Grid Constraints & AI: Why Natural Gas is the Unavoidable Power Bridge in 2026

From Grid-Tied to On-Site: How AI Power Demand is Driving Natural Gas Adoption

The primary strategic shift in powering AI is the move away from relying on congested public grids toward developing dedicated, on-site natural gas generation. This change is driven by the urgent need to bypass multi-year grid interconnection delays and guarantee the extreme operational reliability that hyperscale data centers demand. The industry has pivoted from simply procuring energy to building and controlling its own power infrastructure.

- Between 2021 and 2024, the strategy was dominated by securing locations with existing grid capacity and procuring renewable energy through power purchase agreements. For example, Microsoft’s December 2023 agreement to use Renewable Natural Gas (RNG) for backup generators signaled an early focus on reliability, but it operated within a grid-centric model where gas was a secondary, not primary, power source.

- Starting in 2025, the strategy decisively shifted toward creating independent power islands. The collaboration announced in February 2025 between Chevron, GE Vernova, and Engine No. 1 to develop up to 4 GW of off-grid gas power co-located with data centers confirms this pivot from buying power to building power infrastructure.

- The market has responded with new service models explicitly designed to bridge the infrastructure gap. Solutions like Enchanted Rock’s “Bridge-to-Grid” service provide interim power, directly addressing the multi-year timeline mismatch between rapid data center construction and slow utility service availability.

- The scale of on-site projects has expanded dramatically, confirming gas as a primary power source. Exxon Mobil‘s plan for a dedicated 1.5 GW plant and the January 2026 partnership between Vantage Data Centers and Liberty Energy to develop 1 GW of power solutions show that on-site gas is now central to baseload AI power strategy.

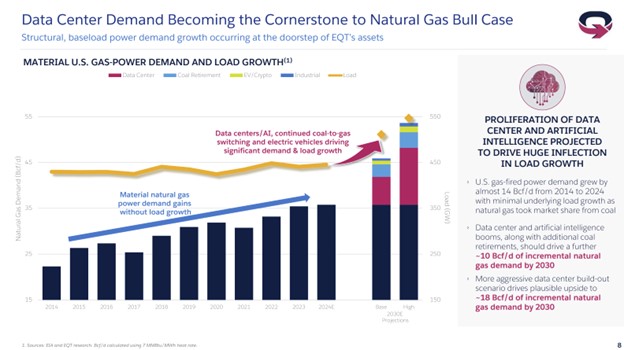

AI Boom Fuels Natural Gas Demand Surge

This chart directly illustrates the section’s main argument, forecasting a surge in natural gas demand driven specifically by the power needs of AI data centers through 2030.

(Source: The Motley Fool)

Billions Invested: Capital Flows into Gas-to-Power Infrastructure for AI Data Centers

A significant wave of capital from private equity, energy majors, and data center operators is now funding dedicated natural gas power infrastructure. This investment confirms the high economic value placed on speed-to-market and reliability, with market participants willing to pay a premium to bypass public grid constraints and bring AI capacity online faster.

Billions Invested in Dedicated Gas-to-Power Infrastructure

This map visualizes the capital flow described in the section, pinpointing a $5B investment to build dedicated gas-powered turbines, which aligns with the theme of infrastructure investment.

(Source: Rextag)

- Private equity firms recognize a generational investment opportunity. Blackstone estimates over $1 trillion will be invested in U.S. data centers in the next five years, with a substantial portion allocated to building the power generation required to support them.

- A vertically integrated investment approach is emerging. The November 2024 partnership between KKR and Energy Capital Partners aims to accelerate the buildout of both data centers and their supporting power generation, linking infrastructure capital directly to the AI power demand.

- Asset managers are directly funding the deployment of on-site generation technology. Brookfield Asset Management‘s commitment to invest up to $5 billion in Bloom Energy‘s natural gas fuel cells for its data centers validates on-site generation as a key strategy to bypass grid delays.

- Energy majors are self-funding large-scale projects to become direct power suppliers to the tech industry. Chevron has advanced a 2.5 GW off-grid gas power project, while Exxon Mobil has built a development pipeline of over 2.7 GW, signaling a strategic commitment to this new market.

Table: Key Investments in Gas-to-Power for Data Centers (2024-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Vantage Data Centers, Liberty Energy | Jan 2026 | Announced a strategic partnership to develop and operate 1 GW of power solutions. The goal is to provide reliable, scalable power for next-generation data centers, bypassing grid limitations. | Vantage & Liberty Partnership |

| Brookfield Asset Management, Bloom Energy | Oct 2025 | Brookfield is investing up to $5 billion to deploy Bloom Energy‘s natural gas fuel cells. This provides reliable on-site power for AI data centers, avoiding grid delays and ensuring operational uptime. | Market Wise |

| Exxon Mobil | Jan 2026 | Has built a development pipeline of over 2.7 GW for data center power projects, focusing on natural gas with carbon capture. This positions Exxon Mobil as a key power provider for the AI industry. | Forbes |

| Entergy | Nov 2024 | Proposed a new $3.2 billion natural gas plant in Louisiana specifically to power a large, unidentified $5 billion data center, highlighting how utilities are building new fossil fuel generation to meet AI demand. | Floodlight News |

Strategic Alliances Forge the Gas-Powered AI Bridge: A 2026 Analysis

The market is rapidly organizing through strategic alliances that connect hyperscale data center operators with energy producers, midstream companies, and technology providers. These collaborations are creating dedicated, private supply chains for reliable power, effectively circumventing the bottlenecks and timelines of public grid infrastructure and regulatory processes.

- A new consortium model combines fuel supply, technology, and capital. The partnership between Chevron (fuel), GE Vernova (turbines), and Engine No. 1 (investment) to develop up to 4 GW of off-grid gas power is a leading example of this integrated approach.

- Utility-technology partnerships are emerging to deliver rapid power solutions. The November 2024 agreement between utility AEP and Bloom Energy for up to 1 GW of fuel cells is designed to serve data centers and other large users that cannot wait for traditional grid upgrades.

- Midstream operators are becoming direct enablers of AI growth. Energy Transfer’s February 2025 agreement to supply natural gas directly to Cloud Burst’s planned 1.2 GW data center campus integrates pipeline infrastructure with digital infrastructure.

- Even climate-focused technology leaders are forming pragmatic fossil fuel alliances. Google’s plan with Broadwing Energy for a 400 MW gas plant featuring 90% carbon capture demonstrates a partnership model aimed at mitigating the environmental impact of its necessary reliance on natural gas.

Table: Key Partnerships for AI Data Center Gas Power (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Vantage Data Centers, Liberty Energy | Jan 2026 | A strategic partnership to develop and operate 1 GW of power solutions for next-generation data centers, focusing on reliability and scalability independent of grid constraints. | Vantage & Liberty Partnership |

| Chevron, GE Vernova, Engine No. 1 | Feb 2025 | A collaboration to develop up to 4 GW of off-grid natural gas power plants co-located with AI data centers. This alliance integrates fuel supply, turbine technology, and investment capital. | Energy Oil & Gas |

| Energy Transfer, Cloud Burst | Feb 2025 | An agreement for direct natural gas pipeline supply to power a new AI-focused data center campus expected to generate up to 1.2 GW of power. | Energy Transfer |

| Google, Broadwing Energy | Dec 2025 | A plan to build a 400 MW natural gas power plant designed to capture approximately 90% of its CO 2 emissions, balancing immediate power needs with long-term climate goals. | The Conversation |

U.S. Power Hubs Emerge: Mapping the Geographic Focus of AI-Driven Gas Demand

The geographic center for new data center development has pivoted from regions with cheap renewables to areas offering direct access to robust natural gas pipeline infrastructure. The U.S. Southeast and Texas are emerging as dominant hubs, as developers prioritize fuel availability and grid independence over proximity to intermittent energy sources.

US Power Hubs Emerge to Meet Demand

This chart validates the section’s geographic analysis by showing that projected power demand growth is concentrated in key states like Texas and Georgia, confirming the emergence of new power hubs.

(Source: Natural Gas Intelligence)

- Between 2021 and 2024, site selection often prioritized locations with access to low-cost wind and solar power. However, grid congestion and interconnection queues in these same regions quickly became a primary constraint on growth.

- Since 2025, a clear trend has emerged toward states with strong gas infrastructure. Utilities in the U.S. Southeast, including Dominion Energy in Virginia and Southern Company in Georgia, have announced dramatic upward revisions to their load forecasts, driven almost entirely by planned data center projects.

- Texas is a nexus for this activity due to its abundant natural gas reserves and independent grid (ERCOT). Chevron‘s 2.5 GW off-grid gas project in West Texas and multiple supply discussions held by Energy Transfer confirm the state’s central role in powering the AI boom.

- New projects demonstrate a strategy of co-locating data centers with fuel supply. The planned sites for Williams gas turbines, powering facilities like Open AI‘s “Stargate” in Abilene, TX, and x AI‘s “Colossus” in Memphis, TN, show a deliberate decision to build where the gas is readily available.

Commercial Scale Achieved: On-Site Gas Generation Technologies for Data Centers

The technologies for on-site natural gas power generation, primarily gas turbines and solid oxide fuel cells, are commercially mature and can be deployed rapidly. This proven technological readiness offers a vital advantage over the long lead times associated with grid expansion and the development timelines of emerging clean energy sources like small modular reactors.

- During the 2021-2024 period, on-site gas was largely considered a backup power solution, with diesel generators remaining the industry standard. The strategic use of natural gas for primary, baseload power was not yet a widespread practice.

- From 2025 onward, speed of deployment has become the key value proposition. Gas turbine suppliers like USP&E Global can deliver and commission entire power plants in 90-180 days, a timeline that is orders of magnitude faster than building new transmission lines.

- Solid oxide fuel cells (SOFCs) from providers like Bloom Energy have been validated as a cleaner, more efficient gas-powered technology now being deployed at gigawatt scale. The $5 billion investment by Brookfield to deploy this technology confirms it as a commercially viable, large-scale solution.

- Current deployments are being future-proofed for a post-gas transition. The specification of “hydrogen-ready” turbines in new projects indicates that while natural gas is the fuel for today, the physical infrastructure is being designed to accommodate cleaner fuels in the future.

SWOT Analysis: Natural Gas as a Bridge Fuel for AI Power Demand

Natural gas offers unmatched strengths in reliability and speed-to-market for powering the AI boom, but it faces significant long-term threats from decarbonization mandates and the potential for stranded assets. The core tension is between meeting the immediate, non-negotiable power needs of AI and navigating the transition to a zero-carbon energy system.

- The primary strength is the ability to meet immediate, gigawatt-scale demand, a capability validated by multi-gigawatt project announcements from energy majors and specialized partnerships.

- A fundamental weakness is the carbon footprint, which creates a strategic paradox for technology companies that have made public commitments to 100% renewable energy goals.

- The opportunity is the creation of a massive new market for “reliability-as-a-service, ” which transforms natural gas from a simple commodity into a high-value enabler of the multi-trillion-dollar AI economy.

- The main threat is the combination of regulatory risk against new fossil fuel infrastructure and the accelerated maturation of alternative firm power technologies, such as advanced nuclear or geothermal, which could render new gas assets obsolete in the long run.

Table: SWOT Analysis for Natural Gas as an AI Power Bridge

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Proven reliability for backup power, as demonstrated by Microsoft’s use of RNG for backup generators. | Unmatched speed-to-market for primary baseload power, with providers like USP&E Global delivering turbines in 90-180 days. | The role of gas shifted from a secondary backup source to a primary enabler of speed and reliability, commanding a higher economic value. |

| Weaknesses | Emissions profile conflicted with corporate ESG goals, but was manageable at a smaller scale. | The massive scale of new build-outs (e.g., Exxon Mobil’s 1.5 GW plant) makes the ESG conflict a core strategic tension. | The scale of reliance on gas grew from a minor issue to a fundamental challenge to corporate climate pledges, requiring mitigation strategies like CCUS. |

| Opportunities | Niche market for on-site generation to supplement grid power or provide enhanced reliability. | Multi-billion dollar partnerships (e.g., Chevron/GE for 4 GW) to build entirely off-grid power islands for AI. | The market opportunity grew exponentially from supplemental power to foundational infrastructure for the entire AI sector. |

| Threats | Competition from expanding grid-scale solar and battery storage projects was the primary alternative. | Long-term stranded asset risk from emerging zero-carbon firm power (SMRs, geothermal) and increasing regulatory scrutiny on fossil fuels. | The long-term technological and regulatory threat became more defined, creating a finite window for the natural gas “bridge.” |

Forward Outlook: Will the Gas Bridge Lead to a Clean Energy Destination?

The critical dependency on natural gas for AI power will persist until at least 2030. The key signal to watch is whether current investments in “hydrogen-ready” turbines and carbon capture projects translate into concrete, large-scale offtake agreements for clean fuels and sequestered CO 2, which will determine if the gas bridge leads to a decarbonized future or a dead end.

Gas and Renewables to Power Future Growth

This chart supports the section’s ‘Forward Outlook’ by showing both natural gas and renewables expanding to meet future power demand, visualizing the ‘gas bridge’ concept.

(Source: x.com)

- If this happens: Energy partners and hyperscalers fail to advance beyond pilot-stage carbon capture (CCUS) and hydrogen blending. Watch this: The operational CO 2 capture rates at new plants like Google’s 400 MW facility and the absence of firm, long-term hydrogen supply contracts for “hydrogen-ready” turbines. This could be happening: The gas bridge becomes a permanent dependency, locking in decades of fossil fuel infrastructure and creating significant stranded asset risk post-2035.

- If this happens: Investment in grid modernization and long-duration energy storage accelerates due to new policy incentives or technological breakthroughs. Watch this: Utility capital expenditure plans shifting from gas peaker plants to large-scale battery projects and federal subsidies for grid-enhancing technologies. This could be happening: The window of opportunity for natural gas as a bridge fuel could shorten, increasing pressure on new gas projects to deliver faster returns on investment.

- If this happens: Small modular reactors (SMRs) clear key federal regulatory hurdles and secure first-of-a-kind financing directly from technology companies. Watch this: Firm purchase orders for SMRs announced by hyperscalers like Microsoft or Amazon to power future data center campuses. This could be happening: Natural gas would be relegated back to a peaking or backup role as a new, zero-carbon baseload power source becomes commercially viable on a post-2030 timeline.

Frequently Asked Questions

Why are tech companies turning to natural gas instead of renewables like solar and wind?

The primary reason is speed and reliability. Tech companies are building dedicated, on-site natural gas generation to bypass multi-year delays in connecting to congested public grids. Natural gas provides the immediate, reliable, 24/7 baseload power that massive AI data centers require, which intermittent renewables and a slow-to-upgrade grid cannot currently guarantee.

Isn’t natural gas just for backup power at data centers?

While it was traditionally used for backup, the strategic shift described is toward using natural gas as the primary, baseload power source. Companies are developing ‘power islands’ independent of the grid. Multi-gigawatt projects, like the 4 GW collaboration between Chevron and GE Vernova, are being built specifically as the main power supply for data centers, not just for emergency backup.

How does this massive investment in natural gas affect the tech industry’s climate goals?

It creates a major strategic conflict with their public commitments to 100% renewable energy. The article highlights this as a core tension. To mitigate the environmental impact, some companies are pursuing solutions like carbon capture and storage (CCUS), as seen in Google’s plan for a plant with 90% capture, and ordering ‘hydrogen-ready’ turbines to allow for a future transition to cleaner fuels.

Who is funding this shift to gas-powered data centers?

A significant wave of capital is coming from private equity firms like Blackstone and KKR, energy majors like Chevron and Exxon Mobil, and asset managers like Brookfield. These entities are forming strategic partnerships with data center operators and technology providers to directly fund and build the required power infrastructure, viewing it as a major investment opportunity.

Is this reliance on natural gas a permanent solution?

No, the article frames it as a ‘bridge’ solution expected to be dominant until at least 2030. The long-term threat is that these new gas plants could become ‘stranded assets.’ The future depends on the commercial viability and regulatory approval of alternative firm power sources like small modular reactors (SMRs), advanced geothermal, or significant breakthroughs in long-duration energy storage.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.