Top 10 Critical Mineral Disruptions; China Export Controls & $64.3 B GDP Risk (2024-2025)

The escalating geopolitical conflict in the Middle East has triggered a global “metals squeeze, ” exposing profound vulnerabilities in critical mineral supply chains essential for defense, clean energy, and semiconductor manufacturing. The primary finding is that the conflict provided geopolitical cover for nations, particularly China, to weaponize their dominance in mineral processing through strategic export controls. This has been most evident in China’s stringent new restrictions on Rare Earth Elements (REEs) and Gallium, imposed in April and May 2025, respectively. In response, the U.S. has scrambled to secure its own supply chains, adding copper, uranium, and silver to its List of Critical Minerals in November 2025. The dominant theme for 2025 is the rapid escalation of resource nationalism, forcing Western industries and governments into a reactive posture to mitigate acute supply shocks and price volatility.

1. Rare Earth Elements (REEs)

Primary Disruption Vector: Weaponization of supply by China amid global instability.

Impact Analysis: China’s export controls directly threaten Western defense supply chains, which rely on REEs for missiles and advanced military technology. With 69% of global production and even higher processing shares, these restrictions have caused price surges and pushed defense contractors toward a “cliff edge” of depleted inventories.

Key 2025 Event: Most stringent export controls on rare earths and permanent magnets imposed on April 4, 2025.

Source: CSIS

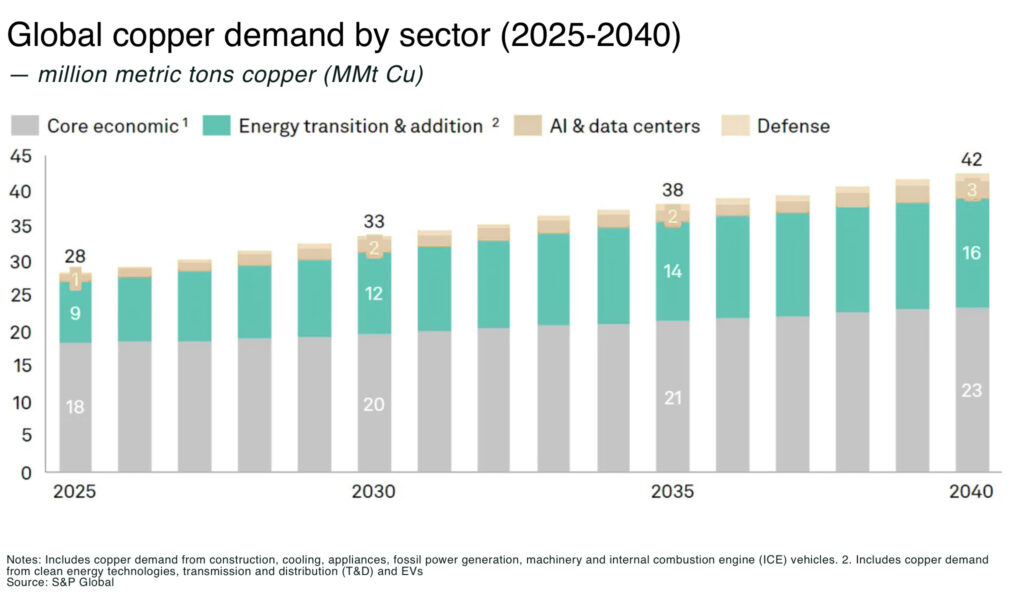

2. Copper

Primary Disruption Vector: Price volatility from geopolitical risk and logistics uncertainty.

Impact Analysis: As a key economic bellwether, copper prices reacted sharply to shipping risks in the Strait of Hormuz. The supply chain was already strained by rising demand and limited new mine development, prompting the U.S. to officially designate copper as a critical mineral to fast-track domestic projects.

Key 2025 Event: Added to the U.S. List of Critical Minerals in November 2025.

Source: Reuters

Global Copper Demand Projected to Surge by 2040

The chart’s focus on future global demand for Copper is a direct and highly relevant match for the section dedicated to Copper.

(Source: The Oregon Group)

3. Graphite

Primary Disruption Vector: Extreme concentration in Chinese processing.

Impact Analysis: The global EV industry faces paralysis risk, as China processes nearly 100% of the spherical graphite required for battery anodes. With demand growing 6-8% in 2024, the heightened geopolitical tensions of 2025 have amplified the threat of a complete export halt.

Key 2025 Event: Amplified risk of export controls due to global instability.

Source: Global Critical-Minerals Overview

4. Lithium

Primary Disruption Vector: Processing bottlenecks and price sensitivity.

Impact Analysis: While mining is diverse, China’s control over 65% of battery-grade lithium refining creates a critical chokepoint. The market instability from the Middle East conflict has caused price volatility and highlighted the fragility of this midstream dependency, especially after global demand surged 30% in 2024.

Key 2025 Event: Price volatility driven by market shocks and logistics concerns.

Source: [PDF] Sucden Financial

Lithium and Copper Face Widening Supply Deficits

The headline explicitly mentions a supply deficit for Lithium, which is the specific subject of Section 3.

(Source: Center on Global Energy Policy – Columbia University)

5. Cobalt

Primary Disruption Vector: High concentration in both mining and refining.

Impact Analysis: Cobalt faces a dual-risk profile with over 70% of mining in the unstable Democratic Republic of Congo (DRC) and 74% of refining in China. The global turmoil has increased investment risk in the DRC and strengthened China’s strategic leverage over the market.

Key 2025 Event: Increased investment risk profile for DRC mining projects.

Source: IEA

6. Gallium

Primary Disruption Vector: Near-total production monopoly by China.

Impact Analysis: Critical for advanced semiconductors, gallium supply has been severely choked after China expanded export restrictions. With an estimated 98% control of global primary production, this move has created an acute crisis for non-Chinese semiconductor manufacturers.

Key 2025 Event: Included in China’s expanded export restrictions in May 2025.

Source: CSIS

7. Uranium

Primary Disruption Vector: Renewed strategic importance for energy security.

Impact Analysis: The global energy shock has renewed focus on nuclear power, leading to uranium’s reinstatement on the USGS Final 2025 List of Critical Minerals. The policy shift aims to stimulate domestic production and secure supply away from Russian and Chinese influence.

Key 2025 Event: Reinstated to the U.S. List of Critical Minerals in November 2025.

Source: Reuters

8. Silver

Primary Disruption Vector: Pre-existing structural deficit exacerbated by safe-haven demand.

Impact Analysis: The silver market entered the conflict with a five-year supply deficit approaching 800 million ounces. The war drove a surge in safe-haven investment, tightening the market for industrial uses in solar panels and electronics and leading to its designation as a critical mineral by the U.S.

Key 2025 Event: Added to the U.S. List of Critical Minerals in November 2025.

Source: FXStreet

9. Nickel

Primary Disruption Vector: Resource nationalism amplified by market volatility.

Impact Analysis: Indonesia’s use of export bans on unprocessed ore to build domestic processing has been emboldened by market uncertainty. This creates supply risks for global battery and steel producers, who saw nickel demand grow by 6-8% in 2024.

Key 2025 Event: Amplified impact of Indonesian export bans due to market instability.

Source: [PDF] USITC

10. Gold

Primary Disruption Vector: Price surge from safe-haven demand impacting industrial use.

Impact Analysis: While primarily an investment asset, gold is essential for high-end electronics. The geopolitical surge in gold prices has squeezed industrial consumers, who face higher costs and procurement challenges, disrupting the supply chain through economic pressure.

Key 2025 Event: Price surge due to global conflict impacting industrial buyers.

Source: The Economic Times

Table: Top Mineral Supply Chain Disruptions (2024-2025)

| Mineral | Primary Disruption Vector | China’s Processing Share (%) | Key Disruption Event (2025) |

|---|---|---|---|

| Graphite | Processing Monopoly | ~100% | Heightened risk of export halt amid geopolitical tensions |

| Gallium | Production Monopoly | 98% | Inclusion in China’s expanded export restrictions (May 2025) |

| Rare Earths | Geopolitical Weaponization | ~85% | Stringent export controls imposed by China (Apr 2025) |

| Cobalt | Refining Concentration | 74% | Increased investment risk in DRC mining due to global instability |

| Lithium | Processing Concentration | 65% | Price volatility from market shocks and logistics concerns |

Critical Mineral Applications, From EV Batteries to Defense Systems

The diversity of applications for these disrupted minerals reveals how interconnected and vulnerable modern industries have become. The list is not merely a collection of industrial inputs; it is the foundational layer for multiple strategic sectors. Graphite, for instance, is not just a battery component but the single point of failure for nearly the entire global electric vehicle industry, given China’s 100% processing monopoly on the anode-grade material. Likewise, Gallium and Indium are indispensable for the Ga N and In P semiconductors that power 5 G infrastructure and advanced defense radar systems. The weaponization of Rare Earth Elements directly targets the production of precision-guided munitions, F-35 fighter jets, and naval destroyers. This broad impact, stretching from consumer electronics to national security hardware, signifies that a disruption in one mineral supply chain can cascade, creating systemic risk across a wide swath of the global economy.

U.S. vs. China, A Geographic Scramble for Mineral Supply Chains

The recent disruptions have starkly illuminated a geographic contest for control over mineral resources, pitting China’s established dominance against a reactive West. China’s strategy has been one of long-term investment in midstream processing, giving it chokepoint control over minerals like graphite (~100%), gallium (98%), cobalt (74%), and lithium (65%), even for materials it does not mine. In contrast, the U.S. and its allies have awakened to their dependency, evidenced by the flurry of policy actions in late 2025. The addition of copper, uranium, and silver to the U.S. Critical Minerals List is a clear policy signal aimed at stimulating domestic exploration and production. This geographic scramble is not just about mining rights but about rebuilding entire midstream and downstream ecosystems—refining, smelting, and magnet manufacturing—outside of China’s sphere of influence, a multi-decade, trillion-dollar challenge.

Geopolitical Conflict Disrupts Global Supply Chains

This headline is an excellent thematic match for the section on the ‘U.S. vs. China, A Geographic Scramble for Mineral Supply Chains,’ as it frames the scramble within a broader geopolitical conflict.

(Source: Emergen Research)

Western Mineral Processing, A Scramble to Close the Maturity Gap

The 2025 metals squeeze reveals less about the maturity of end-use technologies and more about the critical immaturity of Western mineral processing capabilities. While the U.S. and Europe lead in designing advanced semiconductors and electric vehicles, they have largely offshored the dirty, low-margin work of turning raw ore into high-purity metals and chemical compounds. The data shows this is where the primary vulnerability lies. China’s control is not in mining REEs (69%) but in its near-monopoly on the complex, multi-stage process of separating them and producing permanent magnets. The conflict has abruptly transformed mineral processing from an overlooked industrial sector into a national security imperative. The challenge now is whether Western nations can deploy the capital and political will to scale these complex industrial processes, which are often capital-intensive and environmentally challenging, before the next supply shock hits.

Sulphuric Acid Crunch Threatens Critical Mineral Supply

A ‘Sulphuric Acid Crunch’ directly impacts mineral processing. This aligns perfectly with the section about the West’s ‘Scramble to Close the Maturity Gap’ in mineral processing.

(Source: The Northern Miner)

98% Dependency, China’s Gallium Export Controls Signal Broader Risk

The single most critical expectation for the year ahead is that Western governments and corporations must prepare for further, more targeted export controls from China on processed minerals. The moves in 2025 were not the final act but the opening salvo.

- If China seeks to exert strategic leverage in geopolitical disputes, watch for official announcements from its Ministry of Commerce (MOFCOM) expanding the list of materials subject to export licensing, potentially to include other minor metals critical for aerospace and electronics.

- The expansion of export controls to include at least 16 key minerals by May 2025, with gallium as a primary target, should be seen as a successful test case for Beijing, demonstrating its ability to inflict precise economic pain with minimal self-harm.

- Watch for a divergence in policy responses: while the U.S. reactively added copper and uranium to its critical list in November 2025, a leading indicator of genuine progress will be proactive, large-scale federal funding for specific domestic processing plants, not just exploration.

- The stock performance of non-Chinese mining and processing firms will be a key barometer. Sustained valuation growth would indicate market confidence in diversification, while continued volatility would signal skepticism about the West’s ability to compete on cost and scale.

China Dominates Global Aluminum Production

Although the chart focuses on Aluminum, it serves as a perfect proxy to illustrate the theme of Section 13, which describes China’s control over a critical mineral (Gallium) and the associated risks.

(Source: Mining.com)

The questions your competitors are already asking

This report covers one angle of the geopolitical risk and strategic response within critical mineral supply chains. The questions that matter most depend on your work.

- Which defense and semiconductor firms are most exposed to China’s 2025 export controls on Gallium and Rare Earth Elements?

- What is the outlook for new mining and processing projects in the U.S. and allied nations following the addition of copper and uranium to the Critical Minerals List?

- Who are the key alternative suppliers for permanent magnets and processed Gallium that can serve the U.S. defense industry?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.