Repsol US Solar Expansion, 43.8% Stonepeak Stake Sale, 1.5 GW RES Deal, and 60 GW Pipeline (2021 to 2026)

Repsol Renewable Project Execution, 6 GW Target and Stonepeak Partnership

Repsol accelerated its renewable energy strategy in 2025 by shifting from a model of solely self-funded projects to a capital recycling model, using strategic partnerships to finance a large-scale utility solar pipeline that feeds the distributed grid. Prior to 2025, Repsol primarily developed assets on its own balance sheet, a capital-intensive approach common for traditional energy firms. The new strategy uses joint ventures to de-risk development, secure growth capital, and accelerate market penetration, especially in the United States.

- In 2025, this strategic pivot was validated by the creation of a joint venture with infrastructure investor Stonepeak, which acquired a 43.8% stake in Repsol’s US solar and storage portfolio. This transaction provides Repsol with the capital to accelerate the development of a 60, 000 MW global project pipeline.

- This capital partnership model is a critical response to market conditions, as overall US renewable deal value fell by 41% in the first nine months of 2025, making access to external capital a significant competitive advantage.

- To ensure the operational viability of these new assets, Repsol signed a major agreement with RES to provide operations and maintenance for 1.5 GWp of its US solar portfolio, covering key projects like the 825 MWp Pinnington and 620 MWp Outpost solar farms.

- While executing its utility-scale solar strategy, Repsol is pursuing a parallel distributed energy initiative by leveraging its existing retail infrastructure to deliver low-carbon fuels, expanding its network of stations selling 100% renewable Nexa Diesel to 1, 500 by year-end 2025.

Repsol Details Renewable Capacity Targets for 2025/2030

The section heading explicitly mentions Repsol’s ‘6 GW Target’ for renewable projects. The chart, which details renewable capacity targets for 2025/2030, directly visualizes and supports this key performance indicator.

(Source: Oil and Gas Online)

€2.7 B Capital Rotation, Repsol’s Low-Carbon Investment Model

Repsol’s 2025 investment strategy validates a capital rotation model where proceeds from selling stakes in mature renewable assets are reinvested into its development pipeline, balancing shareholder returns with transition funding. This model allows the company to leverage its development expertise to bring projects to maturity and then monetize a portion of the asset to fund the next wave of growth without overburdening its balance sheet. The strategy is proving effective in generating returns while advancing decarbonization goals.

- The company’s successful rotation of 1.8 GW of commissioned capacity has generated €2.7 billion in proceeds with an average Equity IRR above 10%, demonstrating the financial viability of its renewable development and monetization cycle.

- In a sign of confidence in its cash flow, Repsol announced new share buyback programs in 2025 after posting a cumulative net income of €1.177 billion for the first nine months, showing it can reward shareholders while funding its low-carbon investments.

- These investments are channeled through Repsol’s Sustainable Financing Framework, which directs capital towards renewable generation, biofuels, and industrial decarbonization efforts like Carbon Capture.

- However, the company remains pragmatic in its capital allocation, adjusting its 2030 green hydrogen production targets downward by up to 63% in February 2025, citing market development delays and redirecting focus toward more mature technologies.

Late-Stage Renewable Projects Attract Investor Capital

The section discusses Repsol’s ‘Capital Rotation’ and ‘Low-Carbon Investment Model’. The chart explains the market dynamic that enables this model: investor appetite for the late-stage, de-risked projects that Repsol develops and then sells stakes in.

(Source: Deloitte)

Table: Repsol Key Financial and Investment Events (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Capital Rotation Program | 2025 | Repsol generated €2.7 B by selling down stakes in 1.8 GW of operational renewable assets, achieving an equity IRR >10% to fund future projects. | Investing.com |

| Share Buyback Program | July 2025 | Following a €603 million net income in Q 2, Repsol announced a new share buyback, balancing shareholder returns with capital-intensive transition projects. | Repsol |

| Green Hydrogen Target Revision | February 2025 | Repsol reduced its 2030 green hydrogen production targets by up to 63% due to market and regulatory hurdles, shifting focus to more mature technologies. | Fuel Cells Works |

Repsol Reaffirms 2025 Financial Guidance

This is a direct match. The section is a table of ‘Key Financial and Investment Events (2025)’, and the chart provides the company’s official financial guidance for that same year.

(Source: Investing.com)

Repsol 3 Key Alliances, Stonepeak and RES US Market Entry (2025)

In 2025, Repsol secured its US market expansion and operational stability through three critical partnerships, focusing on capital infusion, asset management, and supply chain security for its separate biofuels division. These alliances demonstrate a sophisticated approach to managing the complexities of the energy transition, ensuring that financial, operational, and supply chain risks are mitigated through collaboration with specialized partners.

- The partnership with Stonepeak is the most critical, establishing a joint venture to develop Repsol’s US renewables portfolio. By taking a 43.8% stake, Stonepeak provides the financial backing needed to advance a 60, 000 MW project pipeline, allowing Repsol to maintain development control while using third-party capital.

- The long-term service agreement with RES for 1.5 GWp of solar assets in Texas and New Mexico ensures the technical and financial performance of these large-scale projects, making them more attractive for future capital rotation and satisfying investor requirements for operational assurance.

- For its renewable fuels business in Europe, the strategic partnership with Bunge secures a stable supply of lower-carbon intensity feedstocks. This move de-risks the supply chain for Repsol’s advanced biofuel production facilities, which are critical to its transport decarbonization strategy.

US Solar Market Reshores Manufacturing in 2025

The section focuses on Repsol’s ‘US Market Entry’ with its alliance partners. The chart provides critical context for this strategic move, indicating a strengthening and self-reliant US solar market that would be attractive for new investment and entry.

(Source: Deloitte)

Table: Repsol Strategic Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Stonepeak | December 2025 | Stonepeak acquired a 43.8% stake in Repsol’s US solar and storage portfolio to co-develop a 60, 000 MW pipeline, providing significant growth capital. | Repsol |

| RES | September 2025 | Repsol contracted RES for operations and maintenance services for 1.5 GWp of its US solar portfolio, ensuring long-term asset performance and bankability. | RES Group |

| Bunge | April 2025 | Formed a strategic partnership to develop and supply lower-carbon intensity feedstocks for Repsol’s renewable fuels production in the European market. | Bunge |

North America Dominates Offshore Energy Market

The section is a table detailing strategic partnerships. The chart provides a compelling rationale for forming partnerships focused on North America, as it illustrates the region’s dominance and attractiveness in the energy market, justifying strategic entry.

(Source: Market Research Future)

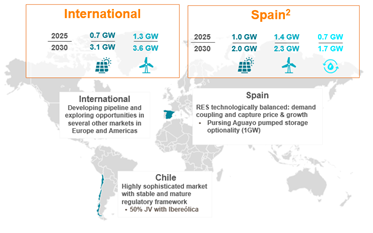

US vs Spain, Repsol Geographic Focus for Renewable Expansion

While maintaining a strong project base in its home market of Spain, Repsol’s strategic focus in 2025 pivoted decisively toward the United States as its primary growth market for large-scale renewables, using it as a platform for capital recycling and rapid scaling. This dual-geography strategy allows the company to leverage its established position in the mature European market while aggressively pursuing high-growth opportunities in the larger, more dynamic US energy landscape.

- Between 2021 and 2024, Spain was the center of Repsol’s renewable efforts, with flagship projects like the development of a renewable hydrogen plant in Cartagena and large hybridization projects combining gas and wind.

- The year 2025 marks a clear pivot, with the Stonepeak and RES partnerships anchoring its growth strategy firmly in the US. These deals provide the capital and operational framework for developing gigawatt-scale solar projects that are more difficult to site in land-constrained European markets.

- The US offers a single, large market with established financing mechanisms for renewable assets, making it an ideal location to execute a capital rotation strategy. This is pursued despite regulatory uncertainty, such as the “One Big Beautiful Bill Act, ” which highlights the risk-reward calculation favoring market scale.

- Meanwhile, Europe remains the focus for Repsol’s advanced biofuels strategy, as demonstrated by the NCLH renewable fuels agreement at the Port of Barcelona and the Bunge feedstock partnership, reflecting a tailored geographic approach for different low-carbon technologies.

Repsol’s Global Renewable Energy Asset Portfolio

The section heading discusses the ‘US vs Spain, Repsol Geographic Focus’. A chart showing the company’s ‘Global Renewable Energy Asset Portfolio’ is the perfect visual aid to illustrate this geographic distribution and strategic focus.

(Source: Repsol)

Technology Maturity, Repsol’s Focus on Solar and Biofuels

In 2025, Repsol prioritized investments in commercially mature technologies like utility-scale solar and advanced biofuels, while pragmatically scaling back ambitions in less developed sectors like green hydrogen to align with market realities and ensure financial returns. This disciplined, technology-readiness approach contrasts with strategies that prioritize bleeding-edge tech, instead focusing on scalable solutions that can deliver immediate decarbonization impact and positive cash flow. Other companies like Sustaera and Remora are tackling different parts of the decarbonization puzzle.

- Utility-scale solar PV is a fully mature and bankable technology for Repsol, validated by its multi-gigawatt development pipeline in the US and the ability to attract infrastructure partners like Stonepeak. Its focus is on execution and scale, not technology risk.

- Advanced biofuels have also reached commercial maturity, moving from pilot production in the 2021–2024 period to widespread commercial distribution in 2025. The rapid expansion to 1, 500 service stations and industrial-scale production of 100% renewable gasoline confirm this status.

- In contrast, green hydrogen remains in an earlier developmental stage. The 63% downward revision of Repsol’s 2030 production targets in 2025 reflects persistent market and regulatory hurdles, a different reality than faced by players in the SOFC market like Ceres Power and Bloom Energy.

- This strategic triage demonstrates a clear pattern: Repsol is willing to invest heavily in technologies once they are commercially viable and scalable, while taking a more cautious, milestone-based approach to emerging solutions like those from SCW Systems or Wacker.

Renewable Fuel Market to Exceed $2T by 2034

The section highlights Repsol’s focus on specific technologies, including ‘Biofuels’. This chart, showing the massive projected size of the ‘Renewable Fuel Market’ (which includes biofuels), provides the strategic context for why Repsol is prioritizing this area.

(Source: Precedence Research)

Repsol SWOT Analysis, Strengths in Partnerships, Risks in Regulation (2025)

Repsol’s 2025 strategy leverages its strong balance sheet and sophisticated partnership capabilities to exploit renewable energy opportunities but faces threats from regulatory uncertainty and a potential strategic gap in consumer-facing distributed power generation. The company’s ability to execute its capital-light, partnership-driven model in the US is a core strength, though this external reliance also introduces new dependencies. A broader look at the Carbon Capture DAC market and SOFC data center applications show how different companies tackle this transition.

Repsol Increases Shareholder Returns Through 2025

The section is a ‘SWOT Analysis’ where financial performance is a key ‘Strength’. A chart demonstrating increased shareholder returns provides direct evidence of the company’s financial strength and successful strategy.

(Source: Oil and Gas Online)

Table: SWOT Analysis for Repsol Distributed Energy Initiatives for 2025: Key Projects, Strategies and Market Impact

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong cash flow from legacy O&G business. In-house project development expertise in Spain. | Proven capital recycling model via Stonepeak JV. Strong balance sheet enables share buybacks alongside green investment. Rapid commercial rollout of renewable fuels. | The 2025 strategy validated that Repsol can successfully transition from a developer-owner to a developer-partner, creating a scalable, capital-light growth engine. |

| Weaknesses | Capital-intensive growth model reliant on own balance sheet. Limited presence in the large US renewables market. | Downward revision of green hydrogen targets signals challenges with nascent tech. Focus on utility-scale and fuels leaves a potential gap in true DERs (VPPs, community solar). | The pragmatic reduction in hydrogen targets confirmed that the company will not pursue immature technologies at the expense of financial discipline, a key signal to investors. |

| Opportunities | Growing demand for decarbonization. Nascent markets for renewable fuels and hydrogen. | Massive US market for utility-scale solar. Long-term offtake agreements for renewable marine fuels (NCLH). Ability to replicate capital recycling model. | The Stonepeak partnership and NCLH agreement validated the huge market opportunity in the US for renewables and in transport decarbonization, respectively. |

| Threats | Commodity price volatility. General policy uncertainty around the energy transition. | Specific regulatory headwinds (US OBBBA) creating project uncertainty. Supply chain bottlenecks for grid components. Falling deal values could reduce returns on future capital rotations. | The shift to a partnership model partially mitigates single-project financial risk but increases exposure to partner performance and broader financial market sentiment. |

Repsol Outlines Business Segments, Including Low-Carbon Generation

The section is a SWOT analysis for a specific area, ‘Distributed Energy Initiatives’. This chart helps contextualize the initiative by showing where it fits within Repsol’s broader business segments, such as ‘Low-Carbon Generation’.

(Source: Oil and Gas Online)

60 GW Pipeline, Repsol’s Execution and the Stonepeak Partnership

The success of Repsol’s energy transition now hinges on its ability to convert its 60, 000 MW project pipeline into operational, cash-generating assets through its partnership with Stonepeak. The strategy is set; the focus for the coming years will be purely on execution. The market will be watching for tangible progress on the ground, not just strategic announcements.

- If Repsol and Stonepeak successfully bring the first gigawatt-scale projects in the US portfolio online on schedule and within budget, it will serve as a powerful proof point for the joint venture.

- Watch for official commissioning announcements for the 825 MWp Pinnington and 620 MWp Outpost solar farms and, more importantly, any new Final Investment Decisions (FIDs) for the next wave of projects within the 60, 000 MW pipeline.

- Then this could be happening: The capital recycling model is validated at scale, attracting more infrastructure partners for future asset rotations and accelerating the development of the remaining pipeline. This would solidify Repsol’s transformation into a major international renewable power producer.

- Conversely, if significant delays or cost overruns emerge, watch for revised project timelines or public statements clarifying the status of the joint venture. This would signal execution risk and could temper market enthusiasm for Repsol’s transition strategy.

Repsol Accelerates Carbon Reduction Targets

The section discusses the execution of a massive ’60 GW Pipeline’ of projects. The chart provides the primary strategic motivation for this large-scale execution: the company’s ‘Accelerated Carbon Reduction Targets’, which the pipeline is designed to meet.

(Source: Oil and Gas Online)

The questions your competitors are already asking

This report covers one angle of Repsol’s capital partnership and execution strategy for renewable energy. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the US utility-scale solar market following the 41% drop in renewable deal value?

- What is actually happening with Repsol’s 60,000 MW global project pipeline since the Stonepeak partnership was announced?

- Repsol’s activities in asset management. Is the 1.5 GW operations and maintenance partnership with RES progressing to a portfolio-wide standard?

- What are the opportunities for infrastructure investors in the US solar market as energy majors shift to capital recycling models?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.