Zero Avia PEM Fuel Cell Delays, $116 M Airbus Funding, 100 Engine American Airlines Deal, and 2-Year Certification Shift (2023 to 2026)

Hydrogen Aviation Commercial Scale, Zero Avia and Airbus Project Delays

The path to commercial hydrogen-powered aviation has narrowed significantly, with timelines for entry-into-service pushed back by several years due to persistent certification and technology hurdles. The initial optimism surrounding rapid adoption has been replaced by a recalibration of expectations, as market leaders Zero Avia and Airbus have both announced major delays and strategic pivots. This shift effectively rules out commercially scheduled passenger flights using hydrogen fuel cells for regional airlines before 2030.

- Between 2021 and 2024, market momentum built around aggressive targets, exemplified by Zero Avia’s successful test flight of a Dornier 228 in January 2023 and its accumulation of conditional orders. This progress created a widespread expectation that its ZA 600 powertrain would enter service by 2025 or 2026.

- The first major reality check occurred in February 2025, when reports confirmed Airbus had suspended its high-profile ZEROe program. This decision removed the industry’s most significant top-down driver for large hydrogen aircraft and signaled that the underlying powertrain technology was not maturing as expected.

- This was followed by Zero Avia’s critical announcement in February 2026 of a significant delay in its certification timeline. The company now aims to certify only its fuel cell system in 2027, with the full powertrain certification not expected until up to two years later, pushing commercial readiness to 2029 at the earliest.

- In response to these core aviation challenges, a strategic pivot toward niche applications has emerged. Zero Avia’s November 2025 agreement with Hybrid Air Vehicles to develop a hydrogen-electric version of the Airlander 10 airship indicates a diversification into markets with potentially different certification pathways and operational demands.

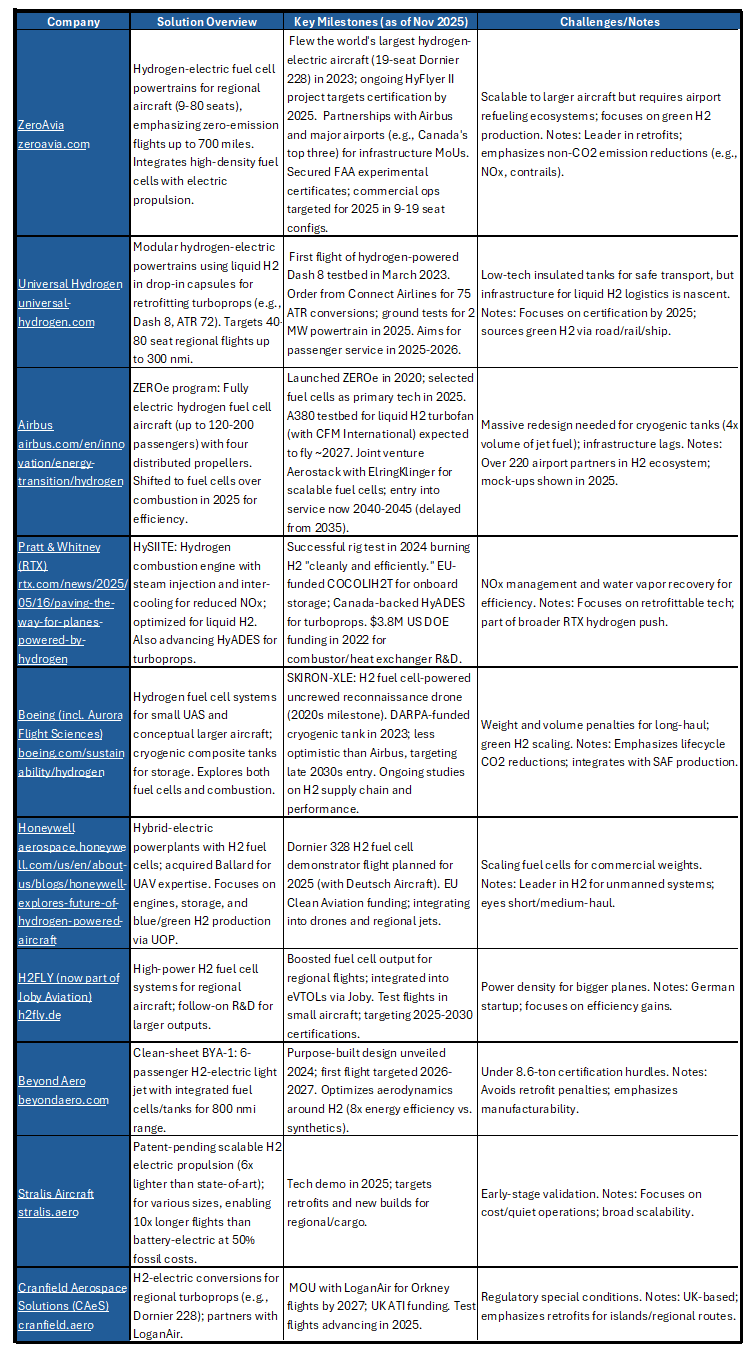

Hydrogen Aviation Milestones and Delays

This table details project delays for key players like Airbus and ZeroAvia, directly supporting the section’s focus on recalibrated timelines and strategic pivots.

(Source: AirInsight)

$116 M Series C, Zero Avia Navigates Certification Headwinds

While significant private and public funding flowed into the sector based on aggressive timelines, recent delays expose projects to increased financial risk and highlight a structural shift in investment strategy. The focus is moving from backing near-term product launches to supporting more foundational, long-lead-time research and development. The challenges in aviation are part of a broader pattern seen across the hydrogen economy, where industrial users like Arcelor Mittal also face difficult investment decisions.

- Investor confidence peaked in November 2023 when Zero Avia secured $116 million in a Series C funding round. The participation of strategic investors, including Airbus and American Airlines, was a strong endorsement of its powertrain retrofit strategy and its original 2025 commercialization target.

- The suspension of the Airbus ZEROe program in 2025 marked a significant de-facto cancellation of a near-term commercial product. This pivoted financial resources toward government-backed R&D, as seen with Germany’s new research program launched in April 2026 to support Airbus in developing next-generation fuel cell components.

- Government support is adapting to the longer timelines. The UK government’s grant of £10.8 million ($13.7 million) to Zero Avia in June 2025 was specifically aimed at developing and testing liquid hydrogen (LH₂) systems, a foundational technology required for larger aircraft and a tacit acknowledgment that the path to market is longer than first anticipated.

Table: Hydrogen Aviation Investment and Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Airbus ZEROe Program | Feb 2025 | Airbus suspended its program to develop a commercial hydrogen aircraft by 2035, citing delays in powertrain technology. This effectively canceled a near-term product launch in favor of a longer-term R&D focus. | Hydrogen Insight |

| Zero Avia Series C Funding | Nov 2023 | Raised $116 million from investors including Airbus, Barclays, and NEOM to scale its 600 k W and 2 MW powertrain development and support its original 2025 entry-into-service target. | Zero Avia |

| Zero Avia UK Gov. Funding | Jun 2025 | Secured £10.8 million ($13.7 million) in UK government funding to advance the development and flight testing of liquid hydrogen (LH₂) systems for larger aircraft, a longer-term technological challenge. | H 2-View |

Zero Avia 100 Engine Deal, American Airlines and Airbus Alliances

Partnerships formed before 2025 were largely predicated on optimistic entry-into-service dates, but the recent timeline shifts are testing these foundational alliances. The dynamic is evolving from straightforward supplier-customer relationships for fleet conversion to more integrated co-development work and a diversification into specialized, non-traditional aviation markets.

- The landmark conditional purchase agreement with American Airlines in July 2024 for up to 100 engines remains a cornerstone of Zero Avia’s order book. However, its fulfillment is now contingent on a successful certification campaign concluding closer to 2029, a significant delay from initial expectations.

- The high-profile partnership between Airbus and CFM International to develop hydrogen combustion technology has been functionally subordinated. With the suspension of the ZEROe program, this collaboration shifts from a near-term product development effort to a longer-range research initiative without a defined commercial airframe.

- A new partnership model focused on niche applications emerged in November 2025 with the agreement between Zero Avia and Hybrid Air Vehicles. This collaboration to supply four ZA 600 powertrains for the Airlander 10 airship signals a strategic pivot toward vehicle types that may offer a less complex and faster path to certification than traditional passenger turboprops.

- The expansion of fuel cell technology into new mobility sectors, such as seen with GM Defense, underscores the broad applicability of the core technology, even as specific market segments like aviation face unique integration and regulatory challenges.

Table: Key Hydrogen Aviation Partnerships and Alliances

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Zero Avia and Hybrid Air Vehicles | Nov 2025 | Partnership to collaborate on a hydrogen-electric version of the Airlander 10 airship. This diversifies Zero Avia‘s application portfolio into a niche market with different operational and certification requirements. | Airport Technology |

| Zero Avia and American Airlines | Jul 2024 | American Airlines made a conditional commitment to purchase up to 100 of Zero Avia‘s hydrogen-electric engines. This provides a critical commercial anchor for the ZA 2000 powertrain program for regional jets. | Zero Avia |

| Zero Avia and MHIRJ | May 2022 | Partnership to develop a hydrogen-electric propulsion system for CRJ-series regional jets, a key target market for Zero Avia‘s larger ZA 2000 powertrain. | Air Insight |

UK vs US Focus, Zero Avia Hydrogen Aviation Development

While early development was concentrated in the UK and US, supported by robust government grants and aerospace expertise, the strategic pivot by Airbus has shifted Europe’s large-scale commercialization focus further into the future. This change reinforces the UK’s position as the primary global hub for near-term regional hydrogen powertrain development and certification, with the US serving as a crucial parallel regulatory and testing market.

- Between 2021 and 2024, the UK and US emerged as dual epicenters for Zero Avia‘s operations. The company established R&D and flight testing facilities in both countries to capitalize on distinct funding opportunities, such as the UK’s Aerospace Technology Institute (ATI) Programme, and deep talent pools.

- The suspension of Airbus‘s ZEROe program in 2025, centered in France and Germany, was a significant setback for Europe’s ambition to lead in large hydrogen aircraft. Subsequent government actions, like Germany’s April 2026 funding for foundational Airbus R&D, confirm a strategic retreat from a 2035 product launch to a much longer-term research cycle.

- The US regulatory pathway remains critical and active. The FAA’s issuance of special conditions for certifying Zero Avia‘s electric motor in April 2026 demonstrates ongoing progress. However, with the core development and flight testing for the ZA 600 system centered at its UK base in Kemble, this region remains the critical path for achieving the world’s first commercial certification.

PEM Fuel Cell Maturity, Zero Avia Certification Delays and Test Data

The core PEM fuel cell technology has successfully matured from component-level validation to integrated system demonstrations in the megawatt-class range. However, the period from 2025 onward has revealed that achieving certifiable reliability, durability, and performance for an entire propulsion system is a far greater challenge than suggested by early prototype flight tests.

- The period between 2021 and 2024 was defined by key subsystem victories, highlighted by Zero Avia successfully flying a Dornier 228 testbed in January 2023. This milestone created a powerful, if ultimately misleading, perception of rapid progress toward a 2025 commercial entry.

- A crucial validation of the core technology occurred in September 2025, when Zero Avia completed a full 250-mile flight profile on a ground-based test rig. This success was paradoxically followed by the February 2026 announcement that certifying the *entire powertrain* would take up to two years longer than certifying the fuel cell system alone, exposing the complexity of system integration.

- The Airbus pivot in February 2025 served as a definitive verdict on the immaturity of megawatt-class fuel cell systems and liquid hydrogen storage for large commercial aircraft. It effectively reset the Technology Readiness Level (TRL) for that market segment back to a foundational research phase.

- The regulatory focus has now shifted from celebrating “firsts” to the difficult work of certification. The FAA’s issuance of special conditions in April 2026 for just one part of the system, the electric motor, underscores the granular, multi-year complexity of certifying every component in a novel propulsion unit. The hurdles are similar to those being addressed in stationary power by firms like Hyundai, showing a cross-industry challenge.

SWOT Analysis, Zero Avia’s Strengths and Market Threats

Hydrogen aviation’s primary strength lies in its potential for true zero-carbon flight, which has attracted powerful airline partnerships and government support. However, this is counterbalanced by significant weaknesses in infrastructure and certification complexity. The recent timeline delays have elevated the pragmatic advantages of Sustainable Aviation Fuel (SAF), creating a major near-term competitive threat.

ZeroAvia’s Hydrogen Aviation Ecosystem

This diagram shows the full “well-to-wake” process, visually representing the scope of the strengths and infrastructure-related weaknesses discussed in the SWOT analysis.

(Source: CleanTechnica)

- The analysis highlights a strong and growing order book, anchored by major airlines, as a key strength.

- The complete absence of airport-based hydrogen production, storage, and refueling infrastructure remains a critical weakness that inhibits network planning.

- An emerging opportunity is the pivot to niche, specialized aviation markets like cargo drones and airships, which may offer faster paths to commercialization.

- The most significant threat is the timeline itself; extended delays make SAF a more attractive and viable medium-term decarbonization solution for airlines needing to meet emissions targets this decade.

Table: SWOT Analysis for Hydrogen-Powered Aviation

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Strong government support (e.g., UK’s ATI) and early airline interest based on ambitious timelines. | Major airline partnerships are formalized (e.g., American Airlines for 100 engines), creating a substantial conditional order book. | The strength shifted from potential interest to a tangible, albeit conditional, market demand. This validates the commercial proposition, assuming technology can be certified. |

| Weakness | Technology is at the prototype stage. Lack of airport hydrogen infrastructure is a known future problem. | Certification complexity becomes a primary, acknowledged barrier. The gap between a working prototype and a certifiable product is now quantified in years. | The weakness evolved from a theoretical technology risk to a validated, schedule-impacting certification hurdle. The infrastructure problem remains unresolved and more acute. |

| Opportunity | Focus is almost exclusively on retrofitting existing regional aircraft (e.g., Dornier 228, Dash 8). | Diversification into adjacent, niche markets like airships (Hybrid Air Vehicles) and e VTOL (Horizon Aircraft) emerges as a viable strategy. | The opportunity set expanded. The realization that traditional passenger certification is slow has opened parallel tracks in less regulated or novel air vehicle markets. |

| Threat | SAF is seen as a parallel, but distinct, long-term solution. The primary threat is failing to meet technical milestones. | Hydrogen’s delayed timeline makes SAF a more dominant and pragmatic near-to-medium-term competitor for airline capital and offtake agreements. | The competitive threat from SAF became more immediate. With hydrogen’s entry pushed to post-2028, SAF is solidified as the only viable path for emissions reduction this decade. |

2027 Certification, Zero Avia’s Phased Rollout for Regional Aviation

The most critical path for 2027 is Zero Avia achieving its revised target of certifying the core fuel cell system. This milestone would serve as a powerful validation of the technology for investors, partners, and regulators, providing crucial momentum even as the full powertrain integration and certification continue toward a 2029 goal.

ZeroAvia’s Phased Aircraft Scaling Strategy

This chart visualizes ZeroAvia’s phased rollout plan, which starts with regional aircraft and scales up, directly corresponding to the certification and rollout strategy described.

(Source: Aerospace Global News)

- If Zero Avia meets its 2027 fuel cell system certification target, watch for a new wave of funding and partnerships aimed at deploying the system in non-passenger applications like cargo or surveying, which have a lower regulatory barrier and can build operational hours.

- If the 2027 milestone is missed, or if the full powertrain certification timeline slips beyond 2029, expect some early airline partners to reduce or cancel conditional orders in favor of securing larger volumes of SAF to meet their mandated emissions targets.

- A leading indicator of this dynamic is the volume and value of SAF offtake agreements signed by major airlines. A continued acceleration in SAF deals by carriers with hydrogen MOUs, combined with persistently high green hydrogen cost projections, would signal a further loss of confidence in near-term hydrogen aviation. This economic reality is a key factor across the entire hydrogen market.

The questions your competitors are already asking

This report covers one angle of the commercial trajectory for hydrogen-powered aviation. The questions that matter most depend on your work.

- What is the outlook for hydrogen fuel cell deployment in regional aviation by 2030?

- What is actually happening with ZeroAvia’s 100-engine American Airlines deal since the certification timeline shifted to 2029?

- How does hydrogen fuel cell propulsion compare to Sustainable Aviation Fuel (SAF) for decarbonizing regional aviation?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.