CNOOC BESS Strategy, 4 Oil Projects, 760 M BOE Target, and 2 LNG JVs (2021 to 2025)

760 M BOE Production Target, CNOOC’s Strategic Divergence from BESS

CNOOC Limited is strategically diverging from China’s national energy storage agenda by intensifying its focus on core hydrocarbon assets, positioning the company as a provider of energy security rather than a participant in the battery market. While its peers and national policy aggressively target the deployment of Battery Energy Storage Systems (BESS), CNOOC’s 2025 business plan prioritizes fossil fuel production, creating a significant gap between its strategy and the country’s broader energy transition goals.

- From 2021 to 2024, CNOOC’s activities were centered on its traditional oil and gas business, with a focus on large-scale international projects like the Queensland Curtis LNG (QCLNG) venture.

- In 2025, this focus hardened with the announcement of a business plan targeting net production of 760 million BOE. The plan explicitly names new oilfield developments, such as the Bozhong 26-6 and Kenli 10-2 Oilfields, as the primary drivers of growth.

- This strategy starkly contrasts with China’s national energy policy, which in 2025 included unveiling measures to bolster “new-type” energy storage, and planning for massive facilities like a 550 MW / 1, 100 MWh system.

- CNOOC’s only stated green initiative is to increase its green electricity consumption to over 1 billion k Wh in 2025, an operational efficiency move that involves no capital investment in new BESS assets and solidifies its negligible impact on the rapidly expanding storage market.

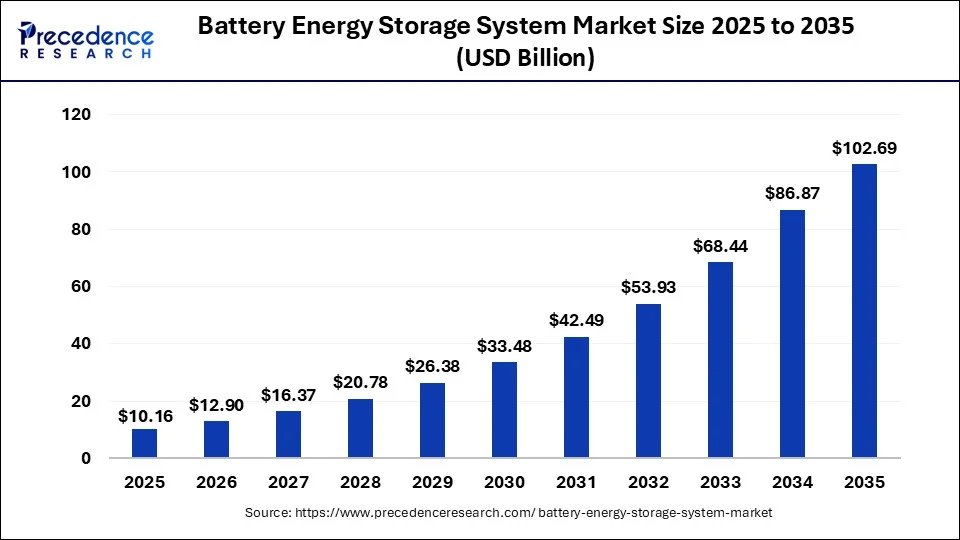

BESS Market to Surpass $102B by 2035

This chart quantifies the BESS market CNOOC is diverging from, giving a specific monetary value ($102B) to the opportunity cost of its hydrocarbon-focused strategy. The section’s ‘Strategic Divergence’ is made concrete by the chart’s market size projection.

(Source: Precedence Research)

CNOOC 4 New Oilfields, No BESS Investment Allocations (2025)

CNOOC’s 2025 capital expenditures are allocated almost entirely to upstream oil and gas exploration and production, with no disclosed investments directed toward the battery energy storage sector. The company’s financial commitments underscore a strategy to maximize hydrocarbon output, even as the domestic Chinese BESS market experiences explosive growth.

- The company’s 2025 investment plan centers on bringing four major projects online, which are collectively projected to add a peak production of 76, 500 barrels per day of crude oil.

- Key projects slated for commissioning in 2025 include the Bozhong 26-6 Oilfield Development Project (Phase I) and the Kenli 10-2 Oilfields Development Project, both requiring substantial upstream capital.

- This investment focus stands in sharp contrast to the broader Chinese market, where new energy storage installations reached 74.1 GW / 177.8 GWh in 2025 alone, a year-on-year growth of 62.5%. This market expansion, similar to the global LNG market growth seen by companies like Sempra, highlights the scale of the opportunity CNOOC is not pursuing.

BESS Market to Nearly Double by 2035

The chart’s headline ‘Nearly Double by 2035’ highlights the rapid growth rate of the BESS market, which directly contrasts with CNOOC’s decision to allocate no investment to this area, instead focusing on new oilfields.

(Source: Cervicorn Consulting)

Table: CNOOC 2025 Capital Allocation vs. BESS Market Growth

| Entity / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| CNOOC – New Oil & Gas Projects | 2025 | Four major projects, including Bozhong 26-6 and Kenli 10-2, are scheduled to come online to increase hydrocarbon production by 76, 500 b/d. | U.S. Energy Information Administration (EIA) |

| China BESS Market | 2025 | New installations reached 74.1 GW / 177.8 GWh, a year-on-year growth of 62.5% in GWh capacity, driven by national decarbonization policies. | China Energy Storage Alliance (CNESA) |

| Global BESS Market | 2025 | Global market projected to add 86 GW / 221 GWh of new capacity, representing 36% Yo Y growth in GWh. | Trend Force |

Battery Storage Market Shows Strong Growth Forecast

This chart provides the visual evidence for the ‘BESS Market Growth’ portion of the table’s title. It confirms the strong growth forecast, serving as the counterpoint to CNOOC’s capital allocation which the table presumably details.

(Source: Fortune Business Insights)

LNG Joint Ventures, CNOOC’s 2 Major Partnerships with Shell and Conoco Phillips

In 2025, CNOOC’s strategic partnerships remained firmly anchored in the global liquefied natural gas (LNG) and upstream exploration markets, reinforcing its hydrocarbon-centric strategy while showing no pivot towards new energy collaborations. All significant joint ventures and agreements announced or active during this period were aimed at securing and developing fossil fuel resources.

- CNOOC’s partnership portfolio is dominated by large-scale LNG projects, including its joint venture stake in the Queensland Curtis LNG (QCLNG) project with Shell.

- The company also holds a significant equity partnership in the Australia Pacific LNG (APLNG) project alongside Conoco Phillips, Origin Energy, and Sinopec, further cementing its role in the global gas market.

- In a move to expand its upstream footprint, CNOOC signed two new production sharing contracts in August 2025 with Indonesia’s regulator, SKK Migas, for new exploration blocks.

- Notably absent from CNOOC’s 2025 partnership activity are any collaborations related to battery technology, grid-scale storage, or renewable energy project development.

Table: CNOOC Hydrocarbon Partnership Portfolio (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Shell (QCLNG Project) | Active in 2025 | Joint venture partnership focused on the production and export of liquefied natural gas from Queensland, Australia. | Australian Government |

| Conoco Phillips, Origin, Sinopec (APLNG Project) | Active in 2025 | Equity partnership in a major Australian LNG project, solidifying CNOOC’s position in the Asia-Pacific gas supply chain. | Australian Government |

| SKK Migas (Indonesian Regulator) | Aug 2025 | Signed two production sharing contracts for new oil and gas exploration blocks in Indonesia, expanding upstream resource potential. | Offshore Technology |

| INEOS Energy | Apr 2025 | Finalized the divestiture of its U.S. Gulf of Mexico assets to INEOS, a move to streamline its international portfolio rather than a collaborative new energy venture. | Offshore Technology |

China vs. International, CNOOC’s Geographic Focus on Hydrocarbons

CNOOC’s geographic strategy in 2025 prioritized domestic offshore oil production in the Bohai Sea and international gas assets in Australia and Indonesia, while a separate, domestic energy storage market boomed across China without its participation. The company’s operational map is exclusively drawn around hydrocarbon basins, not renewable energy hubs.

- Between 2021 and 2024, CNOOC solidified its international presence through major LNG joint ventures in Australia, establishing a strong foothold in the Asia-Pacific gas market.

- In 2025, the company doubled down on domestic production, with key new projects like Bozhong 26-6, Kenli 10-2, and another new development all located in the Bohai Sea and southern China waters.

- This domestic oil focus was complemented by continued international expansion in its core business, evidenced by the new exploration contracts secured in Indonesia in August 2025.

- Concurrently, the geography of the BESS market, while also heavily concentrated in China, was driven by a completely different set of state-owned enterprises and private companies focused on grid stability and renewable integration, leaving CNOOC outside of this domestic growth story.

China’s Renewables and Storage Capacity to Surge

This chart directly supports the section’s theme by showing a massive surge in renewables and storage in CNOOC’s home country, China. This highlights the contrast between national energy trends and CNOOC’s stated ‘Geographic Focus on Hydrocarbons’.

(Source: Wood Mackenzie)

1 B k Wh Green Power Goal, CNOOC’s Tech Focus on O&G Efficiency

In 2025, CNOOC’s technological advancements were exclusively aimed at enhancing upstream oil and gas efficiency and localization, not developing or deploying commercially mature energy storage technologies. While the company has a goal to “gradually expand” its wind energy portfolio, its tangible technology milestones for the year were all in its core business.

- Throughout 2021-2024, CNOOC focused on developing proprietary technologies to support its deepwater exploration and production activities.

- This culminated in 2025 with the announcement of key proprietary equipment, including a localized deepwater underwater production system and real-time measurement tools for building “intelligent oil and gas fields.”

- The company’s primary “new energy” technology initiative for 2025 was its goal to consume over 1 billion k Wh of green electricity, a 30% year-on-year increase. This is an operational decarbonization tactic, not a strategic entry into energy storage technology deployment.

- This focus confirms that while BESS technology is commercially mature and scaling rapidly within China, CNOOC has opted not to engage with it, instead directing its R&D and engineering resources to its hydrocarbon operations.

Global Electricity Demand Projected to Surge

This chart provides the broader context for CNOOC’s ‘Green Power Goal.’ The projected surge in global electricity demand explains why even an oil and gas company would focus on power generation and efficiency, framing its 1B kWh goal as a response to a larger market trend.

(Source: BloombergNEF)

SWOT Analysis, CNOOC’s Strengths in Oil and Weakness in Energy Transition

CNOOC’s SWOT profile reveals a company that is successfully maximizing its established strengths in hydrocarbon production but is simultaneously creating significant long-term strategic weaknesses by remaining on the sidelines of the rapidly growing energy storage sector. Its 2025 actions reinforce its position as a powerful incumbent in the old energy system, but a laggard in the new one.

- The company’s core strength remains its deep offshore engineering expertise and robust cash flow from oil and gas operations.

- Its primary weakness is a near-total lack of diversification into high-growth clean energy sectors like BESS, exposing it to long-term transition risk.

- A major missed opportunity is the failure to leverage its offshore expertise to pioneer integrated offshore wind and battery storage projects.

- The most significant threat is future regulatory pressure from China’s 15 th Five-Year Plan (2026-2030), which is expected to mandate greater grid flexibility and could force CNOOC into a costly and rushed strategic pivot.

Global Energy Storage Growth Projected Through 2034

The chart’s projection of global energy storage growth visually represents the ‘Energy Transition’ mentioned as a weakness in the SWOT analysis. It quantifies the scale of the transition that CNOOC is currently not a major part of.

(Source: Reuters)

Table: SWOT Analysis for CNOOC Energy Storage and Battery Initiatives

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Deep offshore engineering expertise and strong hydrocarbon production base. | Production target of 760 million BOE and launch of new deepwater projects like Bozhong 26-6. | The 2025 business plan validated that CNOOC is doubling down on its core strengths, prioritizing hydrocarbon production over diversification. |

| Weaknesses | Limited portfolio diversification and minimal presence in renewable energy sectors. | Absence of any BESS or significant renewable energy projects in the 2025 plan. The green goal is consumption, not generation or storage. | The lack of investment in BESS during a year of explosive market growth confirmed this strategic weakness and highlighted the growing gap with national policy. |

| Opportunities | Potential to leverage offshore expertise for integrated wind and battery storage projects to align with China’s decarbonization goals. | China unveiled a three-year action plan (2025-2027) to boost new-type energy storage, creating a massive domestic market opportunity. | CNOOC’s inaction in 2025 indicates this remains a missed opportunity, as the company did not respond to the new national BESS policy with investments. |

| Threats | Long-term risk of stranded assets and competitive disadvantage as the global energy transition accelerates. | The stark contrast between CNOOC’s strategy and China’s aggressive BESS deployment highlights a growing misalignment with national long-term goals. | The threat of future regulatory action became more acute, with the upcoming 15 th Five-Year Plan looming as a potential catalyst for a forced strategic shift. |

CNOOC Post-2025 Pivot, Watch for 15 th Five-Year Plan Alignment

The most critical indicator for CNOOC’s future strategy is its response to China’s upcoming 15 th Five-Year Plan (2026-2030), which will signal whether the company will finally pivot from its hydrocarbon-only strategy to integrating energy storage. The policy framework will determine if CNOOC is compelled to join the energy transition or is allowed to continue its role as a dedicated fossil fuel provider.

- If CNOOC maintains its current trajectory, watch for its 2026 business plan to feature another round of high capital expenditures on oil and gas projects with no specific budget allocated to BESS.

- A strategic pivot would be signaled by the announcement of pilot projects that integrate battery storage with its offshore wind assets, moving beyond vague commitments to “expand the scale” of renewables.

- The primary trigger for such a shift will be the specific mandates and incentives within China’s new-type energy storage action plan for 2025-2027. CNOOC’s response, or lack thereof, to this national directive will define its role in the energy transition for the rest of the decade.

The questions your competitors are already asking

This report covers one angle of CNOOC’s role in China’s energy transition. The questions that matter most depend on your work.

- Which Chinese state-owned oil companies are gaining or losing ground in the BESS market?

- Is CNOOC a good investment for exposure to China’s energy security strategy versus its energy transition goals?

- What is the outlook for BESS deployment by Chinese oil and gas majors through 2025?

- CNOOC investments and funding. Are the Bozhong 26-6 and Kenli 10-2 oilfield projects on track to meet the 760 million BOE target?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.