Climeworks DAC Offtakes, $162 M Fund, Schneider Electric Deal, and 5 Major Agreements (2025)

Offtake Agreements, Climeworks Secures 100 k+ Tonnes in 2025

The Direct Air Capture market’s growth mechanism solidified in 2025, with companies like Climeworks leveraging large, multi-year corporate offtake agreements to de-risk the immense capital required for technology development and megaproject deployment.

- Between 2021 and 2024, the market was defined by smaller, pilot-scale agreements with early adopters like Microsoft, which retired 700 tonnes of removal credits from the Orca plant. These deals were crucial for technology validation.

- The year 2025 marked a significant shift to industrial-scale demand, with Climeworks securing over 100, 000 tonnes in new long-term offtake commitments. Key agreements included a 31, 000-tonne deal with Schneider Electric and a 40, 000-tonne deal with Morgan Stanley.

- This new class of agreements extends delivery timelines out to 2039, providing the long-term revenue certainty needed to secure financing for capital-intensive projects like the 36, 000-tonne-per-year Mammoth plant.

- The customer base also diversified, moving beyond the tech sector to include industrial and logistics giants. Climeworks signed its first shipping industry partner, Mitsui O.S.K. Lines, for a 15, 000-tonne removal, signaling broadening market adoption.

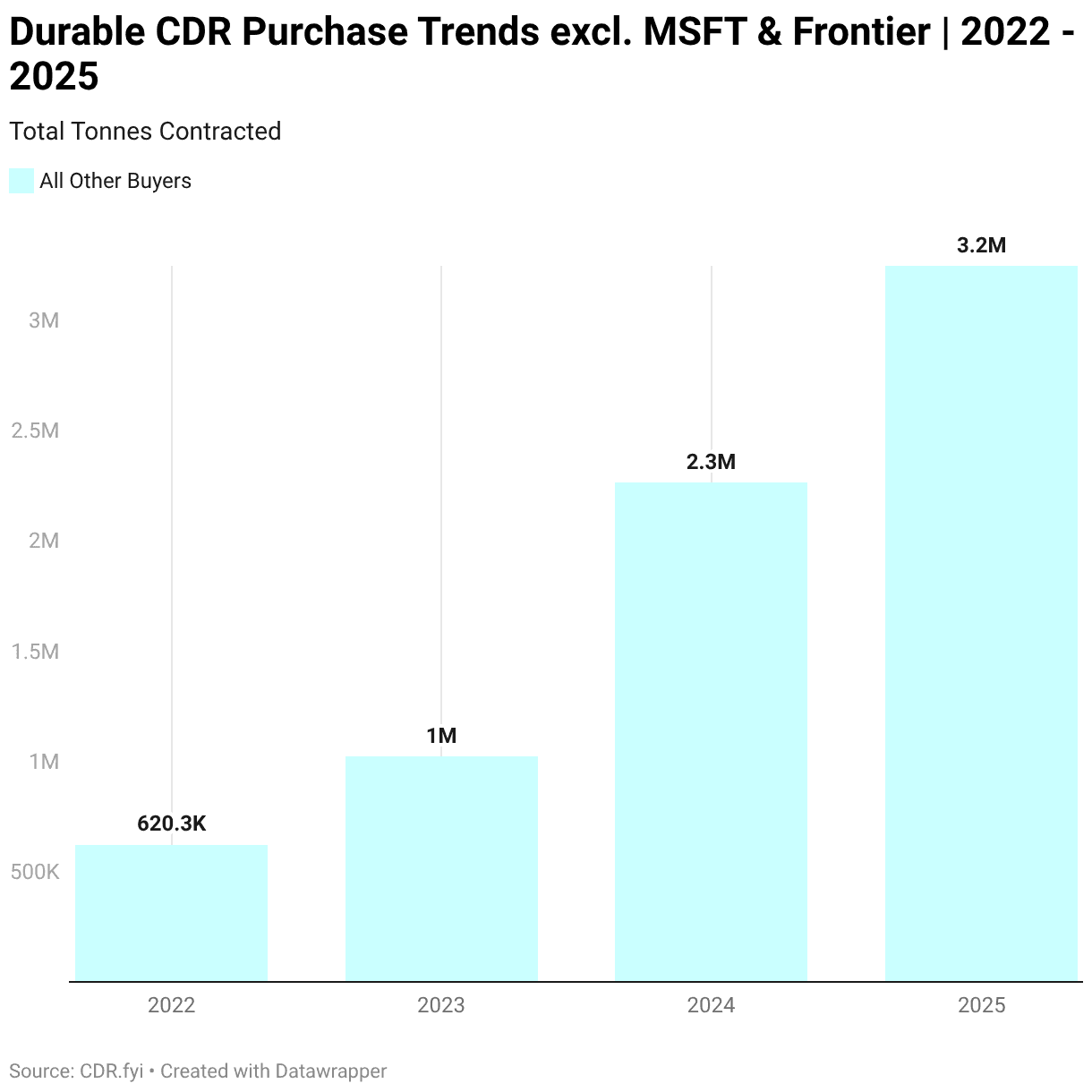

Durable CDR Offtakes Surge Through 2025

The section discusses Climeworks securing over 100,000 tonnes in offtake agreements. This chart, showing a surge in durable Carbon Dioxide Removal (CDR) offtakes, directly visualizes the growing market demand that enables such large-scale agreements.

(Source: CDR.fyi)

$162 M Equity Round, Climeworks’ Funding Exposes Scaling Pressures

Climeworks demonstrated its ability to attract significant private capital in 2025, but this success was tempered by strategic restructuring that revealed the company’s sensitivity to broader economic conditions and government policy uncertainty.

- The company successfully closed a $162 million equity round in July 2025, the largest carbon removal investment of the year, pushing its total funding past the $1 billion mark. This capital is explicitly earmarked for advancing its Generation 3 technology.

- Just two months prior, in May 2025, Climeworks announced a workforce reduction of over 10%, affecting up to 106 positions, to “maintain agility and efficiency” amidst economic uncertainty.

- This restructuring was linked to potential cuts in U.S. Department of Energy funding for major Direct Air Capture hubs, a critical policy support for the company’s planned North American expansion.

- This juxtaposition of a major fundraise and layoffs highlights the core challenge for the industry: managing high operational cash burn and long development cycles while navigating volatile market and policy environments.

CDR Market Transactions Exceed $200M in Q1 2025

The section details Climeworks’ specific $162M equity round. This chart provides the broader market context, demonstrating that this funding is part of a larger wave of investment in the Carbon Dioxide Removal (CDR) sector, validating investor confidence.

(Source: CleanTechnica)

Table: Climeworks Key Financial and Strategic Actions (2025)

| Date | Action / Event | Details and Strategic Purpose | Source |

|---|---|---|---|

| Jul 2, 2025 | Equity Funding Round | Raised $162 million to accelerate Generation 3 DAC technology and scale operations, bringing total funding over $1 billion. | Wall Street Journal |

| May 21, 2025 | Workforce Reduction | Reduced workforce by over 10% (up to 106 positions) to manage costs and maintain efficiency in response to economic uncertainty and potential U.S. policy shifts. | The Guardian |

| May 15, 2025 | Gen 3 Technology Announcement | Announced a major R&D focus on its Generation 3 technology, aimed at doubling capture efficiency and halving energy consumption to reach cost targets of $250-$350/tonne. | Clean Technica |

Timeline of Direct Air Capture Industry Milestones

This section is a table detailing key actions in 2025. A timeline of industry milestones provides historical context, allowing the reader to understand the significance of Climeworks’ 2025 actions within the broader evolution of the DAC industry.

(Source: BCC Research)

US vs. Iceland, Climeworks’ Geographic Expansion Faces Headwinds

While Climeworks successfully scaled its operational footprint in Iceland, its expansion into the critical North American market faced significant headwinds in 2025, highlighting the dependence of DAC projects on stable, large-scale government incentives.

- From 2021 to 2024, Climeworks‘ strategy was centered on Iceland, leveraging the country’s abundant geothermal energy to launch its Orca and then Mammoth plants, de-risking the technology in a favorable environment.

- In 2025, the Mammoth plant in Iceland became the world’s largest operational DAC facility, solidifying the company’s technical leadership and its ability to execute projects where clean energy is available.

- However, the company’s plans to expand into the U.S. to leverage the $180/tonne 45 Q tax credit hit a snag. Reports in October 2025 surfaced about potential U.S. Department of Energy funding cuts for large DAC hubs, including Project Cypress in Louisiana, where Climeworks is a partner.

- This uncertainty was a direct contributor to the company’s strategic workforce reduction, showing how dependent large-scale DAC expansion is on consistent government policy, a risk not present in its privately-funded Icelandic operations.

US Dominates Announced DAC Project Pipeline

The section compares Climeworks’ efforts in the US and Iceland. This chart, which highlights US dominance in the project pipeline, graphically explains the strategic rationale and the competitive landscape for Climeworks’ geographic expansion into North America.

(Source: Internationale Politik Quarterly)

Climeworks Gen 3 Tech, 50% Energy Reduction Target (2025)

Climeworks advanced its technology to a high readiness level with the validation of its Gen 3 design, shifting the central challenge from proving the science works to proving it can be manufactured and operated at a cost-competitive industrial scale.

- Before 2025, the primary focus was on proving operational reliability at scale, which Climeworks achieved with its Orca plant and further validated with the commissioning of Mammoth. The technology was considered mature, with a Technology Readiness Level (TRL) of 7-8.

- In 2025, the strategic focus pivoted to cost reduction through innovation. The company announced its Generation 3 technology aims to halve energy consumption and double CO 2 capture efficiency per module.

- This technological push is a direct response to the high cost of removal, currently estimated between $600 and $1, 000 per tonne. Achieving the targeted $250-$350 per tonne by 2030 is entirely dependent on the successful deployment of this new, more efficient hardware.

- The company also deployed a small demonstration unit in Saudi Arabia in July 2025, not for scale but to test its technology’s performance in a different climate and showcase it to regional stakeholders, a key step in global market development.

Chart Analyzes Cost Drivers for Direct Air Capture

The section focuses on Climeworks’ Gen 3 technology and its 50% energy reduction target. This chart, by breaking down the cost drivers of DAC, perfectly illustrates why a reduction in energy consumption is a critical technological goal for achieving economic viability.

(Source: Nature)

SWOT Analysis, Climeworks Strengths vs. Market Risks

The strategic position of Climeworks in 2025 reflects a company successfully transitioning from technology developer to industrial operator, though this transition exposes it to significant market and policy risks.

- Strengths: The company’s primary strength is its established technological leadership and proven operational capability at a scale no other DAC company has achieved.

- Weaknesses: Its business model remains highly dependent on external factors, including volatile government subsidies and a nascent voluntary carbon market, making it vulnerable to economic and political shifts.

- Opportunities: The massive, multi-year offtake agreements signed in 2025 represent a significant opportunity to secure long-term revenue and finance the next generation of megaton-scale plants.

- Threats: The primary threat is the failure to drive down costs. If Gen 3 technology does not deliver the promised cost reductions, the company will struggle to compete for capital and corporate climate budgets.

Key Factors Driving the Carbon Capture Market

This section provides a SWOT analysis for Climeworks. A chart detailing the key factors driving the market directly supports the ‘Opportunities’ and ‘Threats’ components of the analysis by outlining the external forces shaping the industry.

(Source: Coherent Market Insights)

Table: SWOT Analysis for Climeworks’ DAC Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | First-mover advantage with Orca plant (4 k t/yr); strong initial corporate partnerships (e.g., Microsoft). | Operational leadership with Mammoth plant (36 k t/yr); technology readiness (TRL 7-8); secured over $1 B in total funding. | Validated the ability to scale technology tenfold and attract significant growth capital, solidifying its market-leading position among Carbon Capture & DAC Leaders. |

| Weaknesses | Extremely high cost of removal; reliance on a small pool of early-adopter customers; limited operational scale. | High operational cost ($600-$1, 000/t); high CAPEX (up to $3, 000/t capacity); pre-profit, capital-intensive scale-up phase. | The financial realities of industrial scaling became clear; high costs are no longer theoretical but a tangible operational challenge that must be solved. |

| Opportunities | Emerging corporate net-zero targets; growing interest in high-durability carbon removal credits. | Secured large-volume, multi-year offtake agreements (Schneider, MOL); development of Gen 3 tech to halve energy use; expansion into new markets. | Corporate demand was validated as a bankable source of revenue to underwrite future projects, shifting from pilot-level purchases to strategic, long-term supply agreements. |

| Threats | Technological scaling risk; competition from other carbon removal pathways; lack of clear policy support. | Uncertainty over U.S. government funding (DOE DAC Hubs); high sensitivity to energy prices; failure to meet cost-down targets for 2030. | The threat shifted from “can the tech work?” to “can the business model survive without massive, consistent subsidies?” The company’s restructuring highlighted its vulnerability to policy changes. |

Climeworks vs. Carbon Engineering DAC Projects Compared

This section is a table-based SWOT analysis. A direct competitive comparison is a crucial input for a SWOT, particularly for assessing ‘Strengths’ and ‘Weaknesses’. This chart provides that essential competitive intelligence at a glance.

(Source: Terraform Now)

Scenario Modelling: Climeworks’ Path to Megaton Scale

The single most critical factor for Climeworks‘ future is the operational performance of the Mammoth plant and the subsequent deployment of its cost-reduced Generation 3 technology.

- If this happens: The Mammoth plant consistently operates at or near its 36, 000-tonne annual capacity throughout the next 12-18 months.

- Watch this: Quarterly and annual reports on delivered and verified tonnes from Mammoth. Announcements of the location and timeline for the first plant to use Gen 3 technology.

- This could be happening: Success at Mammoth would validate the company’s “deployment-led innovation” strategy, proving it can execute at an industrial scale. This would de-risk future investments and likely trigger a new wave of even larger corporate offtake agreements, providing the financial foundation to proceed with megaton-scale facilities. Conversely, any significant underperformance would raise serious questions about the technology’s reliability and the company’s ability to meet its existing contractual obligations.

Direct Air Capture Market to See 61% CAGR

The section models Climeworks’ path to megaton scale. A chart projecting a strong Compound Annual Growth Rate (CAGR) for the entire DAC market provides a fundamental assumption and macro-level justification for the aggressive scaling scenarios being modeled.

(Source: Research Nester)

The questions your competitors are already asking

This report covers one angle of Climeworks’ commercial scaling and market strategy for Direct Air Capture. The questions that matter most depend on your work.

- Climeworks’ activities in project deployment. Is the Mammoth plant progressing from construction to full commercial operation on schedule?

- Climeworks’ investments and funding. Is the $162M equity round sufficient to de-risk the financing for its next wave of megaprojects?

- Which industrial and logistics operators, beyond Schneider Electric and Mitsui O.S.K. Lines, are adopting Climeworks’ carbon removal services?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

Direct Air Capture Dominates Patent Activity

The section’s title refers to ‘questions your competitors are already asking’. Patent activity is a primary indicator of competitors’ R&D focus and future strategy. This chart provides key competitive intelligence on where the industry is investing in innovation.

(Source: AlliedOffsets)