MP Materials Rare Earth Lawsuit, $1.6 B USA Rare Earth Funding, $2.8 B Serra Verde Deal, and 2 Do D Agreements (2021 to 2026)

The United States’ multi-billion-dollar industrial policy to construct a domestic rare earth supply chain has ignited a high-stakes legal war between its two government-backed champions, MP Materials and USA Rare Earth. A lawsuit filed by MP Materials on May 27, 2026, alleges its rival stole proprietary magnet manufacturing technology, a conflict that threatens to derail the nation’s strategic goal of breaking dependence on China. This internal clash, fueled by massive federal investments, exposes deep fractures in the U.S. strategy and risks ceding further ground in a critical sector where China controls nearly 90% of global processing.

US Rare Earth Supply Chain Risks, MP Materials Lawsuit & Project Delays

The U.S. government’s aggressive industrial policy, designed to fast-track a domestic rare earth supply chain, has inadvertently created a hyper-competitive environment that has escalated into open legal conflict, undermining the core national security objective.

- Between 2021 and 2024, the U.S. strategy focused on kickstarting domestic capabilities through foundational policies like the Inflation Reduction Act’s Section 45 X tax credit and Defense Production Act funding. The objective was to create a competitive field of players, including MP Materials as the sole large-scale miner and newcomers like USA Rare Earth and Ucore Rare Metals.

- The period from 2025 to 2026 saw a dramatic escalation as massive, targeted capital injections transformed the landscape into an urgent commercial race. The government awarded a landmark $1.6 billion funding package to USA Rare Earth in January 2026 and provided MP Materials with over $550 million in Do D support, including a crucial offtake agreement with a guaranteed price floor.

- This intense, government-fueled competition culminated in the May 2026 lawsuit, where MP Materials accused USA Rare Earth of technology theft. The dispute strikes at the heart of the U.S. “mine-to-magnet” strategy, as both companies are considered essential for onshoring the high-value processing and manufacturing stages.

- The conflict threatens to cause significant project delays, disrupt investor confidence, and undermine the very resilience the policy was meant to build. While the U.S. government intended to foster a robust ecosystem, it has instead pitted its two designated champions against each other, creating a strategic vulnerability that benefits China’s market position.

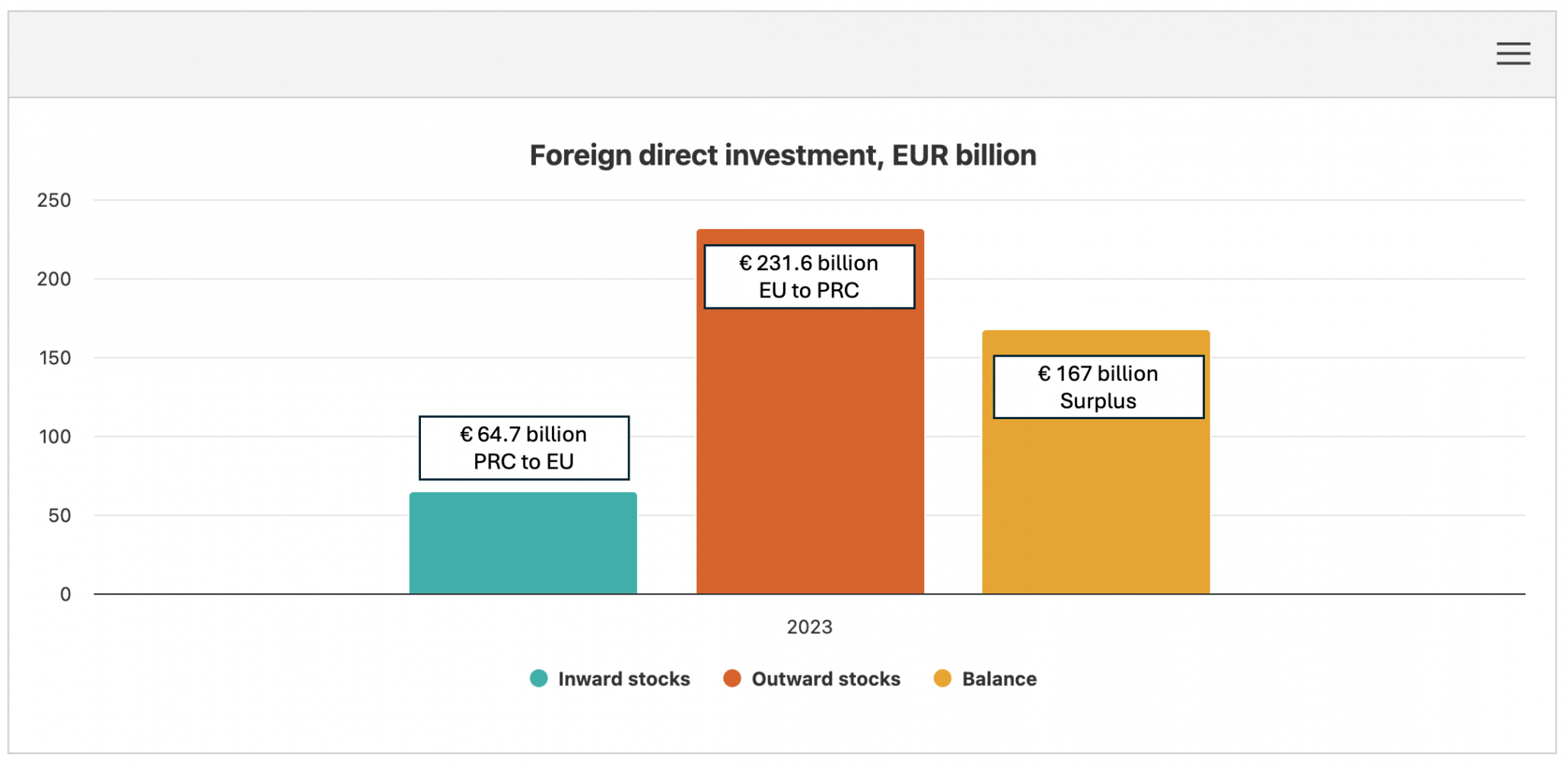

EU Investment in China Reaches €231.6 Billion

This chart illustrates the deep economic entanglement between Western allies (the EU) and China, which is a critical factor contributing to the complexity of US rare earth supply chain risks. Significant EU investment in China highlights potential fractures in a unified Western strategy and underscores the geopolitical challenges in decoupling from China-centric supply chains.

(Source: China Articles – Substack)

Over $3 B in US Funding, MP Materials and USA Rare Earth Capital Race

Massive injections of public and private capital since 2025 have dramatically accelerated timelines and raised the financial stakes, transforming the U.S. rare earths landscape into a high-pressure competition for market dominance.

- USA Rare Earth secured a combined $3.1 billion in January 2026, consisting of a $1.6 billion federal funding package from the Commerce Department and $1.5 billion in a concurrent private placement. This capital is designated to execute its aggressive “mine-to-magnet” buildout, including developing the Round Top project in Texas.

- MP Materials received $550 million from the Department of Defense in February 2026 to add heavy rare earth separation capabilities to its Mountain Pass facility. This funding is buttressed by a 10-year offtake agreement with a price floor of $110/kg for its magnet materials, a mechanism designed to de-risk its capital-intensive expansion into downstream processing.

- The U.S. government is also funding other parts of the supply chain, with the Export-Import Bank providing a letter of interest for a $120 million investment in Critical Metals Corp‘s Greenland project, and the Do D awarding $18.4 million to Ucore Rare Metals for its Louisiana processing complex.

Table: MP Materials and USA Rare Earth Strategic Investments

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| USA Rare Earth | Apr 2026 | Announced a $2.8 billion agreement to acquire Brazilian producer Serra Verde, one of the few scaled producers of all four magnetic rare earths outside of Asia, to secure near-term production capacity. | Financial Times |

| MP Materials | Feb 2026 | Secured $550 million in Do D funding ($400 million preferred stock, $150 million loan) to establish heavy rare earth separation capabilities at its Mountain Pass facility. | Investor News |

| USA Rare Earth | Jan 2026 | Received a $1.6 billion U.S. government funding package ($1.3 billion loan, $277 million grant) and raised $1.5 billion in private capital to accelerate its domestic “mine-to-magnet” value chain. | Wall Street Journal |

| Ucore Rare Metals | Apr 2023 | Announced a $75 million investment to establish a Strategic Metals Complex in Alexandria, Louisiana, for rare earth separation and purification, with operations planned to start in early 2025. | Opportunity Louisiana |

US vs China, MP Materials and USA Rare Earth Geographic Strategy

While the stated goal is to build a resilient U.S.-based supply chain, intense domestic competition and the hunt for near-term production are pushing American-backed firms to secure assets abroad, complicating the onshoring narrative.

- The primary geographic focus of U.S. industrial policy is North America. Key projects include MP Materials‘ operational Mountain Pass mine in California, USA Rare Earth‘s development-stage Round Top project in Texas, and new processing facilities being built by Lynas Rare Earths (Texas) and Ucore Rare Metals (Louisiana).

- This domestic build-out directly confronts China’s long-held geographic dominance. In 2025, China accounted for 69.2% of global rare earth mine output and nearly 90% of the world’s refining capacity, giving it immense control over global supply and pricing.

- In a significant strategic move to secure immediate production, USA Rare Earth announced a $2.8 billion deal in April 2026 to acquire Serra Verde in Brazil. This acquisition gives the U.S.-backed firm control of one of the only non-Asian, at-scale producers of all four critical magnetic rare earths, highlighting a strategy that pairs domestic development with international acquisition to compete with China.

West Outspends East in GDP and R&D

This chart provides the high-level economic context for the ‘US vs China’ geographic strategy by showing the substantial financial and research capabilities of the West. This data supports the section’s theme that while China dominates the rare earth market, the West possesses the overall economic power to fund and develop alternative, geographically distinct supply chains.

(Source: Haq’s Musings)

MP Materials Mine-to-Magnet Scale-Up and Technology Risks (2025-2026)

The U.S. has proven its ability to mine rare earths at scale, but the technological leap to downstream processing and magnet manufacturing remains the critical, unproven stage where competition is fiercest and strategic risk is highest.

- From 2021 to 2024, the primary technological achievement was MP Materials‘ successful operation of the Mountain Pass mine, re-establishing the U.S. as a significant source of raw rare earth concentrate, producing approximately 40, 000 metric tonnes annually.

- The period from 2025 to 2026 marks a pivot to the more complex and valuable stages of the supply chain: separation, refining, and magnet production. This is the technological bottleneck where China’s dominance is most profound and where proprietary intellectual property becomes a critical competitive advantage.

- The lawsuit filed by MP Materials against USA Rare Earth for alleged theft of magnet technology underscores that this advanced manufacturing stage is the new battleground. The dispute reveals the intense pressure on companies to acquire or develop this technology quickly to justify massive government and private investment.

- Failure to secure and scale this downstream technology domestically would leave U.S. miners like MP Materials in their historical position: forced to ship concentrate to China for processing, thereby failing the core “mine-to-magnet” objective of U.S. policy.

SWOT Analysis, MP Materials and US Rare Earth Competitive Dynamics

The U.S. rare earths sector has rapidly evolved from a state of dependency to a high-stakes, government-backed race, where the strengths of new funding have also created internal threats that could undermine the entire strategy.

Table: SWOT Analysis for the US Rare Earth Sector

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Sole large-scale domestic mine (Mountain Pass). Bipartisan political support for onshoring. | Massive federal funding ($1.6 B for USA Rare Earth, $550 M+ for MP Materials). Do D offtake agreements with price floors ($110/kg Nd Pr for MP). | The U.S. government validated its commitment with billions in direct investment and financial de-risking mechanisms, transforming financial viability for domestic projects. |

| Weaknesses | Almost total lack of domestic processing and magnet manufacturing capacity. Reliance on shipping concentrate to China. | Nascent processing capabilities still in development. Intense domestic rivalry leading to litigation over technology. | The weakness shifted from a lack of funding to a lack of scaled, proven domestic technology and internal cohesion, with infighting now a primary execution risk. |

| Opportunities | Growing demand from EVs and defense. Legislative support (IRA, DPA). | Explosive demand forecasts (magnet market to grow from $10.8 B to $56.7 B by 2040). Opportunity to capture market share via M&A (e.g., Serra Verde deal). | The market opportunity became significantly larger and more immediate, prompting aggressive M&A and accelerating the race to secure offtake agreements with auto and defense OEMs. |

| Threats | China’s ability to manipulate prices and control supply. High capital costs of building processing plants. | Internal legal battles (MP vs. USA Rare Earth) threatening project timelines. Risk of private capital flight due to domestic instability. Continued Chinese market dominance. | The primary threat is no longer just external (China), but also internal. The lawsuit creates delays and uncertainty, which directly benefits China’s strategic position. |

MP Materials 2026 Outlook, Lawsuit Impact on US Rare Earth Strategy

The legal confrontation between MP Materials and USA Rare Earth is now the single most critical variable for the U.S. rare earths strategy, with the outcome poised to either consolidate a national champion or create crippling delays.

- If MP Materials prevails in its lawsuit, it could solidify its position as the undisputed U.S. leader, potentially forcing a rationalization of government support and consolidating the domestic strategy around its integrated Mountain Pass operations. Watch for any moves by the government to mediate or choose a primary partner to avoid further fragmentation.

- If the case drags on or USA Rare Earth successfully defends itself, the U.S. will continue to have two heavily funded, competing champions. This could foster innovation but also risks redundant investment, slower overall progress, and continued instability that may deter private-sector partners in the automotive and defense industries.

- A key signal to monitor is the progress of USA Rare Earth’s acquisition of Serra Verde and its ability to integrate the asset. Success would give it a major production advantage over MP Materials, while a failure or delay could tilt the scales back in MP’s favor, regardless of the lawsuit’s outcome.

The questions your competitors are already asking

This report covers one angle of the U.S. domestic rare earth supply chain strategy and the commercial conflicts it has created. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the US rare earth supply chain race amid the legal battles?

- What is actually happening with the MP Materials lawsuit against USA Rare Earth and how does it impact their DoD-backed projects?

- Is USA Rare Earth’s $1.6 billion project at risk following the technology theft allegations from MP Materials?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.