DAC Offtake Agreements, sub-$200 JPMorgan Deal, $2.58 B Market Forecast, and 5+ Commercial Projects (2025)

DAC Commercial Projects: High Costs vs. Corporate Offtake Demand in 2025

The Direct Air Capture (DAC) market in 2025 is defined by a fundamental tension: the high cost of capture is clashing with surging corporate demand that signals a clear path to commercial scale. While the operational cost for current DAC technologies ranges from $300 to over $1, 000 per tonne, major corporations are signing multi-year offtake agreements at prices under $200 per tonne. This disconnect indicates that buyers have confidence in the technology’s cost-down trajectory, creating a significant opportunity for project developers who can validate lower-cost pathways and secure long-term revenue streams. The performance of pioneering large-scale projects in 2025 will serve as the critical validation point for the entire industry.

- The mid-2025 commissioning of Occidental’s Stratos DAC plant in Texas is the sector’s most important milestone. Its operational data on cost and efficiency will establish a new benchmark and heavily influence future investment decisions across the DAC market.

- Landmark commercial agreements define the 2025 landscape. JPMorgan Chase signed a large-scale offtake deal with CO 280 for carbon removal at a price point under $200 per ton, demonstrating market appetite for bankable, long-term contracts that de-risk new project development.

- While federal support like the Section 45 Q tax credit, valued at $180 per metric ton for DAC with geologic storage, is a critical enabler, the market is shifting focus. Success is now being measured by the ability to secure private offtake agreements that provide revenue certainty for capital-intensive projects.

- The project pipeline is expanding beyond initial hubs. In April 2025, Occidental’s subsidiary 1 Point Five announced a new carbon capture project in Louisiana, signaling a strategy of geographic diversification to capitalize on regional storage and industrial integration opportunities.

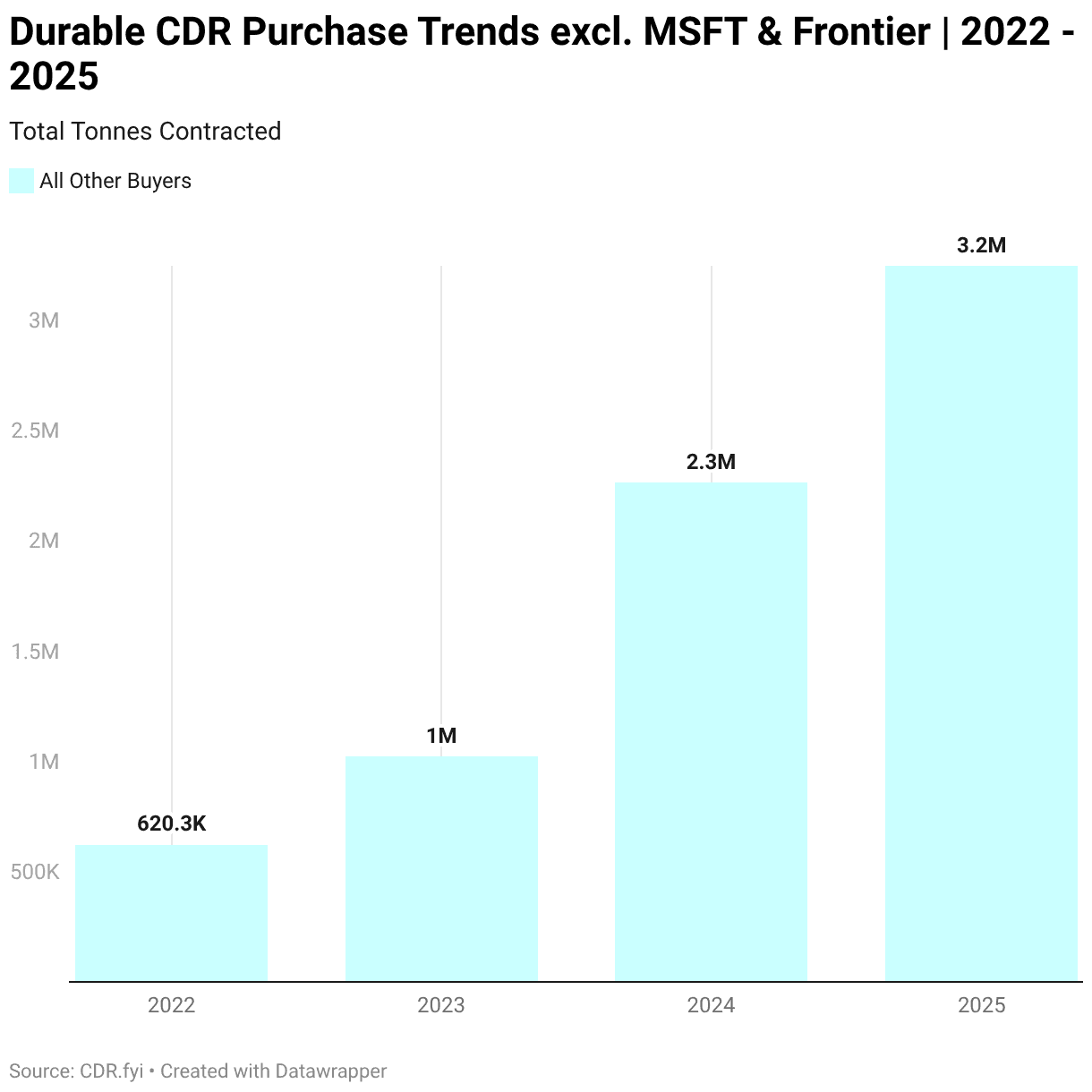

Corporate CDR Demand Surges Through 2025

This chart quantifies the strong corporate offtake demand mentioned in the section heading, illustrating the market pull that counterbalances the high costs of DAC projects.

(Source: CDR.fyi)

$137 M in Q 1 CDR Funding, DAC Market Growth Signals for 2025

Despite uncertainty around long-term federal funding for specific hubs, private investment in Carbon Dioxide Removal (CDR) accelerated in 2025, driven by the urgent need for developers to scale supply to meet corporate demand. The significant influx of capital, particularly into DAC-focused companies, demonstrates strong investor confidence in the sector’s growth trajectory and its ability to overcome near-term cost hurdles. This funding is primarily allocated to the capital expenditures for first-of-a-kind commercial facilities and validating next-generation technologies.

- In Q 1 2025, 24 companies in the CDR sector raised over $137 million in private equity. This investment was directly tied to scaling operations to satisfy the growing pipeline of corporate buyers seeking high-quality carbon removal credits.

- Volatility in public funding was signaled in March 2025 with reports that the Department of Energy (DOE) was considering funding cuts for two major DAC hubs. While these projects are projected to remove over 2 million metric tons of CO 2 annually, this development introduces risk for projects heavily reliant on government grants over private offtakes.

- Market infrastructure is maturing to support growth. On September 4, 2025, carbon removal crediting platform Puro.earth secured €11 million in a Series B round led by Nasdaq to enhance the platform’s ability to issue credits and facilitate long-term offtake agreements.

- Startup funding remains robust for companies with differentiated technology. The Los Alamos-based DAC startup Spiritus secured a $30 million Series A round in March 2025 to advance its novel sorbent technology, which aims for a capture cost below $100 per ton.

DAC Attracts 36% of Q1 CDR Funding

This chart provides the specific data point referenced in the section heading, confirming DAC’s leading position in attracting recent CDR investment and signaling market growth.

(Source: AlliedOffsets)

Table: Key DAC and CDR Investments in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| CDR Sector Companies | Q 1 2025 | 24 Carbon Dioxide Removal companies raised over $137 million in private equity to scale operations and meet the surge in corporate demand for carbon removal credits. | CDR.fyi |

| Puro.earth and Nasdaq | Sep 2025 | Puro.earth secured €11 million in Series B financing led by Nasdaq. The investment is aimed at building market infrastructure to support long-term offtake agreements. | Nasdaq |

| Spiritus | Mar 2025 | The DAC startup raised a $30 million Series A to advance development of its novel sorbent technology, targeting capture costs under $100/ton. | Albuquerque Business First |

| U.S. DAC Hubs | Mar 2025 | Reports emerged that the DOE was considering funding cuts for two federally backed DAC hubs, introducing uncertainty for their long-term financial outlook despite a planned 2 million metric ton annual capacity. | Carbon Herald |

DAC Dominates Durable CDR Investment from 2021-2025

This chart provides high-level context for the table of investments by showing DAC’s overarching dominance in attracting durable CDR funding over the past several years.

(Source: LinkedIn)

Key DAC Technology Partnerships, Leilac and Heirloom Target Cost Reduction

Strategic partnerships in 2025 are a primary mechanism for de-risking technology and accelerating the path to lower-cost DAC solutions. Collaborations are focused on adapting existing industrial processes for DAC, validating new capture methods, and creating integrated value chains from capture to sequestration. For a new entrant, these partnerships provide a template for building an ecosystem that connects technology innovation with industrial-scale deployment and market access.

- A key partnership announced in 2025 was between Leilac and Heirloom. The collaboration aims to apply Leilac’s innovative kiln technology to Heirloom’s limestone-based DAC process, directly targeting efficiency gains and cost reductions in the energy-intensive calcination step.

- Offtake agreements are increasingly structured as strategic partnerships. The agreement between Mitsui O.S.K. Lines and Captura Corp. in March 2025 for Direct Ocean Capture credits included a broader strategic alliance, demonstrating a move towards deeper collaboration between technology providers and buyers.

- Project developers are building portfolios of offtake partners to ensure financial stability. In June 2025, Deep Sky announced a multi-year offtake agreement with Rubicon Carbon, with credit deliveries scheduled between 2025 and 2033, providing long-term revenue visibility.

Mapping Corporate Demand to CDR Providers in 2025

This chart illustrates the commercial ecosystem where technology partnerships, such as those involving Heirloom, translate into offtake agreements between corporate buyers and providers.

(Source: AlliedOffsets)

Table: Strategic DAC Partnerships in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Leilac and Heirloom | Aug 2025 | Technology partnership to adapt Leilac’s kiln technology for Heirloom’s limestone-based DAC process, aiming to reduce energy consumption and cost. | Global CCS Institute |

| Deep Sky and Rubicon Carbon | Jun 2025 | Multi-year offtake agreement for permanent carbon removal credits. The deal provides Deep Sky with long-term revenue certainty for its project pipeline. | Deep Sky |

| JPMorgan Chase and CO 280 | May 2025 | Significant carbon removal offtake agreement securing a price under $200 per ton. The deal is intended to help finance CO 280’s projects, which aim to remove 10 million tons of CO₂ annually. | ESG Today |

| Mitsui O.S.K. Lines and Captura Corp. | Mar 2025 | Strategic partnership and offtake agreement for carbon removal credits from Captura’s Direct Ocean Capture technology, expanding the market into new methodologies. | Mitsui O.S.K. Lines |

DAC Market Projected to Reach $2B by 2030

This chart provides the financial motivation for the strategic partnerships detailed in the table, highlighting the significant near-term market size that companies are collaborating to capture.

(Source: P&S Intelligence)

US Leads DAC Deployment, Occidental Texas Project Anchors 2025 Growth

The United States solidified its position as the global center for large-scale DAC deployment in 2025, driven by a combination of supportive federal policy, significant private investment, and favorable geology for sequestration. Activity is concentrated in the Gulf Coast region, particularly Texas and Louisiana, where companies are leveraging existing infrastructure and expertise from the oil and gas industry. For a potential Cincinnati-based initiative, this geographic concentration highlights the importance of securing access to suitable geological storage and building regional industrial partnerships to compete.

- The commissioning of Occidental’s Stratos project in the Texas Permian Basin is the anchor of U.S. DAC activity in 2025. Its success is critical to validating the model of large-scale deployment in the region.

- The U.S. project pipeline represents a total capital investment of $77.5 billion across more than 270 publicly announced carbon capture projects, with DAC representing a growing and high-profile segment of this investment.

- Expansion into Louisiana is a key trend in 2025. 1 Point Five announced a new project in the state in April 2025, seeking to replicate its Texas model in another region with deep saline aquifers suitable for permanent CO₂ storage.

- While the U.S. leads in commercial-scale projects, the global pipeline is also growing. As of April 2025, over 700 Carbon Capture and Storage (CCS) projects were in development globally, highlighting the worldwide scale of ambition, though most are smaller or focused on point-source capture.

US Dominates Planned DAC Project Capacity

This chart directly visualizes the section’s core assertion, geographically breaking down planned capacity to show the commanding leadership of the US in DAC deployment.

(Source: Internationale Politik Quarterly)

DAC Technology at TRL 9, Commercial Viability Hinges on Cost in 2025

While Direct Air Capture technology is considered commercially available with a Technology Readiness Level (TRL) of 9, the primary barrier to mass deployment is economic viability, not technical feasibility. The industry-wide goal is to drive the cost of capture down from the current $300-$500+ per tonne range to the target of $100 per tonne. Innovations in sorbents, process efficiency, and energy integration are the critical pathways to closing this economic gap, with several promising next-generation technologies moving toward pre-commercial validation in 2025.

- The dominant DAC approach in 2025 uses liquid solvents or solid sorbents to chemically bind with CO₂. The innovation focus is on developing materials that require less energy for regeneration, which is the most cost-intensive part of the process.

- Emerging technologies show a credible path to the $100/tonne target. Research published in November 2025 on pyridinic-N-rich membranes suggests a theoretical capture cost of just $25-$50 per ton, representing a potential disruption if commercialized.

- Energy sourcing is a key area of innovation. A project announced in Texas in March 2025 plans to be the world’s first DAC facility powered directly by on-site wind power, aiming to lower both operational costs and the overall carbon footprint of the capture process.

- Alongside DAC, other carbon removal pathways are gaining traction. A U.S. legislative proposal in June 2025 to create a tax credit for Biomass Carbon Removal and Storage (Bi CRS) indicates a diversification of policy support beyond purely technological removal solutions.

DAC Cost-Benefit Scenarios Projected to 2050

This chart directly supports the section’s focus on commercial viability by projecting long-term cost-benefit scenarios, which are crucial for evaluating the technology’s path to profitability.

(Source: Nature)

SWOT Analysis for DAC Initiatives in 2025

The strategic environment for a new Direct Air Capture initiative in 2025 is characterized by strong market-pull and policy support, which create significant opportunities. However, these are counterbalanced by substantial threats related to high upfront costs, technological competition, and potential shifts in government funding priorities. A successful strategy requires leveraging policy incentives to attract capital while aggressively pursuing cost-reduction pathways to secure long-term, private-sector offtake agreements.

DAC Market to Reach $120B by 2034

This chart quantifies a major “Opportunity” within a SWOT analysis, showcasing the massive long-term market potential that encourages investment in DAC initiatives despite current challenges.

(Source: Market.us)

Table: SWOT Analysis for a New DAC Initiative in 2025

| SWOT Category | Pre-2025 Context | 2025 Status | What Changed / Validated |

|---|---|---|---|

| Strengths | Technology proven at pilot scale; existence of 45 Q tax credit. | Technology validated at commercial scale (TRL 9); 45 Q credit enhanced to $180/ton for DAC; a robust pipeline of 270+ U.S. projects. | Commercial readiness is no longer in question. The economic incentive provided by the 45 Q credit is a powerful and bankable strength for new projects. |

| Weaknesses | High estimated costs ($600-$1, 000/ton); high energy consumption. | High realized costs ($300-$500+/ton); significant OPEX from energy needs remains a primary challenge. | While costs have come down from early estimates, they remain the single largest weakness and barrier to profitability without subsidies. |

| Opportunities | Emerging corporate climate goals and demand for carbon credits. | Surge in demand for high-quality removal credits; major corporations (JPMorgan Chase) signing multi-year offtake deals at sub-$200/ton prices; $137 M+ in Q 1 private funding for CDR. | The market for offtake agreements has matured rapidly, creating a bankable, private-sector revenue stream that did not exist at scale previously. This is the single largest opportunity. |

| Threats | Policy uncertainty; competition from cheaper nature-based solutions. | Potential for DOE funding cuts to major DAC hubs; emergence of highly competitive, low-cost technologies (e.g., membranes at $25-$50/ton); long-term stability of 45 Q policy. | The primary threats shifted from general policy risk to specific project-level funding risk and the pace of technological obsolescence from lower-cost innovators. |

DAC and BECCS Dominate CDR Market Value

This chart sets the competitive context for the SWOT analysis table, highlighting DAC’s market position as a “Strength” and the presence of BECCS as a potential “Threat”.

(Source: AlliedOffsets)

Scenario Modelling: A New Entrant’s Path to DAC Success in 2026

For a new entrant like a hypothetical “Cincy Carbon, ” success in the DAC market beyond 2025 will be determined by its ability to secure a multi-year offtake agreement predicated on a credible, lower-cost technology pathway. The window of opportunity is driven by the current imbalance between high corporate demand and limited supply of high-integrity carbon removal. Watching the operational cost data from Occidental’s Stratos plant and the price points of the next wave of offtake agreements will be critical for shaping a competitive strategy.

- If the Stratos plant’s operational costs in its first year are publicly or privately signaled to be in the $300-$400 per ton range, watch for a surge of investment into next-generation technologies that promise a clear path to sub-$200 per ton, as the market will see first-generation technology as uncompetitive long-term.

- If the DOE confirms funding reductions for its major DAC hubs, watch for project developers to immediately shift their financing strategies to be more heavily weighted toward private equity and offtake agreements. This could slow deployment but will accelerate the market’s focus on purely commercial viability.

- If another major corporation signs an offtake agreement at a price point near or below $150 per ton, this could indicate that buyers are confident that the $100 per ton target is achievable within the contract’s delivery window (5-10 years). This would put immense pressure on all developers to demonstrate a similar cost trajectory.

CDR Projected to Scale Rapidly to Meet 2050 Targets

This chart establishes the macro-level scenario for a new entrant, showing the rapid and large-scale market expansion required to meet climate targets, which defines the overall opportunity.

(Source: Clean Air Task Force)

The questions your competitors are already asking

This report covers one angle of Cincy Carbon’s DAC initiatives and market strategy for 2025. The questions that matter most depend on your work.

- What is actually happening with Occidental’s Stratos DAC plant, and will its operational data validate a new industry cost benchmark in 2025?

- JPMorgan Chase’s sub-$200/tonne offtake deal with CO280. Is this price point a viable investment benchmark for new projects?

- What are the opportunities for project developers given the gap between current DAC costs and corporate offtake prices?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

DAC Purchase Volume Trends from 2022-2025

This chart directly addresses the “questions your competitors are asking” by providing concrete data on the trajectory and growth of actual customer purchase volumes over time.

(Source: CDR.fyi)