international partnerships for CCUS changing?

Partnerships are evolving from broad, exploratory alliances (like early-stage agreements in China) to highly specific, transactional deals. A key example is the 2025 agreement between BP and Japan’s Chubu Electric Power. This partnership aims to create a value chain to transport CO2 from industrial sources in Japan for storage at the Tangguh project in Indonesia, establishing a commercial model for cross-border carbon management and storage-as-a-service.