Top 10 Data Center Liquid Cooling Vendors: Supermicro’s 100 K GPU x AI Win & 10 MW CDUs Emerge (2024-2025)

The AI-driven surge in data center power density has made high-capacity liquid cooling a mandatory infrastructure component, shifting the market decisively from niche application to mainstream necessity. The primary finding from 2024-2025 commercial activity is a clear pivot towards multi-megawatt, scalable solutions capable of supporting entire AI clusters. This is evidenced by vendors like Liquid Stack and Nautilus Data Technologies launching groundbreaking 10 MW Coolant Distribution Units (CDUs), while system integrators like Supermicro are winning massive contracts, such as the 100, 000 GPU “Colossus” cluster for x AI, by offering complete, pre-engineered liquid-cooled racks. The dominant theme for 2025 is no longer *if* liquid cooling is needed, but *how quickly* it can be deployed at unprecedented scale to handle rack power densities now exceeding 80 k W.

1. Liquid Stack: 10 MW Modular CDU Launch

Company: Liquid Stack

Installation Capacity: Up to 10 MW cooling capacity

Application: Modular Coolant Distribution Unit (CDU) for large-scale AI data centers and high-performance computing (HPC).

Source: Liquid Stack touts modular, scalable data center coolant distribution …

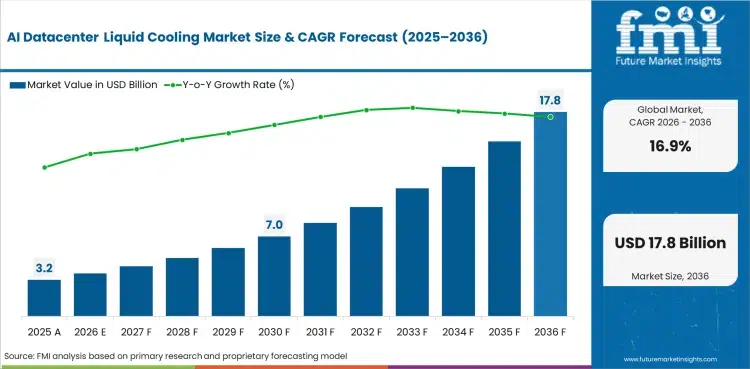

AI Liquid Cooling Market to Hit $17.8B

This section introduces a new 10 MW AI cooling product from Liquid Stack. The chart quantifies the significant market opportunity in AI liquid cooling that this high-capacity product is designed to capture.

(Source: Future Market Insights)

2. Nautilus Data Technologies: 10 MW Containerized CDU

Company: Nautilus Data Technologies

Installation Capacity: Up to 10 MW heat rejection

Application: The Eco Core XCD, a containerized CDU module for scalable, water-efficient cooling in modern data centers.

Source: Nautilus | Water-Efficient, Scalable Data Center Liquid Cooling

AI Liquid Cooling Market to Reach $17.8B

This section details Nautilus’s competing 10 MW containerized CDU. The chart, identical in headline to the one in the previous section, reinforces the large market size and justifies the entry of multiple large-scale competitors targeting the same lucrative AI cooling space.

(Source: Future Market Insights)

3. Schneider Electric: 2.5 MW High-Density CDU

Company: Schneider Electric

Installation Capacity: 2.5 MW

Application: The Motivair MCDU‑70 CDU, designed for high-density AI environments and part of a comprehensive liquid cooling portfolio.

Source: Liquid cooling solutions for AI and high-density data centers

Data Center Liquid Cooling Market to Expand

This section describes a 2.5 MW CDU from Schneider Electric, a major industry player. The chart, showing the general expansion of the data center liquid cooling market, provides the context of overall market growth that necessitates such products.

(Source: MarketsandMarkets)

4. Vertiv: Top-Ranked Cooling Provider for AI Expansion

Company: Vertiv

Installation Capacity: Positioned to support a projected 32.9 GW of data center expansion by 2027.

Application: Comprehensive cooling solutions for hyperscale and enterprise clients, recognized as a market leader for the AI-driven buildout.

Source: Top 7 Most Innovative Data Center Cooling Companies

Data Center Liquid Cooling Ecosystem Mapped

This section names Vertiv as a top-ranked provider for AI expansion. An ecosystem map visually contextualizes Vertiv’s leading position within the competitive landscape, illustrating the various partners, competitors, and customers it interacts with.

(Source: MarketsandMarkets)

5. Johnson Controls: Strategic D 2 C Technology Investment

Company: Johnson Controls

Installation Capacity: N/A (Strategic Investment)

Application: Investment in Accelsius, a specialist in two-phase direct-to-chip (D 2 C) cooling technology, to capture the high-density market.

Source: Johnson Controls Announces Investment in Data Centre Liquid …

Direct-to-Chip to Lead AI Liquid Cooling Market

This section focuses on Johnson Controls’ strategic investment in Direct-to-Chip (D2C) technology. The chart strongly validates this strategy by forecasting that Direct-to-Chip will become the leading technology segment within the AI liquid cooling market.

(Source: Future Market Insights)

6. DCX: 2.6 MW European CDU Portfolio

Company: DCX

Installation Capacity: Up to 2.6 MW

Application: A comprehensive portfolio of performance-matched CDUs, enabling optimized redundancy and investment for data center operators.

Source: DCX Liquid Cooling Systems – cooling solutions for datacenters

Liquid Cooling Market to Reach $27.65B by 2033

This section discusses DCX’s 2.6 MW European CDU portfolio. The chart provides the large global market size for liquid cooling, showing the scale of the worldwide opportunity that regional players like DCX are addressing with their focused offerings.

(Source: MarketsandMarkets)

7. Danfoss: Key NVIDIA-Recommended CDU Supplier

Company: Danfoss

Installation Capacity: Reportedly supplying the majority of CDUs for AI data centers.

Application: A critical component supplier in the AI supply chain, with its vendor status recommended by NVIDIA for facilities deploying its latest GPUs.

Source: Liquid Cooling – by Patrick Zhou – Deep Dive

Data Center Electricity Use to Exceed 1,000 TWh

This section highlights Danfoss as a key supplier recommended by NVIDIA. The chart, showing the massive surge in data center electricity use, explains the fundamental problem (immense power and heat) created by high-performance NVIDIA GPUs that Danfoss’s cooling solutions are designed to solve.

(Source: Bessemer Venture Partners)

8. Cool IT Systems: Direct Liquid Cooling Specialist

Company: Cool IT Systems

Installation Capacity: Scalable systems for cluster deployments.

Application: A top-tier vendor providing direct liquid cooling (DLC) solutions highly optimized for dense HPC and AI deployments.

Source: Top 8 Liquid Cooling Companies Powering the Modern Data Center

Data Center Cooling Market Shifts to New Technologies

This section profiles Cool IT Systems, a specialist in Direct Liquid Cooling. The chart complements this by illustrating the broader market trend of shifting away from traditional air cooling and towards the new technologies that specialists like Cool IT champion.

(Source: MarketsandMarkets)

9. Supermicro: 100, 000 GPU AI Cluster Deployment

Company: Supermicro

Installation Capacity: In-row CDUs up to 1.8 MW; built the 100, 000 GPU “Colossus” cluster.

Application: Fully integrated, ground-up liquid-cooled server and rack solutions for massive-scale AI infrastructure projects like x AI‘s cluster.

Source: [PDF] Inside the 100 K GPU x AI Colossus Cluster that Supermicro Helped …

AI Power Use in Data Centers to Surge

This section describes a massive 100,000 GPU AI cluster deployment by Supermicro. The chart, which shows the surge in AI power consumption, directly illustrates the primary challenge—managing immense power draw and resultant heat—that a deployment of this unprecedented magnitude creates.

(Source: SemiAnalysis)

10. Flex: 1.8 MW Modular Rack-Level CDU

Company: Flex

Installation Capacity: Up to 1.8 MW

Application: A modular, rack-level CDU launched to meet the evolving demands of AI, HPC, and hyperscale workloads with flexible deployment.

Source: Flex Expands Data Center Cooling Portfolio with Launch of Modular …

Table: Top 10 Liquid Cooling Vendors and Recent Activity (2024-2025)

| Company | Capacity/Key Activity | Application | Source |

|---|---|---|---|

| Liquid Stack | Up to 10 MW | Modular CDU | facilitiesdive.com |

| Nautilus Data Technologies | Up to 10 MW | Containerized CDU | nautilusdt.com |

| Schneider Electric | 2.5 MW CDU | High-density cooling | se.com |

| Vertiv | Supporting 32.9 GW expansion | Comprehensive cooling | abiresearch.com |

| Johnson Controls | Investment in Accelsius | Direct-to-Chip (D 2 C) | johnsoncontrols.com |

| DCX | Up to 2.6 MW CDU | Specialized CDUs | dcx.eu |

| Danfoss | Major supplier to AI data centers | NVIDIA-recommended CDU | deepfundamental.substack.com |

| Cool IT Systems | Scalable DLC systems | HPC & AI clusters | lianliwork.com |

| Supermicro | Built 100, 000 GPU cluster | Integrated rack solutions | supermicro.com |

| Flex | 1.8 MW CDU | Modular rack-level cooling | investors.flex.com |

10 MW CDUs, Liquid Stack and Nautilus Redefine AI Cooling Scale

Industry adoption has matured rapidly, with a clear diversification in cooling strategies to meet different deployment needs. The market now offers a complete spectrum of solutions, indicating widespread commercialization. At the highest end, facility-level cooling is being redefined by modular, multi-megawatt systems like the 10 MW CDUs from Liquid Stack and Nautilus, designed for massive greenfield AI factory builds. In parallel, integrated rack-level solutions from vendors like Supermicro and Flex are winning contracts by simplifying deployment for both new and existing data centers. Finally, targeted technology plays, such as Johnson Controls’ strategic investment in Accelsius’ direct-to-chip technology, demonstrate that even specialized component-level innovations have a clear path to market to solve hyper-specific thermal challenges. This diversity implies that customers are no longer forced into a one-size-fits-all approach and can select the most efficient technology for their specific workload and facility.

AI Cooling Market Sees Strong Global Growth

This summary section discusses how new 10 MW CDUs are redefining AI cooling scale. A high-level chart showing strong global growth in the overall AI cooling market perfectly establishes the macro trend that these large-scale solutions are a response to.

(Source: Future Market Insights)

US and Europe, Supermicro and Danfoss Lead Regional Deployments

The current wave of high-capacity liquid cooling deployments is heavily concentrated in North America and Europe, aligning with the locations of major AI development and hyperscale data center construction. The United States is host to landmark projects like Supermicro’s buildout of the 100, 000 GPU “Colossus” cluster for x AI, demonstrating the capability to deliver liquid cooling at an unprecedented scale. Europe is a critical hub for component manufacturing and innovation, with Denmark-based Danfoss emerging as a pivotal supplier of CDUs. Its status as a recommended vendor by NVIDIA gives it a powerful competitive advantage in securing contracts wherever advanced GPUs are deployed, solidifying a strong European presence in the global AI supply chain.

Data Center Liquid Cooling Market Shows Strong Growth

This section highlights the regional leadership of Supermicro and Danfoss. The chart’s message of ‘strong growth’ in the liquid cooling market reinforces the idea that these companies are leading in a dynamic and rapidly expanding market, not a stagnant one.

(Source: Global Market Insights)

Integrated Racks, Supermicro’s 100 K GPU Cluster Shows Maturity

The technology has advanced far beyond the experimental stage, with commercial maturity now defined by the ability to deliver turnkey solutions at scale. The clearest signal of this is the success of integrated rack systems. Supermicro’s delivery of a fully liquid-cooled, 100, 000 GPU cluster for x AI proves that the market can support complex, large-scale deployments while significantly reducing the integration burden for the end-user. This “one-stop-shop” approach is becoming a major competitive differentiator. Concurrently, component technology is keeping pace, with the launch of 10 MW CDUs by Liquid Stack and Nautilus in 2025. This leap in capacity shows the industry is proactively engineering solutions for the next generation of gigawatt-scale AI campuses, shifting the focus from server-level to facility-level thermal management.

Data Center Infrastructure Market to Exceed $1T by 2030

This section uses Supermicro’s 100K GPU cluster as a sign of market maturity. The chart, showing the total data center infrastructure market growing to over $1 trillion, provides the macro-level context for this scale, linking a specific example of maturity to the massive size of the overall industry.

(Source: IoT Analytics)

Vertiv & Schneider Electric Face 10 MW Competition (2025-2026)

The most critical strategic action for established infrastructure giants in the year ahead is to either accelerate their high-capacity CDU roadmap or acquire specialists to compete with the new 10 MW performance benchmark. If hyperscalers begin to standardize facility designs around these next-generation modular CDUs, incumbents risk being relegated to lower-tier enterprise deals. Watch for major M&A activity in the cooling sector and monitor the adoption rate of Liquid Stack’s and Nautilus’s systems in new campus announcements throughout late 2025 and 2026. This could signal a bifurcation of the market, with technology specialists dominating the high-performance tier.

- Gaining Traction: Fully integrated, pre-validated liquid-cooled rack systems are proving to be a winning strategy. The success of Supermicro’s massive contract with x AI, announced in late 2024, validates this model as the fastest path to large-scale deployment.

- Gaining Traction: Modular, facility-level cooling systems are setting new performance standards. The launch of 10 MW capacity CDUs by Liquid Stack in June 2025 and Nautilus in September 2025 shows the market is scaling to meet gigawatt-level demand.

- Gaining Traction: Strategic partnerships and investments are validating specialized technologies. Johnson Controls’ investment in direct-to-chip specialist Accelsius in October 2025 signals that legacy HVAC leaders see component innovation as critical for future market share.

- Losing Steam: The concept of using traditional air cooling for any new, high-density AI cluster is now obsolete. The industry has fully accepted that rack power densities above 50 k W make liquid cooling a non-negotiable, foundational requirement.

The questions your competitors are already asking

This report covers one angle of the commercial race to supply liquid cooling for AI data centers. The questions that matter most depend on your work.

- Which companies are gaining ground in the AI data center liquid cooling market, and which are falling behind?

- Which hyperscalers and AI companies are the primary adopters of these new multi-megawatt liquid cooling solutions?

- What is the status of Supermicro’s 100,000 GPU liquid-cooled cluster for xAI since the initial win?

- What are the performance realities and technical risks of deploying 10 MW CDU systems like those from Liquid Stack and Nautilus at scale?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.