China Lithium Supply Chain Control, $100 M Lanshen Deal, Zijin Mining Projects, and 4 Key Agreements (2021-2026)

Lithium Supply Chain Risks, China’s 50% Control and Vertical Integration

The assertion from Chinese industry leaders that global lithium demand will exceed conventional forecasts is a strategic action plan, not a passive prediction. This confidence is built on China’s unparalleled control over the lithium value chain, which allows it to both absorb and create price volatility that disciplines the market, squeeze out higher-cost Western competitors, and ultimately turn its aggressive demand projections into a self-fulfilling prophecy. This vertically integrated strategy moved from theory to practice between 2024 and 2026, demonstrating China’s capacity to influence global supply and demand dynamics.

- Between 2021 and 2024, China’s strategy focused on consolidating its midstream dominance, refining over 70% of the world’s lithium and creating a critical supply chain bottleneck for Western economies.

- The period from 2025 to today revealed the execution of this strategy, as a market surplus and price crash to near $13, 400/tonne stalled Western project development and led to the cancellation of $11 billion in announced U.S. battery projects in 2025.

- While Western projects paused, state-backed Chinese firms used the downturn to advance. For example, in April 2026, Zijin Mining Group announced its major lithium projects in Tibet had completed construction and commenced production, ready to capitalize on the price recovery to over $26, 000/tonne.

- By 2027, Chinese-owned entities are projected to control approximately 50% of total global lithium production, up from 35% in 2022, cementing their ability to manage market cycles to their advantage.

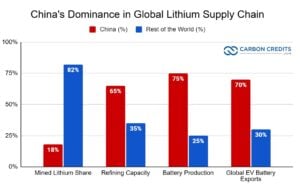

Chart Shows China’s Dominance Over Lithium Supply Chain

The chart’s headline directly aligns with the section’s focus on ‘China’s 50% Control and Vertical Integration’ of the lithium supply chain, providing a high-level visual representation of this dominance.

(Source: CarbonCredits.com)

China Lithium Offtake Deals, 4 Major Agreements from Pilbara to Argentina (2025-2026)

Since 2025, Chinese entities have intensified their global campaign to secure long-term lithium supply, moving beyond simple offtake agreements to deals that involve direct financing, prepayment, and joint project development. This strategic shift is designed to lock in raw material inputs for their dominant battery and EV manufacturing sectors at preferential terms, providing insulation from price volatility and geopolitical risks while starving competing supply chains of unallocated resources. These agreements demonstrate a clear intent to control the upstream, not just the midstream.

- Before 2025, offtake agreements were common but less financially integrated. The post-2025 era is defined by deals that blur the line between customer and financier, securing supply while also influencing the miner’s financial stability.

- In February 2026, Chinese processor China Canmax finalized an offtake deal with Australian miner Pilbara Minerals that included a substantial $100 million prepayment and a floor price, a mechanism to secure volume while protecting the miner from downside risk.

- In April 2026, Lanshen, a subsidiary of China’s Jinshi Resources Group, signed a US$100 million framework agreement with Argentina Lithium & Energy Corp. for the joint development of the Rincon West project, giving it a direct stake in South American brine production.

- This pattern is also visible in a January 2026 Memorandum of Understanding between private Chinese firm Jinjianqiao and Chariot Resources, which explicitly links project financing to long-term, exclusive priority offtake rights.

Table: China’s Strategic Lithium Partnerships and Investments (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Zijin Mining Group (3 Q & Lakkor Tso Salt Lakes) | Apr 2026 | Announced that major domestic lithium projects have completed construction and commenced production, signaling a significant increase in internal capacity release to feed China’s processing and battery manufacturing pipeline. | [PDF] Zijin Mining |

| Lanshen / Argentina Lithium & Energy Corp. | Apr 2026 | A US$100 million framework agreement for joint development of the Rincon West project, which holds 238, 000 tonnes of LCE. This provides a Chinese technology provider with direct access to South American brine resources. | Newsfile Corp |

| China Canmax / Pilbara Minerals | Feb 2026 | Finalized a significant offtake agreement that included a $1, 000/tonne floor price and a $100 million prepayment, demonstrating the use of financial leverage to secure long-term spodumene supply. | Discovery Alert |

| Jinjianqiao / Chariot Resources | Jan 2026 | A Memorandum of Understanding where the Chinese firm provides project financing in exchange for long-term, exclusive priority offtake of spodumene concentrate, linking capital directly to resource control. | TMX Money |

Africa & South America, China’s Lithium Mining Expansion Targets

China’s geographic strategy for lithium acquisition has matured from procuring raw materials from established producers like Australia to directly funding and developing new assets in emerging frontiers, particularly Africa and South America. This pivot diversifies its supply away from potential geopolitical rivals and secures resources at the source, aiming to build a global resource portfolio that mirrors its downstream manufacturing dominance. This strategic geographic expansion underpins the broader Chinese critical minerals policy.

- From 2021 to 2024, China’s primary upstream reliance was on Australian spodumene and Chilean brine, which were then shipped to China for processing. This model was efficient but created a dependency on foreign governments.

- Beginning in 2025, the strategy visibly shifted toward direct ownership and development. Wood Mackenzie forecasts that by 2030, Chinese-owned entities will control 39% of global lithium output, driven largely by aggressive investments in African mining projects.

- The recent agreements in South America, such as the Lanshen deal with Argentina Lithium, confirm that the “Lithium Triangle” (Argentina, Bolivia, Chile) is a key target for Chinese capital and technology.

- This expansion also includes domestic resources, with Zijin Mining bringing its significant salt lake brine projects in Tibet online in 2026, creating a multi-pronged approach to securing upstream supply.

Australia and Chile Lead in Global Lithium Mining

This chart establishes the global context for China’s mining expansion targets by identifying the current leaders in lithium mining, which includes South America (Chile), a key region mentioned in the section heading.

(Source: Center on Global Energy Policy – Columbia University)

80% Recovery Rates, China’s Strategic Interest in DLE Technology

While conventional hard-rock and brine-evaporation mining dominate current supply, Direct Lithium Extraction (DLE) has progressed from a speculative technology before 2025 to a commercially viable method poised to unlock vast, previously uneconomical brine resources. China’s strategic interest in DLE is high, as its successful deployment aligns perfectly with its objectives of increasing production speed, improving efficiency, and consolidating control over global brine assets in regions like South America and Tibet.

- In the 2021-2024 period, DLE was primarily in pilot stages, with questions surrounding its cost, water usage, and scalability. It was considered a long-term prospect rather than an immediate market factor.

- Since 2025, DLE has matured, with technologies now claiming recovery rates of 80-95%, compared to 40-60% for traditional evaporation ponds. Innovators also claim DLE can reduce processing times from over a year to mere hours.

- Chinese firms are well-positioned to lead DLE adoption. As operators of major brine assets, they can integrate this technology to significantly boost output from existing and new projects, such as the salt lakes in Tibet or joint ventures in Argentina.

- The U.S. Department of Energy’s focus on funding DLE research underscores its strategic importance, creating a competitive dynamic with China to master a technology that could redraw the global lithium supply map.

Future Lithium Demand May Outstrip Known Reserves

This chart provides the strategic rationale for China’s interest in DLE technology. The risk of demand outstripping reserves directly motivates the need for advanced extraction technologies that promise higher recovery rates.

(Source: Hannah Ritchie | Substack)

SWOT Analysis, China’s Lithium Strategy Strengths and Risks

China’s strategic approach to the lithium market is founded on the strength of its vertically integrated supply chain and robust state support, which allows it to set the pace of the global energy transition. However, this aggressive posture creates weaknesses related to geopolitical friction and exposes it to risks in unstable resource-rich nations, which in turn presents an opportunity for Western nations and companies to build alternative, more resilient supply chains.

- Strengths: China’s control over ~80% of lithium refining and over 75% of battery manufacturing provides unparalleled market insight and price influence.

- Weaknesses: Growing geopolitical pushback, evidenced by policies like the U.S. Inflation Reduction Act, and the operational risks of concentrating investments in politically unstable regions in Africa and South America.

- Opportunities: The ability to stimulate and capture new demand in sectors beyond passenger EVs, such as electric ships, commercial trucks, and large-scale energy storage systems.

- Threats: The successful onshoring of a complete Western supply chain, epitomized by cornerstone projects like Lithium Americas‘ Thacker Pass mine, could reduce reliance on Chinese processing.

Table: SWOT Analysis for China’s Global Lithium Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strength | Dominance in midstream refining created a critical processing bottleneck for the world. | Demonstrated ability to use price volatility to discipline the market, squeezing Western projects while advancing their own. Control extends across the entire value chain. | The strategic value of vertical integration was validated; China can endure price lows that are fatal to competitors. |

| Weakness | High reliance on raw lithium imports, particularly spodumene from Australia. | Increased geopolitical friction from Western governments (e.g., U.S. IRA) and growing exposure to operational risks in new African and South American mining investments. | The solution to import reliance (overseas acquisition) has created a new weakness: heightened geopolitical and sovereign risk. |

| Opportunity | Capitalize on growing EV demand by scaling up battery manufacturing for global automakers. | Drive next-generation demand in energy storage systems (ESS) and heavy transport electrification (ships, trucks). Commercialize DLE to dominate brine resources. | The market opportunity has expanded from being a component supplier for EVs to creating and owning new, large-scale ecosystems of lithium demand. |

| Threat | Potential for slower-than-expected global EV adoption, leading to overcapacity in battery manufacturing. | Successful formation of a complete, non-Chinese supply chain from mine to battery, enabled by Western industrial policy and the success of key projects. | The primary threat is no longer a lack of demand, but the emergence of a viable, resilient, and competitive alternative supply chain. |

China Lithium Price Volatility and Western Project Viability

The most critical strategic indicator for the global lithium market in the next 12 to 18 months is the trajectory of lithium prices. The key question is whether prices will stabilize within a range ($15, 000–$20, 000/tonne) that is high enough to support the economic viability of new Western projects, or if Chinese-influenced volatility will continue to deter investment and stall the development of a non-Chinese supply chain.

- If this happens: Lithium prices remain consistently above $20, 000/tonne throughout 2026. Watch this: The announcement of Final Investment Decisions (FIDs) for major Western projects that have secured permitting, such as Lithium Americas‘ Thacker Pass in the U.S.

- These could be happening: Sustained high prices could signal that global demand, including from China’s expanding non-EV sectors, is absorbing new supply faster than expected. This would validate that Western industrial policies like the IRA are sufficient to de-risk investment even with Chinese market influence.

- If this happens: Lithium prices fall back towards the lows seen in late 2025. Watch this: An increase in announcements of Chinese firms acquiring stakes in or fully purchasing distressed Western or junior mining assets.

- These could be happening: A price drop would confirm the effectiveness of China’s strategy to use oversupply and price warfare to eliminate rivals. It would indicate that Western projects remain uncompetitive without government price supports or offtake agreements that insulate them from market volatility.

China Lithium Carbonate Price Surges 191%

The chart’s headline is a direct and powerful illustration of the ‘Lithium Price Volatility’ discussed in the section, making it a perfect match.

(Source: CarbonCredits.com)

The questions your competitors are already asking

This report covers one angle of China’s strategic dominance in the global lithium supply chain. The questions that matter most depend on your work.

- Which Chinese vs. Western lithium producers are gaining or losing ground after the 2025 price crash?

- What is the outlook for Western lithium project development given China’s projected 50% control of global production by 2027?

- Zijin Mining’s investments in Tibet. Are its new lithium projects on track to capitalize on the price recovery to over $26,000/tonne?

- What are the opportunities for automakers to de-risk their battery supply chains amid China’s 70% control of lithium refining?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.