CNOOC LNG Bunkering Strategy: CLP Group JV, 2 New Oilfields, and 2 Strategic Shifts (2021-2025)

CNOOC’s Dual-Track Energy Strategy, 2 New Oilfields vs. 1 New JV

In 2025, China National Offshore Oil Corporation (CNOOC) is executing a dual-track strategy, simultaneously maximizing its core hydrocarbon production while making calculated entries into adjacent low-carbon markets. This approach prioritizes near-term energy security and revenue from fossil fuels, using that foundation to fund a cautious, synergistic expansion into new energy sectors where its existing infrastructure provides a competitive advantage.

- From 2021 to 2024, CNOOC focused on developing its upstream assets and LNG supply chains. This period laid the groundwork for the strategic moves seen in 2025.

- In 2025, CNOOC brought major new hydrocarbon projects online, including the Bozhong 26-6 Oilfield and the Kenli 10-2 Oilfields, reinforcing its commitment to its primary oil and gas business.

- Concurrently, CNOOC is leveraging its extensive LNG infrastructure by forming a joint venture with CLP Group (CLPe) in August 2025 to provide LNG bunkering services in Hong Kong, marking a significant step into a distributed energy market.

- The company also stated its intent to prioritize offshore renewable energy projects, signaling a long-term plan to pivot its offshore operational expertise toward wind and other clean power generation, though concrete project investments remain in the future.

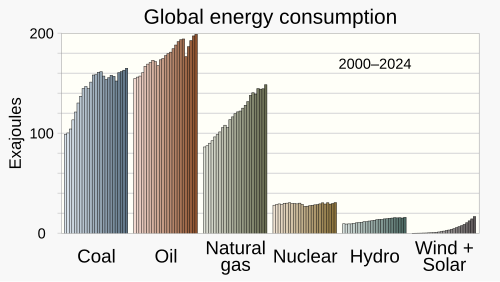

Fossil Fuels Dominate Global Energy Consumption Through 2024

This chart justifies CNOOC’s dual-track strategy. The continued dominance of fossil fuels in the near-term global energy mix provides the rationale for investing in new oilfields, while the impending transition necessitates parallel ventures into new energy.

(Source: Wikipedia)

CNOOC’s CLPe Joint Venture, a Strategic Entry to LNG Bunkering (2025)

CNOOC utilizes partnerships to enter new, lower-carbon markets with reduced risk, leveraging its core competencies in asset-heavy industries while relying on partners for market access and regional expertise. The collaboration with CLPe exemplifies this model, pairing CNOOC‘s LNG supply and infrastructure with CLPe‘s position in the Hong Kong energy market.

- The joint venture, expected to form in August 2025, is a direct outcome of a successful trial LNG bunkering operation in June 2025, validating the commercial and operational viability of the service.

- This partnership creates a new revenue stream for CNOOC that aligns with the maritime industry’s decarbonization push, turning its existing LNG assets into a distributed energy service for a growing market.

- This strategy of partnering to enter adjacent markets is also seen among its peers; for example, ADNOC partnered with Petronas in October 2025 to explore offshore CO₂ storage solutions, another instance of a national oil company leveraging partnerships for low-carbon ventures.

- The company’s interest alongside CNPC in Greenland’s offshore exploration, though halted by a government moratorium, shows a pattern of seeking partnerships for resource access, a model it is now applying to new energy services.

Table: CNOOC Strategic Partnerships and Peer Comparison (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| CNOOC / CLP Group (CLPe) | Aug 2025 | Formation of a joint venture to provide LNG bunkering services in Hong Kong. This leverages CNOOC‘s LNG assets to serve the decarbonizing maritime sector. | CLP Group |

| ADNOC / Petronas (Peer Activity) | Oct 2025 | Partnership to explore opportunities in offshore CO₂ storage. This shows a trend of national oil companies collaborating on low-carbon infrastructure. | Global CCS Institute |

| CNOOC / CNPC | Jul 2025 | Expressed joint interest in Greenland offshore oil and gas exploration, which was subsequently halted by a moratorium. This highlights a continued focus on securing traditional resources globally. | Carnegie Endowment |

China vs. Global, CNOOC Concentrates New Energy Efforts in Asia

CNOOC‘s initial foray into distributed and new energy is geographically concentrated on its home market and immediate region, aligning its transition strategy with China’s national energy security and decarbonization objectives. While its core fossil fuel business remains global, its new ventures are distinctly local.

- Between 2021 and 2024, CNOOC‘s geographic focus was on expanding its global upstream portfolio, including major projects like Payara in Guyana.

- In 2025, the company’s key new energy initiative, the LNG bunkering JV with CLPe, is based in Hong Kong, directly serving a major Chinese maritime hub.

- The major oilfields brought on stream in 2025, Bozhong 26-6 and Kenli 10-2, are located in China’s Bohai Sea, underscoring a push to bolster domestic production.

- This regional focus contrasts with the company’s thwarted global ambitions in traditional exploration, such as the interest in Greenland, suggesting a deliberate strategy to incubate new energy businesses in familiar territory before potential global expansion.

APAC Energy Transition Market Exceeds $1T

This chart provides the economic context for CNOOC’s strategic focus. By quantifying the massive scale of the energy transition market in the Asia-Pacific region, it validates the company’s decision to concentrate its new energy efforts there.

(Source: Fortune Business Insights)

Mature LNG Technology, CNOOC’s Application in New Bunkering Markets

CNOOC is mitigating technology risk by applying commercially proven technologies to new, growing markets rather than investing in early-stage, unproven clean technologies. The strategy centers on leveraging its decades of experience in offshore operations and LNG handling to secure a first-mover advantage in related low-carbon services.

- The period from 2021 to 2024 was characterized by the build-out and operation of large-scale LNG receiving terminals and associated infrastructure, solidifying CNOOC‘s technical expertise.

- In 2025, the company is monetizing this expertise by repurposing it for the LNG bunkering market, which uses the same fundamental technology but serves a different end-user (ships instead of grids).

- This approach avoids the high capital expenditure and uncertain returns associated with nascent technologies, focusing instead on operational excellence and market execution in a sector where CNOOC already holds a competitive advantage.

- While the company has stated an interest in offshore renewables, its actions in 2025 show a clear preference for business models that are direct extensions of its existing technological and operational capabilities.

SWOT Analysis: CNOOC’s Offshore Strengths and Energy Transition Risks

CNOOC‘s strategic position in 2025 is defined by the strength of its legacy offshore operations, which provides both the capital and the operational capability for a transition, yet also exposes it to significant stranded asset risk if the pivot to new energy is not executed effectively.

- Strengths: The company’s deep expertise in complex offshore projects and existing LNG infrastructure are significant competitive advantages, enabling moves into offshore wind and LNG bunkering.

- Weaknesses: A corporate structure and capital allocation process heavily weighted towards fossil fuels creates inertia and slows the pivot towards cleaner energy sources.

- Opportunities: The growing demand for LNG as a marine fuel and the potential to develop offshore wind farms in Chinese waters present clear growth pathways.

- Threats: Accelerating global decarbonization policies and competition from more agile pure-play renewable companies pose significant long-term challenges to its business model.

Table: SWOT Analysis for CNOOC’s Energy Transition Strategy (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 Status | What Changed / Validated |

|---|---|---|---|

| Strengths | Deep expertise in offshore E&P (e.g., Payara project development) and operation of LNG import terminals. | Leveraging offshore expertise to bring new oilfields (Bozhong 26-6) online and LNG infrastructure for a new bunkering JV with CLPe. | The 2025 strategy validates that existing operational strengths are the primary enablers for new ventures. The company is monetizing its core competencies in new markets. |

| Weaknesses | High dependence on fossil fuel revenue and capital-intensive upstream projects. Slow to enter renewable energy compared to some European peers. | Continued large-scale investment in oil and gas production, with new energy representing a small fraction of overall capital expenditure. | The 2025 business plan confirms that despite new initiatives, the company’s financial and operational center of gravity remains firmly in hydrocarbons, indicating a slow-paced transition. |

| Opportunities | Stated goals for low-carbon development and potential to build on offshore capabilities for wind energy. | Formation of LNG bunkering JV captures a new market. Stated priority for offshore renewables. Potential for carbon capture on offshore assets. | In 2025, CNOOC moved from stating goals to initial execution with the CLPe JV, validating the LNG bunkering market as a tangible opportunity. Offshore wind remains an opportunity, not yet a reality. |

| Threats | Global pressure to decarbonize and competition from rapidly scaling renewable energy projects. | Greenland’s moratorium on oil exploration directly impacts expansion plans. Peer Chinese firms like Dongbaishan Holding Group are making large ($500 M) international solar investments. | Policy risks (Greenland) and competitive risks (peer investments in renewables) became more concrete in 2025, highlighting the external pressures on CNOOC‘s traditional business model. |

Scenario Modelling for CNOOC: Offshore Wind vs. LNG Bunkering Execution

The critical question for CNOOC‘s strategy heading into 2026 is whether it will escalate its energy transition from synergistic, adjacent moves to transformative, large-scale investments in a second core business like offshore wind. The success of the CLPe joint venture will serve as a crucial test case for its ability to execute in new, customer-facing distributed energy markets.

- If this happens: CNOOC announces a multi-billion dollar investment in a large-scale offshore wind project with a clear commissioning timeline.

- Watch this: The company’s 2026 capital expenditure budget. A significant allocation (e.g., 10-15% of total CAPEX) to “new energy” would signal a genuine strategic shift.

- These could be happening: CNOOC is building confidence from the operational and financial success of the LNG bunkering venture and is now willing to take on the larger development risk of offshore wind to build a long-term growth engine.

Renewables to Dominate 2050 Energy Scenarios

This chart visualizes one of the key potential futures that CNOOC must plan for. It directly relates to the ‘Offshore Wind’ aspect of the scenario modeling, illustrating a future state where renewable energy investments are critical for long-term survival.

(Source: RFF.org)

The questions your competitors are already asking

This report covers one angle of CNOOC’s strategy for leveraging its fossil fuel assets to enter new energy markets. The questions that matter most depend on your work.

- What is actually happening with CNOOC’s CLP Group JV for LNG bunkering since the August 2025 announcement?

- CNOOC’s activities in offshore renewables. Is the initiative progressing from a stated intent to concrete project investments?

- What is the outlook for LNG bunkering deployment in the Hong Kong shipping market by 2030?

- Which international shipping lines are adopting LNG bunkering services in Hong Kong?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.